A teller machine is being used to count currency notes — FE Photo

A teller machine is being used to count currency notes — FE Photo ![]() Bangladesh is now on the path of continuous development after overcoming various obstacles. Bangladesh has reached the stage of graduation from the category of Least Developed Countries (LDCs) of the United Nations to a Developing Country. The announcement came as Bangladesh celebrated its golden jubilee of independence this year. However, there is no scope to be complacent and we have to face challenges on the growth path. We have to overcome many challenges. The first challenge is our institutional weakness. Most of the regulatory bodies like the central bank, securities exchange commission and development support agencies like the Export Promotion Bureau and the Bangladesh Investment Development Authority are yet to become efficient and dynamic. There are still many barriers faced by private entrepreneurs in the areas of trade and commerce. The second challenge is ensuring good governance, transparency and accountability both in the public and private sectors. Waste of scarce resources, corruption and money laundering have all made the task of rapid and equitable development a difficult task. Along with other countries of the world, the economy of Bangladesh is also facing major challenges arising out of the Covid situation and the Ukraine war. The country's economy is now facing a three-pronged challenge. Inflation, trade deficit, and energy supply and prices. Inflation is constantly increasing. Besides, our imports are high and exports are relatively low, resulting in a large trade deficit. The devaluation of money is increasing. The third challenge is inadequate gas and electricity supply. This has led to increased load-shedding. There is a negative impact on industrial production. The problems themselves must be acknowledged and concerted action must be taken by the policy makers and institutions. Then it will be possible to overcome these challenges.

Bangladesh is now on the path of continuous development after overcoming various obstacles. Bangladesh has reached the stage of graduation from the category of Least Developed Countries (LDCs) of the United Nations to a Developing Country. The announcement came as Bangladesh celebrated its golden jubilee of independence this year. However, there is no scope to be complacent and we have to face challenges on the growth path. We have to overcome many challenges. The first challenge is our institutional weakness. Most of the regulatory bodies like the central bank, securities exchange commission and development support agencies like the Export Promotion Bureau and the Bangladesh Investment Development Authority are yet to become efficient and dynamic. There are still many barriers faced by private entrepreneurs in the areas of trade and commerce. The second challenge is ensuring good governance, transparency and accountability both in the public and private sectors. Waste of scarce resources, corruption and money laundering have all made the task of rapid and equitable development a difficult task. Along with other countries of the world, the economy of Bangladesh is also facing major challenges arising out of the Covid situation and the Ukraine war. The country's economy is now facing a three-pronged challenge. Inflation, trade deficit, and energy supply and prices. Inflation is constantly increasing. Besides, our imports are high and exports are relatively low, resulting in a large trade deficit. The devaluation of money is increasing. The third challenge is inadequate gas and electricity supply. This has led to increased load-shedding. There is a negative impact on industrial production. The problems themselves must be acknowledged and concerted action must be taken by the policy makers and institutions. Then it will be possible to overcome these challenges.

The main reason for global recession (2007-08) can be traced back to the mismanagement of banks and financial institutions. Despite all the measures taken by different countries, with the US taking the lead, full recovery has taken a long time and involved considerable efforts. The situation around the globe is a challenging one against the backdrop of the Covid-19 pandemic and most recently the Russia-Ukraine conflict. Small economies like Bangladesh are by no means immune to fallouts from global downturns or negative spillover of the unprecedented pandemic and global instability. Bangladesh needs to argue forcefully for the same priority in stability as recovery, as well as for stability action agenda going beyond addressing symptoms (i.e. lapses in risk management, default loan, money laundering) to addressing underlying causes (i.e. lax policies, non-compliance of prudential and management norms, poor financial reporting, lack of good corporate governance).

So what are the implications of Bangladesh's economy minimizing external shocks and internal shocks? This article will mainly address the several challenges facing the banking sector from the internal shocks for the economy. The Hallmark and Bismillah Group financial scams and then the financial irregularities in BASIC Bank, one of the state-owned commercial banks, have demonstrated cracks in the governance and management of the commercial banks. From the Board of Directors to the management group to the lower-level officials, banks have not shown any sign of good governance, transparency and accountability. A disturbing fact is that these irregularities have permeated to a substantial number of private commercial banks and financial institutions as well.

