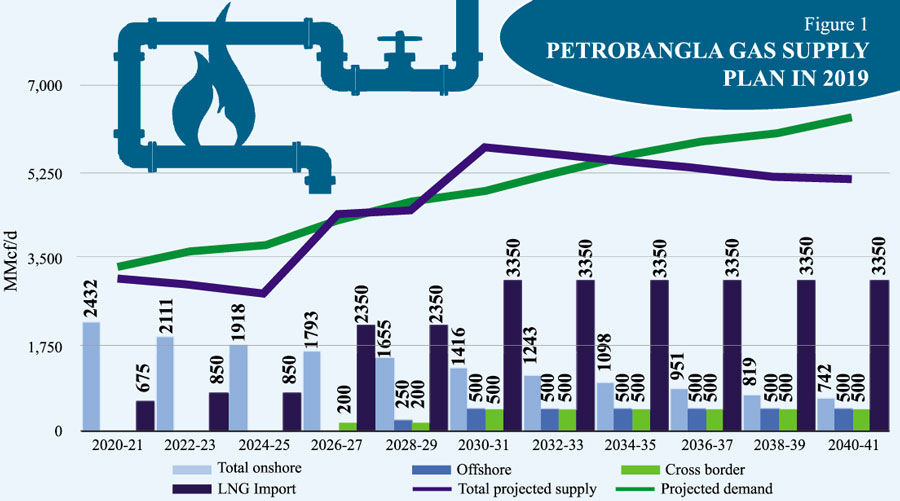

![]() The primary energy planning of the previous years starting from PSMP 2010 were heavily dependent on import. While the 2010 plan was more inclined on coal usage with 50% power coming from it, only 20% was meant from local sources. Since 2010, Petrobangla (300 mmcfd) and IOCs (700 mmcfd) were able to increase local gas production by 1,000 mmcfd (million cubic feet per day) peaking at 2,750 mmcfd in 2016-17. Typically a peak production is maintained for a plateau period of 6 to 10 years, especially from a portfolio of multiple producing fields. While IOCs were able to maintain their production, Petrobangla failed and as a result, the total production declined to 2,350 mmcfd in 2020-21. The power development board moved from the coal-heavy plan in their 2016 PSMP relying more on import - both on coal and LNG (liquefied natural gas) to produce 35% electricity by each with no local coal production. Adding another 10% from nuclear and 10% from cross border import, 90% of primary energy to produce electricity in 2041 was meant to be imported. Petrobangla showed a gas supply plan to match the PSMP (Power Sector Master Plan) 2016 demand with severe supply shortage until 2026 (Figure 1).

The primary energy planning of the previous years starting from PSMP 2010 were heavily dependent on import. While the 2010 plan was more inclined on coal usage with 50% power coming from it, only 20% was meant from local sources. Since 2010, Petrobangla (300 mmcfd) and IOCs (700 mmcfd) were able to increase local gas production by 1,000 mmcfd (million cubic feet per day) peaking at 2,750 mmcfd in 2016-17. Typically a peak production is maintained for a plateau period of 6 to 10 years, especially from a portfolio of multiple producing fields. While IOCs were able to maintain their production, Petrobangla failed and as a result, the total production declined to 2,350 mmcfd in 2020-21. The power development board moved from the coal-heavy plan in their 2016 PSMP relying more on import - both on coal and LNG (liquefied natural gas) to produce 35% electricity by each with no local coal production. Adding another 10% from nuclear and 10% from cross border import, 90% of primary energy to produce electricity in 2041 was meant to be imported. Petrobangla showed a gas supply plan to match the PSMP (Power Sector Master Plan) 2016 demand with severe supply shortage until 2026 (Figure 1).

The cross border and offshore gas supply shown in this figure are not even in the planning stage of any sort. The sudden jump of supply in 2026 is supposed to be from a 1,000 mmcfd land-based RLNG (Regasified Liquefied Natural Gas) plant, construction of which has not been awarded as yet. At the current rate of onshore gas decline, as shown in the Petrobangla projection, and just the two FSRUs (Floating Storage Regasification Units), the total gas supply would be 2,500 mmcfd in 2025 with demand for 4200 mmcfd. It is obvious that irrespective to post-Covid economy bounce back or the Russia-Ukraine war, we were in big trouble in our primary energy supply planning.

