![]() In recent times, the overseas development assistance (ODA) scenario, and the consequent debt liabilities and debt repayment obligations have attracted heightened attention in public discourse in Bangladesh. This was not without reason. The problems facing the economy of Sri Lanka, a neighbouring country in the region known for its robust economy and high standard of living, has fuelled this discussion and raised concerns about debt sustainability in other countries of the region as well. As is known, Sri Lanka's economic woes culminated in its failing to repay its due debts, and formally declaring itself as bankrupt on July 5, 2022. This indeed came as a shock to many. While Bangladesh's track record in terms of servicing of foreign borrowings has been quite robust, the timing of the Sri Lankan crisis coincided with Bangladesh's hitherto comfortable foreign exchange reserves coming under considerable pressure owing primarily to the high global price-induced import payments and the resultant large trade and current account deficits.

In recent times, the overseas development assistance (ODA) scenario, and the consequent debt liabilities and debt repayment obligations have attracted heightened attention in public discourse in Bangladesh. This was not without reason. The problems facing the economy of Sri Lanka, a neighbouring country in the region known for its robust economy and high standard of living, has fuelled this discussion and raised concerns about debt sustainability in other countries of the region as well. As is known, Sri Lanka's economic woes culminated in its failing to repay its due debts, and formally declaring itself as bankrupt on July 5, 2022. This indeed came as a shock to many. While Bangladesh's track record in terms of servicing of foreign borrowings has been quite robust, the timing of the Sri Lankan crisis coincided with Bangladesh's hitherto comfortable foreign exchange reserves coming under considerable pressure owing primarily to the high global price-induced import payments and the resultant large trade and current account deficits.

This led to significant depreciation of the Bangladeshi taka (BDT) by about 12.0 per cent in the course of only a few months. The difference between central bank's formal exchange rate and the informal market rate widened significantly, at one point standing at about 15.0-20.0 per cent. The government was forced to take a number of unprecedented measures to curtail imports, slow down the implementation of foreign-funded projects, and other measures to curtail the demand on US dollar and stabilise the foreign exchange market. The pressure on foreign exchange has led the government to seek budgetary support from the World Bank and other financial institutions and negotiate balance of payments support from the IMF. However, concerns still remain in this regard.

In this backdrop and in consideration of the increasingly large foreign aid coming to the country in recent period, with anticipated higher debt service payments in foreseeable future, questions have been raised as to whether Bangladesh had reasons to be concerned about its debt management and addressing debt servicing obligations in near to medium term future.

To underwrite growing public expenditure and finance fiscal deficit, developing countries such as Bangladesh do resort to large borrowings - from internal and also from external sources. The borrowings from external sources create foreign debt servicing obligations. The principal amount and interests need to be paid as per repayment schedules. This in itself should not be a reason to worry about as long as the foreign borrowings are strategically made, debt servicing obligations are under control, the borrowings generate the expected socio-economic returns that leads to strengthening of the economy and raises the capacity of the concerned country to repay, and the foreign exchange (forex) reserves are adequate to underwrite the obligations.

In this backdrop, the objective of the present article is rather narrow: to assess whether Bangladesh should be worried about its debt repayment obligations, conceding that any concerns in this regard would have broader economy-wide ramifications and implications. In view of this, the article deals with three issues: first, salient features of Bangladesh's overseas borrowings, debt servicing obligations and trends; second, an assessment of whether the country has reasons to pursue a cautionary stance in view of the emerging scenario; and third, strategies to be pursued to mitigate any anticipated risks.

SALIENT FEATURES OF THE BORROWINGS SCENARIO: As of March, 2022, Bangladesh's outstanding foreign debt stood at US$68.25 billion. This, as share of GDP, was 16.9 per cent; as share of foreign exchange earnings from export and remittance this amount was equivalent to 91.3 per cent. To note, these figures were way below the two thresholds used by the World Bank and the IMF to assess the strength of debt carrying capacity of a country: 55.0 per cent as share of GDP, and 240.0 per cent as share of earnings from exports and remittances. Also, Bangladesh's external debt service as share of domestic revenue stood at 8.3 per cent in FY2021, comfortably below the World Bank-IMF corresponding threshold of 23.0 per cent. Foreign debt service payments as share of export plus remittance earnings was about 4.5 per cent for Bangladesh, whereas the critical threshold was considered to be 21.0 per cent. Thus, in terms of both the outstanding foreign debt and the foreign debt servicing obligations Bangladesh's position is, as it stands now, quite comfortable. Indeed, as the above shows, the country has considerable cushion in respect of all the critical markers and reference points of World Bank-IMF. No surprise that Bangladesh is considered to be a strong debt carrying country according to these criteria.

