The need for setting up Integrated National Financing Framework (INFF) to finance SDGs in developing countries was agreed as Addis Ababa Agenda 2015. The agenda has become more pronounced in the COVID context whereby the ODA either reducing or are likely to reduce significantly. Under this situation, transformation towards "Financing for Development" from "Funding for Development" in line with the "Financing for Development Initiative (FFDI)" taken in 2020is inevitable.The shift from funding to financing SDGs essentially means, increasingly extracting financing through investment, business benefits, engagement of private sector creditors and public debt efficiency for meeting SDGs instead of depending heavily on ODA and donors'funding. As per ILO's report on World Employment and Social Outlook: Trends 2020, almost 492 million full time equivalent jobs were lost from 2020 to mid-2021. Relative to 2019, an estimated additional 108 million workers are now extremely or moderately poor distorting the five years of progress towards the eradication of working poverty and reverting to the status 2015.Therefore, generating employment and reviving inclusive economic growth that fall under SDG 8 will be the major challenge for countries to overcome in the post COVID era. This unprecedented crisis in the job market and inclusive economic growth amplifies the investment and financing needs for SDG 8 more than any other

As per ILO's report on World Employment and Social Outlook: Trends 2020, almost 492 million full time equivalent jobs were lost from 2020 to mid-2021. Relative to 2019, an estimated additional 108 million workers are now extremely or moderately poor distorting the five years of progress towards the eradication of working poverty and reverting to the status 2015.Therefore, generating employment and reviving inclusive economic growth that fall under SDG 8 will be the major challenge for countries to overcome in the post COVID era. This unprecedented crisis in the job market and inclusive economic growth amplifies the investment and financing needs for SDG 8 more than any other

Now, let us focus on the financing gap for SDG 8 in Bangladesh aligned with the global context I have explained so far. As of 2018 in a Business as Usual (BAU) scenario, Bangladesh is facing a significant financing gap worth 928.48 billion USD for financing SDGs. COVID-19'snegative impact on the macroeconomic confounding factors distorts BAU assumptions for SDG financing. In this article, I will analyse the financing needs for SDG 8. The global narrative explained earlier gives us a hint that financing for SDG 8 should get the highest priority when we speak of financing SDGs, especially for countries like Bangladesh that is on the verge of graduating from the LDC status to avoid middle income trap.

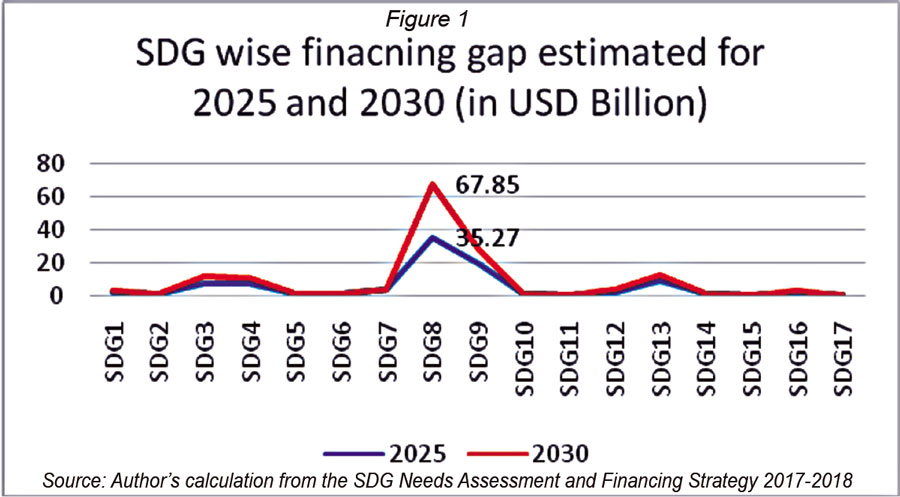

I will start by analysing the financing gap for SDG8 in a BAU case as per the calculation of 2017-2018 SDG Financing strategy. The following figure reflects the SDG wise financing gaps in BAU for 2025 and 2030.

