There are desperate people who brave healthcare challenges as they try to make a living by offering manual labour — FE Photo

There are desperate people who brave healthcare challenges as they try to make a living by offering manual labour — FE Photo ![]() The Covid-19 pandemic coupled with the measures employed to fight it has driven the global economy into a deep recession which is the worst ever seen after the Great Depression of the 1930s. More than a million lives have been claimed by the pandemic, and the livelihoods of many million people around the globe have been affected by the recession. During spring of this year, harried nations were seen shutting down public life and economic activities and finding their economies plunging into unprecedented recession. Even after the shutdown measures were ended, economic activities did not return to their normal level. And now, a second wave of the virus has hit many countries - especially in Europe. So, the misery of common people is only going to worsen.

The Covid-19 pandemic coupled with the measures employed to fight it has driven the global economy into a deep recession which is the worst ever seen after the Great Depression of the 1930s. More than a million lives have been claimed by the pandemic, and the livelihoods of many million people around the globe have been affected by the recession. During spring of this year, harried nations were seen shutting down public life and economic activities and finding their economies plunging into unprecedented recession. Even after the shutdown measures were ended, economic activities did not return to their normal level. And now, a second wave of the virus has hit many countries - especially in Europe. So, the misery of common people is only going to worsen.

Loss of jobs is not the only misfortune that has befallen the working people: those who are able to keep their jobs are facing increasingly difficult situations due to a variety of reasons including fall in real wages and shift to precarious contracts.

If policy making for economic recovery were to include protecting the vulnerable people, it would be necessary to understand the mechanisms through which the impact of the Covid pandemic is getting transmitted to the real economy and how livelihoods of the working people are being affected.

The Covid pandemic has hit the economy through different channels

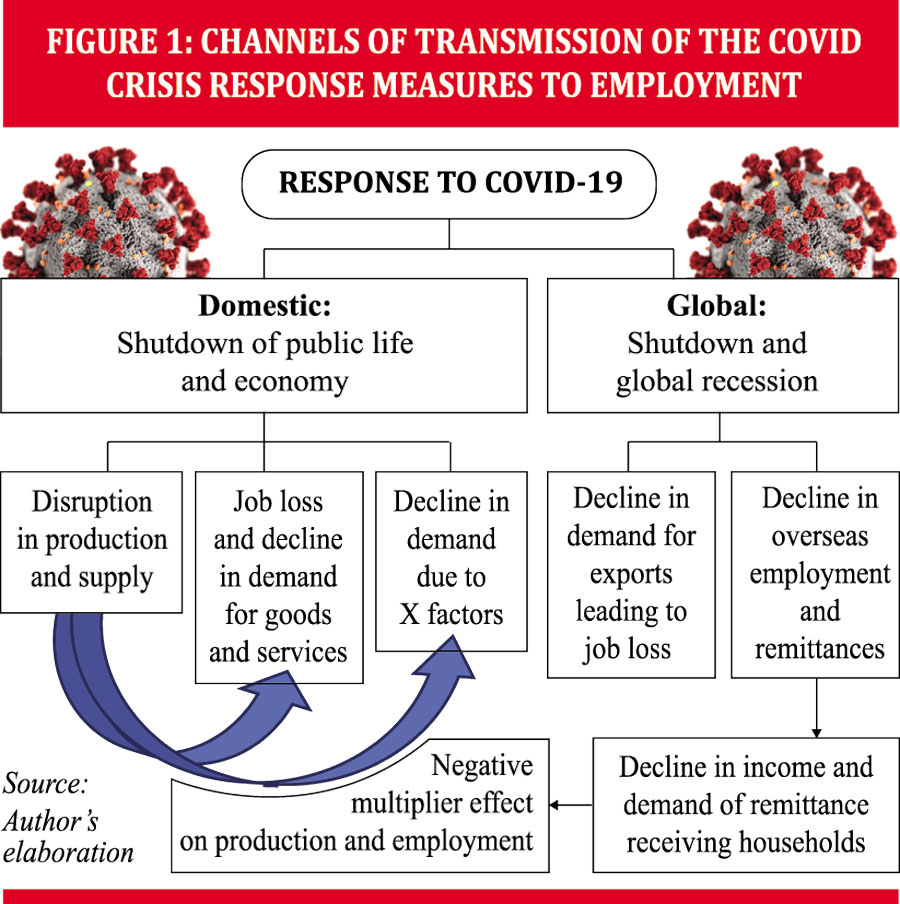

Figure 1 depicts a picture of how the interplay of various factors emanating from the pandemic affected output and employment in the economy. On the domestic front, the lockdown resulted in the stoppage of economic activities, an immediate impact of which was loss of jobs in a wide range of industries and professions. But the situation soon got transformed into a demand shock. With countries closing their borders, putting restrictions on travel, banning public gatherings, airlines stopping flights, and people cancelling their holidays, the demand for a wide range of goods and services was affected. Loss of jobs resulted in loss of incomes, causing an adverse effect on demand.