Also to note, of the US$68.25 billion of outstanding foreign debt of Bangladesh, the overwhelming part, 93.9 per cent, is of long-term nature, while only 6.1 per cent is of short term nature. This allows Bangladesh to plan well-ahead as regards debt repayment and ensuring debt sustainability.

Yet another positive aspect relates to the structure of Bangladesh's foreign loans. Of the total US$101.36 billion of foreign loans disbursed since independence (1971/72 - 2020/21), the overwhelming part, US$83.49 billion (about 82.4 per cent), was project loan; the shares of food aid and commodity aid, 6.8 per cent and 10.8 per cent respectively, were rather low by comparison. This pattern has strengthened further in recent years as well; for example, the corresponding figure for project loan in total disbursed loan in FY2021 was 99.8 per cent. The loans in the pipeline, amounting to US$ 50.34 billion, are also almost exclusively geared towards project aid (with some amount earmarked for budgetary support). This meant that most foreign borrowings of Bangladesh went to hard (socio-economic infrastructure) and soft areas (health, education and social sectors), and not for purposes of consumption. The borrowings incurred as project loans were spent for productive purposes, with potentially robust medium to long-run returns that should generate the economic capacity to underwrite the consequent debt obligations.

THE EMERGING CONCERNS: The preceding picture does evince a comfortable picture for Bangladesh, in terms of the amount of foreign borrowings and the accumulated debt, structure and composition of borrowings and debt repayment scenario. However, it is argued here that in spite of the above, Bangladesh should exercise due caution in going forward. There are several reasons for this.

While the Bangladesh economy cannot and should not be compared with that of Sri Lanka, the Sri Lankan experience should serve as a learning opportunity for Bangladesh. The developments in Sri Lanka has shown how even a relatively well-developed economy, and one with higher standard of living, could fall into the dreaded debt trap if the overseas borrowings are not well-planned, money is not well-spent, the debt servicing liabilities are not well-anticipated, forex reserves are not adequately replenished and measures are not well in place in advance to deal with likely repayment obligations. In itself Sri Lanka's debt to GDP ratio was not exceptionally high; at 67.0 per cent (at the crisis point of March 2022) it was only somewhat higher than the 55.0 per cent threshold mentioned earlier. Many developing countries have higher debt to GDP ratio but they did not face bankruptcy as has been the case with Sri Lanka.

Cross-country evidence suggests that many countries tend to fall into middle income trap after having experienced impressive GDP growth and making the transition from low income country (LIC) to lower middle income country (LMIC) and from there to upper middle income country (UMIC). And oftentimes it is a dual trap - a combination of middle income trap and debt trap. Countries that have fallen into lower middle income trap (mostly in Asia), and higher middle income trap (mostly in South America, but also in Asia), have similar experience. Countries that fall into the dual trap, Sri Lanka included, have one common contributing factor- these countries have failed to make appropriate use of the borrowed money. The reasons and lessons could be grouped by posing the following questions: whether the terms and conditions of borrowings were properly negotiated with overseas partners -interest rate, grace period, maturity period, conditionalities; whether the borrowed funds were allocated to priority sectors; whether the overseas borrowings were used by ensuring good governance and good value for money and the anticipated rates of returns were justified; whether repayment plan was properly sequenced in view of the obligations; whether exchange rate risks were properly factored into the estimations (more specifically, when returns are accrued in local currency but repayments have to be made in foreign currency).

In the particular case of Sri Lanka, one finds evidence of lack of due diligence in all the aforesaid areas. Sri Lanka's foreign debt structure was significantly tilted towards sovereign bonds. Indeed, share of sovereign bond debt in Sri Lanka's total outstanding external debt of US$ 35.1 billion (as of April 30, 2021) was 47.0 per cent. To recall, Sri Lanka borrowed heavily from global financial markets by issuing sovereign bonds at relatively high cost. Corresponding figures for Chinese debt, a much talked about subject, was relatively low at 10.0 per cent. In March, 2022 Sri Lanka's forex reserves had come down to US$ 1.9 billion, at a time when it was scheduled to repay US$ 1.0 billion on account of its sovereign bond repayment, in addition to US$ 4.0 billion of debt servicing for other foreign borrowing obligations.

