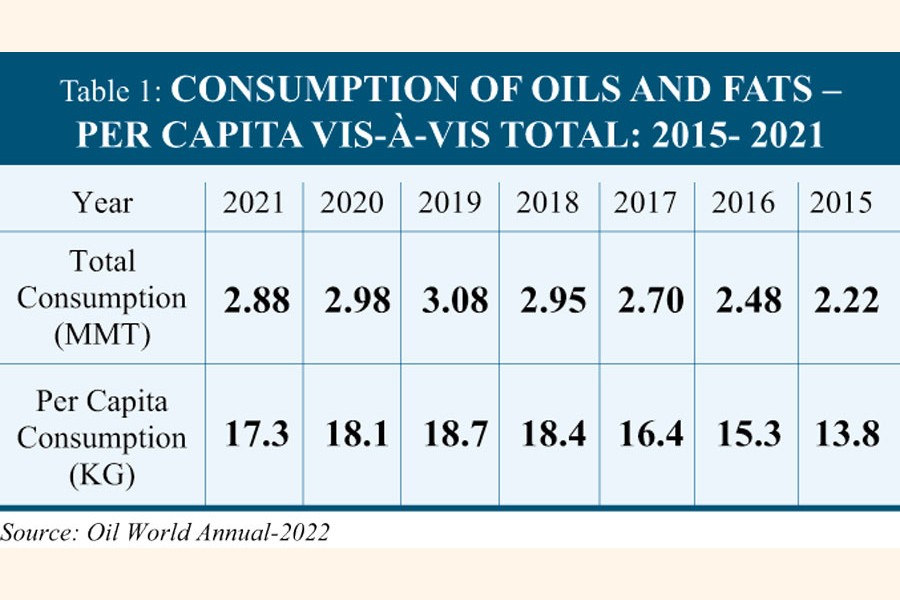

![]() Bangladesh consumed little over 3.0 million tonnes of oils and fats in 2019, the highest in a year. The per-capita consumption increased to 18.7 kilograms, by that account, from 13.8 per cent in 2015. The consumption of oils and fats had been on an upturn since 2015 apace with the country's steady economic advances, improving living standard and food habit. But the COVID-19 came down as a havoc on the consumption of oils and fats like other commodities, and as a result, consumption vis-à-vis import of oils and fats started declining in 2020, which still continues. In the year 2020 annual consumption of oils and fats decreased by 3.24 per cent compared to 2019 level, while it plummeted to 6.49-percent in the year 2021. The trend may be seen in the Table - 1.

Bangladesh consumed little over 3.0 million tonnes of oils and fats in 2019, the highest in a year. The per-capita consumption increased to 18.7 kilograms, by that account, from 13.8 per cent in 2015. The consumption of oils and fats had been on an upturn since 2015 apace with the country's steady economic advances, improving living standard and food habit. But the COVID-19 came down as a havoc on the consumption of oils and fats like other commodities, and as a result, consumption vis-à-vis import of oils and fats started declining in 2020, which still continues. In the year 2020 annual consumption of oils and fats decreased by 3.24 per cent compared to 2019 level, while it plummeted to 6.49-percent in the year 2021. The trend may be seen in the Table - 1.

Most likely, declining trend in consumption of oils and fats would continue in the year 2022 also as the country's economy has yet to recover fully from the dent caused by the COVID-19 pandemic. In addition, new issues, namely, upturn in prices of food commodities, fuels and freight etc as a fallout from the Ukraine- Russia war aggravated the situation further.

Market Overview:

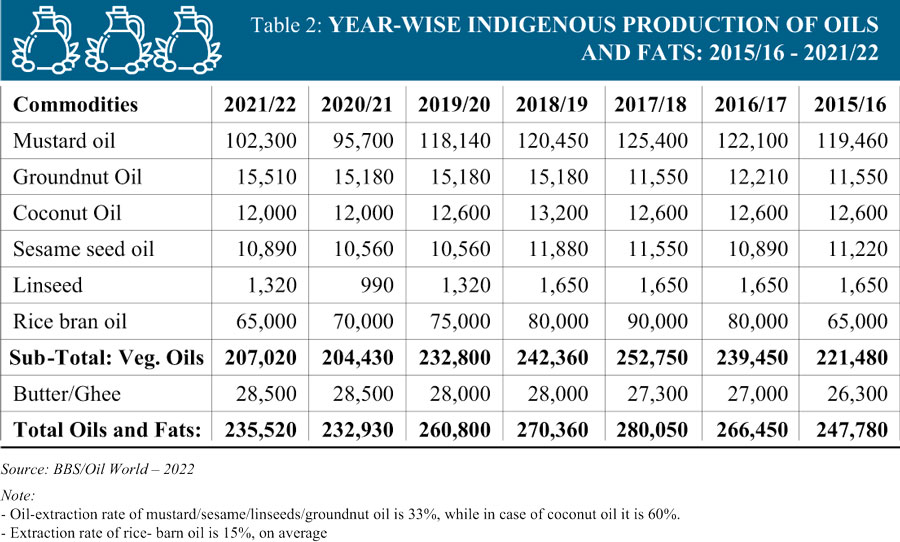

Bangladesh has been deficient in oils and fats since early '60s. It is an overpopulated country with limited land for cultivation of oilseeds. The land for oilseeds cultivation is shrinking gradually due to competition with food and cash crops, which left no other options but to import almost 92 - 93 per cent of country's annual requirement of oils and fats. Local production is about 250,000 tonnes, on average, against the present annual demand for little over 3.0 million tonnes, as of 2019. Among the locally produced edible oils, mustard oil is the major one, which constitutes about 36 per cent of the indigenous production of edible oils. Other kinds are rice-bran oil, groundnut oil, coconut oil, sesame oil etc. Soyabean is the second-largest oilseed crop produced in the country, to the tune of about 145,000 tonnes annually, but the entire quantity of it is used as poultry feed without extracting oil. As such, locally grown soyabean has no contribution to indigenous oils and fats production. Annual production of other oilseeds crops, such as groundnut, coconut, sesame, and linseed, is very insignificant in quantity and having almost no contribution to country's oils and fats production. Detail on year-wise local production of oils and fats may be seen at Table - 2.

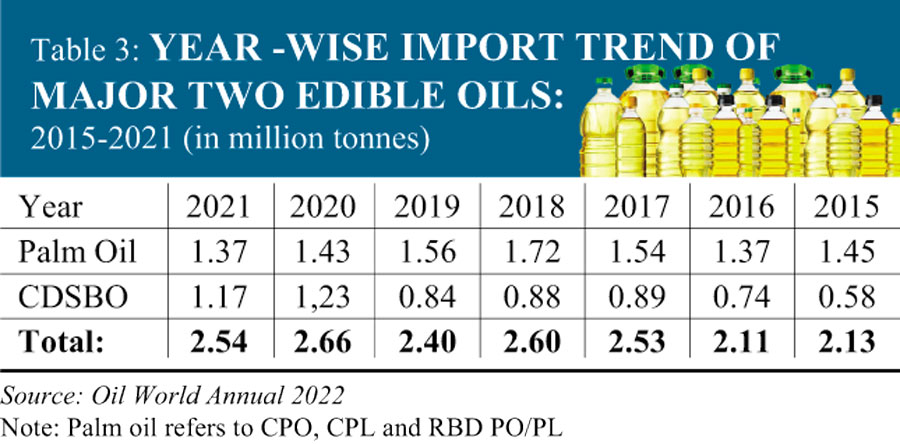

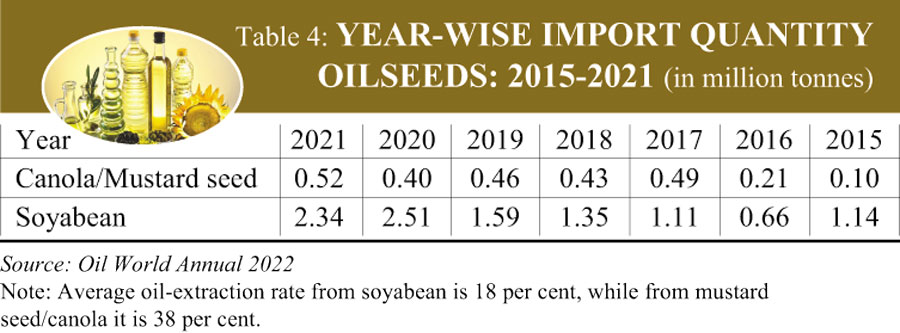

Because of insignificant local production of oils and fats against the annual requirement, about 3.0 million tonnes, the country is mainly dependent on imported oils and fats, to the tune of about 92 to 93 per cent. In pace with population growth, economic development vis-à-vis increases in purchasing power of the general consumers, consumption of oils and fats had been in a growing trend during last decade. Detail on item-wise import trend of edible oils and oil seeds during 2015 to 2021 may be seen at Table 3 and 4.