The cross border and offshore gas supply shown in this figure are not even in the planning stage of any sort. The sudden jump of supply in 2026 is supposed to be from a 1,000 mmcfd land-based RLNG (Regasified Liquefied Natural Gas) plant, construction of which has not been awarded as yet. At the current rate of onshore gas decline, as shown in the Petrobangla projection, and just the two FSRUs (Floating Storage Regasification Units), the total gas supply would be 2,500 mmcfd in 2025 with demand for 4200 mmcfd. It is obvious that irrespective to post-Covid economy bounce back or the Russia-Ukraine war, we were in big trouble in our primary energy supply planning.

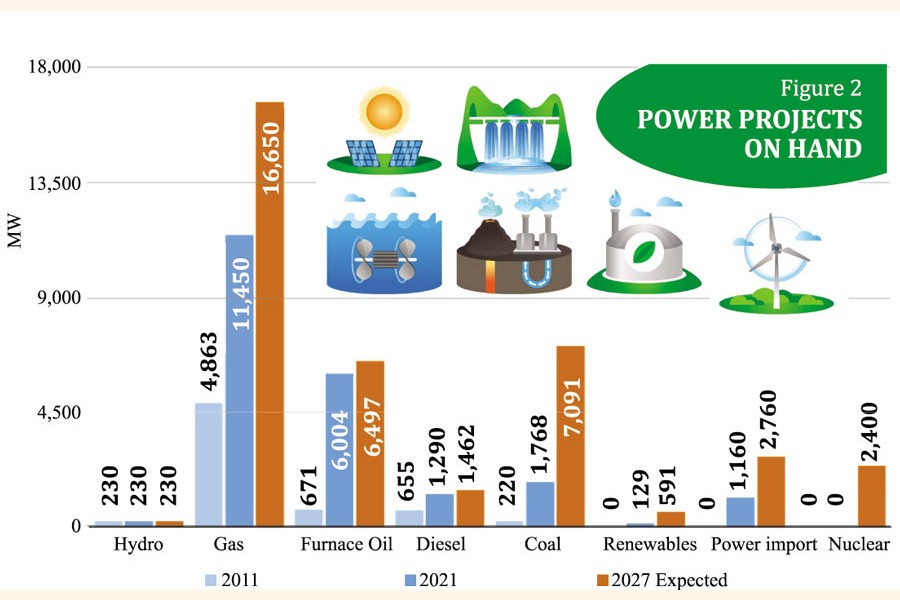

A closer look at the power projects in progress (Figure 2) shows that gas based power plants would reach 16,600 MW (megawatts) capacity in 2027 requiring at least 2500 mmcfd (0.9tcf per annum) gas and 7,000 MW coal requiring 25.5 million tons of coal per year. This would cost $11 billion @$12/mmbtu (1 Million British Thermal Units) and $5 billion (@$200/ton) respectively to import provided the current high energy price settles into a new equilibrium. Including oil for power plants (still at 6,000 MW) and transport, power import from India and nuclear fuel, the overall energy bill would be a whopping $25 billion in 2027. Taking some contribution from local gas, the conservative bill would be at least $20 billion a year. Using the PSMP 2016 plan or even the new IEPMP 2022 energy mix, the total energy import bill in 2041 would be no less than $40 billion a year.

Unless the country takes an about turn on its primary energy supply plan (heavy gas exploration, coal mining and serious government investment in renewable, storage and grid upgradation i.e. indigenous sources), Bangladesh needs to look into its energy import portfolio for the next 15 years - price and probable supply sources.

