Khaled Mahmud Raihan and Mohammad Jasim Uddin | November 23, 2020 00:00:00

![]() Sukuk, an Islamic equivalent of bonds, is a certificate representing ownership in tangible assets or the assets of particular project or special investment activity. As opposed to conventional bonds, which merely confer ownership of a debt, Sukuk grants the investor a share of an asset, along with commensurate cash flows and risk.

Sukuk, an Islamic equivalent of bonds, is a certificate representing ownership in tangible assets or the assets of particular project or special investment activity. As opposed to conventional bonds, which merely confer ownership of a debt, Sukuk grants the investor a share of an asset, along with commensurate cash flows and risk.

Thus, the primary condition of issuance of Sukuk is the existence of assets on the part of the issuer which may be the government corporate entity, banking and financial institutions or any entity which wants to mobilse financial resources. Identification of suitable assets is the first and arguably the most integral step in the process of issuing Sukuk certificates.

These authors have made an attempt to describe the mechanics of Sukuk, their structure with particular focus on regulatory framework for sukuk issuance in Bangladesh.

Definition: Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI), the Bahrain-based Islamic financial standard setter, has defined Sukuk as as follows:

“Certificates of equal value representing undivided shares in ownership of tangible assets, usufruct and services or (in the ownership of) the assets of particular projects or special investment activity, however, this is true after receipt of the value of the Sukuk, the closing of subscription and the employment of funds received for the purpose for which the Sukuk were issued.”[Shari’ah Standard-17]

Mechanism of Sukuk: The mechanism of Sukuk is akin to the concept securitisation. Securitisation is the process of packaging a pool of assets into tradable securities that can be sold to investors (through Sukuk) in the capital market. It allows an entity to utilise non-marketable assets on its balance sheet by packaging them into a pool of assets and transforming them into marketable assets. This enables institutions to efficiently recycle assets from their balance sheet and use the resultant liquidity for some productive purpose. The parties involved in the Sukuk deal are:

Subscribers: Subscribers are also known as Sukuk-holders or investors that invest in Sukuk instruments. Subscribers can be institutional investors or retail investors.

Originator: The first step towards securitisation is when a government, private corporation or financial institution identifies the asset(s) it wants to pool and transfers the same through contractual sale to a Special Purpose Vehicle (SPV). The issuing entity is called the originator or the issuer.

Special Purpose Vehicle: An SPV is a bankruptcy remote entity. It is an independent entity set up specifically for the securitisation process. Forming an SPV is beneficial as it will not be affected in case of financial distress of the originator and vice versa.

Credit Enhancers: The originator arranges for various forms of credit enhancement to be provided in order to lower the overall perceived risk of the instrument. This can take the form of a third-party guarantee – from an Islamic financial institution or even a sovereign. Credit enhancement can also occur during the rating process when issuers realise that their issuances are set to receive a rating which is lower than expected. In order to improve the rating, issuers introduce a respected third party to offer additional credit guarantees or resort to over-collateralisation.

Rating Agency: Securities require a rating to be issued by a recognised rating agency to increase the confidence of potential investors. The rating agency is required to perform an extensive due diligence exercise on the worthiness of the collateral, the structure of the cash flows from the asset that is being securitised and a stress test to check the extent to which the SPV is vulnerable to bankruptcy.

Features of Sukuk from Shari’ah Perspective: Unlike conventional securities under securitisation deal, Sukuk must adhere to Shari’ah rules and principles, including its structuring, the underlying assets that back the sukuk issuance, the investment of sukuk proceeds, as well as its trading and other related issues.

• A number of Shariah-compliant contracts are used to create financial obligations between the sukuk issuers and sukuk holders, including sale, lease, partnership, agency and a combination of contracts.

• The underlying assets of the sukuk structure must be Shariah-compliant and may include tangible assets, usufructs, income-generating services, intangible assets, receivables from Shariah-compliant commodities, and the assets of particular projects or investment activities.

• The underlying assets of sukuk have further developed to include a mix of both debts (e.g. receivables from Shariah-compliant sales of commodities) and non-debt assets (e.g. tangible assets comprising lease assets and Shariah-compliant shares) to form a blended portfolio.

