![]() Before getting down to writing this article, I decided to conduct a small survey in the nearby supermarket from where I buy my groceries regularly. Danube is one of the largest supermarkets in Jeddah and they have branches all over Saudi Arabia. We have one such branch next to our housing compound. To get an idea how large one such Danube branch is, you can just assume it is three times larger than an average Agora store in Dhaka.

Before getting down to writing this article, I decided to conduct a small survey in the nearby supermarket from where I buy my groceries regularly. Danube is one of the largest supermarkets in Jeddah and they have branches all over Saudi Arabia. We have one such branch next to our housing compound. To get an idea how large one such Danube branch is, you can just assume it is three times larger than an average Agora store in Dhaka.

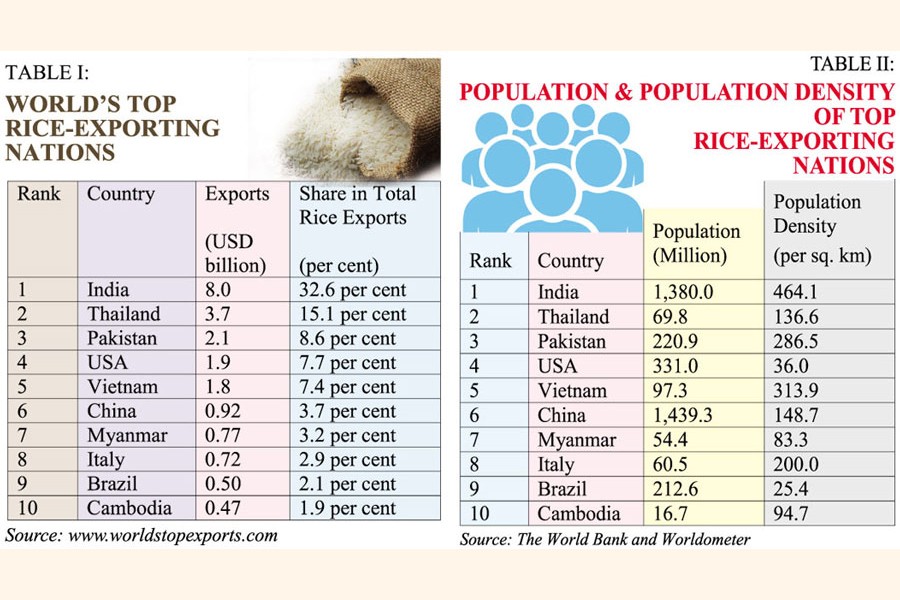

I went straight to the section where packets of rice are stored for the customers. I started counting all the brands available in that section and also looked into their origins. Surprisingly, 49 out of 88 rice brands (55.6 per cent) were actually imported from India!!

Pakistan stood second with 9 brands (10.2 per cent) and the USA third jointly with Italy with 6 brands (6.8 per cent). Brands of some other countries, such as, Italy, Vietnam, Spain, Thailand, Egypt, and the UK were also available, but in smaller numbers.

This very small survey in only one branch of a supermarket chain in Saudi Arabia might not be representative of the actual global scenario because marketing a product is completely a different ball game compared to the production. To make a product competitive on the export market, there is a need for considering various other factors, such as, transportation cost, fiscal advantages offered by the government, taxes and, above all, the availability of surplus. Geographically India is very near to Saudi Arabia, and thus, one may argue that the presence of Indian rice varieties in Saudi markets might not be a matter of surprise if we consider all the above-mentioned factors.

However, the global scenario of rice exports is almost similar to what I found in this very small survey. Those who are aware of global rice trade know very well that Indian varieties of rice are not only widely available in Saudi Arabia, these are also available all around the world. In 2020, India topped the list of rice exporters with an export revenue of over USD8.0 billion, occupying a share of almost 32.6 per cent of global rice exports. Thailand, the second in the position, fetched USD3.7 billion, way lower than India (Table I). Pakistan and the USA occupied the third and fourth positions respectively. India’s overall export of agricultural products is also one of world’s largest. In 2019, India stood ninth with a share of 3.1per cent in global agricultural exports, according to World Trade Organization (WTO) Report on Trends in World Agricultural Trade in Recent 25 Years.

However, the global scenario of rice exports is almost similar to what I found in this very small survey. Those who are aware of global rice trade know very well that Indian varieties of rice are not only widely available in Saudi Arabia, these are also available all around the world. In 2020, India topped the list of rice exporters with an export revenue of over USD8.0 billion, occupying a share of almost 32.6 per cent of global rice exports. Thailand, the second in the position, fetched USD3.7 billion, way lower than India (Table I). Pakistan and the USA occupied the third and fourth positions respectively. India’s overall export of agricultural products is also one of world’s largest. In 2019, India stood ninth with a share of 3.1per cent in global agricultural exports, according to World Trade Organization (WTO) Report on Trends in World Agricultural Trade in Recent 25 Years.