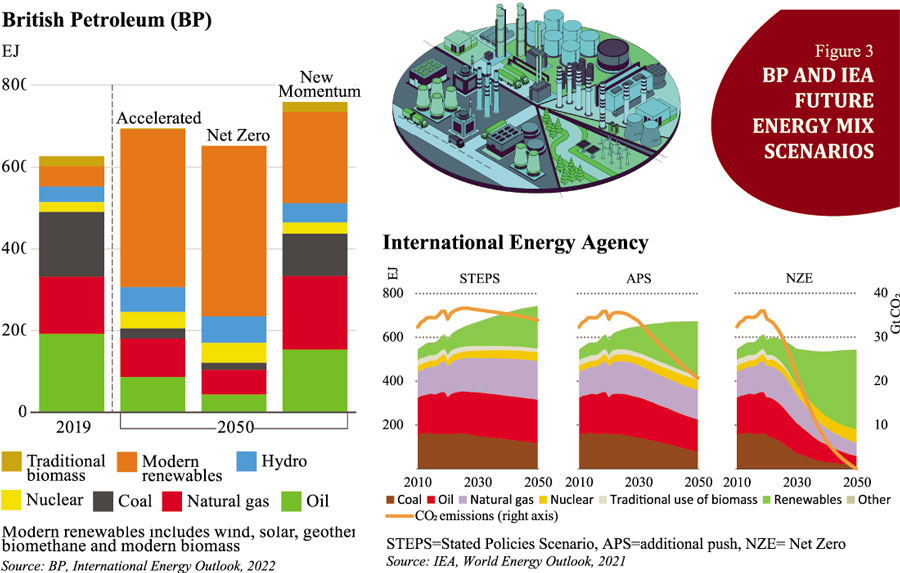

Despite the massive energy transition towards renewables, all major thinks tanks and agencies agree that, significant dependency on fossil fuel will prevail till 2050. Both the BP (British Petroleum) prediction and IEA (International Energy Agency) estimates (Figure 3) show that the even with the new momentum, the current stated policy will bring about one third of energy from renewables whereas to achieve net-

Despite the massive energy transition towards renewables, all major thinks tanks and agencies agree that, significant dependency on fossil fuel will prevail till 2050. Both the BP (British Petroleum) prediction and IEA (International Energy Agency) estimates (Figure 3) show that the even with the new momentum, the current stated policy will bring about one third of energy from renewables whereas to achieve net- zero that contribution need to be more than two third of the energy mix. Increasing global oil, gas and coal trading will prevail at least till 2040 but most likely beyond 2050. EIA (US's Energy Information Administration) and Exxon-Mobil forecasts project a very similar picture. These predictions are based on current technology.

zero that contribution need to be more than two third of the energy mix. Increasing global oil, gas and coal trading will prevail at least till 2040 but most likely beyond 2050. EIA (US's Energy Information Administration) and Exxon-Mobil forecasts project a very similar picture. These predictions are based on current technology.  A breakthrough in nuclear fusion or hydrogen or some other technology may change the scenario completely but no planning can be done on that probability. Wishing a carbon free world and achieving that are not the same. The net zero scenario shown in Figure 3 is more a wish than reality.

A breakthrough in nuclear fusion or hydrogen or some other technology may change the scenario completely but no planning can be done on that probability. Wishing a carbon free world and achieving that are not the same. The net zero scenario shown in Figure 3 is more a wish than reality.

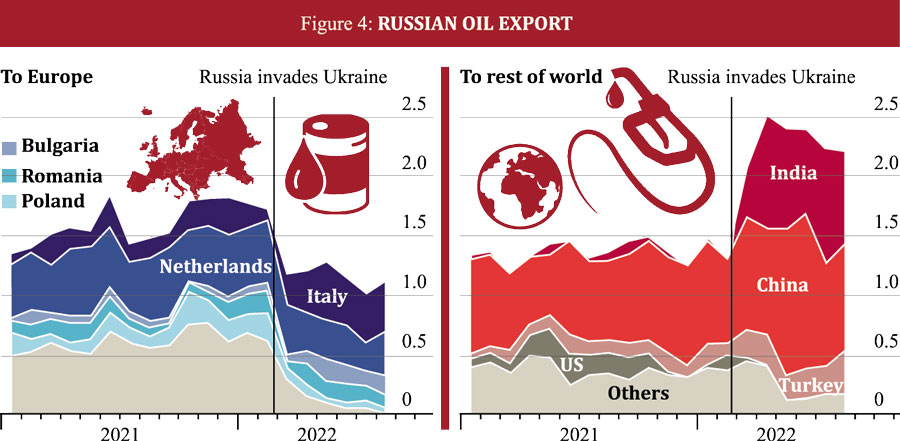

The Ukraine war has exposed the dependency of Europe on fossil fuel despite being most advanced in the renewable transition. Even after the war is over, Europe is not going back to Russia for its oil and gas need. The current sanction shows the movement of Russian oil shifting from Europe to Asia. The world cannot cope without Russian oil and gas. This war will just redistribute their flow. Russia will target the hungry Asian market through pipeline and also LNG in future. Figure 4 shows this shift.

