![]() The Covid-19 pandemic has seriously threatened the lives and livelihoods of all groups of people, especially those of the poor, in Bangladesh. In addition, it has created deep-rooted uncertainties regarding when and how a 'new normal' could be achieved. The pandemic has also generated unprecedented challenges for the microfinance institutions (MFIs), which serve the poor and disadvantaged communities and a large number of cottage, micro, small and medium enterprises (CMSMEs) through their microenterprise operations. Indeed, in view of the nature of the activities of their clients, the MFIs have been severely affected by the ongoing crisis since the operational portfolio of MFIs is overwhelmingly dominated by informal sector activities. These mostly comprise low-return businesses undertaken by the poor borrowers with few resources to cushion the impacts of a crisis, such as the Covid-19 pandemic.

The Covid-19 pandemic has seriously threatened the lives and livelihoods of all groups of people, especially those of the poor, in Bangladesh. In addition, it has created deep-rooted uncertainties regarding when and how a 'new normal' could be achieved. The pandemic has also generated unprecedented challenges for the microfinance institutions (MFIs), which serve the poor and disadvantaged communities and a large number of cottage, micro, small and medium enterprises (CMSMEs) through their microenterprise operations. Indeed, in view of the nature of the activities of their clients, the MFIs have been severely affected by the ongoing crisis since the operational portfolio of MFIs is overwhelmingly dominated by informal sector activities. These mostly comprise low-return businesses undertaken by the poor borrowers with few resources to cushion the impacts of a crisis, such as the Covid-19 pandemic.

The MFI members generally save very little; and invest their meagre resources (including their borrowings from the MFIs) in small scale livelihood activities. Most of these borrowers and microentrepreneurs rely on their daily incomes for meeting basic survival needs. In reality, any dislocation of their daily activities, such as the lockdown and supply chain disruptions during the present pandemic, means that they are unlikely to pay for food, healthcare and other basic necessities for themselves and their families. Also, the coverage of the government's assistance package is mostly limited and does not provide access to many of these deprived populations. Further, the distribution of even the limited food/cash assistance is often disrupted by the lockdown measures, especially when the cash assistance cannot be distributed using electronic money.

Since the beginning of the pandemic in March 2020, the resilience and commitment to support their members are evident for all MFIs in the country. The MFIs have taken measures on their own to set up specific support mechanisms for their members to ensure stability of their income-generating activities (IGAs). These measures include, for example, support for the members to cope with the impact of the pandemic based on ground realities, such as deferring the repayment of loan maturities on a case-by-case basis and offering credit refinancing for members operating in sectors affected by the Covid-19 crisis. Many MFIs have also undertaken awareness-raising campaigns on basic protective measures for their employees and members. Others have adopted digital transfer systems which limit contacts.

Since the beginning of the pandemic in March 2020, the resilience and commitment to support their members are evident for all MFIs in the country. The MFIs have taken measures on their own to set up specific support mechanisms for their members to ensure stability of their income-generating activities (IGAs). These measures include, for example, support for the members to cope with the impact of the pandemic based on ground realities, such as deferring the repayment of loan maturities on a case-by-case basis and offering credit refinancing for members operating in sectors affected by the Covid-19 crisis. Many MFIs have also undertaken awareness-raising campaigns on basic protective measures for their employees and members. Others have adopted digital transfer systems which limit contacts.