Because of insignificant local production of oils and fats against the annual requirement, about 3.0 million tonnes, the country is mainly dependent on imported oils and fats, to the tune of about 92 to 93 per cent. In pace with population growth, economic development vis-à-vis increases in purchasing power of the general consumers, consumption of oils and fats had been in a growing trend during last decade. Detail on item-wise import trend of edible oils and oil seeds during 2015 to 2021 may be seen at Table 3 and 4.

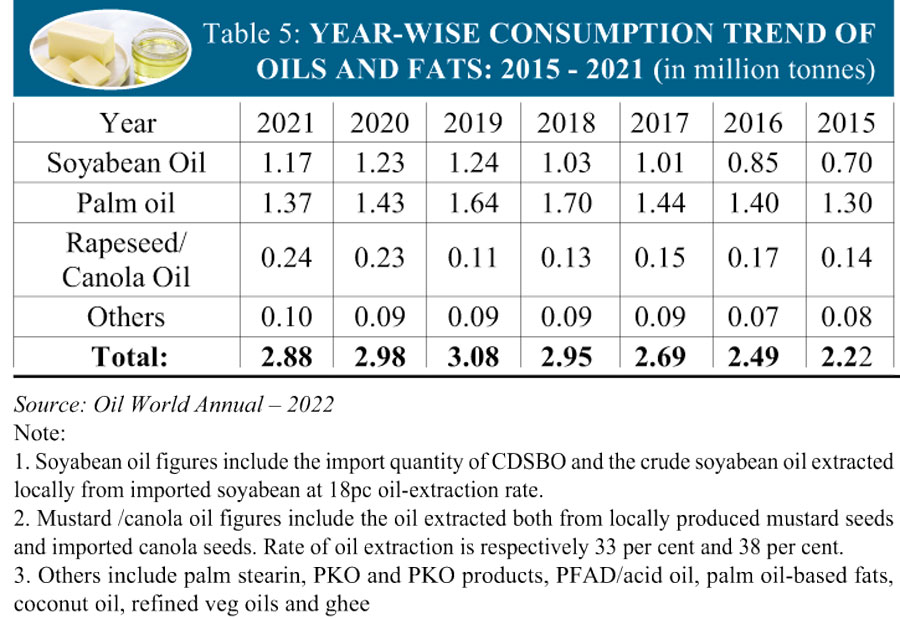

Present market share of various oils and fats: Palm oil, soyabean oil and canola/mustard oil are three major edible oils imported and consumed in the country, which constitutes almost 98 per cent of total consumption of oils and fats. Mustard oil is a traditional cooking oil of the country, being consumed since ancient times, while soyabean oil was introduced during early '60s and palm oil during mid-

Present market share of various oils and fats: Palm oil, soyabean oil and canola/mustard oil are three major edible oils imported and consumed in the country, which constitutes almost 98 per cent of total consumption of oils and fats. Mustard oil is a traditional cooking oil of the country, being consumed since ancient times, while soyabean oil was introduced during early '60s and palm oil during mid-  '70s. Until 2003, soyabean oil had been the major consumed edible oil in the country, and in the year 2003, palm oil had clinched the leading position among the three edible oils and since then till time, it has been dominating country's edible-oil market. Although mustard/canola is traditional cooking oil, but, because of comparatively high price, its consumption remains confined among rich people in the rural areas.

'70s. Until 2003, soyabean oil had been the major consumed edible oil in the country, and in the year 2003, palm oil had clinched the leading position among the three edible oils and since then till time, it has been dominating country's edible-oil market. Although mustard/canola is traditional cooking oil, but, because of comparatively high price, its consumption remains confined among rich people in the rural areas.  Besides, some industrial users also use mustard/canola oil in preparing pickles, which are very popular among all segments of consumers of the country.

Besides, some industrial users also use mustard/canola oil in preparing pickles, which are very popular among all segments of consumers of the country.

