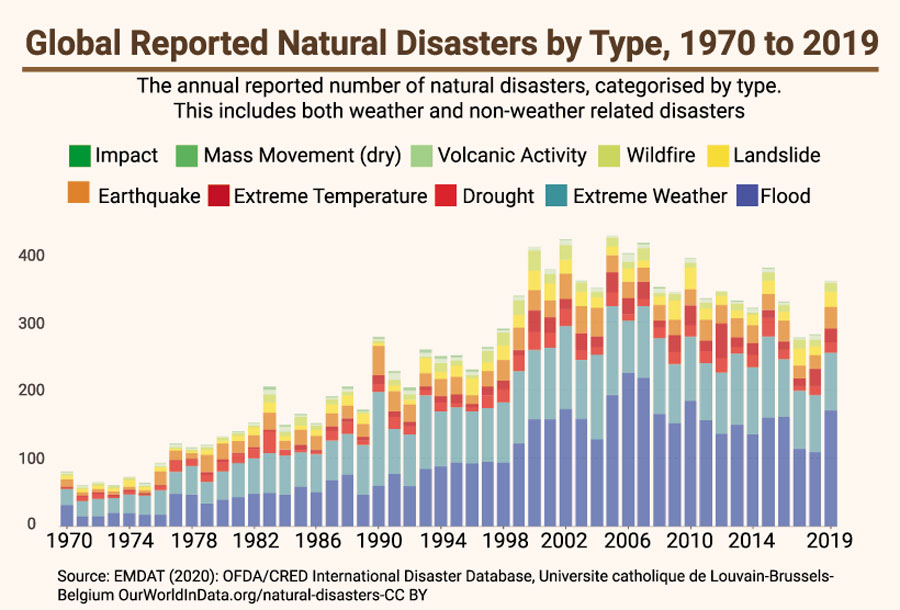

As an instance, while contributing less than 0.47 per cent of global Green House Gas (GHG) emissions, Bangladesh is reported to be one of the most vulnerable countries prone to adverse weather impact that has degraded natural habitats and increased the population's economic hardship, which is again a major barrier to the sustainability of development milestones achieved so far. Therefore, this community is enduring exactly the kind of future that the COP26 climate conference in Glasgow tried to avoid. Building on a motto of net-zero equation, the 26th session of the Conference of the Parties (COP26) of the United Nations Framework Convention on Climate Change just held in Glasgow, Scotland, tried to address the pressing global issue of climate change, global warming and increase in global carbon footprint. For instance, the graph of natural disasters show that natural calamities' trends have been

Therefore, this community is enduring exactly the kind of future that the COP26 climate conference in Glasgow tried to avoid. Building on a motto of net-zero equation, the 26th session of the Conference of the Parties (COP26) of the United Nations Framework Convention on Climate Change just held in Glasgow, Scotland, tried to address the pressing global issue of climate change, global warming and increase in global carbon footprint. For instance, the graph of natural disasters show that natural calamities' trends have been

The country began its journey with the agenda to implement the SDGs having 17 goals and 169 targets, in response to a universal call to action to end poverty, to protect the planet and ensure that all people enjoy peace and prosperity. Building on the successes of MDGs, these goals include new areas such as climate action (SDG 13), economic inequality, innovation, responsible consumption, and peace and justice, among other priorities. The goals are interconnected - often the key to success on one will involve tackling issues more commonly associated with another.

The government has adopted 'Whole of Society' approach to ensure wider participation of NGOs, development partners, private sector, financial institution, media and CSOs in the process of formulation of the Action Plan and implementation of the SDGs. This whole-of-society approach incorporates wide range of policies such as Vision 2041, Intended Nationally Determined Contributions (INDC) and reduction in GHGs.

Therefore, in order to attain the milestones of the intended policies, financial sectors are recognized as the key promoter of sustainable growth through catalyzing environment-friendly financing. As such, to align Sustainable Financing with SDGs, the banking sector of Bangladesh is playing the pivotal role as it is the dominant source of financing in the country. In this respect, Bangladesh Bank[BB], the Central Bank of the Country, has done a commendable job in bringing a meaning and introducing local banks to the world of Sustainable Financing. Starting from establishing the Green Banking Policy for banks in 2011 to journey towards the more rigorous Sustainable Finance Policy in 2020, BB also introduced the green-finance taxonomy in the country for the first time.