Microfinance in Bangladesh

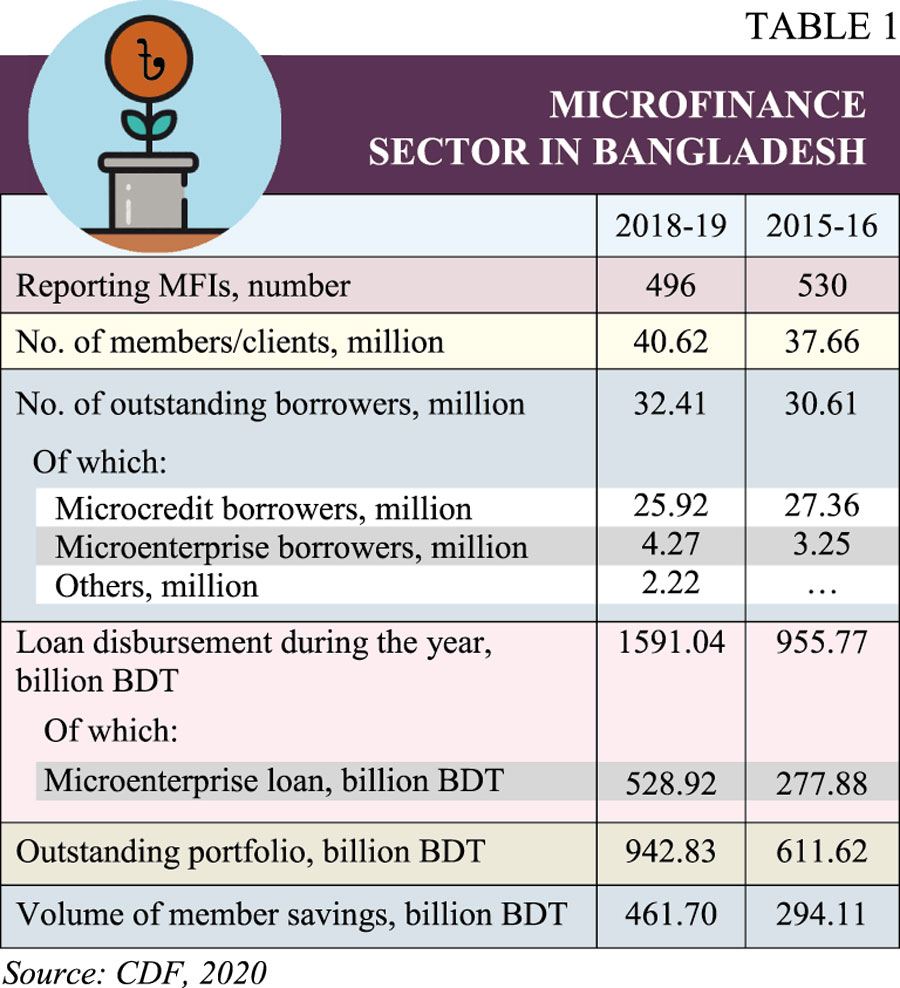

The MFIs in Bangladesh provide savings, credit and other financial and human development services to more than 32 million low income members/microenterprises having a total of outstanding loans of nearly BDT 943 billion and a savings portfolio of about BDT 462 billion in 2019 (Table 1). Credit services of the microfinance sector are categorised into six groups: (i) general microcredit for small-scale self-employment based activities; (ii) microenterprise loans; (iii) loans for the ultra-poor; (iv) agricultural loans; (v) seasonal loans; and (vi) loans for disaster management. A loan amount up to BDT 50,000 is generally considered as microcredit; while loans above the amount are taken as microenterprise loans. Moreover, nearly 92 per cent of the microfinance members are women and around 65 per cent of the microfinance operations take place in the rural areas.

The MFIs in Bangladesh provide savings, credit and other financial and human development services to more than 32 million low income members/microenterprises having a total of outstanding loans of nearly BDT 943 billion and a savings portfolio of about BDT 462 billion in 2019 (Table 1). Credit services of the microfinance sector are categorised into six groups: (i) general microcredit for small-scale self-employment based activities; (ii) microenterprise loans; (iii) loans for the ultra-poor; (iv) agricultural loans; (v) seasonal loans; and (vi) loans for disaster management. A loan amount up to BDT 50,000 is generally considered as microcredit; while loans above the amount are taken as microenterprise loans. Moreover, nearly 92 per cent of the microfinance members are women and around 65 per cent of the microfinance operations take place in the rural areas.

As of June 2018, the total number of licensed MFIs (by the regulatory authority, Microcredit Regulatory Authority, MRA) is 805 with more than 18,000 branches and 154,000 employees. The concentration ratio of the microfinance sector is relatively high in Bangladesh with the two largest MFIs (BRAC and ASA) contributing around 50 per cent of total outstanding loans and savings of the microfinance sector. They each serve over four million microfinance borrowers. Overall, 20 largest MFIs control nearly three-quarters of the market share; while the two largest MFIs have control over half in terms of both clients and total financial portfolios.

Over the years, the microfinance sector in Bangladesh has changed rapidly along with significant transformations from group-based limited-scale microcredit operations to individual microenterprise operations in order to create widespread and sustainable development impacts. Throughout these years, microcredit has graduated from its mainstream activity of supporting basic needs of the poor people to nurturing broader farm and nonfarm activities and microenterprises of the graduating microcredit borrowers and the microentrepreneurs. The focus on 'appropriate' finance through scaling up credit to meet threshold level of activities for generating sustainable livelihoods--along with targeting the extreme poor groups and the remote areas; mobilising the poor for promoting social development; creating awareness on health, education, women's empowerment and other social issues; providing access to technologies and decent income earning opportunities - has given the MFIs a unique opportunity to emerge as important partners of development in Bangladesh, particularly during difficult times, such as the present pandemic.

