KAS Murshid, Shahid Khandker, Khondoker Shakhawat Ali, Hussain Samad and Monzur Hossain in a BIDS report | November 23, 2020 00:00:00

![]() Bangladesh has embraced mobile financial services (MFS) with the aim of expansion of financial inclusion and economic development. MFS has expanded rapidly in both rural and urban Bangladesh over the past 9 years propelled by bKash Limited, a subsidiary of BRAC Bank, which has assumed the industry leadership position through a virtually unassailable lead in the market. It has a 55 per cent share of the MFS market.

Bangladesh has embraced mobile financial services (MFS) with the aim of expansion of financial inclusion and economic development. MFS has expanded rapidly in both rural and urban Bangladesh over the past 9 years propelled by bKash Limited, a subsidiary of BRAC Bank, which has assumed the industry leadership position through a virtually unassailable lead in the market. It has a 55 per cent share of the MFS market.

The number of registered MFS accountholders stands currently at over 70 million compared to less than 30 million in 2015. However, the number of active MFS accountholders is 32.5 million compared to around 12 million in 2015. The average of daily total transactions is 6.7 million, while the value of daily transactions exceeds Tk 10 billion. Furthermore, bKash has more than 37 million customers with an active customer base of more than 17 million. MFS like bKash is now rapidly gaining traction in many new areas to make payments at shops, pay utility or internet bills, top-up money on phones, send money to government safety net beneficiaries, and so on. Bank accounts can now be linked up with the bKash accounts to make financial planning and transactions even more seamlessly efficient.

However, very few attempts have been made in Bangladesh to understand MFS' impact on people's welfare. Thus, it is in this context that the field survey for the leading MFS provider namely bKash was carried out bythe Bangladesh Institute of Development Studies(BIDS) in 2018. The study points to the considerable impact of bKash on household welfare, including income, consumption stabilisation, educational and health expenditures, and women's empowerment.

Access to Finance and MFS

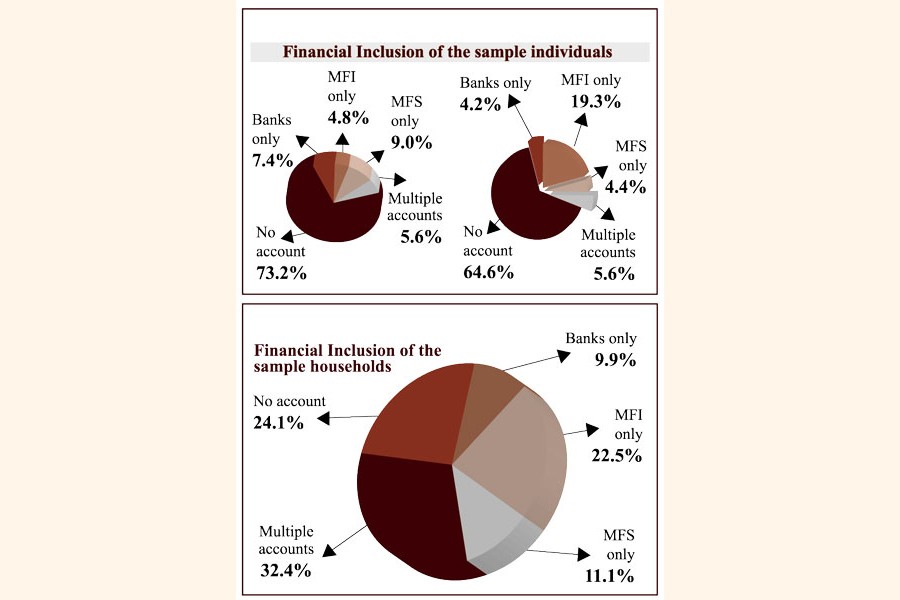

The data collected for the study show that 30.9 per cent of the adult population in rural Bangladesh have a financial account. Of these, 5.9 per cent have a bank account only, 11.8 per cent have an account with an MFI (microfinance institution) only, 6.7 per cent have an MFS account only, and 6.5 per cent have accounts with multiple financial entities including bKash.

The data collected for the study show that 30.9 per cent of the adult population in rural Bangladesh have a financial account. Of these, 5.9 per cent have a bank account only, 11.8 per cent have an account with an MFI (microfinance institution) only, 6.7 per cent have an MFS account only, and 6.5 per cent have accounts with multiple financial entities including bKash.

Women were more likely to have a financial account: 35.4 per cent of adult females had an account compared to 26.8 per cent of males. Females have greater access, partly because of a substantially higher share of microcredit loans from MFIs. More than 19 per centof females have an MFI account compared to only 4.8 per centof males.

Attaining universal financial inclusion still remains a distant goal: 73.2 per centof males and 64.6 per centof females do not have access to any form of financial service. However, only 24 per cent have no access to finance in case we consider financial inclusion at the household level.