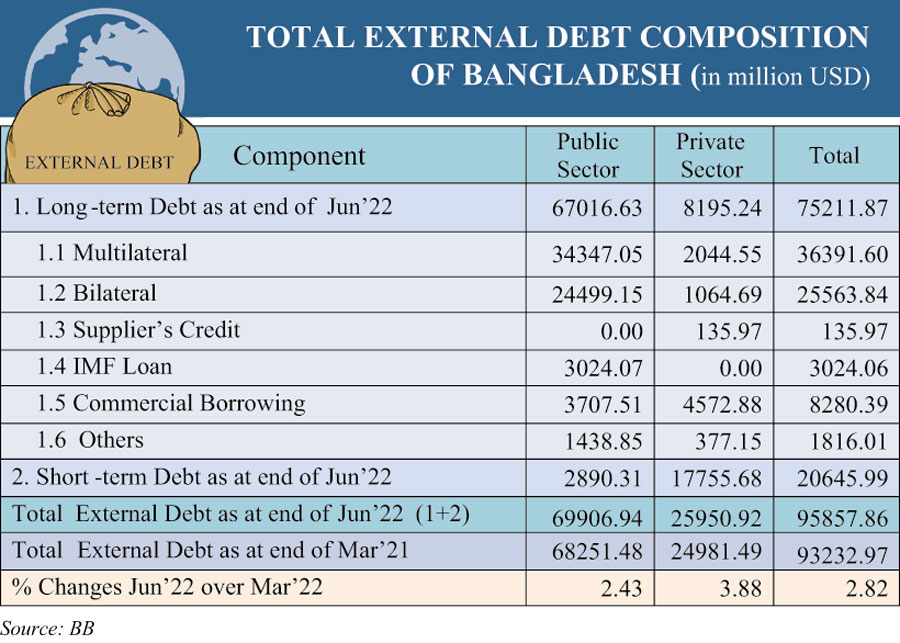

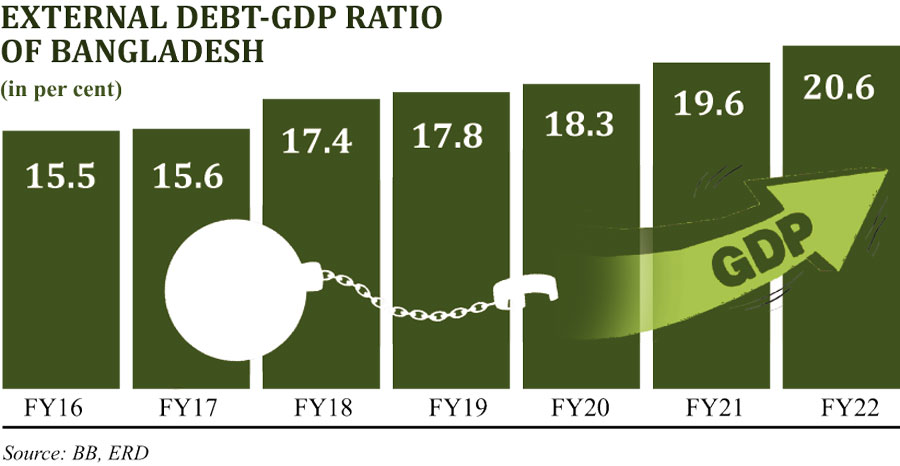

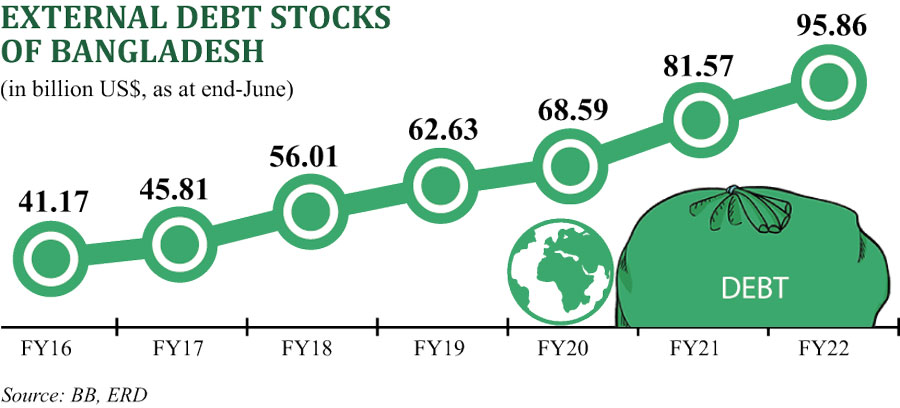

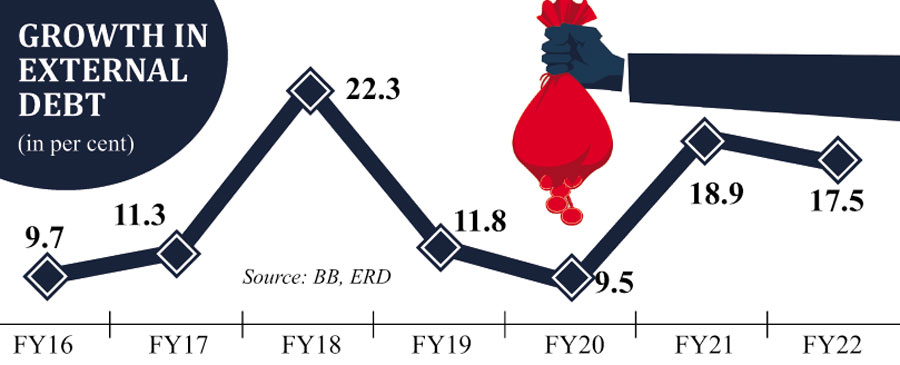

To recall, Bangladesh's foreign debt-GDP ratio and debt servicing to foreign exchange earnings ratio are robust. However, to note, in recent years both the amount and the foreign debt servicing liabilities of Bangladesh have been on the rise. Foreign debt-GDP ratio was 17.6 per cent in FY2011-12 coming down to 12.8 per cent in FY2016-17 and then experiencing a secular rise to 16.0 per cent in FY2021. This is set to rise further in the backdrop of higher foreign borrowings to underwrite fiscal deficits and service development needs. If in FY2012 and in FY2015 the amount of foreign aid disbursed was US$2.13 billion and US$3.04 billion respectively, in FY2020 and FY2021, the corresponding figures have risen to US$7.38 billion and US$7.96 billion. Bangladesh has received more money as foreign loan in the first nine months of FY2022 compared to the full FY2021. In the ongoing FY2023, the projected amount of foreign borrowing is more than USD 12.0 billion. Indeed, the rise in public sector debt is also corroborated by the figures for the country's outstanding foreign debt in June FY2021 and June FY2022: US$ 62.9 billion and US$ 68.25 billion respectively, indicating a rise of 22.1 per cent in one year. The aid in the pipeline (more than US$50.0 billion) to be disbursed over the next few years, also substantiate