In Bangladesh, many poor people and micro-entrepreneurs rely on various financial services offered by the MFIs including credit, savings, remittance transfer, loan insurance etc.; most of whom were financially excluded prior to their involvement in the microfinance sector. These transformations have also induced the MFIs to supplement their internally-generated funds (e.g. members' savings) with commercial and other sources (e.g. borrowings from the banks).

As a result, the source of financing of MFIs' operations has broadened over time to include loanable funds from several sources, such as savings collected from the members, cumulative net surplus, borrowing from the commercial banks, concessional loans received from different sources such as the Palli Karma-Sahayak Foundation (PKSF), loans from local large MFIs, loans from non-institutional sources (e.g. board and client members), and other sources such as reserve fund, staff security fund, loan loss provision fund and others e.g. funds from donors, government sources, welfare fund, depreciation fund, and emergency fund. Overall, the most important source of fund for the MFIs at the aggregate level is savings of their members/clients (nearly 43 per cent) followed by cumulative net surplus (about 31 per cent) and borrowings from banks (19 per cent). In addition, subsidised loans from the microfinance wholesale funding agency, PKSF, is a major source of loan fund for the PKSF's partner organisations (POs) while the remaining ones are relatively minor sources.

Over the years, the MFIs have contributed much towards expanding access of the poor and low-income households to microfinance services in the country. In Bangladesh, microfinance to the poor (especially poor women) for undertaking IGAs is widely treated as virtuous and is seen by many as valuable in the country's poverty reduction efforts. It is also argued that microfinance is a relatively efficient means for assisting the poor. These views, however, have not gone unchallenged. Although the interest rates on micro-loans are relatively high, this is seen as a positive mechanism for rationing the limited volume of microfinance available to the borrowers who can earn sufficient returns to cover the costs. In practice, this self-selection process is far from perfect; because the poor may borrow in desperation and become locked into a vicious cycle of indebtedness. There may exist moral hazard problems as well.

While the controversy about the effectiveness of microfinance in poverty reduction in Bangladesh is deep, an adequate assessment of the capacity of microfinance to reduce poverty needs to employ an economy-wide framework. Although microfinance can provide some short term relief from poverty, it is probably not a long term solution for poverty, especially in situations where the poor households own small amounts of land or other productive assets. In modern agriculture, there exist strong positive economies of scale which small farms are unlikely to tap to the required extent and benefit in the longer term. The nonfarm economic opportunities may also remain limited in the absence of strong overall economic growth and technological innovations.

A more important aspect of microfinance, however, is its role in increasing the status of women and their bargaining power in the family as most micro-loans are given to women in Bangladesh. Although there exists counter-evidence that increased access to microfinance does not necessarily improve the health and educational status of women, nor increase the availability of consumer goods to them, and fails to enhance their role in decision making within the household, these results may be context-specific, situational, and dependent on the nature of the patriarchy in society. If men have strong control over all finances in the household, micro-loans can do little to empower women. The overall picture in Bangladesh's society is, however, more positive, where many women have been empowered and became successful microentrepreneurs through using microcredit as their stepping stone.

Moreover, in the context of financial inclusion, the MFIs need to work in designing new and innovative financial products and services with terms and conditions more suitable for the vulnerable and risk-averse groups of poor households. Probably, these financial products and services need to give more emphasis of creating multiple income sources, accumulating productive assets and adopting risk minimising techniques (e.g. microinsurance) for the risk averter and vulnerable left-out poor households. Evidently, the need is to identify the constraints against expanding MFI services more to the relatively vulnerable and less accessible areas and to more vulnerable and low-income households and work together with other stakeholders to remove these constraints. The use of technology like mobile banking, on-line banking and ATMs may provide new avenues to reduce risks for both lenders and borrowers in less accessible areas. Along with appropriate supply side policies, demand side interventions are also necessary to ensure that the poor and low-income households are financially literate with ability to use the services productively and efficiently.

The MFIs and Covid-19

In Bangladesh, microfinance allows the poor and disadvantaged people excluded from the traditional banking sector to access financial services, generally tailored to their needs. In particular, micro-individual and micro-enterprise loans support the income-generating activities of these poor households. Yet, the Covid-19 pandemic has led to significant disruptions to the activities of the microfinance sector.