Restrictions on public life, the fear instilled into the people's collective psyche, and the general sense of uncertainty created by the situation -- factors that may be described as "Xfactors" (see Figure 1) -- also created a negative impact on the demand for goods and services.

Restrictions on public life, the fear instilled into the people's collective psyche, and the general sense of uncertainty created by the situation -- factors that may be described as "Xfactors" (see Figure 1) -- also created a negative impact on the demand for goods and services.

Thus, measures taken to fight the health crisis created a dampening effect on jobs, incomes, and demand for a wide range of goods and services, especially those of manufacturing, construction, trade, transport, recreation, education, personal services, etc. What started as a supply shock soon transformed into a demand shock through the inter-linkages between the markets of goods and services. As the situation evolved and life moved beyond the period of shutdown, the metamorphosis of the supply shock  into a wider crisis for the economy, with both demand and supply interacting on each other, became clearer.

into a wider crisis for the economy, with both demand and supply interacting on each other, became clearer.

On the external front, during the early stage of the pandemic, Bangladesh was facing a bottleneck in its supply chain as it is dependent on China for a variety of goods that are used as raw materials in various industries. Soon, the situation became more complex as the major markets of Bangladesh's export goods -- viz. USA and European countries -- faced recession due to shrinking demand resulting from shutdown in their own countries. As  a result, the suppliers in Bangladesh were confronted with cancellation of orders from buyers. Thus, the economy of Bangladesh was hit by disruption in the demand for export goods, especially ready-made garments.

a result, the suppliers in Bangladesh were confronted with cancellation of orders from buyers. Thus, the economy of Bangladesh was hit by disruption in the demand for export goods, especially ready-made garments.

An additional factor on the external front is overseas employment and remittances sent by those working abroad. Countries that are major employers of workers from Bangladesh, especially those in the Middle East region, have also been hit by the pandemic and went into recession. As a result, they have not only stopped recruiting workers from abroad but also started to send laid-off workers back to their own  countries. Anecdotal evidence, especially media reports, indicate that large numbers of migrant workers have been returning since April.

countries. Anecdotal evidence, especially media reports, indicate that large numbers of migrant workers have been returning since April.

The other side of this adverse effect on a major source of employment is the possibility of a decline in remittances. Although this has not happened yet, the possibility needs to be kept in mind. If remittances start falling, the families of migrant workers may cut down spending on non-essential items, thus causing an adverse effect on demand.

Labour markets adjust to economic crisis in different ways

Although the first mechanism of adjustment to an economic downturn is retrenchment of workers and freeze on recruitment, adjustment can also occur through the price mechanism, i.e., through a fall in real wages. This may happen even if nominal wages/salaries are not reduced, if growth of wages slows down and cannot keep pace with consumer price rise.

Changes may take place in the type of employment, e.g. shift to part-time work, precarious contracts, and other flexible work arrangements.

During economic crises that result from downturn in formal sectors, workers losing jobs may move to the informal sector. But during the Covid pandemic crisis, the informal sector was first hit; and it may seem that this mechanism could not play a role in adjustment. However, as economic activities return to their normal levels, formal sector enterprises may not take back all their workers. So, some may have to look for alternatives; and in a depressed economy, informal sector usually provides the needed refuge.

Reverse migration to rural areas can also be a mechanism for adjustment in the labouir market, although that may dampen wages in agriculture and rural non-farm sectors.

Young people seeking their first jobs may find it more difficult than in normal circumstances. In fact, there may be a whole "lockdown generation" or "pandemic generation" who may experience a difficult start of their working life; and the scar created by that may remain with them for the rest of their life. On the other hand, some of the older people may have to drop out of the labour force prematurely.