After its introduction, BB began a comprehensive green-banking initiative to support environmentally responsible financing, issuing guidance for the environmental-and social-risk assessment in lending and for the greening of internal processes and practices within banks and FIs. These green initiatives incorporate financing in green products, sustainable agriculture, sustainable CMSME, renewable and alternative energy and liquid waste management to name a few.

In the light of this, BB introduced the first-ever Sustainability Rating for the banks in Bangladesh, which incorporates aggregate score for five parameters of the bank: Sustainable Finance, Green Finance, CSR, Core Banking Sustainability and Banking Service Coverage.

In 2020, City Bank Limited became one of the top-rated sustainable banks as per published Sustainability Rating. This is a prestigious rating, uplifting image of the bank locally and to overseas counterparts. As such, this is a mechanism in order to facilitate and motivate banks to rethink their investment policy and integrate sustainable financing in their core lending mechanism, and must be a part of KPI of lending officer.

In this way, they can benefit from increased goodwill, enhanced brand value, and, on the other hand, be involved with responsible banking and ensure sustainable growth.

However, such green initiatives will only prove to be sustainable if we address and funnel down the main obstacles of financing sustainably from two ends of a spectrum: The demand drivers and supply dynamics. The generation of financing for sustainable business activities will only be significant if the entrepreneurs experience both monetary and non-monetary benefits behind it. Asserting that each and every one of economic activities is done in environmentally sustainable way needs investing huge money, which ultimately will result in additional expenditure. This can be done from moral obligation to a certain extent, but, this additional expenses need to be compensated by tax rebate, tariff benefits or any other financial gains for cementing its progress.

Another side to this demand dynamic is incorporating other sub-sectors that are helping reduce carbon footprint to accommodate a wide range of entrepreneurs under the benefits of green refinance scheme. The central bank has set a target of 20 per cent of total loan disbursements under sustainable financing within which 5.0 per cent as green finance against long-term- loan disbursements of banks/FIs. Many financial institutions can already meet this target with 'indirect green lending' to entities that are helping conserve the environment but not necessarily in the categories enlisted under green financing.

Furthermore, to build sustainability into broader efforts reduced transaction costs and simplified due-diligence process required for entities seeking investment for green and sustainable projects. Developing facility-driven products with friendly interface and requirements will result in faster need and subsequent quick disposal and disbursement of sustainable financing.

In addition, overall banking operations also need to be brought under digital governance to reduce carbon emission. Banks' trade operations and regulatory reporting are still heavily paper-based. These cause waste of energy as well as contribute to increased carbon footprint. Thus, to ensure more sustainable growth with lesser carbon emission, a wholesale change is needed by simplifying process and regulations and bring it under the umbrella of digitalization.

This brings us to the other spectrum of the challenge -- the supply dynamics. That is, FIs and banks' effective lending to entities that are operating in environmentally responsible way. The capability and capacity of entrepreneurs need to be assessed by competent authority to find out whether green funds are properly used in environmentally viable way. In order to do so, huge resources need to be deployed in the form of manpower and infrastructure, which still need to be addressed efficiently by our country. Monitoring each and every production unit of our country and finding out whether they are operating as per said norms and having all eligible regulatory documents is a very meticulous job, and this is another sticking challenge of present times. This is because, without proper monitoring, no system and practice can foster sustainably.

Therefore, having addressed both ends of spectrum, we can conclude that environment and social risks are integral part of assessing credit risks. Banks/FIs must not lend to factories or businesses which are polluting the environment and causing damage to air, rivers, lands, biodiversity and, thereby, risking sustainability of economic and social developments in the future. Lenders shouldn't be accomplice for damaging the climate. We need to be mindful of the fact that we need the earth for our survival but earth doesn't need humans -- we are just one species among millions of species. And there is no vaccine available for climate's adverse change.

Thus, bankers must embrace sustainable and green finance from today, not tomorrow. Time is running out. We need to act. When we act, hope is all around us.

Mesbaul Asif Siddiqui is currently working as the head of Credit Risk Management & Gultekin Binte Azad is working as the risk manager of Credit Risk Management at The City Bank Limited.

mesbaul.asif@thecitybank.com, gultekin.binte@thecitybank.com