![]() As the global financial industry is advancing towards "the future", two ground-breaking concepts are being vigorously cherished worldwide. FinTech and InsurTech. The banking industry, being one of the major players of the whole unit, has been much more successful in adopting and implementing FinTech while altering their operations and practices over the years. On the other hand, the global insurance industry is significantly lagging in adopting InsurTech. The reasons behind the slow pace, as global experts have suggested, that the insurance products are much more complex in every possible way than the banking products and also, insurance has always been a "push product" which entails the slow pace of scale-up of the global insurance industry as well as the adaptation of InsurTech. Still, the silver linings between traditional insurance, microinsurance, and InsurTech are blurring increasingly day by day.

As the global financial industry is advancing towards "the future", two ground-breaking concepts are being vigorously cherished worldwide. FinTech and InsurTech. The banking industry, being one of the major players of the whole unit, has been much more successful in adopting and implementing FinTech while altering their operations and practices over the years. On the other hand, the global insurance industry is significantly lagging in adopting InsurTech. The reasons behind the slow pace, as global experts have suggested, that the insurance products are much more complex in every possible way than the banking products and also, insurance has always been a "push product" which entails the slow pace of scale-up of the global insurance industry as well as the adaptation of InsurTech. Still, the silver linings between traditional insurance, microinsurance, and InsurTech are blurring increasingly day by day.

Looking into the case for Bangladesh, in the last couple of years, the economy of Bangladesh has seen rapid growth with active and ever-increasing intervention of digitalization starting from creating a support system for young digital entrepreneurs, tech-based startups, e-commerce sites to access to finance, digital payment systems. The blessings of digital intervention throughout the economy has pushed Bangladesh a step forward in achieving the goal of transforming into "Digital Bangladesh", yet there are a number of places where digital solutions can aid the loopholes. Remit foreign payments through digital payment channel for managing business operations of e-commerce merchants, absence of Interoperable Digital Money Transfer Platform are to name a few. As we are having increasing concern and investment in digitalization of the economic sector of Bangladesh, the endeavour that can accelerate the process is to transform the industry sector into InsurTech.

The insurance industry of Bangladesh has been observing steep growth over the past years. Despite the constant growth, both life and non-life insurance industries are lagging a little behind from reaching the expected market penetration despite having enormous potentiality. Statistics suggest that only 6.0% of the huge population are covered under life products and the penetration rate for non-life insurance is around only 1.0% across the whole country; whereas South Africa has more than 60% insurance penetration and the Philippines has over 21% if we compare Bangladesh with successful global examples of insurance penetration. (LankaBangla Asset Management, 2020)