Europe, on the other hand will focus on Middle East and North Africa or MENA. The EIA predicts that future oil and gas supply will come from MENA area whereas the Russian supply will increase moderately, both USA and Canada supply will decline.

In 2017 Qatar lifted a 12 year ban on the development of the world's largest gas field in Persian Gulf (also shared with Iran) and started its North Field Extension (NFE) for new LNG capability. The NFE project will increase its current 77 million tons per annum (mtpa) capacity to 110 mtpa in 2026. A further extension will increase the total capacity to 125 mtpa in 2027. Currently the top four LNG capacities are with Australia (87 mtpa), Qatar (77 mtpa), USA (73 mtpa) and Malaysia (31 mtpa). The USA export capacity will increase to almost 20 Billion cubic feet per day (Bcfd) from current 11 Bcfd. Europe could not secure long term supply from Qatar as most of its gas is tied with long term contracts, mostly with its preferred Asian clients.There are other projects in the planning as well. Australia is also investing to increase its LNG production. The current LNG crisis is encouraging the increase of long term oil indexed contracts (10 years) although gas indexing is also getting popular. Seventy five percent of all new contracts since 2021 is destination bound long term contracts.

There were very little investment in LNG capacity during Covid period due to uncertainty of market but the interest bounced back in late 2021 and increasing. Although uncertainty of LNG as a transition fuel prevails among the investors, new capacity is being added and due to demand destruction and economic slowdown, LNG supply and price is expected to ease out in 2024. For importing countries, the greatest challenge would be constructing regasification facilities and securing shipping contracts - both of them are in serious shortage right now. As of August 2022, just 20 FSRU were available or were under construction with 12 of them going to Europe. Nine more are in the planning.

High gas price did reduce gas demand. China, India, Pakistan, Bangladesh, Thailand either reduced or stopped purchasing spot LNG. The overall gas demand was reduced by 4% in the first eight months of 2022. This reduction varied from 9% to 30% in the Asia pacific region.

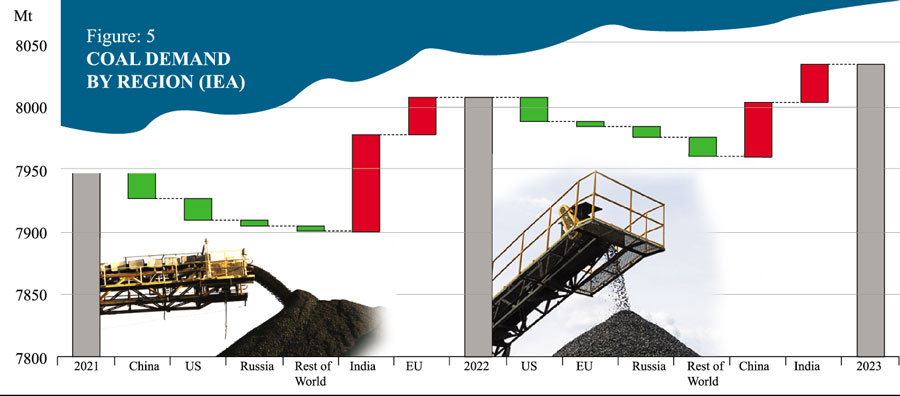

As a result, power production from both coal and oil increased in these countries. Coal demand is expected to increase by 60 million tons in 2022 and remain steady in 2023 with a slight increase. The key factor would be China and India, the two largest coal producers as well as consumers in the world.