• The investment of sukuk proceeds should be for Shariah-compliant purposes and mostly fund activities in real sectors.

• The tradability of sukuk is guided by the relevant Shariah rules, e.g. sukuk holders must own all the rights and obligations associated with the ownership of the sukuk assets, and sukuk must not represent receivables or debts.

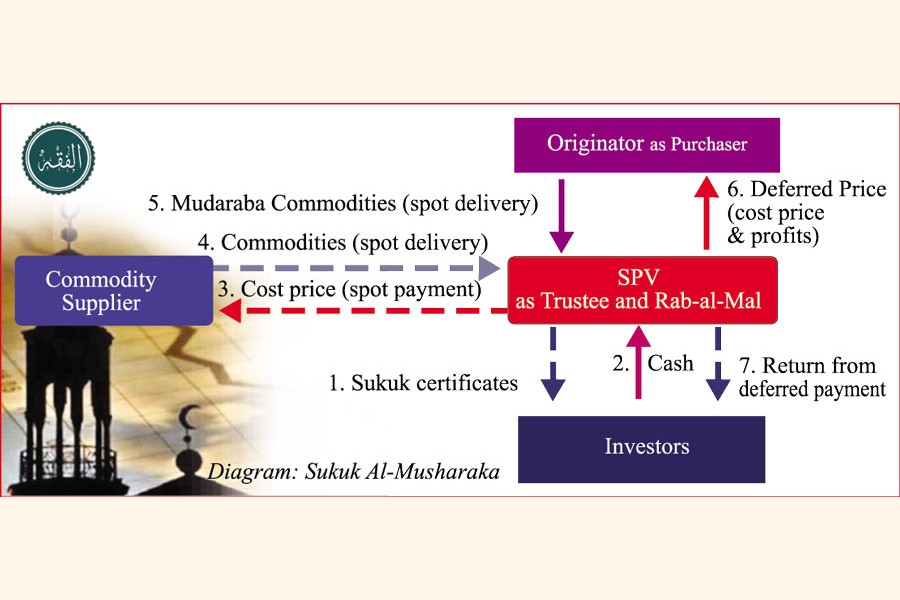

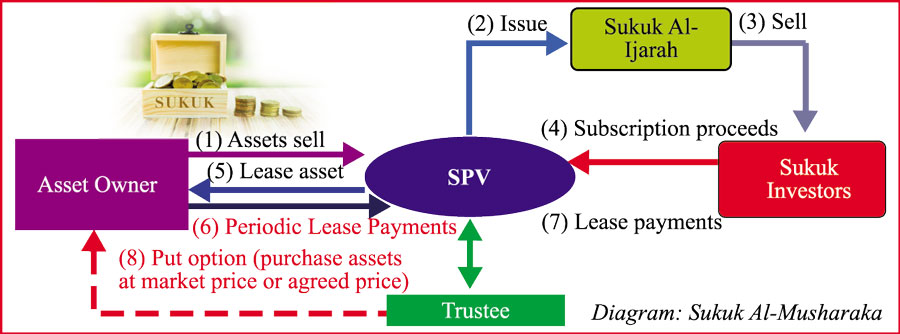

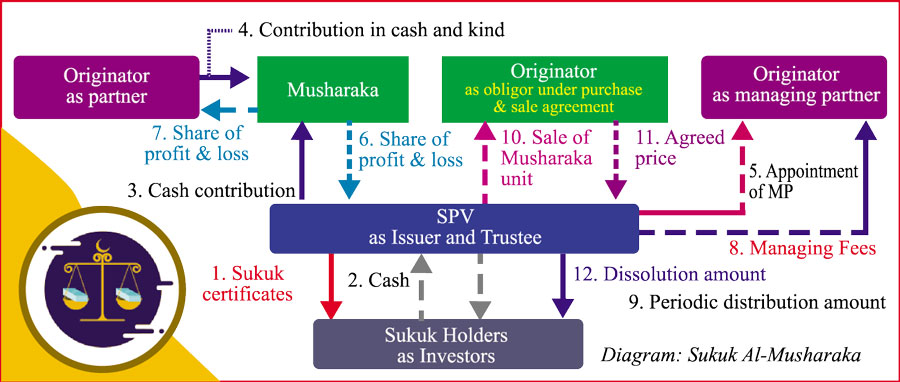

Some Structure of Sukuk: A Special Purpose Vehicle (SPV) lies at the heart of the sukuk structure that purchases the asset from the original owner on behalf of the sukuk holders. The SPV is often set up as part of the group of companies selling the asset and, hence raising the funds. For the interest of the sukuk holders, the SPV needs to be bankruptcy remote, which means that any insolvency of the original seller of the asset does not affect the SPV. Some sukuk structures are depicted below, although