The norms provided by the central bank are fairly well-formulated. It followed international standards. The International Accounting Services Board (IASB) under the Bank for International Settlements (BIS) in Basel, Switzerland, has provided three major norms, namely Basel I, Basel II and Basel III. Basel I of 1988 required banks and financial institutions to have sufficient capital adequacy, which was originally 8% of risk-weighted assets (RWA). Later on, it was raised to 10% for banks, including those in Bangladesh. There are some banks in the country whose requisite capital adequacy falls short of the norm. Basel I set up a mechanical, non-market-oriented measurement of capital adequacy which could not take care of fundamental risks, e.g. operational risk and market risk. Basel II, introduced in 2004, took care of the different types of risks for financial intermediaries (i.e. banks) as well as the supervisory review process for the management of banks. Basel III has introduced more stringent conditions for equity capital, liquidity ratio and capital adequacy.

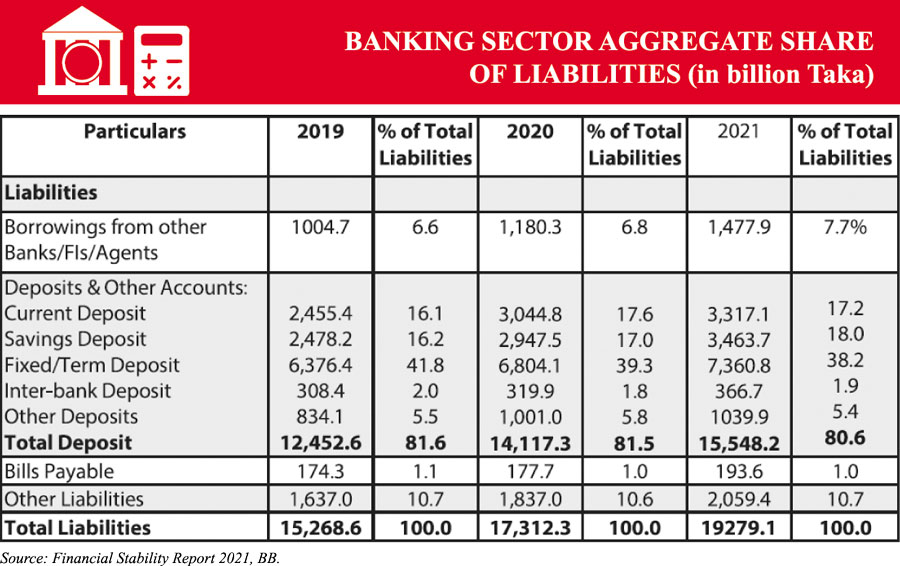

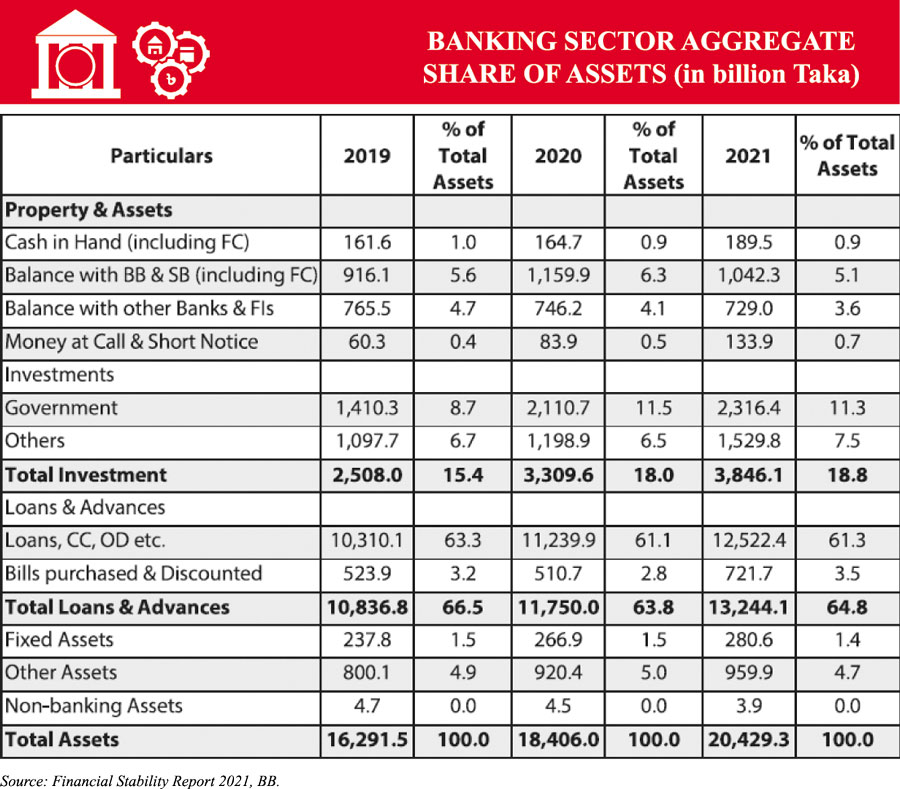

In Bangladesh, requirements for the financial reports of banks, non-bank financial institutions (regulated under the Financial Institution Act) and various companies are quite reasonable. The disturbing part is that these requirements are not properly complied with by various institutions. This means that the implementation (enforcement and compliance) of rules and regulations is an 'Achilles' heel'. Despite supervision and monitoring by the regulatory bodies such as Bangladesh Bank and BSEC, serious mismanagement and malpractices have occurred in the banking sector as well as in the capital market. The disclosure of banks in their financial reports is prepared following the International Accounting Standards-30 (IAS-30). This has been replaced by International Financial Reporting Standards (IFRS-7).

According to this format the financial disclosure is more logical, which means that banks now face a higher risk in investment and management of capital. If the required standard is followed, then depositors and clients of the banks and the general people will not face any loss. Besides IAS-30, there are also IAS-32, IAS-39 and IFRS-9, which are prescribed for the management, supervision, and monitoring of financial intermediaries. The government of Bangladesh promulgated the Financial Reporting Act (FRA) in September 2015. Under the aegis of the FRA, the Financial Reporting Council (FRC) started functioning in the middle of the year 2017. The FRC is empowered to cancel the registration of auditors and give punishment for fabricating audit reports. We expect that FRC will be proactive to bring discipline in the banking sector.