How many jobs were lost due to the pandemic-induced economic crisis

Unfortunately, it is not possible to provide a precise answer to this question because there is no official data on this. Data relating to employment and unemployment are usually provided by labour force surveys (LFS) carried out by the Bangladesh Bureau of Statistics (BBS). The latest year for which this survey was carried out is 2016-17. While no regular LFS has been carried out in 2020, a survey titled "RxweKvi Dci aviYv Rwic 2020" was undertaken by BBS in September 2020. But that was very different from the usual household income and expenditure survey or the labour force survey. Considering the method used (telephone rather than personal interview), low response rate (48.48%) and small sample (only 989), this cannot be regarded as a national survey. As an alternative, we have made estimates for job losses by using the data from the survey of 2016-17 as the base and making certain assumptions. Details of the projection methodology and the results are described in a recent paper by the present author.

Before presenting our estimates, two points need to be made. The first is the difference between the situation that prevailed during the period of shutdown (April and May) and the one after restrictions were withdrawn. While all economic activities except for essential services came to a standstill during the former, it was possible to restart them once opening up was allowed. So, the type and magnitude of the impact must have been different during these two periods. Accordingly, separate estimates have been made for the two periods - one for April-May 2020 while the other is for the year 2019-20.

Second, the degree of risk faced by different sectors of the economy varied considerably, with activities in manufacturing, transport, construction and certain services, especially food and accommodation, facing high degrees of risk. Within these sectors, it is the informal type establishments that faced greater risk because their operation remained almost completely suspended during the period of shutdown.

Jobs lost during April-May 2020

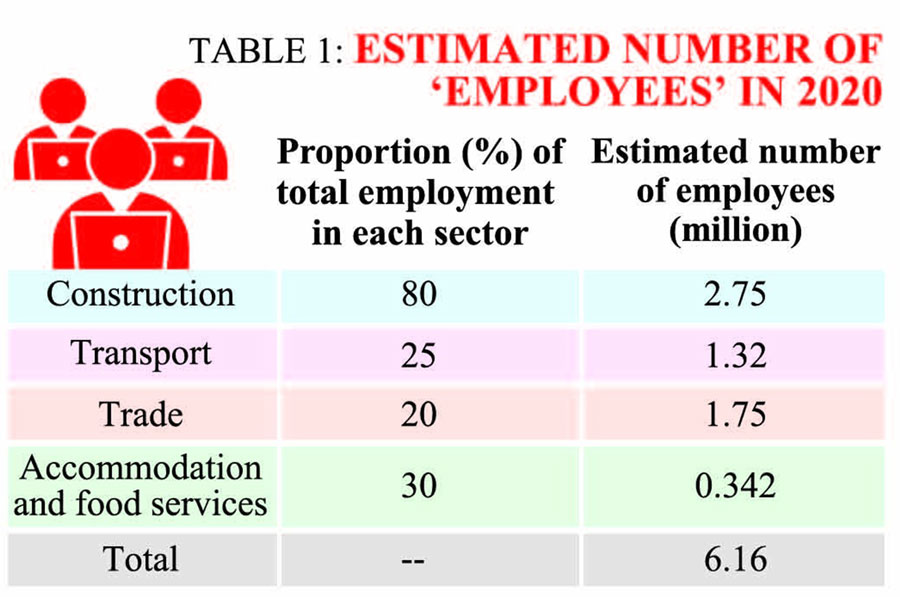

We start by noting that work in most urban economic activities came to a standstill during the shutdown period. So, those who are employed on a daily basis or on precarious contract were without jobs. In the above context, we take note of the numbers engaged as day labourers, e.g., in construction, informal service, and transport as well as the numbers in petty self-employment in retail trade, food service, repairs, etc.

It has been assumed that those engaged in organized manufacturing would be able to go back to their existing jobs and lay-offs will be limited to about ten per cent of their workforce,

Based on data from the 2016-17 labour force survey, following are the projected (for 2020) number of "employees" in selected sectors that are likely to have been hit hardest:

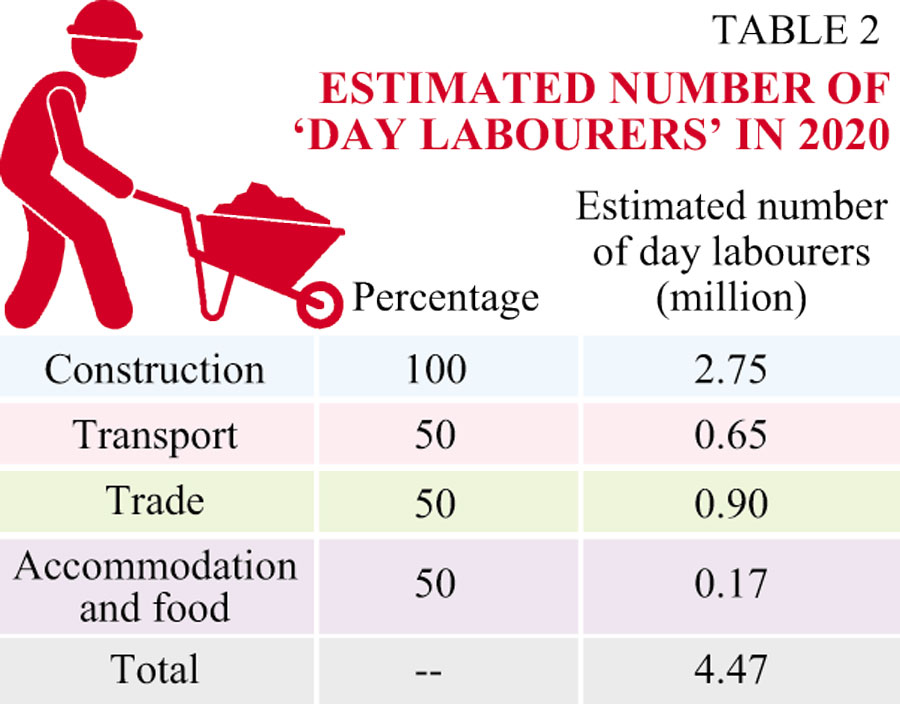

(i) The estimated numbers of "day labourers" (using the proportion of employees from the LFS 2013) are shown in Table 2 (total: 4.47 million):

(ii) The number of the self-employed in urban areas is 6.05 million of which 85% (i.e., 5.19 million) are informally employed.

(iii) Assuming that 10% of those employed in the manufacturing sector have been laid off, the number works out to be about 0.9 million

Based on the above, the total number of workers who may have lost their jobs is estimated as the total of (i) + (ii) + (iii). That gives us: 4.47 + 5.19 + 0.9 = 10.56 (million).

The backlog of unemployed for 2020 was estimated to be three million. Thus, the total number unemployed during the shutdown worked out to be 13.56 million which is about a fifth of the estimated labour force for that year.

Projected unemployment rate for 2019-20

In order to make this projection, use has been made of the relationship between growth of employment and output based on recent data (2010 to 2016-17). Applying this relationship to the GDP growth of 2019-20, total employment for that year has been projected. The difference between the labour force projected for that year and employment projected in the manner described above is the projected unemployment. As a result of the Covid-affected decline in GDP growth, the rate of unemployment was estimated at between 6.74 and 8.71 per cent depending on the growth rate of labour force that is used. Comparing these figures with the unemployment rate of 4.3 per cent in 2016-17, it can be seen that the rate of unemployment may have doubled.

Loss of jobs by major sectors (2019-20)

In order to see the extent of job losses in major sectors, projections have been made of employment in agriculture, manufacturing, construction and services. The main points that emerge from our results can be summarized as follows.

• The total number of jobs lost is likely to exceed 2 million which is 3.14 per cent of total employment under the no-Covid scenario.

• In terms of absolute numbers, the service sector has probably seen the highest number: 1.23 million.

• The manufacturing sector is estimated to have lost over half a million jobs - 5.5 per cent of its estimated employment without Covid.

Loss of jobs in the urban informal sector

The loss of jobs in urban areas is estimated to be 1.25 million which is over 7.0 per cent of the urban employment in 2016-17. In the urban informal sector, the loss is estimated to be 1.08 million which is over 8.0 per cent of the sector's employment in 2016-17.

Loss of jobs in the ready-made garment industry

On this question also, as there is no definite information, possible loss of jobs had to be estimated.

In a press release on 06 June 2020, BGMEA mentioned that in two months (presumably April and May), 348 factories had to close down and the remaining 1926 are operating at much less than full capacity. That implies that although officially workers may not have been laid off, those who were working in the factories that were shut down must have lost their jobs. In fact, in June, national media continued to report layoffs of workers. As there is no official information on these aspects (i.e., closure of factories and workers affected by closures, layoff of workers from factories that are operating), it is difficult to say with confidence how many workers lost jobs. But one can at least draw some inferences from existing figures.