it should be taken into consideration that variations occur depending on the underlying transaction type, but the underlying principles remain the same.

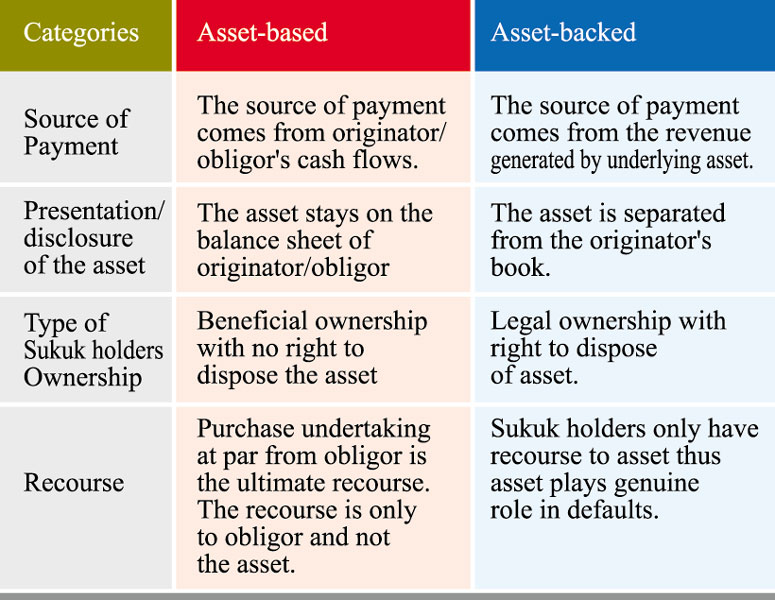

Structure of Sukuk: Asset-Backed Vs. Asset-Based Sukuk: There has been considerable debate as to whether Sukuk instruments are akin to conventional debt or equity finance. This is because there are two types of Sukuk:

1) Asset-based Sukuk where the principal is covered by the capital value of the asset but the returns and repayments to Sukuk holders are not directly financed by these assets.

2) Asset-backed Sukuk where the principal is covered by the capital value of the asset and the returns and repayments to Sukuk holders are directly financed by these assets. According to being asset backed or asset based, Sukuk can be more similar to bonds or shares so we explain the structure of both of them.

We can summarise the differences of these two types of Sukuk as below table:

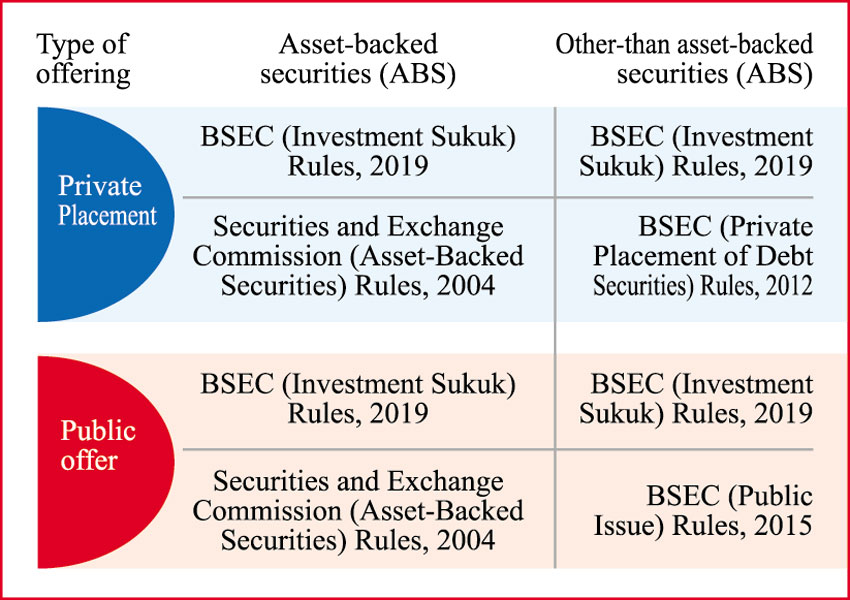

Regulatory Framework: Sukuk Rules in Bangladesh: Bangladesh Securities and Exchange Commission (BSEC) issued Investment Sukuk Rules for governing all types of investment sukuk structured in line with Shari’ah principles. Now we will discuss the legal procedures in issuing and governing investment sukuk under purview of Bangladesh Securities and Exchange Commission or BSEC (Investment Sukuk) Rules, 2019. Investment Sukuk under this rule can be issued through private placement or public offering. The relevant rules for issuance of sukuk are given below:

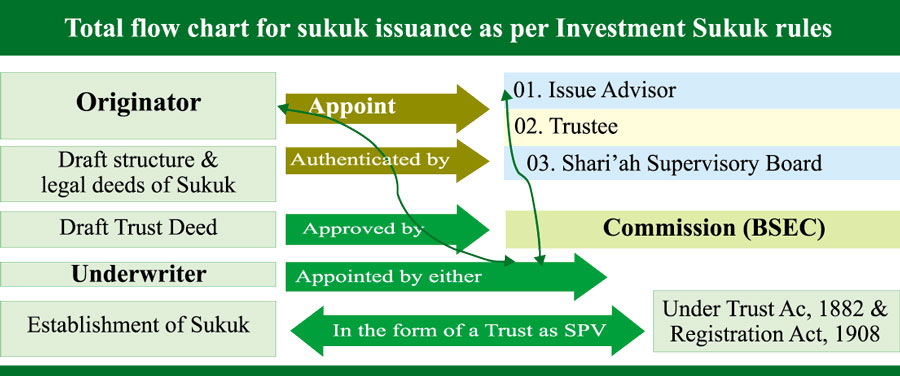

Sukuk Governance and Management Structure: An Investment Sukuk shall be constituted in the form of a trust as a Special Purpose Vehicle (SPV) and has the following organs of governance:

A. Body entrusted with governance: The Board of Directors or equivalent or other relevant committee of the originator or issuer, as appropriate is entrusted with the governance of Sukuk issuance;

B. Body entrusted with Management: The management team of originator or issuer or any other team assigned by deed of trust is entrusted with the management of an SPV’s operations;

C. Sukuk’s Shari’ah Supervisory Board (SSB): The body formed by originator, under these rules to supervise the Shari’ah compliance and the Shari’ah pronouncement. The SSB is not accountable to the Board of the Originator or Board of Trustee about their role and independence in giving opinion. SSB is also responsible for authentication of the annual financial statements of the SPV as well as consideration, adaptation and approval of restructuring and termination of Sukuk.

D. Trustee: An entity appointed by the originator to serve as an intermediary between the originator and the Sukuk holders, to hold Sukuk assets on behalf of the Sukuk holders and to safeguard the interest of the both parties. Trustee is also responsible for liquidation/disposal/sale of Sukuk’s assets, in case of default/noncompliance in favour of the Sukuk holders with due approval of the Commission to protect the interest of the Sukuk holders.

E. Auditor: Auditor includes Shari’ah auditor.

Total flow chart for sukuk issuance as per Investment Sukuk rules is presented top right above.

Utilisation and Management of Sukuk Proceeds and Assets: Sukuk assets and proceeds are kept with SPV under the Trustee legally or beneficially in line with the Shari’ah principles and rules in the following manner:

Sukuk proceeds or investments shall be governed by a prudent investment policy duly adopted by the originator and the trustee through an “Investment Management Agreement (IMA)”

Sukuk assets shall be clearly identified in the prospectus or offer document of the Sukuk.

Sukuk assets shall be free of any legal impediments through:

3.1. Transferring to the SPV at fair value or a value reasonably close thereto;

3.2. Keeping separately to the SPV identified from the assets of the originator.

4) Disposal or changing of Sukuk assets shall be done on business perspective considering interest of the Sukuk holders.

