Farmers harvest their winter vegetables at a field in Bangladesh — FE Photo

Farmers harvest their winter vegetables at a field in Bangladesh — FE Photo ![]() It goes without saying that we now live in an uncertain world. Policymakers, both global and national, are regularly sounding words of caution about uncertainty in the global economy, which is going through a rollercoaster experience. The World Economic Outlook (WEO) portrayed by the International Monetary Fund (IMF) is being changed on its own regularly to catch up with the fast-deteriorating global economic landscape. The latest projection has been given in the October 2022 Outlook. It says that global economic activities are experiencing a 'sharper-than-expected' slowdown alongside inflation as high as not seen in decades. This dismal outlook is, as indicated by the IMF, owing to "the cost-of-living crisis, tightening financial conditions in most regions, Russia's invasion of Ukraine, and the lingering COVID-19

It goes without saying that we now live in an uncertain world. Policymakers, both global and national, are regularly sounding words of caution about uncertainty in the global economy, which is going through a rollercoaster experience. The World Economic Outlook (WEO) portrayed by the International Monetary Fund (IMF) is being changed on its own regularly to catch up with the fast-deteriorating global economic landscape. The latest projection has been given in the October 2022 Outlook. It says that global economic activities are experiencing a 'sharper-than-expected' slowdown alongside inflation as high as not seen in decades. This dismal outlook is, as indicated by the IMF, owing to "the cost-of-living crisis, tightening financial conditions in most regions, Russia's invasion of Ukraine, and the lingering COVID-19 pandemic…".

pandemic…".

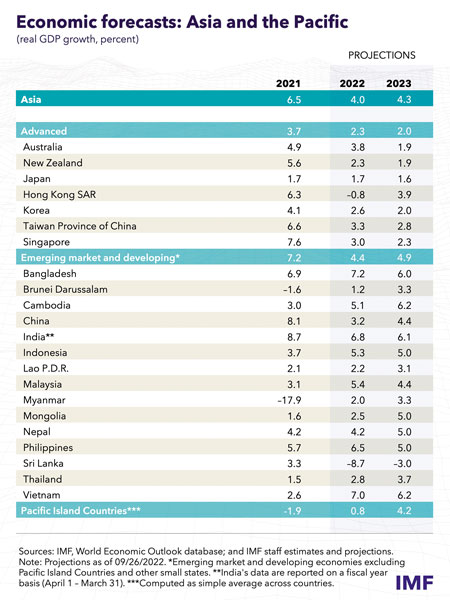

According to the 'Outlook', global growth will likely slow down to 3.2 percent in 2022 compared to 6.0 percent in 2021. The forecast for 2023 is even more disappointing. The growth will be 2.7 percent. The report argues that this is "the weakest growth profile since 2001 except for the global financial crisis and the acute phase of the COVID-19 pandemic." The forecast for global inflation is equally disturbing. This is forecast to rise to 8.8 percent in 2022 compared to 4.7 percent in 2021. However, it is projected to climb down to 6.5 percent in 2023 and then 4.1 percent in 2024.

Speaking regionally, the advanced economies will shrink to 1.1 percent in 2023 compared to 2.4 percent in 2022. While the emerging market and developing economies are expected to hold their average growth at 3.7 percent in both 2022 and 2023, much lower than 6.6 per cent in 2021.The two leading economies of the group will face a significant slowdown. India will slow down to 6.8 percent in 2022 compared to 8.7 percent in 2021. The outlook for 2023 is even worse (6.1 percent). China's growth outlook is equally dismal-- 3.2 percent in 2022 compared to 8.1 percent in 2021. The scenario is slightly better for 2023, with a 4.4-percent growth rate.

Bangladesh, demonstrating greater strengths on its growth trajectory, has also been affected. According to this Outlook, Bangladesh is expected to grow 6.0 per cent compared to 7.2 percent in 2022. The figure in 2021 was 6.9 percent.The World Bank also slashed Bangladesh's growth rate this fiscal year to 6.1 percent from its earlier projection of 6.7 percent. The Asian Development Bank also readjusted Bangladesh's growth rate to 6.6 per cent from its earlier projection of 7.1 percent. The government has, however, an ambitious projection of 7.5 per cent for this fiscal year which will certainly be scaled down given the impacts of the global economic crisis. Its projection may not be less than 7.0 per cent.