the rising debt to be incurred over the next 3-5 years. It is to be noted in this connection that Bangladesh's outstanding domestic debt was about US$75.8 billion in FY2021-22 as against outstanding medium to long term (MLT) foreign debt of US$55.6 billion. On the other hand, foreign debt servicing for MLT loans stood at US$ 3.30 billion (in FY2020-21) as against US$ 29.0 billion for domestic debt servicing. This reveals the relatively very low interest rates on foreign debt as against the high interest rate on domestic debt incurred by the government.

It needs to be mentioned that in recent times the interest rates on foreign loans have been on the rise. The grant element in the loan portfolio of Bangladesh has been on a decline. Developmental partners have reduced this element drastically in view of the country's rising GDP and growing per capita income. In FY1992 the shares of loan and grant in total disbursed borrowing were 49.3 percent and 50.7 per cent respectively; in FY2002 the corresponding shares were 66.8 per cent and 33.2 per cent. The share of grants is coming down at a fast pace - in FY2012, the two shares (loans and grants in total ODA) were 72.4 per cent and 27.6 per cent which had further declined in FY2021, with the two shares being 93.6 per cent and 6.4 per cent respectively. Indeed, the grant element is likely to disappear in near term future. This would indicate Bangladesh's rising foreign debt servicing liabilities in near and medium term future.