5) Relocation of Sukuk assets shall not be done jeopardizing the interests of the Sukuk holders.

6) Sukuk assets shall be registered in the name of SPV.

Tradability of Investment Sukuk: Trading of investment Sukuk can be taken place both for listed and un-listed sukuk; however, the same can be clearly allowed in Shari’ah pronouncement. In case of listed sukuk, the instrument can be traded in the bourses through trading platform. On the contrary, for un-listed sukuk, the instruments can be traded in Over the Counter (OCT) platform of the Exchanges or Alternative Trading Board (ATB) of the Exchanges.

Legal Documents related to Investment Sukuk

Such documents are: 1. Certificate of Investment Sukuk; 2. Shari’ah Pronouncement; 3. Deed of Trust; 4. Draft Structure of Investment Sukuk 5. Prospectus of Sukuk and

6. Information Memorandum (Brief of the SPV, Originator, Trustee, Issue Advisor and other organs of the Sukuk issuance, issue date, size of the issue, types of sukuk, mode of issue, purpose of issue and utilisation proceeds, expected return, its structure, payment schedule, profit distribution, profit/loss sharing mechanism, details of recourse mechanism, credit enhancements, options, if any; name and contact detail of the Shari’ah Advisors, final Shari’ah pronouncement, credit rating of Investment Sukuk and the Originator; details of the mechanism for final settlement etc.).

Way Forward

Every year the government faces considerable challenges to mobilise resources in meeting its development expenditure and regularly borrows from the banking sector to finance the deficit. With a huge budget deficit of Tk 1,900.00 billion in Finance Bill 2020-21 (about 6 per cent of GDP), the government has to spend a substantial amount as interest expense for borrowing from banking and non-banking sources. Too much borrowing from the banking sector (Tk 849.80 billion proposed for FY2020-21 against Tk 824.21 billion in the revised budget of FY2019-20) may put the country’s financial sector under tremendous pressure as credit flow to the private sector may be hampered to a great extent which in turn may further slow down the country’s Covid-stricken economic progress.

Every year the government faces considerable challenges to mobilise resources in meeting its development expenditure and regularly borrows from the banking sector to finance the deficit. With a huge budget deficit of Tk 1,900.00 billion in Finance Bill 2020-21 (about 6 per cent of GDP), the government has to spend a substantial amount as interest expense for borrowing from banking and non-banking sources. Too much borrowing from the banking sector (Tk 849.80 billion proposed for FY2020-21 against Tk 824.21 billion in the revised budget of FY2019-20) may put the country’s financial sector under tremendous pressure as credit flow to the private sector may be hampered to a great extent which in turn may further slow down the country’s Covid-stricken economic progress.

Considering the upcoming $300 billion infrastructure development projects to be implemented by 2031, time has come to explore the opportunity to lessen the burden on the country’s banking sector to finance budget deficit as well as to help boost the country’s capital market for further expansion programme in public sector along with the private sector being supported by existing regulatory framework for investment sukuk.

Recently, the Ministry of Finance has issued the guidelines titled ‘Bangladesh Government Investment Sukuk Guidelines, 2020’ through a gazette notification aiming to expand and smoothen the participation of Shari’ah-based finance in the ongoing development projects. Islamic banks and financial institutions can join there to finance the government’s deficit through the proposed Shari’ah-compliant Sukuk instrument and these sukuk would be a component of Statutory Liquidity Ratio (SLR) for the Banks and NBFIs.

In line with the above, the Bangladesh Bank issued a circular in this regard on October 21, 2020. As per the guidelines, the central bank would form a Shari’ah Advisory Committee comprising experts from the central bank and the Finance Division (MoF) as well as Shari’ah, business and finance experts.

The views expressed in the article are the authors’ own and not necessarily the organisation they represent.

Khaled Mahmud Raihan FCCA and Mohammad Jasim Uddin work at Corporate Investment Wing of Islami Bank Bangladesh Ltd.

raihan.accaglobal@gmail.com.

© 2026 - All Rights with The Financial Express