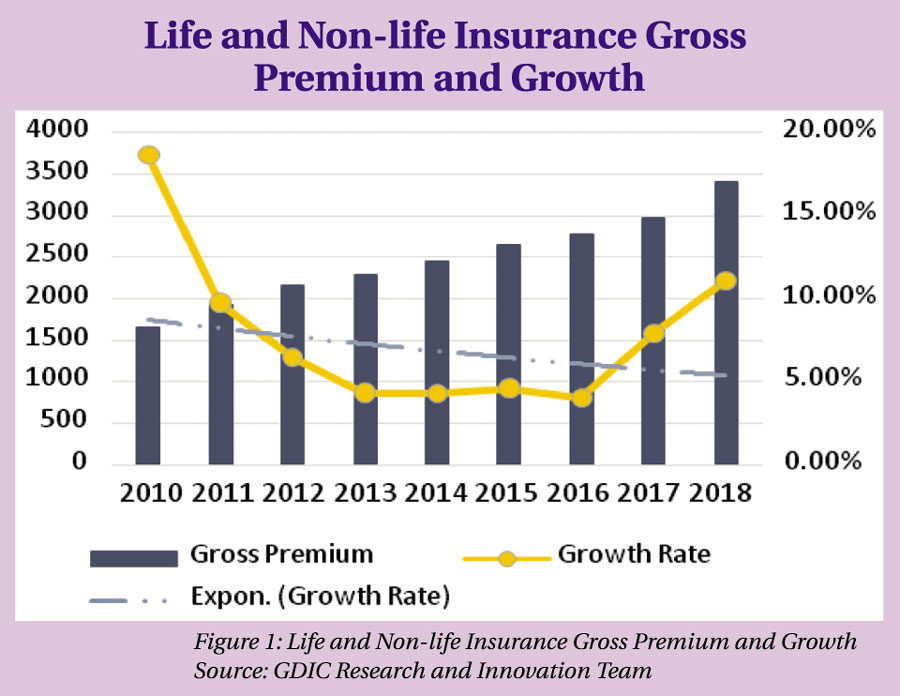

The preparedness of the insurance industry towards establishing InsurTech: The insurance industry is experiencing growth recently after a drastic fall after the year 2010 which was caused by the concentration of the market, fewer diverse products, and the market's unwillingness to face and mitigate the challenges. The life insurance market's growth in terms of gross premium earning was 7.52% and non-life's growth is 13.33% in 2018 following the gradual growth from the year 2016. (Insurance Development and Regulatory Authority (IDRA), 2019). It can be derived from the recent trend that the market is getting more attention and demand for non-life products is increasing gradually.

After the outbreak of the pandemic COVID-19 as the economic activities have been disrupted significantly during the lockdown period, the projected growth and expansion of the insurance market is formidable given the higher possibilities of inflation and probably an economic recession at this point. Among all the negative movements within the industry, this market has been observing positive changes, in terms of customer demands of diverse life and non-life products, especially health products, which also indicates the increasing level of awareness and preparedness for the upcoming pandemics.

COVID-19 has also stimulated a strong realisation that technology is the only key to the future. Companies had to plunge into introducing digital solutions into their operations to refrain a complete halt of businesses and incomes. That was the time when it became clear that it is almost prepared to enter a new chapter towards the most desired future of the industry through adopting InsurTech and it's no longer a threat.

Shifting Dynamics: Bangladesh has entered the bottom of the pyramid for establishing InsurTech a couple of years ago. Raising industry awareness, increasing investments for digital solutions, involving youth in generating tech-savvy ideas, adopting digital solutions are among the few initiatives that have commenced in recent years to inspire the industry players to move towards InsurTech. It is the solution that will enable the industry to be effective while being efficient at the same time.

Digital advancement across the whole country is also an indicator of the preparedness of the market. With 120 national companies exporting ICT products, 162.92 million mobile users, 93 million internet subscribers, and a vibrant ICT industry projected to be a USD 5.0 billion market by 2021 indicates a rapid transition towards the vision of being transformed into a digital economy by the year 2021. Adopting emerging technologies i.e. IoT, Blockchain, Artificial Intelligence (AI), Big Data and Analytics, etc. are the upcoming priorities under the backdrop of becoming a knowledge-based economy by 2041. (Bangladesh - Commercial Guide, 2020)

Digital advancement across the whole country is also an indicator of the preparedness of the market. With 120 national companies exporting ICT products, 162.92 million mobile users, 93 million internet subscribers, and a vibrant ICT industry projected to be a USD 5.0 billion market by 2021 indicates a rapid transition towards the vision of being transformed into a digital economy by the year 2021. Adopting emerging technologies i.e. IoT, Blockchain, Artificial Intelligence (AI), Big Data and Analytics, etc. are the upcoming priorities under the backdrop of becoming a knowledge-based economy by 2041. (Bangladesh - Commercial Guide, 2020)