Figure 1 clearly reflects that in a BAU scenario, SDG 8 or decent work agenda will face the highest financing gap in 2025 and in 2030by far margins compared to all the other SDGs. Indeed, as we observe the trends, all the other SDGs are facing financing gaps within the range of 1-10 Billion USD for both the time thresholds 2025 and 2030. However, SDG 8 will be facing a financing gap of 35 billion USD in 2025and 65.85 billion USD in 2030 that is twice the gap of 2025. The estimated financing gap in 2030 for SDG 8 is almost 7 times than the financing gap for other SDGs (individually) in 2030. One must remember that we are still exhibiting and analysing the financing gaps for SDG8 compared to all the SDGs in a BAU scenario.

Some of the major assumptions for SDG financing under the BAU case were; i) annual GDP growth rate to be 8.5 per cent in 2025 and 9 per cent for 2030; ii) inflation rate will be more or less similar until 2030; and iii) employment growth rate was calculated from 2010-2013 baseline and was assumed constant or non-decreasing until 2030. However, the economic crisis due to COVID-19 brings significant divergence from the BAU assumptions and new benchmarking macroeconomic indicators leading towards a larger financing gap for SDG 8.

To dig deeper in the shocks on BAU situation let usassume some of the deviations and their impacts on financing gap for SDG 8. For instance, the annual GDP growth rate for 2021 is recorded somewhere near-about 5.5 per cent to 6 per cent. However, in the SDG financing strategy, the annual GDP growth rates wereestimated to be 8.1 per centin 2021, 8.5 per cent in 2025 and 9 per cent in 2030. By inducing the current annual GDP growth rate and synchronizing the COVID-19 recovery trends for the last year, we investigate two possible cases. First case is the optimistic case, where the economy will recover reasonably but not fully with somewhere near 7.8 per cent annual GDP growth rate in 2025 and 8.4 per centgrowth rate in 2030. The second case is the pessimistic case, where the annual GDP growth rates will reach up to 7.5 per cent and 8.1 per cent respectively in 2025 and in 2030. Holding other things constants, financing gaps for other SDGs constants and relaxing the synchronized cost analysis for the interconnected SDGs, we find the following financing gaps for SDG 8 for both the cases.

Figure 2 depicts SDG 8 COV as the optimistic scenario and SDG 8 COV' as the pessimistic scenario. In both the scenarios, we see a huge increase and jump in financing gap for SDG 8 for 2025 and 2030. In the pessimistic scenario, the financing gap is estimated more than twice the gap of BAU scenario for worth 148.43 billion USD. This exercise surely has limitations as it assumes other things remaining constant and relax the synergies in estimating the costs for interconnected SDGs. However, this is a simple and helpful estimation to understand how financing gap for SDG 8 will increase due to pandemic's economic impacts and why financing for SDG8 should the top most priority for Bangladesh when we speak of SDG financing. As per studies in Bangladesh, around 25 million employed people became jobless due to COVID-19 within a year. Therefore, the Business as Usual (BAU) assumption of having a constant (average) employment growth rate until 2030 is certainly an unlikely case for the country. Adjusting for these employment shocks and recovering the lost jobs will require huge financing in order to create jobs, enterprises and businesses to achieve the targets of SDG 8 by 2030.

To meet the financing gap for SDG 8, I recommend four policy interventions. First, active and robust engagement of the private sector for increased investment in establishing and/or scaling up SMEs and microenterprises linking with manufacturing industries and global value chain. This will increase the manufacture-based production resulting in increased numbers of job creation and improved productivity. Second,integrating financial inclusion not as a cross cutting instrument but as a core component of active labour market policies (ALMPs) such as skills development programs. Innovative financial services and products such as digital wage payment system, access to credit for start-ups and business scale up, SDG bonds, green bonds and impact insurance can increase the self-employment opportunities and can offer informal/formal jobs for many. Third, attracting FDI for high growth sectors with a special focus on women and youth, and having the appropriate policy, institutional set up and regulatory framework. Fourth, channelling remittance money towards new businesses and impact investment ventures. However, formulating and implementing these recommendations will be difficult without appropriate policy and regulations in place.

All the analyses here represent the author's personal point of view and concept.

Mohammad Nazmul Avi Hossain, Labour Economist, currently working as a Programme Officer at the SDG Finance Unit, ILO, Bangladesh