Apart from edible uses, a significant quantity of mustard/canola oil is also used for cosmetic purpose. During winter season, people who live in rural areas prefer to rub the mustard/canola oil on the body, which is a traditional practice.

Despite comparatively higher price, since 2020, consumption of mustard oil/canola oil has witnessed a gradual growth,  and to cope up with the increased demand, import of canola seed also growing. In 2020 and 2021, consumption of mustard oil/canola oil witnessed increase respectively by 109 per cent and 118 per cent compared to 2019. Myth prevails among the common people that mustard oil/canola oil has a beneficial property against COVID and it is one of the main reasons for increased consumption of the same during 2020 and 2021.

and to cope up with the increased demand, import of canola seed also growing. In 2020 and 2021, consumption of mustard oil/canola oil witnessed increase respectively by 109 per cent and 118 per cent compared to 2019. Myth prevails among the common people that mustard oil/canola oil has a beneficial property against COVID and it is one of the main reasons for increased consumption of the same during 2020 and 2021.

Refined palm oil is leading edible oil in the country since 2003 occupying a significant  market share. Initially palm oil's market share was 60 per cent to 63 per cent of total edible-oil market of the country. Quantit-wise gap between refined palm oil and refined soyabean oil was huge until 2016. However, starting from 2017, the aforesaid gap is gradually minimizing because of substantial rise in the import of soyabean by local seed-crushing-plant owners, which

market share. Initially palm oil's market share was 60 per cent to 63 per cent of total edible-oil market of the country. Quantit-wise gap between refined palm oil and refined soyabean oil was huge until 2016. However, starting from 2017, the aforesaid gap is gradually minimizing because of substantial rise in the import of soyabean by local seed-crushing-plant owners, which  is contributing to the increased supply of soyabean oil on the local market at a competitive price. Seed- crushing plants are contributing to increased supply of soyabean oil at a comparatively cheaper price compared to the imported crude degummed soyabean oil (CDSBO). Because, imported CDSBO is subject to 15-percent value-added tax (VAT), while import of soyabean and crude soyabean oil extracted from imported soyabean is exempt from payment of the VAT. Accordingly, availability of soyabean oil on the local market at competitive price is increasing apace with increased import of soyabean.

is contributing to the increased supply of soyabean oil on the local market at a competitive price. Seed- crushing plants are contributing to increased supply of soyabean oil at a comparatively cheaper price compared to the imported crude degummed soyabean oil (CDSBO). Because, imported CDSBO is subject to 15-percent value-added tax (VAT), while import of soyabean and crude soyabean oil extracted from imported soyabean is exempt from payment of the VAT. Accordingly, availability of soyabean oil on the local market at competitive price is increasing apace with increased import of soyabean.

Palm oil established itself on the local market mainly with its price advantage over refined soyabean oil. Due to increased availability of refined soyabean oil at a competitive price, palm oil is losing its dominance on the local oils and fats market, while refined soyabean oil is gradually regaining its leading position. In 2020 and 2021, the share of palm oil in country's oils and fats market came down to about 48 per cent, which was 53 per cent in 2019. Table 5 would give a clearer picture on the consumption trend of three oils in the country.