Regulatory regime of the financial sector of any country is important for effective and smooth functioning of all financial institutions. In the wake of global as well as domestic financial challenges an independent and strong central bank is essential. Central bank autonomy is a debatable but crucial issue. However, to achieve the objectives of the bank such as inflation control, economic stability, better financial management, etc., it is necessary for the central bank to be free from all external influences. Thus, the bank should be fully autonomous in all its functional and decisional activities.

Some attributes of interdependence are whether the central bank can refuse credit to the government; whether it can meet its expenses without depending on the government; whether its governor or board of directors can function independently; whether its governor is independent in following monetary policy; whether it is free to choose its monetary instruments; and finally, whether it is free to regulate and monitor the banking policy and the banks.

The main responsibilities of the Bangladesh Bank are monetary policy functions, to be a bankers' bank, a banker of the government and regulators as well as supervisor of the commercial banks. The functions of the Bangladesh Bank are quite large in number and wide in coverage like many central banks in the developing countries. However, in many countries, especially in some developed countries its functions are limited to monetary functions. For example, the Bank of England (BoE) deals with monetary policy functions and other functions are performed by Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA), two independent bodies under the overall guidance of BoE. Most of the Central Banks have dual functions like those of the Bangladesh Bank. Therefore, its tasks are enormous. The performance of the economy and that of the different sectors are closely linked with the performance of the Bangladesh Bank.

Implementing the vision and mission of the Bangladesh Bank face serious challenges and limitations. In the context of Bangladesh Bank, the debates on macroeconomic issues centered around how Bangladesh Bank can set up monetary targets without political pressure and how far monetary policy can be implemented without any political and structural limitations. The authority of the Bangladesh Bank over the constituent banks and financial institutions recently shows some limitations in controlling corruption, non-performing loans, ensuring good governance and strong management and finally enhancing public faith in the bank. It seems that Bangladesh Bank due to both "internal" (within the bank itself) and "external" (outside the purview of the bank) hurdles, finds it difficult to exert effective control over the banking sector. The pressure groups of stakeholders namely Bangladesh Association of Bankers (BAB) - an association of bank owners and, the Association of Bankers, Bangladesh (ABB) - an association of CEOs/ MDs of banks, play vital roles in the regulatory aspects of the banking sector.