On the other hand, for the MFIs, the Covid-19 crisis has led many to close down their branches, change their work modality and reduce their contact with the members. The MFIs, like their members, have thus been directly affected by the crisis. Although most MFIs have taken rapid action to avoid a liquidity crisis, but the sector needs external support especially to address the increase in loan demand when the economic activities gradually resume, as has been happening at present. Many MFIs have managed to adapt to the impacts of the crisis to ensure the continuity of services. Some have adopted teleworking to allow their staff to continue their essential operations including the provision of emergency loans to highly-affected clients to overcome their serious liquidity problems.

In practice, most MFIs are on the front line in the response to the impacts of the Covid-19 pandemic. No doubt, this is a responsible and necessary reaction on the part of the MFIs-- social organisations having a rich tradition of serving the poor and disadvantaged especially during any crisis. The overarching virtue of the MFIs in Bangladesh is that they not only deliver financial and development services tailored to the need of the country's poor and the poorest, they do so in a sustainable manner. During this Covid-19 devastation, the MFIs are again working to face the challenge of safeguarding the restoration and financial empowerment of their vulnerable members excluded from the formal support mechanisms.

Innovation Drivers for MFIs in Post-Covid-19 Period

The MFIs have already emerged as major players in providing financial services to the poor and disadvantaged in Bangladesh. More than 30 million individuals exist under the microfinance network and about 2.0 million small businesses are lateral entrants into the MFIs' credit network. Most of these clients are parts of the 'missing middle' in the formal bank credit market. Over time, the horizon of MFIs has also expanded; micro loan products have been diversified to include both financial and non-financial products.

Moreover, the regulations of MFIs have contributed to a structural shift in the microcredit market, signifying a move towards microenterprise-based higher loan size creating an intense competition for loans between microenterprises and traditional household-based activities. On the other hand, with emphasis on sustainability, the MFIs have also targeted their activities with a renewed focus on transaction costs and risk minimising approaches. On the other hand, the coverage of the poor members under the MFI financial network has been facilitated by the availability of subsidised fund, institution of risk minimising informal microinsurance (e.g. credit life insurance, livestock insurance, health insurance) and programme-induced and targeted lending activities. However, the shift towards microenterprises-based lending activities has perhaps affected the loan portfolio of the extreme and moderate vulnerable poor households at least to a certain extent.

At present, there are three major targeted clientele groups of the MFIs: (i) the vulnerable poor including extreme poor and moderate poor; (ii) graduating microcredit members; and (iii) lateral entrants of small businesses e.g. microentrepreneurs. This has also led the MFIs to adopt two major mechanisms to deliver financial services to the clients: (a) relationship-based lending to individual microentrepreneurs and small businesses; and (b) group-based lending under which several small borrowers come together to apply for loans and other services as a group. The group-based model represents an approach under which the poor and near-poor households can have access to an appropriate range of financial services, including not just credit but also savings, microinsurance, and fund transfers.

Some evidences show that, for the MFIs, the default rate is higher in relationship-based microenterprise lending than in group-based lending. Moreover, as the average size of the microenterprise (ME) loan is much higher than the group-based loan, even a low default rate of ME loan causes a bigger liquidity constraint for the MFIs. On the other hand, net return is higher for ME loans as these loans generally have low administrative and supervision costs. Thus, there is a dilemma; and the need for MFIs is to strike a right balance between the two types of loans and minimise the risks of ME loan default. Further, while meeting the demand of the ME clientele groups comprising the 'missing middle' no doubt is important, bringing the excluded vulnerable and extreme poor households is also the key to fulfilling their social mission.

In short, the operational characteristics of the microfinance market in Bangladesh show that: (i) about 58 per cent of the extreme poor households still do not have access to microfinance market; (ii) around 53 per cent of the moderate poor do not access financial services of the MFIs; (iii) women-headed households have lower access to microfinance services; and (iv) there seems to exist a recent trend of rising flow of credit to the non-poor households who are graduating members and lateral entrants belonging to small and micro businesses.

Considering these realities, three aspects of the financial operations of the MFIs need attention in the post Covid-19 period: (i) explore innovative and sustainable measures to ease the binding financial constraints to provide financial services to the target population/business groups; (ii) develop appropriate financial products/services(including housing, business scaling-up and enterprise development, technology adoption, and emergency loan products) to meet the needs of different groups of excluded poor households/microbusinesses; and (iii) ensure more efficient and cost-effective MFI operations through adoption of digital and modern technologies and resolve the asymmetric information problem of the excluded households/enterprises. In addition, capacity building of the MFIs needs to be prioritised to meet the demand of different segments of the targeted populations through addressing problems like lack of skilled and trained staff; inaccessibility to haor, hilly and remote areas; limited access to technology and information; inadequate information flows to the excluded households/enterprises; and limited financial education to manage financial resources in a more productive and efficient manner.

