Bangladesh Bank: The central bank of the country — FE Photo

Bangladesh Bank: The central bank of the country — FE Photo ![]() Bangladesh's banking sector is likely to face extra challenges in the coming years as the asset quality, capital and profitability are projected to deteriorate significantly mainly due to the ongoing Covid-19 pandemic.

Bangladesh's banking sector is likely to face extra challenges in the coming years as the asset quality, capital and profitability are projected to deteriorate significantly mainly due to the ongoing Covid-19 pandemic.

Global rating agency Moody's has already projected that non-performing loans (NPLs) or problem loans will double, on an average, across the 14 Asia-Pacific (APAC) economies including Bangladesh by 2022 as economic conditions worsen.

Moody's Investors Service analysis is focused on cumulative outcomes at the end of 2022, rather than the precise timing of NPL formation, because various loan moratoriums implemented in response to the pandemic will delay the recognition of problem loans.

The rating agency has simulated the impact of the current economic downturn on asset quality, capital and profitability for 218 rated banks in the region. Its results show that despite substantial risks, most banks' creditworthiness will remain intact.

In Bangladesh, the most important indicator to demonstrate the asset quality is the position on classified loans that has maintained an upward trend until December 2019 despite special policy support, provided by the Bangladesh Bank (BB), the country's central bank, to loan defaulters.

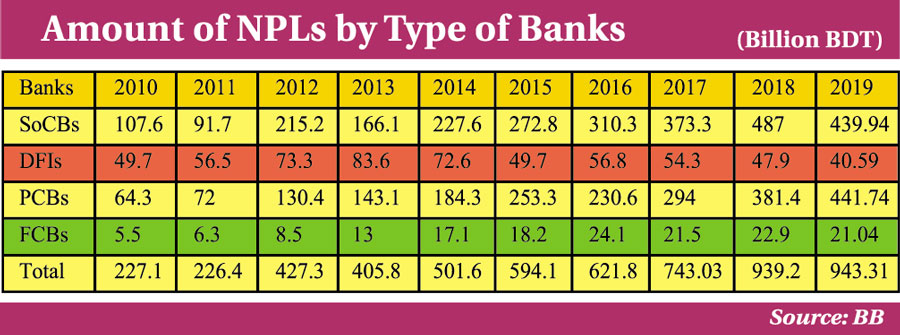

The amount of NPLs edged up by 0.45 per cent to Tk 943.31 billion in 2019 from Tk 939.11 billion a year earlier, despite the policy support from the central bank to delinquent borrowers.

Earlier on May 16, 2019, the BB offered a special facility to loan defaulters, allowing them to reschedule loans by paying 2.0 per cent down payment for a maximum of 10 years.

Also, such borrowers were allowed to avail one-time exit facility clearing dues within 360 days after approving such facility by the banks.

Meanwhile, the central bank has extended for three more months the suspension of rigid rules for classification of loans to help the businesses overcome the damaging effect of the Covid-19 pandemic.

The BB has already asked all the scheduled banks not to be harsh while classifying loans until December 31 next. The original deadline for the facility was due to expire on September 30.

This was the second extension. The concession that came into effect for the first time on March 19 was made effective until June 30. But it was extended for another three months until September 30 to help the businesses battered by the pandemic.

Besides, the repayment of all loan installments has been deferred from January 01 to December 31.

The central bank is expected to issue a new directive on the provisioning of such loans and advances for the period by the end this month.

Senior bankers, however, welcomed the BB's latest moves, saying it is necessary for revamping business activities across the country.

Actually, the rapid and widening spread of the coronavirus outbreak, deteriorating global economic outlook and asset price declines are creating a severe and extensive credit shock across many sectors, regions and markets.

Bangladesh's banking system has been one of the sectors affected by the shock, especially given the persistent weaknesses in underwriting standards and high credit concentrations in large domestic corporate entities.

Bankers feared that NPLs would increase across multiple sectors, including but not limited to, apparel and clothing sector, retail, manufacturing and trade services.

The classified loan in the banking sector of Bangladesh is still a number one challenge despite close monitoring by the central bank.

The NPLs have become a major concern for the banking sector of Bangladesh due to their multiple prolonged adverse impacts on bank's balance sheet having consequential effect of erosion of capital and impairing earnings, profitability, liquidity and solvency of the banking industry.