There have been some shifts in the terms of borrowings as well. Bangladesh's graduation from LIC to LMIC meant that it is no longer eligible for borrowing exclusively on soft terms from the World Bank (the interest/service charge of loans from the International Development Assistance, World Bank's soft window, is very low, at 0.7 per cent per annum with 40 years' maturity and 10 years of grace period for most loans. To note, the World Bank is at present the single largest borrowing source for Bangladesh. Bangladesh is now a gap country according to World Bank criteria and soon (after a review which is scheduled to take place 6 years after LMIC graduation, Bangladesh has already approached this timeline) it will be a blend country, with a mix of concessional and non-concessional loan. The doors for low-cost borrowings are closing fast and increasingly World Bank borrowings will need to be incurred by Bangladesh on commercial, IBRD (International Bank for Reconstruction and Development) terms. Already the costs of borrowing are rising. For example, for IDA20, interest rate on about 33.0 per cent of the US$ 6.05 loan (July 2022 - June 2025) would be on market terms, as against 13.7 per cent for IDA19. Other lending institutions such as the ADB and the IDB are following suit as also the bilateral partners.

Loans from China and Russia, with relatively higher interest rates (on non-concessional, commercial terms) and shorter grace and maturity periods, have in recent years emerged as important features in the Bangladesh loan portfolio. The terms of such borrowings are also relatively less generous - shorter grace and maturity periods: 4-5 years and 15 years respectively for suppliers' credit and 2-3 years and 12-15 years in case of buyers' credit. About 47.6 per cent of outstanding loans of about US$ 4.0 billion from China were either of supplier's credit type (up to 2004) or of buyer's credit type (since 2011). These involved higher interest rate and more stringent terms: 2.2 -3.25 per cent for buyers' credit and 3.5 - 5.0 per cent for suppliers' credit plus high service charges.

Whilst time and cost escalation are common features in the implementation of public infrastructure projects (PIPs) in Bangladesh, issues of good governance and ensuring good value for money spent, to generate the expected internal, financial and economic rates of returns, have emerged as major concerns in recent times. Higher per unit costs in implementing PIPs, weak monitoring of implementation, and inadequate human resources and shortage of efficient project directors have been pointed out in successive reports of the Implementation Monitoring and Evaluation Division (IMED) of the Bangladesh Planning Commission, the oversight body.

If the projects implemented by borrowed money do not generate expected income, the returns end up to be lower, creating pressure on repayment obligations. The oft-experienced delays in implementation of foreign-funded projects not only leads to escalation of project costs, but also leads to a situation when debt repayment following end of grace period starts at a time when the project is still being implemented. Projects being implemented as part of Indian Lines of Credit (LoCs) are cases in point. This creates a mismatch between the time income is generated from the project (to underwrite debt repayment) and the time when debt repayment starts. This makes overall debt management challenging.