From a study conducted by the Centre for Policy Dialogue (CPD) in 2018, we have the figures on the number of factories - 3,856 and the number of workers - 3.6 million. From these two figures, the average number of workers per factory turns out to be 933. Closure of 348 factories (mentioned in the BGMEA press release referred to above) would then imply that 324,684 workers may have lost their jobs.

An alternative estimate has been made by the present author on the basis of some assumptions. Since the RMG industry is almost entirely export-oriented, a one-to-one correspondence may be expected between exports and production. That would imply that in 2019-20, output also declined by 18 per cent. If the elasticity of employment with respect to output/export growth is assumed to be about 0.55 (estimated using the export and employment growth figures for the period 1999-2000 and 2010-11), export decline of 18.45 per cent can be expected to result in employment decline of about 10 per cent. Depending on whether the base figure is assumed to be 3.6 million or 4.4 million (CPD estimate and BGMEA President's statement respectively), the job loss would be 360,000 or 440,000.

To sum up, the estimates of job loss in the RMG industry during 2019-20 are between 325,000 and 440,000.

Overseas employment

Although the number of people with overseas employment fluctuates from year to year, there has been a general rising trend over time. But after reaching a peak (of more than one million) in 2017, there was a downward trend during 2018 and 2019. The destinations of migrant workers are concentrated in eight countries - Bahrain, Kuwait, Malaysia, Oman, Qatar, Saudi Arabia, Singapore, and UAE. Some of these countries, including Saudi Arabia, have been hit hard by the Covid pandemic and recession; and as a result, have not only stopped recruiting new workers but are also sending a large number of expatriate workers back.

Although there is no data on overseas employment after May of 2020, one can surmise that very few were able to get such jobs. Moreover, periodic media reports indicate that large of number of workers are returning from abroad. Given the global economic situation, it seems that new employment may remain limited till economic recovery starts in the labour-receiving countries. So, it can be assumed that the tap of overseas jobs is unlikely to re-open until about the end of 2020 or early 2021. In that scenario, the number of such jobs for the whole of 2020 is unlikely to be more than two lakhs(the total up to May was 181,218 according to data available on the BMET website). If one takes into account the number that are likely to return because of loss of jobs, the net outflow may turn out to be insignificant. So, the current year (2020) is likely to be a lost year as far as overseas employment is concerned.

What is happening to real wages of workers?