Even the projections of various international organizations now look ambitious, given the economic turmoil created by higher inflation (likely to average out at 8.5 percent in the current fiscal year), energy shortages, the stronger dollar, the slower pace of recovery from the pandemic, and of course the war in Ukraine further disrupting the supply chains. The situation still looks highly uncertain, and we don't know when the Ukraine war will end.

Given these external headwinds, it is unlikely that our economic growth can improve further. Rather, given the external shocks, uncertainty in the balance of payments, slowing export and remittance earnings, and rapidly deteriorating power situation, we should be happy with the six- percent growth, if we can achieve it. We must also keep in mind that the worst is yet to come, as cautioned by Pierre-Oliver Gourinchas, editor of the IMF Economic Review. We must not fall into the trap of propping up the GDP-growth rate at any cost, as has been the case in the UK, where there was a clear mismatch between monetary and fiscal-policy goals. An ill attempt at going back to Thatcherism by proposing a drastic cut in the taxes for the rich at a time when the Bank of England was deeply engaged in tightening monetary policy to rein in inflation proved to be self-inflicting for the new government. The Central Bank hurriedly intervened and saved the situation.

However, with the significant depreciation of the pound sterling against the US dollar, inflation, including food-and energy-price hikes, remains a serious matter of headache for UK policymakers. Indeed, we can learn a lot from the macroeconomic policy disaster of the UK. Learning from the policy blunder from the UK, Bangladesh must go back to the drawing room and refocus on the macroeconomic policy parameters to stabilize the same through a balanced approach.

We must, therefore, get back the exchange-rate stability by streamlining the multiple exchange rates into a unified rate that may remain flexible within a small band as allowed by our Foreign Exchange regulations. The incentives provided to various stakeholders may remain for some time.The rate of interest should be made more flexible, as desired by the market, perhaps with some exceptions to promote productive sectors like agriculture which has been the savior during the crisis period. The fiscal policy must reorient itself to focus on tax reforms, including digitization of the system and desired human-resource development. The spending policy must also be reoriented to make it more cost-effective and on target. Overall, the fiscal deficit must be curtailed to reduce demand which has been fueling inflation. Credit growth must be lowered to reduce inflation and the demand for imports. Bangladesh government and Bangladesh Bank have taken prudent initiatives to cut unnecessary public spending and constrain luxury and unnecessary imports. However, despite all this, the trade-and current-account deficits remain very high with a knock-on effect on the foreign-exchange reserves, which is experiencing fast depletion. This pace of depletion of the reserves must be arrested at any cost.

Mind it, we managed to tide over the global financial crisis which originated in the US mortgage subprime leverages in 2008-09 quite well by concentrating our policy support on the real economy without compromising the basic tenets of the Monetary Policy. We focused more sharply on the productive sectors, including agriculture, small and medium enterprises, and the manufacturing sector (mostly export-oriented), to sustain domestic consumption and cater to the demand of foreign customers who were prepared to buy our low-cost apparel. This indigenous development strategy was supported by the innovative, inclusive, and sustainable financing policy of the central bank of Bangladesh. Indeed, the outcomes of this policy push were stunning, with increased growth and moderate inflation. And this was best reflected, for example, in the success of agricultural production and its diversification.

Indeed, the success story of Bangladesh's agriculture has been made possible through several homegrown solutions. Enabling public policies helped mobilize field-level officials who, in turn, ensured quality extension services for farmers and small-scale agricultural entrepreneurs. A significant share of the public expenditure ensured the required power (mainly for irrigation) and infrastructure for bolstering the sector. Also, government efforts for agricultural research and development have been sufficiently complemented by non-government organizations and private- sector actors. All these policy supports have resulted in homegrown solutions implemented at the grassroots and safeguarded the macroeconomy. Infusion of modern technology, modernization of agricultural production, integration of education with the field, continued subsidies over the years, and continued growth of agricultural education have created an enabling policy environment that has fostered robust and sustainable growth of the agriculture sector.

Bangladesh made a heroic comeback in 1996 with Prime Minister Sheikh Hasina forming the government focusing on desired policy planning, prioritizing self-sufficiency in food by investing heavily in agriculture. Food production has quadrupled in the last fifty years, surpassing 40 million metric tonnes. Back in 2008, this was 28.9 million metric tonnes. Bangladesh also made stunning progress in non-cereal food, vegetable, eggs, meat, chicken, and fish production. Bangladesh is ranked second in jute and freshwater fish production, fourth in tea production, and first in Hilsha production. Indeed, Bangladesh has been able to transform itself into a food-sufficient country from its earlier status of food deficit. To give you some concrete examples, the per-capita rice production was 140 kg in 1973 which increased to 240 kg in 2018. This must have crossed 250 kg by now. Similarly, fish production per capita increased from 11kg to 25 kg, meat from 3kg to 44 kg, egg from 15 pieces to 101 pieces, and milk from 6 kg to 58 kg during this period. The figures are now much more robust.