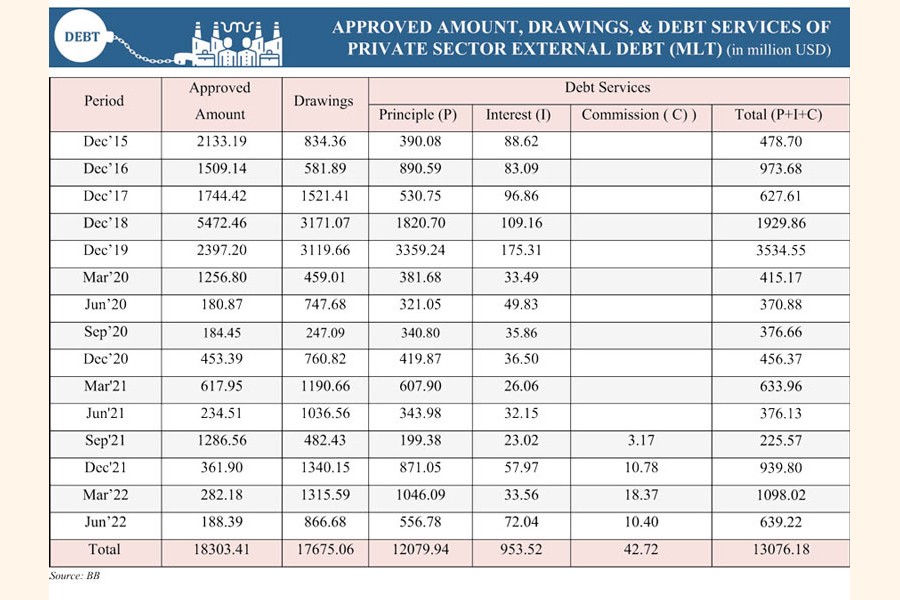

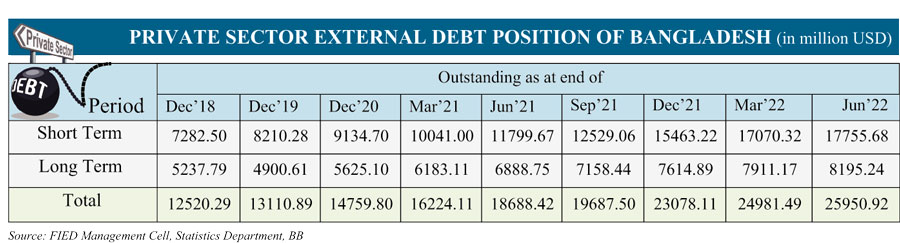

The other disquieting trend is the significant rise in external debt incurred by the private sector of Bangladesh. This stood at USD 24.98 billion in March 2022; to note, the corresponding figure was USD 16.22 billion in March 2021, indicating a rise of 54.0 per cent in one year. It is also interesting to note that, private sector outstanding MLT borrowing from China which stood at US$ 0.42 billion in March 2021 rose to US$ 1.96 billion in March 2022, a whooping rise of 364.5 per cent in one year. Although the government has not given any sovereign guarantee for these loans, two important implications should not be lost sight of - one, the rising demand for foreign exchange for repaying the loan which would create pressure in the country's foreign exchange market; and the damage to country's image if any private borrower fails to repay the foreign debt on time.

In view of rising government borrowings, the foreign debt servicing liabilities are set to rise significantly in near term future. If in FY2020-21 and FY2021-22 the external debt servicing on MLT loans were US$ 1.92 billion and US$ 2.01 billion respectively, according to ERD projections these are envisaged to rise to US$ 4.02 billion in FY2024-25 and further to US$ 5.15 billion in FY2029-30. Indeed, these projected figures also reflect some of the hard term loans such as those from Russia, China and India for which the grace period (the period at the end of which repayment of principal amount and interest payments would start) will end in a couple of years.

In view of rising government borrowings, the foreign debt servicing liabilities are set to rise significantly in near term future. If in FY2020-21 and FY2021-22 the external debt servicing on MLT loans were US$ 1.92 billion and US$ 2.01 billion respectively, according to ERD projections these are envisaged to rise to US$ 4.02 billion in FY2024-25 and further to US$ 5.15 billion in FY2029-30. Indeed, these projected figures also reflect some of the hard term loans such as those from Russia, China and India for which the grace period (the period at the end of which repayment of principal amount and interest payments would start) will end in a couple of years.

Another concern is related to currency depreciation and its implications for foreign debt repayment. This is of particular importance for projects funded by foreign borrowings which are to generate income in local currency. Any currency depreciation - as has happened in recent times when BDT experienced a depreciation of about 12.0 per cent within a period of few months - will have significant adverse impacts in terms of debt repayment liabilities accruing from overseas borrowings. This has already emerged as a major concern, both in the context of public and private borrowings.

STRATEGIES IN GOING FORWARD: The discussion above indicates that in spite of Bangladesh's impressive track record in terms of dependence on foreign borrowing and debt servicing, there is no room for complacence. Bangladesh will need to be vigilant and strategic in order not to fall into debt trap particularly if one takes into account the growing needs of foreign borrowings to underwrite its developmental aspirations. If the country is to realise the aspirations set out in the SDGs and the Bangladesh Vision 2041, it will need to mobilise a significant amount of resources, including from foreign sources. For example, it has been estimated that attaining the SDGs will require about US$ 70.0 billion worth of investment annually of which a large part will need to be underwritten through foreign borrowings. On the other hand, the growing debt stock will create increasing debt servicing liabilities at a faster rate than was the case previously. This is because, as was noted earlier, interest rates on borrowings are set to rise over the near term and the terms of borrowings will also become more stringent. In view of the anticipated scenario, it is reckoned that Bangladesh should do the following:

Make realistic projections as regards debt servicing obligations. In Bangladesh, the ERD undertakes periodic exercise to estimate future debt servicing liabilities. This provides an idea about the payment to be made to underwrite foreign borrowings. The projections are based on the basis of end of grace period of particular loans ends, rate of interest and other terms of borrowings. A number of recent loans, particularly from Russia and China but also from India and others, are of semi and non-concessional nature; many of these also have service charges attached to the loans. Also, because of delayed project implementation, as it happens frequently, the loan amounts estimated at the initial period tends to rise. As noted, the amount of non-concessional loans in the borrowing portfolio is rising and will rise further in future because of Bangladesh's middle income graduation. The debt repayment obligations should be estimated based on ground realities, reliable projections and anticipated risks.

Ensure good governance in PIP implementation. Ensuring good governance in implementing PIPs that involve significant amount of borrowed money ought to be given highest priority. A number of mega projects in Bangladesh have been put under special scrutiny and implementation of these is regularly monitored. However, concerns remain as regards time and cost escalation and the consequent higher amount of borrowed money. A good governance framework should be developed and put in place in view of the emergent concerns in this regard. The OECD framework for good governance as an oversight tool to monitor implementation of infrastructure projects may serve as a suitable reference in this connection. Concrete measures should be taken to strengthen the IMED's institutional capacities and oversight function. Zero-tolerance policy announced by the government with respect to corrupt practices in the conduct of feasibility study, cost estimations, procurement, implementation and post-implementation works concerning particularly the PIPs, will need to be fully enforced. One lesson from the Sri Lankan experience is the need to enforce highest standards in view of selection, procurement, management and implementation to ensure good value for money in investing in PIPs, underwritten by borrowed money.

Factor-in exchange rate movement. Bangladesh should take cognizance of the risks emanating from exchange rate depreciation in estimating the returns from foreign borrowings-induced investment, particularly when the projects are geared to domestic market and the earnings are in local currency. A large number of PIPs in

Factor-in exchange rate movement. Bangladesh should take cognizance of the risks emanating from exchange rate depreciation in estimating the returns from foreign borrowings-induced investment, particularly when the projects are geared to domestic market and the earnings are in local currency. A large number of PIPs in  Bangladesh, implemented with foreign loans, such as in roads, transport and energy sectors, will generate income in local currency. When the returns from such projects are calculated and these are juxtaposed to costs of borrowings to justify the particular investment, the foreign exchange movement risks should be properly accounted for and factored into the estimations. Currency hedging could be one way to mitigate the likely negative impact of exchange rate fluctuations on future repayments.

Bangladesh, implemented with foreign loans, such as in roads, transport and energy sectors, will generate income in local currency. When the returns from such projects are calculated and these are juxtaposed to costs of borrowings to justify the particular investment, the foreign exchange movement risks should be properly accounted for and factored into the estimations. Currency hedging could be one way to mitigate the likely negative impact of exchange rate fluctuations on future repayments.

Be mindful of the dual graduation. While LDC graduation itself does not have any significant implications as regards access to aid and concessional funds, two issues need to be kept in mind -Bangladesh will miss out on the international support measures in place for LDCs once it graduates out of the group. Some LDC-focused financial support window such as LDC-specific Climate Fund will no longer be available to Bangladesh on graduation. This will necessitate higher amounts of borrowed money. As was noted, the grant element in foreign borrowings is coming down, and the share of borrowings conducted on commercial terms has been on the rise because of middle income graduation. Second, graduation is highly likely to influence decision of lending countries since these countries justifiably give priority to LICs and LDCs when extending loans on concessional and soft terms. Bangladesh should make best use of the time it has at its disposal prior to the transition to IRBD-status only country from the current 'gap' and 'blend' country status.

Be mindful of the dual graduation. While LDC graduation itself does not have any significant implications as regards access to aid and concessional funds, two issues need to be kept in mind -Bangladesh will miss out on the international support measures in place for LDCs once it graduates out of the group. Some LDC-focused financial support window such as LDC-specific Climate Fund will no longer be available to Bangladesh on graduation. This will necessitate higher amounts of borrowed money. As was noted, the grant element in foreign borrowings is coming down, and the share of borrowings conducted on commercial terms has been on the rise because of middle income graduation. Second, graduation is highly likely to influence decision of lending countries since these countries justifiably give priority to LICs and LDCs when extending loans on concessional and soft terms. Bangladesh should make best use of the time it has at its disposal prior to the transition to IRBD-status only country from the current 'gap' and 'blend' country status.