The innovation drivers of MFIs during the post-Covid-19 period should encompass both push and pull factors. The push factors will come from external sources outside the microfinance sector that will motivate the MFIs to develop innovative financial products and services to expand outreach to currently excluded and low-income groups. Internal factors will act as the pull forces which will come from within the MFIs encouraging them to develop internal capacities for delivering better-suited and efficient services to these groups.

The most important push factor will be the government's determination to rejuvenate the financial sector to overcome the deep scars of the pandemic and make the sector more inclusive. In this context, the MFIs may follow a three-pronged approach: (i) expand the capacity and enhance the confidence of the potential customers regarding efficient delivery of tailored financial products and services; (ii) provide information and education on access and use of digital financial instruments by the microfinance sector; and (iii) encourage the delivery of a variety of products and services using digital and more efficient mechanisms in line with the need and demand of different target groups.

In the post-Covid-19 world, the priority for the MFIs would be to provide their services in more efficient and sustainable ways facilitated by a better understanding of local communities, innovative service design and delivery models, and lending techniques. Further, new innovations may also be explored in the existing MFI models. For example, the MFIs may explore the feasibility of developing partnerships with other financial service providers (e.g. agent banking and e-money agents, local cooperative associations and other local level institutions) for performing some of their activities e.g. accepting repayment instalments and micro-savings, releasing micro-loans to microcredit/microenterprise borrowers, providing microinsurance and other services through creating access points of financial services in locations where the MFI branches are not available.

The MFIs may also explore several options to enhance their activities to meet the challenges of the post-coronavirus period: (i) build a long-term relationship with the banks for supply of funds for lending; (ii) design new and digital financial products/services particularly long term housing loans and multiple loans including emergency loans and risk minimising microinsurance products; (iii) implement human resource development programmes both through training of existing staff and recruiting adequately skilled personnel especially in digital technologies; (iv) enhance security of funds especially less accessible areas; (v) ensure access to information technology for complete documentation of members and borrowers using information from the credit information bureau for the microfinance sector; (vi) use right skills and information for selecting borrowers/microenterprises and providing services; and (vii) explore options to mobilise voluntary and term deposits.

At present, the MFIs depend on several sources of fund for their operations, such as member savings, cumulative net surplus, borrowings from banks and PKSF, and others. Thus, the MFIs use both 'own sources' and 'other sources' for conducting their loan and other operations. And, there are obvious advantages and disadvantages in regard to using own sources or other sources. Using 'own sources' offers advantages to the MFIs in the form of 'quick disbursement', 'flexibility in terms and conditions' and 'flexibility and control'. However, higher profit margin or greater cost of funds is a key challenge for using 'own funds' for such financing. There exists a common perception that higher monitoring cost in MFI operations cannot be covered through a lower profit margin. There are instances of using other sources of funds like PKSF, donor or government's soft funds by the MFIs. Generally, the use of the 'other sources' offers advantages to the MFIs in the form of 'availability of low cost of fund'. However, a complex set of formalities, terms and conditions, and the time consuming nature of the process are amongst the challenges that the MFIs face.

At the operational or retail level, the MFIs usually follow the single mode for delivering credit to their borrowers, that is loans are directly disbursed to the borrowers which may be termed as 'direct lending' instead of 'linkage lending' under which loans are channelled to the borrowers through other institutions. The MFIs mostly use their own funds (e.g. member savings and cumulative net surplus) through direct lending. The mode has benefits as well as advantages and disadvantages. The 'direct lending mode' offers advantages in the form of 'quick disbursement' and 'direct monitoring'. However, the high cost of fund and high monitoring cost are the key challenges of this mode for the MFIs. On the other hand, the 'linkage lending mode' offers advantages to the banks through accessing local level microfinance operations with the help of the MFIs.

However, other support services are not included with the micro-loan product of the banks. As is well known, for the MFIs, microfinance is not just providing adequate and timely credit to the poor borrowers, it is a package in which the required amount of credit is integrated with inputs/services for broader wellbeing of the poor and disadvantaged, such as sustainable livelihood, health and nutrition, education, women's empowerment, community development, training and skill building, and entrepreneurship development (e.g. the credit-plus-plus approach). Moreover, many green products like solar home system (SHS), solar irrigation, organic farming, afforestation, and other sustainable and climate resilient services are often integrated within the MFI packages.