Of course, there are still many challenges in the field of agriculture. The floods in Sylhet and seawater surges in the coastal belt have certainly affected rice production. The higher level of food insecurity in Sylhet and Barishal divisions, as indicated by the recently conducted survey by the World Food Programme, confirms this apprehension. The recovery from the pandemic has also been slower in these areas, with the substantial prevalence of unemployment, lack of purchasing power, and enhanced level of malnutrition. So, these areas need to be prioritized in providing more subsidized agricultural inputs and a higher proportion of social protection.

Luckily, the Aman production has been salvaged by the last-minute monsoon rainfall, which will help sustain moisture in the field for better Boro production. The policymakers and the field officials will have to remain alert in terms of providing all the inputs in time at a reasonable cost. Hopefully, Aman harvest will be more than what we expected, and other winter crops will follow in line if we can provide the necessary support to the farmers. If we can coordinate well, we will be able to avoid the specter of famine in Bangladesh, contrary to what is being anticipated by some of the onlookers of the food landscape.

Certainly, the war in Europe has been affecting the grain supplies to the world. We, therefore, need to procure rice both from within and import from abroad to build up the food stock to nearly three million metric tonnes.The government is aware of this tricky situation and is doing its best to keep Bangladesh food self-sufficient at any cost.

There is no alternative to harnessing the potential of our agriculture to combat the fallouts from the ongoing global financial crisis. To do so, the financial sector must focus on channelling credits into small agricultural enterprises. Following are some ideas that the decision-makers may consider while planning to bolster our agriculture sector amid the ongoing crisis:

a) A special credit programme may be launched to support successful farmers who have received or have been nominated for the Bangabandhu agricultural award.

b) It has already been established that Solar Irrigation Pumps can reduce agricultural production costs and consequently reduce our reliance on fossil fuels to a significant extent. The National budget has allocations for farm mechanization, a portion of which can be channelled for this purpose. Bangladesh Bank can also channel credits for setting up a few hundred thousand Solar Irrigation Pumps across the country from the newly created refinance scheme of Tk 25,000 crore for small entrepreneurs. The fiscal authority can also give its supportive hand to this climate-friendly transformation of rural irrigation system using green energy.

c) Agricultural research has been expedited over recent years. The private sector is also contributing to agricultural research. Targeted Research and Development fund may be launched to encourage agricultural scientists to do more of such research and innovation.

d) There remains significant scope for improvement in the marketing and storage of agricultural products. Fortunately, we now have numerous success stories regarding establishing viable market linkages for farmers and improving storage facilities. Lessons can be learned from these pilot initiatives, and upon due contextualization, these may be scaled up and replicated. While the government itself can take up such projects, the banking sector must also be directed to channel credits to entrepreneurs interested to take up agri-marketing-and storage enterprises.

e) Many of the up-and-coming agricultural entrepreneurs need very small-sized loans, which they find challenging to secure because of not having trade licences. Banks and NBFIs should be directed to provide such 'nano loans' to these agricultural entrepreneurs via agent banking and MFS. Instead of asking for trade licences and/or business accounts, financial-service providers could select whom to give a loan considering the transaction track records (in their regular bank accounts or MFS accounts). This will especially encourage the proliferation of e-commerce in the agriculture sector.

f) Many educated women entrepreneurs are now engaging in (mostly online-based) agricultural enterprises. Bangladesh Bank may think about launching special credit programmes for these emerging women entrepreneurs as well.

g) Bangladesh Bank's start-up fund may also be utilized to bolster emerging agricultural entrepreneurs. The central bank may collaborate with agriculture universities and other researchers to develop a short- to medium-term strategy for promoting agriculture-focused start-ups in Bangladesh.

We have highlighted here the strengths of the agricultural sector with some policy suggestions to address the economic challenges that are looming large in Bangladesh as well. There are similar other success stories in our small and medium enterprises as well. Our recent gains in green finance in making the RMG sector sustainable and work-friendly also deserve to be noted. Finally, we must remain focused on our strengths and weaknesses to tide over the economic crisis imposed on us from outside.

Dr Atiur Rahman is an economist and former Governor of Bangladesh Bank.

dratiur@gmail.com

© 2026 - All Rights with The Financial Express