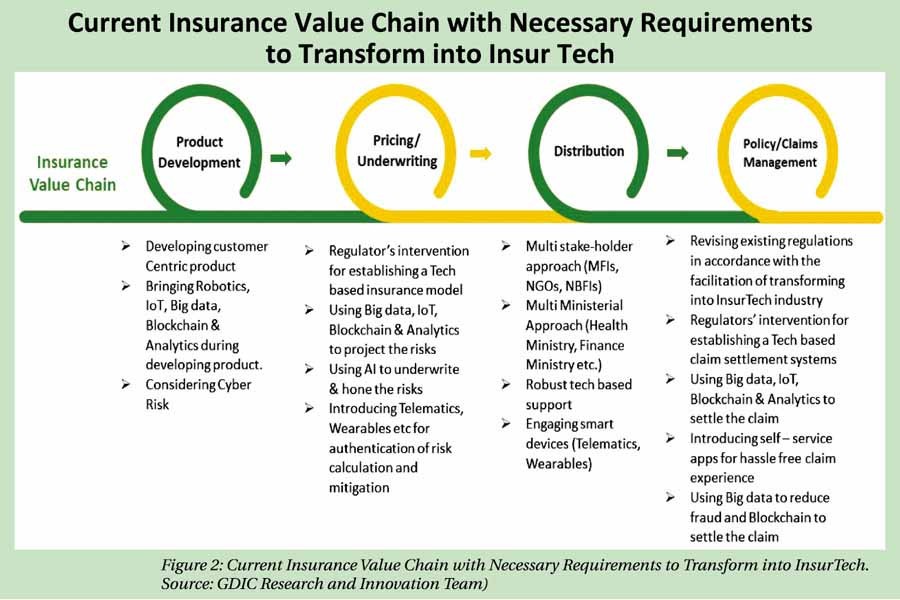

Increased collaboration among insurance companies, MFIs, NGOs, banks, and a wide spectrum of national and international development organizations are also very noticeable in recent years. The inclusive model that is evolving across the industries is increasing partnerships while strengthening operational efficiency, introducing disruptive business models, invoking new product innovations, and incorporating digital solutions throughout different processes across the insurance value chain. The experience gained through this inclusiveness is that the use of digital technologies can help all the stakeholders to add values to their services and can create a win-win paradigm for everyone including the clients.

Figure 2: Current Insurance Value Chain with Necessary Requirements to Transform into InsurTech. (Source: GDIC Research and Innovation Team)

The glimpse of future insurance industry of Bangladesh: What will the future of the insurance industry look like? The answer lies in the recent investment growth in the InsurTech industry and technology in recent years by the market leaders. Advanced countries around the world have successfully transformed their insurance industry into InsurTechand it is as famous as Fintech in many of them. With the $2.2 billion global investment in the InsurTech industry in 2017, the global InsurTech market revenue stood at $5.48 billion in 2019 and is expected to reach $10.14 billion by 2025, which is growing at a compound annual growth rate of 10.80%, from 2019 to 2025. It indicates that the global market is heavily driving towards transforming their traditional market into a tech-driven one.

As 80% of the global premium earning comes from emerging markets and Asia is one of them, it has high potentiality to transform the insurance industry into InsurTech. The global experts have suggested that emerging Asia has the potentiality to reach 14% of premium growth through digitally-enabled products. InsurTech began to make its presence felt in several Asian countries in 2013. It took the leading emerging Asian countries 6 years to reap positive results through growth in premium incomes specifically from the InsurTech industry. Among them, China is leading the emerging market of Asia having a growth of 16.2% of premium earning from InsurTech, whereas Thailand (5.3%), Malaysia (4.8%), Indonesia (2.4%), Vietnam (2.1%), and the Philippines (1.8%) also favourable growth rates in terms of premium earning from InsurTech industry. With this growth rate, it will take 9 more years for the emerging Asian industry to reach the projected 14% growth in terms of premium earning. Following the examples of fellow Asian countries, it can be said that it is high time for Bangladesh to start investing in and gradually transforming the insurance industry into InsurTech. (Oxford Business Group, 2020)

The benefits of having a fully established InsurTech industry are manifold. A few highlights are:

• Wider availability of insurance products through digital solutions can reduce the protection gap for natural disaster risks and healthcare, which is currently residing at 5.0%.

• As InsurTech can enable greater insurance penetration through increased collaboration and ease of access, the insurance gap of 2.1% of GDP can be reduced.

• Disruptive technology-based digitally integrated business models can facilitate the whole financial ecosystem while enabling the financial industry to contribute to achieving SDG goals through financial inclusion.

• As the insurance industry has always been suffering from trust issues among its customers, InsurTech can increase transparency and accountability of the insurers and help in building more intimate relations with the customers through increased direct communication.

• InsurTech can enable the insurers to design and deliver customer-centric services through a well-established integrated value chain, which is not currently possible through contemporary insurance products.

• Because of the increased transparency and well-connected ecosystem, InsurTech can also increase the control of the regulators which, in turn, will result in more coordination among the decision-makers and integrated policies driving towards holistic development and prosperity.

Despite having an economic slowdown projected in 2021 and the aftermath of the slowdown can take a few more years to overcome, the insurance industry has a significant potential that it can achieve through a vigorous transformation. Regulatory reform should also be in the focus to protect the insurers as well the customers and the relevant members of all economic strata.

..................................................

The writer is additional managing director & company secretary of Green Delta Insurance Company, managing director, GD Assist and In-charge, PABL. He can be reached at ahmed.moin@green-delta.com

© 2026 - All Rights with The Financial Express