Advantages of Digital Route for MFIs

For adapting to the post-Covid-19 landscape, the key option for the MFIs will be to take the digital transformation route. With rapid development in digital transformation of the financial sector itself, this is inevitable for the MFIs as well. Digital financial services (DFS) refer to digital access to and use of financial services by the excluded and underserved populations. For the purpose, such services should be suited to the customers' needs, and delivered responsibly, at a cost both affordable to the customers and sustainable for the providers. There are three key components of DFS: (i) a digital transactional platform, (ii) retail agents, and (iii) use by customers and agents of a device - most commonly a mobile phone - to transact via the platform.

The DFS presents a unique opportunity for the MFIs to improve service delivery, enhance transparency and accountability, increase operational efficiencies and reduce costs of operation. Delivering financial services through technological innovations, including mobile money, can be a catalyst for the provision and use of a diverse set of other financial services by the MFIs. Those who are now excluded can enjoy expanded access to money-transfer, microsavings, and microinsurance services. For the microentrepreneurs, the adoption of DFS by the MFIs, along with providing efficient access to finance, can create opportunities to adopt electronic payment systems, secure a varied menu of financial products and a chance to build a financial history. Innovations in electronic payment technology like mobile and prepaid services will enable the MFI members to lead more secure, empowered and included lives.

For the CMSMEs, the adoption of digital technologies by the MFIs can help address specific challenges in the value chain - especially those that need financial services solutions, and where traditional finance has limitations to fully address the demand in the rural market. This is often due to high infrastructure costs and a lack of incentives to adapt products to the unique needs of these enterprises. Digital finance also offers a way to expand access to the formal financial system (e.g. through a basic transaction account supervised by the regulators), taking advantage of the rapid growth of digital and mobile telephone infrastructure and the advent of agent banking. These factors have a direct link to increasing the microentrepreneurs' income and wellbeing. The benefits of digital transformation of the MFIs are many including:

• Access to digital financial services empowers the MFI members in multiple ways. The intake of different financial services typically expands over time as the customers gain familiarity with and trust in the digital transactional platform.

• Typically, lower costs of digital transactional platforms, both to the MFIs and the customers, allow the members to transact locally in more frequent and tiny amounts, helping them manage their uneven income and expenses.

• Additional financial services tailored to the members' needs and financial circumstances are possible for the MFIs through the payment, transfer, and value storage services embedded in the digital transaction platform itself and the data generated within it.

• The MFIs can reduce risks of loss, theft, and other financial crimes posed by cash-based transactions as well as reduced costs relative to transactions in cash.

• Digital transformation can also promote economic empowerment by enabling asset accumulation especially for women, thereby increasing their economic participation and welfare.

Obviously, there could also be different types of risks that the MFIs may encounter due to digital transformation, such as novelty risks for the members resulting from their lack of familiarity with the digital products and services creating vulnerability to exploitation and abuse; agent-related risks due to offering of services by the new providers which may not be subjected to consumer protection provisions; and digital technology-related risks which can cause disrupted services and loss of data, including payment instructions (e.g. due to dropped messages) as well as the risk of privacy or security breach resulting from digital transmittal and storage of data. Nevertheless, customer uptake of digital financial services in different markets suggests that on balance these risks do not outweigh the benefits of being financially included, especially in the presence of appropriate regulation and supervision.

Designing Digital Business Models for MFIs

Business models, to a large extent, determine the costs incurred to deliver financial products/services on the one hand and the value generated on a sustainable basis, on the other. This in turn determines whether the provision of financial products and services will be sustainable or not. As such, designing efficient business models is a key determinant of successful delivery of financial services by the MFIs. It also needs to be recognised that business models are inspired and motivated by various factors. Usually, the MFIs adopt diverse strategic approaches to product development, including roll-out and scale-up. The key for the MFIs would be to adopt pragmatic approaches towards developing business models recognising both operational, regulatory and policy challenges as well as practical difficulties of reaching out to the customers.

One of the key concerns for developing business models of the MFIs is the challenges that emerge from traditional small transactions, completing paperwork, providing outreach and others. For the MFIs, the microfinance value chain involves multiple players which allow several business model alternatives. In fact, the MFIs can potentially emerge as intermediaries with a significant value proposition to their client base, extending financial products through their existing infrastructure in remote rural areas. However, designing business models will have to address several challenges such as, lack of investment capital, low system efficiencies, difficulties in scaling IT and operating models, and demand for resource intensive processes.

Overall, the key concerns will be to satisfactorily resolve several existing challenges e.g. operating models are not designed for low-income sector/clients; IT solutions are not appropriate; persistence of limited infrastructure; frequently changing regulatory environments; little/no financial history of low-income clients; and high cost of traditional channels.