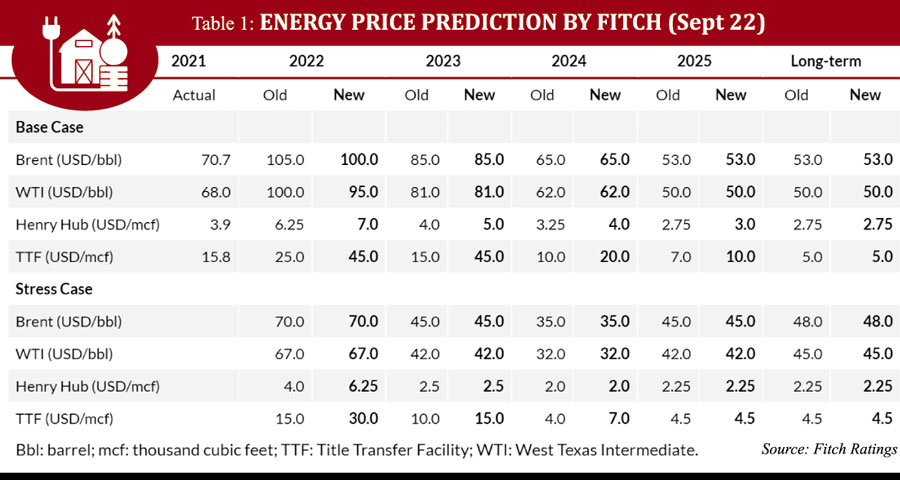

Energy price prediction is as good as gambling. Different investment banks routinely forecast energy price for their clients. Morgan Chase sees the possibility of crude price going over $350/bbl whereas Deloitte predicts the oil price varying between $76 and $105 per bbl between 2022 and 2041. Table 1, estimated by Fitch as of September 2022 shows very low future energy price. They assume zero gas supply to Europe by Russia. Long term coal price is expected to be much lower than the current price. The table clearly shows high energy price holding in 2023 and easing off in 2024 and stabilize by 2025. Most of the short term predictions are very similar. Just like the Ukraine war, any event may influence the future price. Planning is always done on the basis of an uneventful and predictable future but energy security is ensured by diversification of fuel and its sources.

Energy price prediction is as good as gambling. Different investment banks routinely forecast energy price for their clients. Morgan Chase sees the possibility of crude price going over $350/bbl whereas Deloitte predicts the oil price varying between $76 and $105 per bbl between 2022 and 2041. Table 1, estimated by Fitch as of September 2022 shows very low future energy price. They assume zero gas supply to Europe by Russia. Long term coal price is expected to be much lower than the current price. The table clearly shows high energy price holding in 2023 and easing off in 2024 and stabilize by 2025. Most of the short term predictions are very similar. Just like the Ukraine war, any event may influence the future price. Planning is always done on the basis of an uneventful and predictable future but energy security is ensured by diversification of fuel and its sources.

Despite our high hope and wish, renewable energy under the current infrastructure and technology will not resolve Bangladesh's rapidly increasing energy demand. It can definitely play a supplementary role and all efforts must be taken to promote and implement renewable projects especially availing the low hanging fruits like solar irrigation and rooftop. The government plan to mix fuel in the form of coal, gas and nuclear is the right approach. The biggest challenge in Bangladesh is timely implementation of the projects within budget. Enough has been said about the failure of exploring and developing indigenous energy resources - both gas and coal. The only officially approved energy policy of 1996 clearly stated the importance of developing our own coal, to bring parity in energy access between East and West part of the country and to avoid the mono-fuel dependency on gas. The economic case of coal development is well established. The challenge is environmental. The nation needs to seriously examine the possibility if our own coal could be developed within a reasonable and acceptable environmental compromise. The failure of managing our own gas fields for optimum production is clearly seen by the contrast between reserve production ratio of Petrobangla and the IOCs. The leadership in the gas sector failed the nation. To revive this sector, we need to inject fresh talent that can be found among the Bangladeshi expats working overseas. Government must invest in this sector.

Very few countries are indeed energy independent. Even if we succeed in increasing local primary energy supply, we will need to import. The current crisis taught us few things but it should not dictate our long term energy policy. Along with local supply, we must secure steady and sustainable sourcing of primary energy by import - coal, gas, cross border electricity, nuclear fuel. The baseline demand must be met through long term contracts and intermediate and/or peak demand can be procured through short term deals. The mistake done in our LNG contracts cannot be repeated. As we are getting involved in international energy trading, a dedicated team of professional trade managers must be built. The team will track international demand supply, price fluctuation and maintain a portfolio along with risk mitigation measures.

M Tamim is a Professor of Petroleum Engineering, BUET

© 2026 - All Rights with The Financial Express