Look for alternative funding sources: Bangladesh will need significant amount of resources to underwrite its future needs and realise the SDGs and Vision 2041 aspirations. As is the case, an increasing amount of ODA is being committed to humanitarian needs and, overall, aid for development needs is under pressure. In this backdrop there will be a need for Bangladesh to proactively search for alternative sources of funding such as blended finance, global climate finance, finance available under south-south cooperation and others.

Diversify the sources of development finance. In view of managing its financial flow portfolio, Bangladesh should seek to have more loans of budgetary supply type which would provide flexibility in terms of use of funds. Loans from non-traditional sources such as the New Development Bank (NDB) and the Asian Infrastructure Investment Bank (AIIB) should be explored more (Bangladesh has already borrowed from these institutions). Fund flows as part of South-South cooperation, on favourable terms, should be explored more. Bangladesh has in recent times seen some flows of blended finance; however, it is important that this does not go only for infrastructure sector but also to health, education and SMEs. Bangladesh should also join others in calling for an expansion of windows such as IMF's Resilience and Sustainable Trust Fund (currently stands at US$ 100.0 billion which came into effect in May, 2022.The original plan was for US$ 300.0 billion) which is geared to providing funds for building resilience to external shocks. A number of developing countries have also been exploring possibilities of currency swaps to reduce demands on dollar-dominated forex reserves to deal with the pressure on foreign exchange. However, in absence of institutional arrangements this has not proved to be very successful. Bangladesh should learn from cross-country experience in this regard and the Bangladesh Bank should look into the possibilities keeping in the purview future needs.

Estimate reliable forex reserve figure. It is important also to have a clear understanding about the size of forex reserves which is unencumbered and which may be used to underwrite imports, service debt obligations and meet other obligations. The recent debate between the Bangladesh Bank and the IMF about the actual size of forex reserves has highlighted this issue. As would be recalled, the IMF's estimation indicated that actual forex reserve which could be deployed to underwrite various expenditures and obligations was about USD 7.0 billion lower than the Bangladesh Bank figure.

Keep private sector borrowings under vigilance. As was noted, the amount of private sector loans incurred from foreign sources are rising at a very fast pace. Although there is no sovereign guarantee for repayment of private loans, the accumulated total foreign borrowings, public and private (to the tune of $93.2 billion as of March 2022) will create a pressure on debt repayment and the foreign exchange market. The central bank and the government should carefully monitor private sector loans, their use and debt servicing record to forestall any default that will undermine Bangladesh's credibility and credit rating.

CONCLUDING REMARKS: The conclusion to be drawn from the preceding discussion is that, whilst till now Bangladesh's foreign borrowing situation and debt servicing track record have been quite impressive, there are reasons to be careful and cautious in going forward. Foreign borrowings are rising at a fast pace, the shares of grant and concessional loans are seeing secular decline, and the terms of loans are becoming more stringent. Debt servicing liabilities will rise significantly as grace period for several loans, some of which were incurred on hard terms, are coming to an end soon. Bangladesh will need to do the needful to maintain its robust track record as a strong debt carrying country.

In view of the above, the article has drawn attention to the implications of Bangladesh's dual graduation for the country's debt management. It has underscored the need for greater attention to good governance and ensuring good value for money in implementation of PIPs underwritten by borrowed funds from foreign sources. Renewed efforts will need to be made to mobilise higher amount of foreign exchange through export, remittances and FDIs to be able to have robust foreign reserves to underwrite debt servicing obligations. The article has highlighted a number of emergent concerns and has put emphasis on designing a forward-looking strategy in view of foreign borrowings and repayment obligations to maintain Bangladesh's impressive debt servicing track record and to ensure robust debt sustainability in going forward.

Professor Mustafizur Rahman is Distinguished Fellow, Centre for Policy Dialogue (CPD). mustafiz223@gmail.com.

[A shorter version of the paper appeared in WhiteBoard magazine published by the Centre for Research and Information (CRI).]

© 2026 - All Rights with The Financial Express