Since the microcredit revolution in the 1970s, the MFIs have been successfully providing credit and other financial services to the poor households without any collateral and third party guarantee. A major factor behind the success is that the microloans are provided under intensive monitoring mechanisms along with appropriate incentive structures. Although high transaction costs (resulting in relatively high lending rates) are one of the major criticisms of the MFI operations, there exists scope to reduce such costs especially through digital transformation. In addition, the transaction costs may be reduced through adopting a number of supply side actions, such as improving efficiency of the MFI operations through innovation in loan production technology e.g. minimising the waiting period for loan sanctioning and focusing on better governance so that efficiency is increased and unnecessary transaction cost is reduced for the borrowers. In all these respects, digital transformation can play a major role.

For successful digitalisation, the MFIs must resolve a number of difficult issues prior to moving towards creating an inclusive digital landscape, such as where to start, how to judge the readiness of a particular MFI to undergo digital transformation, what challenges and risks should be considered before embarking on the transformation routes, and similar issues.

In practice, digital lending (and other operations) can be a powerful force for enhancing the efficiency of operations for the MFIs just like other financial service providers (FSPs). The rapid innovations in digital financial operations will enable the MFIs to offer better financial products to more underserved customers in faster, more cost-efficient and inclusive ways. The government and the regulators are also working to create a more enabling landscape and providing incentives to adopt innovative digital models to provide quality financial services especially to the underserved communities (e.g. the poor and marginalised; and women) and the CMSMEs who are the clients of the MFIs.

In the developing world, many MFIs have undergone digital transformation successfully enabling them to evolve, scale, and compete more efficiently in the rapidly-changing financial landscape. The expectations of the customers are also changing rapidly which are increasingly being shaped by their experience with smartphone apps, fintechs, and the social media. For the MFIs, digitising operations will no doubt emerge in the coming years as one of the most credible ways to meet the changing expectations of their customers in Bangladesh.

In reality, realising the vision of a fully-integrated digital operation model needs a successful navigation by the MFIs to complete the necessary institutional transformation. Moreover, since the MFIs belong to different size categories, have different levels of institutional maturity, and are guided by their own specific mandates, a 'one-size-fits-all' menu is unlikely to be applicable to all MFIs in the country. Moreover, each MFI faces a unique set of challenges to its operation. However, the key issue for the MFIs is to adopt the right mindset and the most appropriate digitisation process. The 'right' level of digitisation is also likely to vary depending on a number of factors, such as adopted objectives of digital transformation, existing level of maturity of digital transformation, and similar other considerations. The MFIs should take these and related aspects into consideration to place the institutions strategically for meeting future challenges and adopt the 'right' type of digital transformation to better respond to client needs and preferences.

In reality, it is true that not all MFIs in Bangladesh are ready to digitise to the same extent or at the same speed. The need for MFIs is to prioritise the processes for digital transformation based on their current and desired level of digital maturity. Based on available best practices, a framework may be used to deepen the understanding of digital transformation by specific MFIs, identify digital transformation objectives and maturity for adoption, and take the steps towards adopting successful digital transformation.

One can identify several key issues in taking the right decisions:

• Choose the right approach to digital transformation: There exist many approaches and a growing literature of case studies and toolkits are available to help explore which would work best for a specific MFI. For Bangladesh, technology options have been explored and key pillars have been suggested for digital transformation of the MFIs (see for example, UNCDF, 2019). It is likely that a number of key benefits can result even from small operational improvements through adopting digital approaches. Moreover, guidance on cultural and interpersonal aspects of the digitisation process for the MFIs, case studies, market overviews, industry opinion and research focused on multiple aspects of digital financial services, including strategy, selecting the right technology, agent networks, customer acquisition and data analytics are available from different developing countries to draw informed conclusions for charting out the most appropriate process in Bangladesh. For choosing the right model for the digital journey, six different toolkits--each focused on a different business model-are also available to integrate digital channels into the service delivery approaches of MFIs.

• Forge partnership between MFIs and fintechs: Such partnerships can play an important role in enabling the access to financial services by the MFIs through offering, among others, more choices to the customers and expanding outreach to the excluded people. Such partnership also drives institutional-level innovation and helps MFIs to remain efficient.

• Secure the right balance between technology and human touch: During the digitisation journey, this is the key to acquiring and retaining the customers. Depending on the nature of the market, all MFI customers may not be prepared to get involved in fully digital financial products or services due to inertia, perceived lack of trust in digital provision or discomfort in using a new technology. For success in digitising, the MFIs will have to strike a right balance between technology and human touch especially to accommodate the'technology-shy' customers.