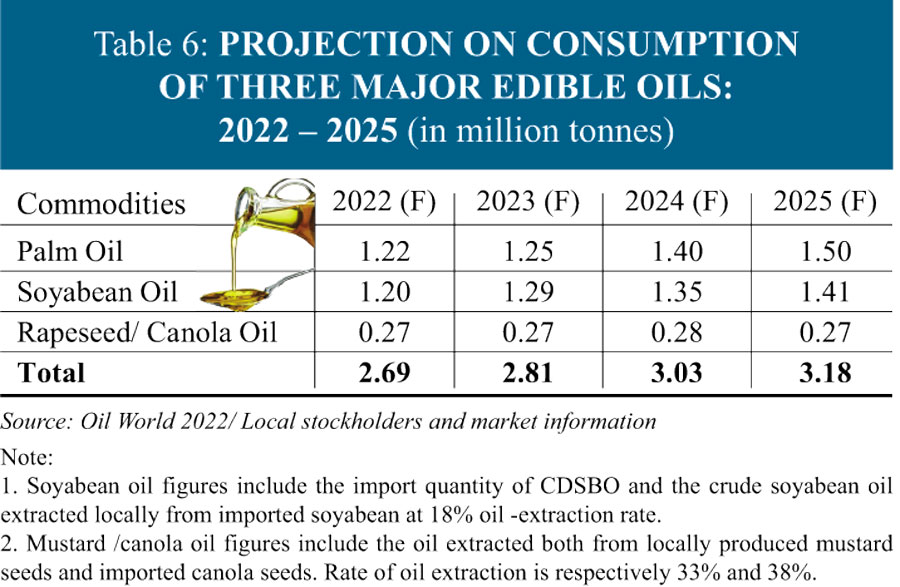

Expected oils and fats imports vis-à-vis consumption scenario: 2022 to 2025

Because of prevailing gloomy economic situation, as seen in Bangladesh and globally as well, consumption vis-à-vis import of oils and fats is likely to be stagnant or decline in coming years. Comparatively higher price of oils and fats on the international market and local market, and prevailing economic inflation in the country together are contributing greatly to eroding the purchasing power of the local consumers, which is also resulting in reduction in the consumption of oils and fats.

People who live in rural areas, who comprises almost 65 - 70 per cent of the 170-million-strong population and the largest segment of the consumers, have cut down the consumption of oils and fats greatly since 2020 under the negative impact of COVID 2019. Present increased prices of food commodities have forced them to spend a significant portion of their income on the buying of staple foods and hence they have no option but to reduce the consumption of oils and fats.

As per a survey conducted by a local NGO, among the aforesaid 65 to 70 per cent of the population living in rural area, about 40 per cent have turned into extreme poor segment of the population mainly due to negative impact of the COVID-19. Price hike of food commodities, noticed sinc early 2022, and prevailing inflation come together as havoc on them. As per information being published in the country's media, the aforesaid segment of pupation is now struggling just to survive.

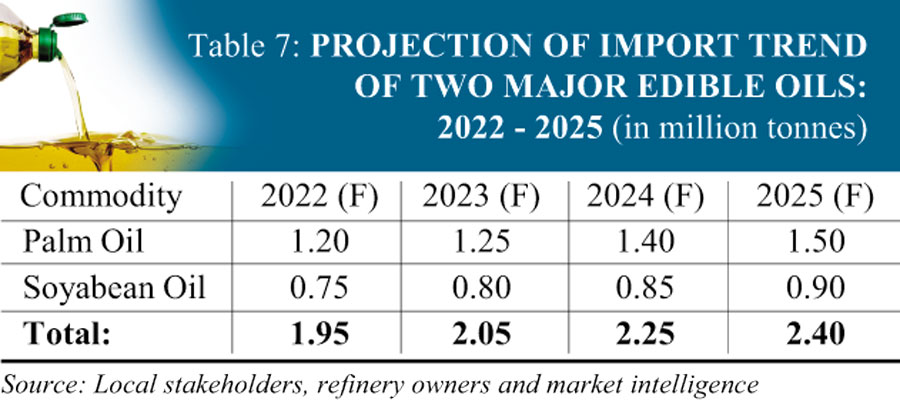

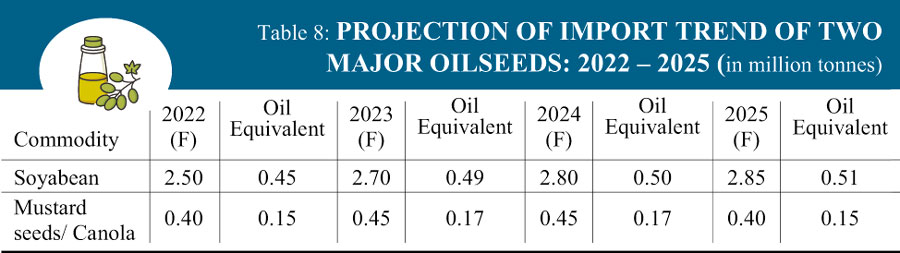

Considering all these adverse factors, it is being apprehended that the consumption as well as import of oils and fats would come down in coming years and likely to witness negative growth until 2025 compared to the past. Accordingly, projection on the consumption vis-a-vis import pattern of major three edible oils and oilseeds during 2022- 2025 period are mapped in the Table - 6, 7 and 8.

The writer is Former Regional Manager of Malaysian Palm Oil Council

fakhrulalam52@yahoo.com

© 2026 - All Rights with The Financial Express