One year later in 2020, India’s exports of agricultural products even grew by 17.34per cent to USD41.25 billion. Despite the economic slowdown caused by the Covid -19 pandemic, such export numbers and associated growth are simply impressive.

One may point out the fact that India is a large country with significant arable land, and therefore, one should not be so surprised with such astounding export figures. To such skeptics, we point out the fact that India also has one of the largest populations in the world. Having a total population of over 1.38 billion, India’s population density is the highest amongst all the top rice- exporting nations (Table 2).

So India’s significant exports of agricultural products mean that after feeding 1.3 billion people every day within the country, India is generating sufficient surplus of food to feed the people of other nations as well.

This is a remarkable achievement, and it should raise anybody’s eyebrows. To attain such a high competitive position in the domain of agriculture, India must have done something differently compared to other countries. They must have planned many things ahead of others and eventually made their farmers so efficient who collectively brought for India this astounding feat

The main objective of this article is to find out one such area of agriculture where India did something different. This is the area of “Agricultural Product Marketing”. In this article, we shed light on the aspect of Indian regulated crop- marketing system, which is much different from the rest of the world where free economy rules the roost.

A bird’s eye view of a regulated market in India

In India, the concept of regulation for marketing crops originated from the British Empire during the pre-independence era when Berar Cotton and Grain Market Act came into force in 1887. Following the passing of this new regulation, Royal Commission on Agriculture was formed, whose recommendations in 1928 also contributed to the development of regulatory culture in crop marketing in the erstwhile undivided Indian subcontinent. These regulations underscored the fact that farmers needed state support to obtain a fair price of their produce from the market.

Inspired from this inherited knowledge, the Government of India enacted Agricultural Produce Markets Regulation (APMR) Acts in various states under which the operations of various market yards were brought under state regulations. During the sixties and seventies, new market yards were constructed under the same regulation, and for each market yard, Agricultural Produce Market Committee (APMC) was constituted to frame the rules and enforce them.

These regulated markets, popularly known as Mandis in local language, required the potential traders to buy produce directly from the farmers under a rule-based system where margins of profits could be monitored and controlled by the APMC.

Although in theory, the farmers of a specific locality were required to sell their produce only through these regulated market yards, but in reality, farmers were free to sell their harvest wherever they wanted. As a result, two parallel marketing channels evolved throughout India since her independence— one was regulated and the other was free and open market.

Such a competition between two competing marketing channels actually benefitted the farmers in the long run. They could fetch more prices for their harvests, which could have been otherwise impossible without two parallel marketing regimes.

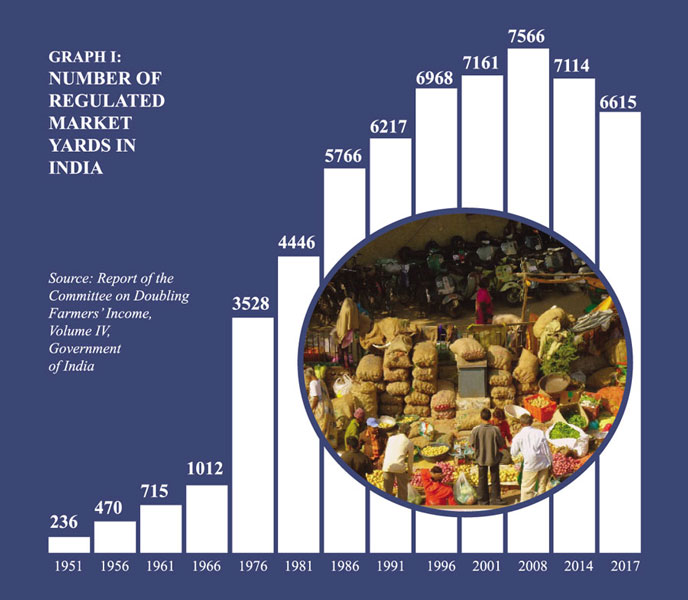

The benefits of having regulated markets are evident from the growth in total number of such markets all over India during the past few decades.

In 1951, when the total number of regulated markets was only 236, it increased to 6,615 by the end of the 2017 (Graph I). India would not have seen such an impressive growth in numbers of regulated markets if the farmers were reluctant to sell their crops through this controlled channel.

This regulated system went through various modifications and changes during the last few decades. After analyzing various weaknesses of the system, the Government of India brought reforms through the Model APMC Act 2003, and later, through the Model APMC Rules 2007.

Eventually in 2016-17, a further review of the existing marketing system was carried out, and as a result, the Ministry of Agriculture & Farmers’ Welfare formulated The Model Agricultural Produce and Livestock Marketing (Promotion & Facilitation) Act 2017 (APLM). Therefore, Indian experts learnt lessons through trial and error and implemented them accordingly through appropriate modifications of this century-old system.