• Keep pace between digital transformation and required regulatory changes: For mitigating the digital risks, digital transformation of MFIs should keep pace with the regulatory framework governing the MFI activities. For accelerating the transformation, successful collaboration between the MFIs, digital financial service providers and fintechs is necessary.

• Secure clear guidance on digitisation: To begin with, the MFIs should seek strategic guidance from the management and the required financial and human resources to successfully navigate the fintech revolution and clearly identify the key challenges and opportunities.

• Include AI in long-term strategy: The MFIs should incorporate Artificial Intelligence (AI) as part of their long-term strategy for digital transformation. This is necessary to reduce the costs, manage the risks, and gain a competitive edge in the long run.

Concluding Remarks

Over the years, the MFIs in Bangladesh have created their unique space as important intermediaries with a significant value proposition to their client base and extending financial products to the remote areas through their widespread network and infrastructure. The MFIs have also gained experience in providing financial services to low income and rural populations and have acquired several strengths, such as ready access to an established client base, experience in cash management, established internal audit and monitoring systems, experienced field staff and local branches, client insights for new product development, and experience in client relationship management.

Despite significant positive achievements, the challenge for the MFIs is their high transaction costs -- large volume of resources traditionally needed to support a large number of small transactions resulting in high costs with low returns per transaction as a unique feature of their operations. For overcoming the challenge, the adoption of digital technology is a major enabler which is proven, scalable, secure, cost-effective, and is likely to be sustainable.

Although Bangladesh still has a long way to go to take the full advantages of digital finance, the country is moving rapidly to build the required ecosystems and remove the barriers to ensure the progression from payments to solutions 'beyond payments'. An enabling policy and regulatory environment have been created including mobile financial services, agent/branchless banking, electronic money, digital payment solutions and other new technologies. Although a large section of the population still remains excluded from the digital economy, the ecosystem has tremendous potential to expand access to affordable financial services to all populations. For exploiting the digital technology both effectively and efficiently, key issues for the MFIs will be to ensure that:

• Financial services are tailored to the specific needs of different groups of their customers; are transparent and secure; and provide optimal balance between different features of the products and their prices.

• Digital financial services are introduced through adopting well-sequenced and well-coordinated policies to nurture in-house technological innovation and ensure that financial operations become more efficient and diversified.

• For harnessing the widespread transformative power of the digital technology, the MFIs should identify both opportunities and challenges; such as that the management is prepared for both rewards and risks of digitising financial services and reaching out to the members of the financially excluded groups.

• In digitising financial services, the MFIs should place emphasis on designing customer-centric financial products and services especially suited to the need of low-income and financially excluded individuals and enterprises.

For the MFIs, the adoption of the customer-centric approach will be instrumental in bridging the access-usage gap in digital technologies. The MFIs need to acknowledge that although more than 90 per cent of the MFI borrowers are women, only 18 per cent of the digital finance users are women. This shows the existence of a significant gender divide in access to digital financial services which has strong repercussions on the uptake of digital technology by the MFI members. On the positive side, although smart phone penetration is still relatively low, it is rapidly gaining ground. Smart phones provide an important opportunity to improve user interfaces and address literacy barriers across all customers. However, the important aspect for the providers would be to develop responsive products meeting the women's needs, potentially working in partnership with the MFIs who have learned so much about serving women in large numbers.

For the poor in Bangladesh, the need is to provide them with access to 'financial services' that can safeguard these vulnerable households from the economic and natural shocks. For the purpose, conventional financial products should be re-designed to reflect the requirements needed by the poor. Along with exploiting potential of the digital technology, this requires the development of simple and affordable financial tools which can act as cushion during times of need. And MFIs are the most suited institutions to serve the poor more effectively through adopting the digital technologies. The MFIs, with fully developed DFS operations, can further reduce barriers of physical access and cost and, over time, would enable a much higher proportion of the population to use all basic financial services through product innovations and other developments.

For the MFIs, digital transformation also creates new scope for adopting innovative technologies like mobile-phone-enabled solutions, electronic money models, and digital payment platforms along with drastic reduction of costs for both the MFIs and their customers. With rapid financial developments currently happening in Bangladesh, digitisation of financial services and its convergence with microfinance are inevitable in which digital credit is likely to have the key focus. The post-Covid-19 era will give the MFIs an opportunity to embrace digital transformation and enhance their capacity and knowledge to keep pace with rapid developments in technology and digital financial services through building interfaces with their microfinance operations.

Mustafa K Mujeri is Executive Director of the Institute for Inclusive Finance and Development (InM), Dhaka

Email: mujeri@gmail.com

© 2026 - All Rights with The Financial Express