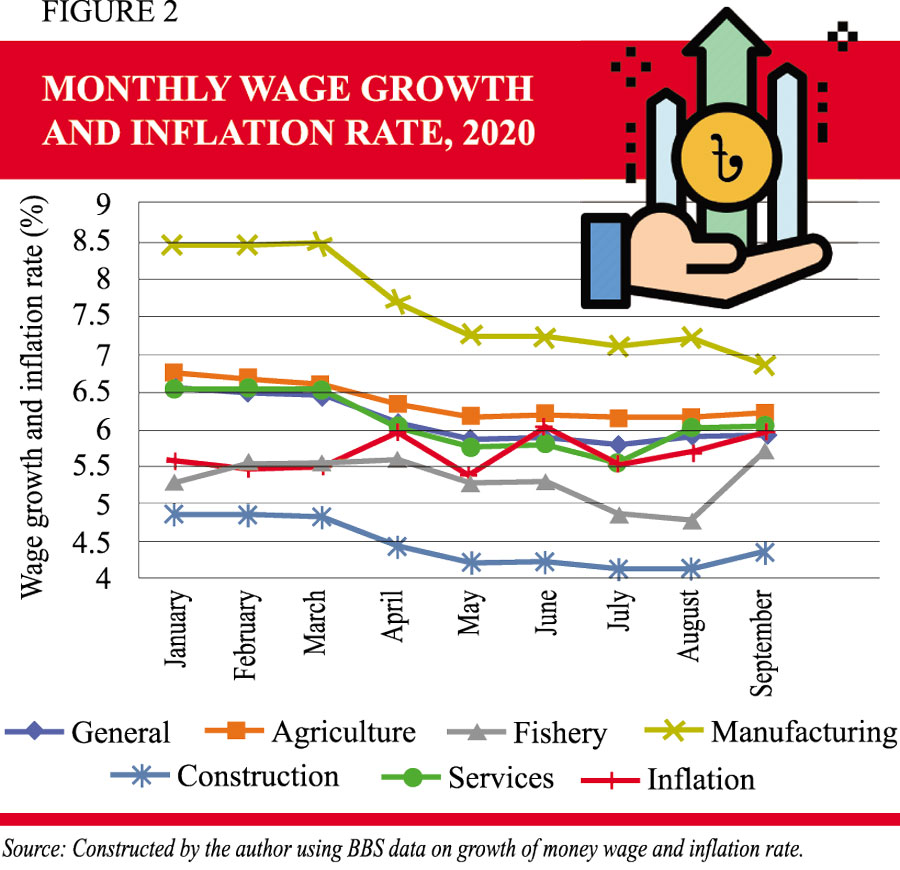

As mentioned already, during an economic downturn, in addition job loss, working people face the possibility of a decline in real wages. Data available from the Bangladesh Bureau of Statistics (BBS) indicates that this may be happening already. Periodic reports of BBS provide data on wage growth and inflation rate on a monthly basis. The data for January to September of 2020 are shown in Figure 2. Several points may be noted on the basis of this data. First, overall wage growth has been declining during this period - with figures for May to September well below those of January to March. Second, the decline is quite sharp for manufacturing. Third, for construction and fishery, the growth rates of money wage rate are well below that of inflation rate (the latter shown by the red line) - thus implying decline in real wages.

It is thus clear that not only were jobs lost, those who were lucky to be in their jobs saw their wages facing downward pressure. The labour market of the country is adjusting to the crisis through both quantity (amount of employment) and price (wage) routes.

Is the labour market recovering?

Recovery in the labour market depends primarily on economic recovery although there is usually a lag in the process. There may be several reasons for such lag, one being the uncertainty in the environment and reluctance on the part of entrepreneurs to start hiring in full swing immediately after the start of recovery. They usually wait and try to feel the pulse of the economy and to understand how durable the recovery is going to be. This may particularly be the case in the current context, because normalcy has not returned either in the domestic or in the external environment. Furthermore, crises normally create opportunities for entrepreneurs to raise efficiency by adopting improved management practices and technology. Those who utilize such opportunities may not hire at the same rate as before the crisis.

Recovery in the labour market depends primarily on economic recovery although there is usually a lag in the process. There may be several reasons for such lag, one being the uncertainty in the environment and reluctance on the part of entrepreneurs to start hiring in full swing immediately after the start of recovery. They usually wait and try to feel the pulse of the economy and to understand how durable the recovery is going to be. This may particularly be the case in the current context, because normalcy has not returned either in the domestic or in the external environment. Furthermore, crises normally create opportunities for entrepreneurs to raise efficiency by adopting improved management practices and technology. Those who utilize such opportunities may not hire at the same rate as before the crisis.

In the absence of up to date data, it is very difficult to understand the extent to which recovery is taking place in the economy. However, based on indicators like credit growth, the index of industrial production, and growth of exports, it is possible to say that there are signs of recovery in the economy - in the form of rise in domestic credit and the return of export growth to positive domain. Of course, growth of credit to the private sector was much lower than to the public sector. And export growth was very small compared to usual growth seen up to the end of 2018. The growth of exports of ready-made garments during the July-September period of 2020 (compared to the corresponding period of 2019) was only 0.85%. Given such tenuous recovery and the continued uncertainty in the global economy (especially with the second wave of coronavirus sweeping across Europe), whether hiring will start at normal pace is a question.

One factor that raises question about the narrow base of the recovery is the very low disbursement rate in the government's economic recovery package earmarked for cottage, micro and small enterprises. This has important implications for recovery in the labour market because outside the ready-made garment industry, such enterprises are a major source of employment. Also, the progress in the disbursement of credit for unemployed youth and returning migrant workers has been very slow.

Of course, those whose living is dependent on a minuscule operation in the informal sector have most likely restarted their operation even if that required loans from informal sources. When a survey question asks them about their current situation, they will probably identify themselves as employed. Whether one should regard that as an indicator of labour market recovery remains a question.

The author, an economist, is former Special Adviser, Employment Sector, International Labour Office, Geneva.

rizwanul.islam49@gmail.com

© 2026 - All Rights with The Financial Express