Today some of these regulated markets are Principal Markets with large infrastructure and facilities, and the rest are relatively smaller-scale Sub-Market Yards. Besides these, there are also 22,000 Rural Periodical Markets (RPMs) all over India.

Bird’s eye view of a Regulated Market in India: The regulated markets have all the facilities and infrastructure to help the farmers to sell their produce at ease. These include auction halls, weigh bridges, warehouses for storing the crops, shops for retailers, cafeteria, roads, lights, drinking water, police station, post office, bore-wells, farmers’ amenity centre, tanks, water- treatment plant, soil-testing laboratory, toilet blocks etc.

In 2017, an assessment was carried out to determine the number of additional regulated markets needed to meet the demand of the farmers, and it was found that 3,568 more regulated markets were needed to be set up in various states of India. This shows that despite having the options of selling the crops freely through open markets, the farmers see distinctive advantages to trade through this regulated mechanism.

Since the Independence in 1947, the Government of India has maintained consistent focus on agriculture to ensure sustained growth of the entire sector. As mentioned earlier, the recommendations put forward by the Royal Commission of Agriculture in 1928 were seen as an important step forward to resolve the issues centering around agricultural sector.

Taking the lessons from the British- era policymaking culture, the Government of India also brought together all the experts in1970 to form National Commission on Agriculture to have a renewed look at the sectoral problems and finding solutions.

The Commission released its report in 1976, where the agricultural sector was analyzed in a comprehensive manner by including not only the crop production but also land and water management, animal husbandry, fishery and forestry.

Again in 2004, the Indian Government formed National Commission for Farmers to look into the sectoral past growth and analyze all the issues involved in the context of new millennia.The Commission in its final recommendations released in 2006 focused areas such as land reforms, soil testing, augmenting water availability, agriculture productivity, credit and insurance, food security and, above all, the farmers’ competitiveness.

The Commission noted upon ten major goals which included a minimum net income to farmers, mainstreaming the human and gender dimensions, attention to sustainable livelihoods, fostering youth participation in farming and post-harvest activities, and brought focus on livelihood security of farmers. The need for a single market in India to promote farmer-friendly home markets was also emphasized.

Again in 2017, the Government of India formed Committee on Doubling Farmers’ Income in order to bring the issue of farmers’ income to the centre stage of all discussions. Led by Mr Ashok Dalwai as its Chairman, the Committee brought together more than 100 experts from the Government, Non-Government, Academics, Farmers’ Organizations Professional Associations, Business Organizations, Consultancy Bodies etc to find the right strategies for doubling the income of Indian farmers within the next five years.

The Committee released its findings and recommendations in fourteen volumes, each containing hundreds of pages. In Volume I of the Report, the Committee started the discussion with an in-depth analysis of the current state of Farmers’ Share in Consumer Prices (FSCP) in various crop categories to identify the constraints to increasing it further.

In Volume 4 titled “Post-Production Interventions: Agricultural Marketing”, the Committee members looked deeper into the problems of existing marketing system in the entire Indian agricultural market. Amongst many other recommendations, the Committee members also suggested developing a new marketing model under which facilities will be established under “Hub and Spoke” format to trade crops amongst the farmers, traders and the ultimate consumers. An illustration of this proposed model is presented in the following diagram.

Proposed “Hub and Spoke” model for crop marketing: So one can readily understand that India’s present success in the agricultural sector and the ability to generate more than USD40 billion export earnings every year does not fall from the sky.

It required decades of continuous attention to understand the sectoral problems and identify solutions in a pragmatic manner that suited the local culture, the mindsets of the farmers and, above all, the needs of the community.

While recommending a set of solutions, the Indian experts must have taken lessons from best practices followed in other countries, but never forgot the ground reality. This is the secret of their success.

LESSONS FOR BANGLADESH: Now the big question is what Bangladesh can learn from India. Before answering this question, let us review the ongoing practice of how development plans are formulated in Bangladesh.

Every five years, the Planning Ministry of the Government of Bangladesh starts drafting Five-Year Plan for the country to chalk out the roadmap for the future. The Planning Ministry invites all other ministries to submit their recommended policies and strategies that would be included in this roadmap. Ministries in turns invite experts in related fields to put forward their recommendations.

If anyone reviews such five-year plans that come out through this rigorous exercise, one would readily identify a very common trend. Each of these planning documents has hundreds of pages covering all the sectors of the economy. But, instead of having a clear strategy outlining “how” the problems should be resolved, the associated chapters have many pages illustrating the trends showing what happened in the past, and only few pages covering in a very broad manner what should be done next.