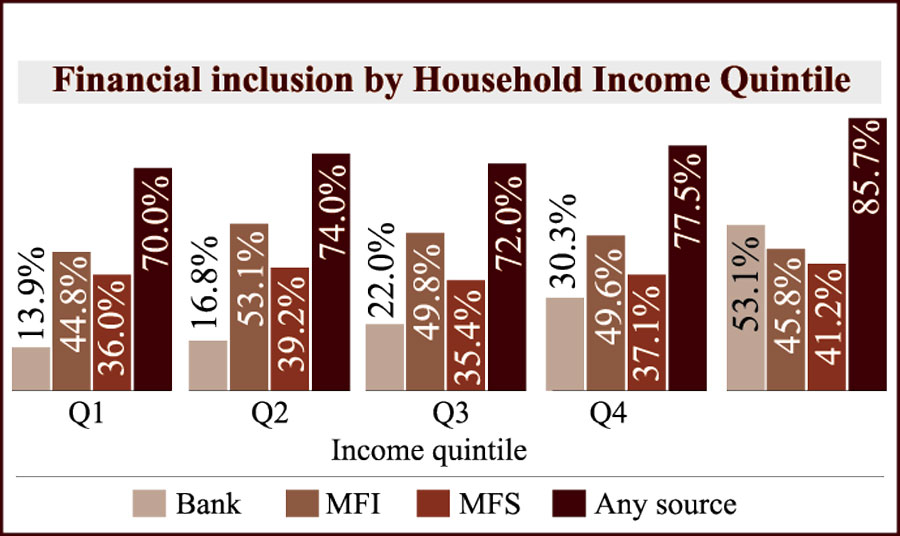

Moreover, access to finance at the household level is higher among the rich than it is among the poor: 85.7 per cent households from the richest quintile compared to 70 per cent from the lowest income quintile.

However, MFS tends to serve the rich and the poor alike. From the poorest quintile, 44.8 per cent households have access to MFIs and 36 per cent to MFS. In contrast, in the richest quintile, 45.8 per cent households have an account with an MFI compared to 41.2 per cent with MFS. The poor perform quite well in terms of MFS usage, especially when compared to the banking sector. Household survey data suggest that three MFS providers mainly serve the selected rural communities, namely bKash, Rocket and SureCash. Ninety eight (98) per cent of rural households have at least one mobile phone, but only 38.4 per cent have an account with an MFS.

As for individual MFS providers, 24 per cent households have an account with bKash only and 28 per cent have a non-bKash account. Among the households with mobile phones, 68 per cent are found to use (any) MFS, with 50.6 per cent using bKash. It may be noted that 'use' needs to be combined with frequency and volume of transactions to understand how important a particular provider is.

Who uses bKash and for what?

bKash is used for receiving and sending money by over 14 per cent of all individuals in rural Bangladesh, (16 per cent males and 12 per cent females). For recipients, the figures for male and female are 14 per cent and 12 per cent compared to only 3.3 per cent who use it for sending money. For bKash and overall, around 56 per cent of recipients were men and 44 per cent were women (out of 1,659 respondents for bKash).

And among all the senders who used bKash, 81.2 per cent were males and only 18.8 per cent were females. Fathers are the most dominant senders, accounting for 28.1 per cent of transactions, followed by males sending money to relatives outside the immediate family (19.1 per cent), and brothers sending money to siblings (12.9 per cent).

The study shows that the most dominant use of money received or sent was for consumption and education. It is interesting, however, to note that, the stated purpose of senders and the actual use reported by users differ quite markedly. In terms of the stated purpose, 26 per cent said it was for consumption while 28 per cent said it was for education. Receipts, however, reported that 74 per cent was used for consumption while only 6.0 per cent went to education.

This is an important finding, underlining the crucial importance of consumption, which cash inflows encourage. The information gathered also points to the non-local origin of money flows to recipients, especially in the case of bKash users. For all MFS, 66 per cent of receipts are originated from outside the district- a figure that is heavily dominated by bKash at 67 per cent. Interestingly, this is somewhat higher for female recipients (70 per cent) compared to males (64 per cent).

Determinants of household access to MFS

There are some factors that influence household access to MFS. Of explanatory variables of particular interest, the findings are- male-headed households are more likely to have an account with MFS and an account with another financial service; age of household head positively affects account-holding with a bank or bKash; and education matters in influencing opening a bank account or accounts with bKash or any other financial service.

Surprisingly, landholding negatively affects access to financial services, while non-land assets have a positive effect. Non-land assets have the largest effect on access to banks.

Having a smartphone in the household increases the probability of financial inclusion by almost 29 percentage points, compared to 23 percentage points in the case of regular mobile phones. Similarly, ownership of a smartphone increases the adoption of bKash account ownership by 22.3 percentage points, whereas ownership of regular phones increases such probability only by 10.1 percentage points. Interestingly, neither a smartphone nor a regular mobile phone affects the use of Rocket or SureCash services, although these have a positive impact on bKash usage. Furthermore, the presence of agents in a village matters. More specifically, the presence of a bKash agent increases its use by 4.9 percentage points. This relationship is slightly weaker for other MFS.