The central bank has already identified seven major issues behind high NPLs in Bangladesh.

The issues include absence of due diligence in borrower selection, deviation from the standard credit risk management procedures prescribed by the central bank or enumerated in bank's own credit policy, inadequate collateralization and at the same time, overvaluation of collaterals cause serious hindrance in the risk mitigation process, sometimes encouraging the borrowers to default.

Poor post disbursement monitoring and follow-up of borrowers, leniency towards large borrowers in case of sanctioning, renewing, waiver of interest, rescheduling and restructuring and diversion of fund by the borrowers, taken as loans from the banks, from their business to use it for other purposes have also been identified as major issues high classified loan in Bangladesh.

In order to bring down NPLs within tolerable levels, effective management of default loans is a crucial matter. The regulator has already taken different policy measures to reduce the volume of NPLs in the banking sector.

Banks have been asked to ensure proper due diligence while disbursing new loans to prevent creation of new NPLs and expedite their recovery drive through disposal of the long pending lawsuits by increasing monitoring and employing renowned lawyers and creation of a task force at the head office, regional office and branch level.

The central bank along with the government is taking necessary initiatives for regulatory and legal reform to create a suitable environ ment for existing NPLs recovery. Amendment of the existing laws is expected to accelerate the defaulted loan recovery process.

Besides, effective practice of corporate governance, transparency and accountability in all aspects, efficient credit risk management, managerial efficiency and adaptation of modern technological changes may improve the overall NPL problem scenario of the banking sector of Bangladesh.

Official data shows that the amount of classified loans increased more than four times during the last 10 years because of poor assessment and inadequate follow-up and supervision of the loans.

During the period covering from 2010 to 2019, the amount of default loans of state-owned commercial banks (SoCBs), private commercial banks (PCBs) and foreign commercial banks (FCBs) have increased by Tk 332.34 billion, Tk 377.44 billion and Tk15.54 billion respectively while such trouble loans with development-finance institutions (DFIs) came down to Tk 40.59 billion in 2019 from Tk 49.70 billion in 2010.

On the other hand, loan loss provision coverage in Bangladesh is inadequate and will provide a limited buffer. While regulatory deferments of loan classification and repayments will provide temporary relief, they could raise risks for banks in the longer term.

Possible lower asset quality will lead to higher credit costs, although regulatory deferments will mitigate the impact. But lower net interest margins (NIMs) will contract because of declines in loan repayments and a regulatory 9.0 per cent cap on lending rates that took effect on April 01 this calendar year.

NIM is a measure of the difference between the interest income generated by banks or other financial institutions and the amount of interest paid out to their lenders (for example, deposits), relative to the amount of their (interest-earning) assets. It is similar to the gross margin (or gross profit margin) of non-financial companies.

Besides, lower interest rate spread may also hit the overall profitability in the country's banking system. The weighted average spread between lending and deposit rates offered by commercial banks stood at 3.00 per cent in September from 4.07 per cent in April 2020 following implementation of the single-digit interest rate in the banking sector.

Bangladesh banks' profitability is likely to fall in the coming years as the coronavirus outbreak accelerates structural changes in the sector.

The NIMs may continue to fall while credit costs will increase. At the same time, an acceleration of the adoption of digital banking services due to lock-downs and social distancing will lead banks to boost investment in technology, which will erode profit.

Reducing the bank's earnings and increasing the stressed asset are the main challenges of the banking sector.

The International Monetary Fund (IMF) has already put forwarded six-point suggestions to address weakness in the banking sector of Bangladesh.

The recommendations include strong corporate governance, enforcing 'fit and proper criteria' for banks' directors, enhancing banking regulation and supervision, reforming SoCBs, tightening criteria for loan rescheduling or restructuring and enhanced legal systems to accelerate loan recovery.

However, to avoid further vulnerability in the sector in terms of default loan and to channel funds for growth recovery, constant supervision and vigilance are required for ensuring growth momentum and macroeconomic stability in the coming years.

The writer is a Special Correspondent of the FE. He can be reached at siddique.islam@gmail.com

© 2026 - All Rights with The Financial Express