If you don’t trust my words, then I would draw your kind attention to the most recent Five-Year Plan that is available on the Planning Commission’s website. The 8th Five- Year Plan that is applicable for 2020-2025 has 849 pages in total, and of these pages, 51 (page No 287-338) were dedicated to analysing the state of agricultural sector and outlining the strategies for moving forward.

In these 51 pages of discussion about the country’s agriculture, while outlining the challenges of the crop sub-sector, the policy planners underscored many issues, such as, low productivity, research and development, climate change, depleting groundwater, land crisis etc but they missed the most crucial area, i.e., the issue of farmers’ income and profits. It is not even stated as a challenge of the sector.

In Section 4.3.3 (Page 296), while discussing the “Strategies for Crop Sub-Sector during the 8FYP”, the planners dedicated only three sentences to addressing the issue of farmers’ income. These three valuable sentences are: (1) Increase farmers’ capability and income through institutional infrastructure development and efficient technology services (2) Provide assistance to the farmers in increasing agricultural production and ensuring marketing facilities of agricultural commodities and obtaining fair prices, and (3) Enhance farmers’ income and livelihood through Holistic Farming System Approach (HFSA) with special emphasis on productivity enhancement of homestead areas.

In later sections, the planners pointed out detailed action plans to implement the strategies outlined in the beginning. However, no detailed analysis is provided to show how the farmers’ income will be increased and their profits will be ensured during the next five years. The chapter also failed to even identify that farmer’s income and profits is at all an issue for detailed discussion.

The same picture is also evident in “Making Vision 2041 a Reality: Perspective Plan of Bangladesh (2021-2041)”, the long-term roadmap that is supposed to make Bangladesh a high-income nation by the end of 2041.

Our farmers will be delighted to find out that on page 74, only two sentences were dedicated in order to address the issue of their income and profits. These are: (1) Rules and regulations will be enacted to ensure that farmers are getting real benefits for their sweat-toiling agricultural products, and (2) Price of agricultural products at the farm level will be maintained in such a way that the farmers get fair prices.

But nowhere in the entire document would one find what these rules and regulations will be and how the price of agricultural products at the farm level will be maintained to ensure fair prices.

We are not aware of any other planning document where this very important issue of farmers’ profits has been analyzed in detail in Bangladesh’s context. We are also not aware of any past Commission formed that went deep into the problems of the agricultural sector and tried to find solutions.

We proposed a detailed Mega Model titled “Bangladesh Accelerated Poverty Reduction Model (BAPRM)” that is more comprehensive compared to “Hub and Spoke” Model and more efficient than the existing regulated market system in India. Our model offers a delicate balance between the market forces and government controls and it resolves all the weaknesses of the Indian regulated market regime (All the the articles under the same series are available at www.ideasfd.org).

This year, with the writing of this article, which is most probably the last part of the series, we would like to conclude the discussion with a set of concrete recommendations

In the context of the detailed discussion above and the articles already published in the Financial Express since 2018, we draw the kind attention of the high-level policymakers, academics, civil- society leaders, journalists, farmers, and above all the general people to take note of the following recommendations:

•The issue of ensuring fair price for the farmers should be brought into the centre stage of all discussions if we wish to sustain the growth of agricultural sector of Bangladesh. Unless this is done, all the policies and strategies targeted for the development of this sector will not see the desired results.

• The current state of farmers’ profits and their share in consumer prices should be analyzed periodically to understand the dynamics of the market and appropriate strategies should be developed to address all the constraints to strengthening the bargaining power of the farmers.

• National Commission on Agriculture should be formed once in a decade, comprising sector experts and all stakeholders. The job of this Commission will be to dive deep into the sectoral problems, analyze the best global practices, and put forward recommendations that would meet the demands of the farmers.

END NOTE: India is not only surrounding Bangladesh geographically, India is also influencing the minds of our citizens in different modes and manners.

We are quite habituated to having Indian onions on our lunch and dinner table every day, without which the price of this essential skyrockets overnight.

Our ladies are very much fond of Indian saris and it has become a norm for wealthy families to pay visit to Kolkata for buying this item before important family occasions.

Our daughters become crazy for Pakhi Dresses before Eid festivals that make them Kareena Kapoor double.

Our wives spend their idle time watching Hindi Serials that also influence their behaviours with their in-laws and husbands.

Glamourous Indian actresses frequently visit Bangladesh to take part in the roles in Bangladeshi movies, a trend that nowadays is moving towards the opposite direction.

Our literary experts received awards in the past from India for their scholarly works.

We have borrowed so much from India since our independence in 1971, but it is a matter of regret that we failed to borrow the most important aspect of Indian economy that could make us prosperous and developed by now.

Mabroor Mahmood is the Founder of IDEAS FOR DEVELOPMENT (IFD).

He can be reached at ideasfd@gmail.com

© 2026 - All Rights with The Financial Express