Household-level impact of bKash

MFS like bKash has a significant impact on the efficiency of household resource allocation and hence impact household income, consumption and other indicators of household welfare by transferring money in an efficient, fast and secure manner. The descriptive statistics of selected outcomes of interest shows that household per capita total expenditure for bKash users is Tk 3,126 per month, compared to Tk 2,580 per month and Tk 2,887 per month for non-bKash MFS users and nonusers of MFS, respectively.

This is due to the higher non-food expenditure of bKash users (Tk 1,626.5 per month) compared to others (Tk 1,163.5 per month). The estimates represent that bKash increases household nonfarm income by 15.2 per cent and total per capita income by 5.8 per cent. According to the findings, a 10 per cent increase in bKash transaction volumes increases per capita non-food income by 0.5 per cent, per capita income by 0.3 per cent, and per capita fishery income by 3.3 per cent.

Income and consumption-smoothing effects of bKash

The use of bKash has a smoothing impact on income and consumption- but mostly on the former. For households who were exposed to shock but did not have bKash, domestic remittances declined by 61.6 per cent, and consequently, per capita income declined by 17.1 per cent, but without any significant impact on per capita consumption. For households who were exposed to a shock and did use bKash, domestic remittance increased by 60 per cent, and as a consequence, per capita expenditure increased by 6.2 per cent and income increased by 28.1 per cent. This is the risk-mitigating role of bKash: it helps smooth income and consumption of households exposed to any shock. Responses to shocks appear to be particularly pronounced for health shocks and floods.

The social sector impact of BKash: Education, Health and Women's empowerment

Education expenses

In the following study, a total of 246 transactions were recorded relating to money sent to students outside the locality. Around 54 per cent of these are sent by bKash while 40 per cent were delivered physically. Thus, on average, Tk 1,549 was sent in a year to a student by his/her household. For households which use bKash, this was Tk 2,807 while for households which do not use bKash, this was Tk 290. It suggests that the traditional form of sending money physically has already turned into a meagre flow.

Compared to non-MFS users, MFS-using households spend significantly more on education (Tk 7,278 vs Tk 4,169), a difference of over Tk 3,000. Between the bKash-users and non-users, the difference is sharper by almost Tk 4,300. The 'Instrumental Variable' or IV approach shows that bKash adoption has a significant impact on educational expenses met by households. BKash adoption leads to a 48 per cent increase in educational costs, while MFS adoption (including non-bKash MFS usage) results in a 45 per cent increase. Note that bKash played a significant role in the government's secondary education stipend programme (SESP) during 2017, 2018 and 2019.

Health expenses

On average, bKash-using households report a total of 10.7 days of illness suffered by members per annum compared to 10.3 days for non-bKash households. However, interestingly, bKash-using households are more likely to seek consultation with a medical professional compared to non-users. On average, bKash users spend Tk 1,658 per annum on medical treatment while non-users spend Tk 1,138. The adoption of bKash or bKash use stimulates health expenses to rise by 54 per cent. And it is 47 per cent in the case of all MFS taken together (including bKash).

Women's empowerment

The study assessed empowerment through a number of qualitative and quantitative indicators. It includes women's freedom of movement outside home, their role in household and financial decision making, their participation in income-generating activity (IGA), earnings from the labour market, and ownership of assets like jewellery and monetary savings. In all indicators except for one (namely, their role in economic-financial decisions of the family), the impact of bKash was positive and significant. BKash has a significant impact on women's welfare. The use of bKash increases women's ownership of assets by 14 per cent and women's engagement in IGA by 9 percentage points. From the findings, it can be seen that a 10 per cent growth in the amount received through bKash increases women's asset by 2.1 per cent and women's engagements in IGA by about 1.1 percentage points.

This study has unearthed quite an impressive set of findings related to the operations of bKash and its impact on a wide range of outcomes. It has a significant impact on income and savings. At the same time, it demonstrates a strong effect on household welfare through mitigating fluctuations in income and consumption and reducing risk when faced with shocks. Outcomes recorded on social factors like education, health and especially women empowerment were strikingly impressive. Given the considerable potential for further development, the evolution of MFS augurs well for Bangladesh's development objectives, and entities like bKash will certainly see the rapid expansion in scale and turnover as fresh markets are explored. However, this will require incentives to be fine-tuned.

[Bangladesh Institute of Development Studies (BIDS) published the report titled "Impact of mobile financial services in Bangladesh: The case of bKash" in September 2020. This article presents the key findings from the report.]

KAS Murshid is the Director General of BIDS. murshid@bids.org.bd

Shahid Khandker is a Consultant and Senior Economist.

Khondoker Shakhawat Ali is a Consultant and Senior Sociologist.

Hussain Samad is a Consultant and Economist.

Monzur Hossain is a Senior Research Fellow of BIDS.

monzur@bids.org.bd

© 2026 - All Rights with The Financial Express