However, in recent times, we have seen that many of the prudential and management norms are not followed by banks. There are several privately owned banks where a number of family members are on the Board of Directors, which is contrary to the notion of good corporate governance. Therefore, one of the main challenges for the banking sector is to ensure good corporate governance which will benefit the depositors, borrowers and investors, expand potential markets, broaden ownership, create alternative financing options, accelerate growth, increase employment and help reduce poverty in Bangladesh.

The recent situation in some banks and financial institutions reveals a very disturbing picture. The financial reports in some cases, mainly the audited ones, have been manipulated and facts concealed. The auditors as independent examiners have failed and worked with corrupt management. Some of the audit firms have been blacklisted by the Bangladesh Bank. The Financial Reporting Council (FRC) has also identified faulty audit reports. Strong actions have to be taken by the concerned regulatory bodies, namely, the Bangladesh Bank, the Financial Reporting Council and the Bangladesh Securities and Exchange Commission (BSEC). The Institute of Chartered Accountants of Bangladesh (ICAB) and the Institute of Cost and Management Accountants of Bangladesh (ICMAB) both have the responsibility of ensuring good and honest practices by the professional accountants, who are integral parts of good corporate governance.

To have an independent and effective Bangladesh Bank, the necessary aspects are:

a) more focus on core banking issues by the central bank,

b) appropriate and prudential management norms of the central bank that are not subject to frequent changes due to external political/administrative pressure, and,

c) a system of prompt corrective actions for management of crises and for legal/ administrative actions against persons responsible for crises in a particular bank or in the banking `system' as a whole.

In real-world situations, full independence and autonomy to the Central Bank may not be easily achieved. Therefore, the central bank like Bangladesh Bank can minimise political and other external pressure by constantly engaging with them and gaining public support for actions that may make Bangladesh Bank autonomous and effective. Whether in good or bad times, supervisors always face pressure from lobbyists and from politicians that can undermine the stability of the financial system.

To be successful in regulating the financial sector, the Bangladesh Bank must have very relevant and pragmatic "policies" and prudential management rules. It should also ensure that these are fully followed by all banks and financial intuitions. "Discretionary" powers or "ad-hoc measure" must be avoided to safeguard the independence and autonomy of the Bangladesh Bank. The typical case of "policy" versus "discretion" must be resolved with the firm stance of Bangladesh Bank where policies and rules will prevail -- not the discretionary powers of any individual and agency. Time has come for Bangladesh Bank to strike a balance, showing an appropriate professional stance while avoiding the danger of politically motivated reforms in a highly technical domain.

To meet the challenges, one of the most important tasks is to make the financial sector (banks, non-banks, insurance, capital market, microfinance market) more competitive and service-oriented catering to the needs of all types of clients across all the areas of Bangladesh. Along with this, the challenges of the external sectors (exports, import of goods and financial services) are also to be met by the regulatory bodies like Bangladesh Bank, National Board of Revenue.

The country needs to enforce strict adherence to regulatory and prudential guidelines that are effectively integrated among all institutions in the monetary sector and the financial sector. The global financial crises of 2007-08 and the present state of low global growth outlook due to the impact of Covid-19 and the Russia-Ukraine conflict point to the fact that there is no substitute for monetary policies with prudent and careful regulations even when market-based, liberalised structures operate. At the same time the central bank should not resort to overregulation of the financial sector, because that may stifle smooth functioning of economic activities.

The present challenges of high inflation rates, depreciation of taka against US dollar, rapid depletion of foreign currency reserve, increase in fuel prices and also low investment in the private sector have created a pressure on the domestic resources as well as foreign resources. What are needed now are improvement of fiscal management and implementation of budget by the government, especially by the Finance and Planning Ministries, and pragmatic monetary policy and monetary management by the Bangladesh Bank. These have to be done in a comprehensive and coordinated manner (often absent) based on reliable data/information, analysis of the problems, and consultation with experts in the relevant fields. Above all, good accountability and proper transparency of all financial transactions have to be ensured. The "political will" is essential to achieve success in all these areas.

Dr Salehuddin Ahmed is Former Governor of Bangladesh Bank and Professor at BRAC University, Dhaka.

asalehuddin@gmail.com

© 2026 - All Rights with The Financial Express