The ripple effects of disruptions in international trade and price rises are being felt in Bangladesh as well. Rise in the cost of imports is having a negative effect on the trade balance which, in turn, created pressure on the country's foreign exchange reserve. The immediate result was mounting pressure on the exchange rate of Taka. Bangladesh Bank (the central bank of the country) tried to stem the depreciation of Taka by selling US Dollars in the open market - an operation that caused further pressure on foreign exchange reserve.

The other development was the impact of the rise in import costs on domestic prices. While "pass through" to domestic prices was immediate, administered prices of fuel were also raised, which added impetus to inflation. Thus, the economy of Bangladesh is now confronted with a multiple challenges on the macroeconomic front - balance of payments deficit, instability in the foreign exchange market and rising inflation.

Of course, one could also raise the issue of the debt burden. On that front, the present situation of Bangladesh is quite comfortable. Even after a rise, debt-GDP ratio was 33.9% in 2020-21. More importantly, the ratio of external debt to GDP (about 14%) was well below what is usually considered to be a safe threshold (one-third of GDP).

Developments mentioned above have given rise to intense discussion and commentary on the macroeconomic challenges being faced by the country. A pertinent question in this context is whether the situation should be characterised as one of "crisis", and whether there are imminent dangers facing the country. The present article addresses this question by looking at issues relating to the external account, foreign exchange reserve, exchange rate, and inflation. It also provides a brief outline of policy alternatives that are available and emphasises that low-income people must be protected from the fallout of measures that may be needed to bring back macroeconomic stability.

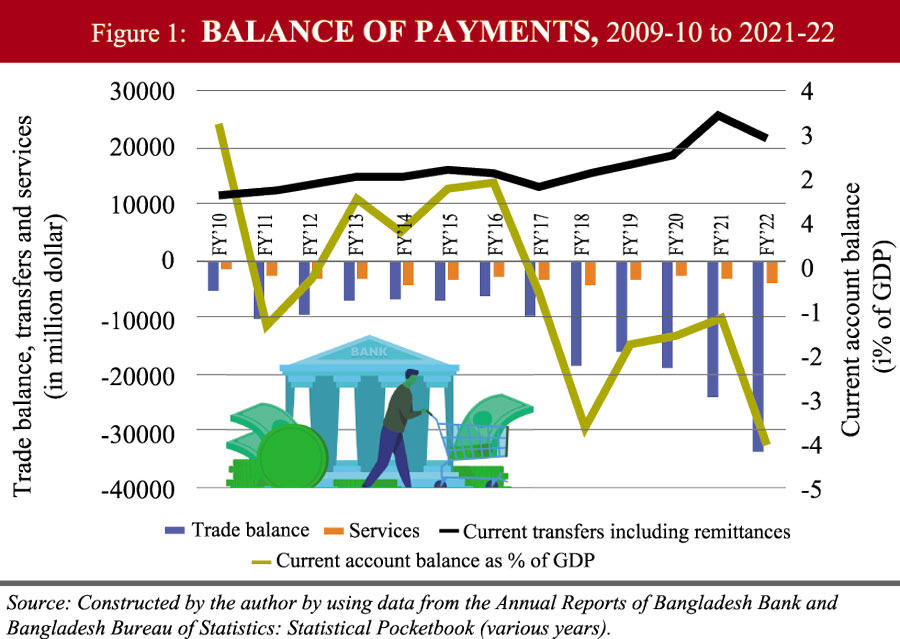

THE BALANCE IN THE EXTERNAL ACCOUNT WAS DISTURBED: Imports of the country often outstrip its earnings from exports, as a result of which, the trade balance is usually in deficit. And that is where the role of remittances comes in - to fill the gap in the trade account. As can be seen from Figure 1, since 2009-10, trade balance has always been negative. But there was a rise in the extent of deficit since 2015-16 and a sudden jump in 2017-18. As a result, the deficit in the current account as a proportion of GDP rose to 3.6%. However, there was no further deterioration in the two subsequent years. Rather, there was some improvement. Of course, during the pandemic-affected years, viz., 2019-20 and 2020-21, the economy experienced a downturn, and imports may have declined because of that.

In the course of 2021, the economy regained some momentum, and imports may have been rising because of that. However, a number of developments were taking place in the global arena. While increases in freight rates led to a rise in the cost of transporting commodities, as a result of the war between Russia and Ukraine, prices of commodities ranging from fuel and food also rose. Altogether, import costs started to rise. Although exports picked up, that was not adequate to meet the cost of imports.

In that kind of situation, remittances play an important role in narrowing the gap in the current account and bringing about a balance. But in 2021-22, there was a slowdown in its flow as well. It may be recalled in that context that during the first year of the pandemic (i.e., in 2020) there was a sharp fall in overseas employment, and hence the slowdown in the flow of remittance was natural.

The result was a rise in current account deficit which in FY2021-22 was 3.9% of GDP and was much higher than in the previous years. It's not that deficit of such a magnitude is completely unknown to the country; in 2017-18, it was 3.6%. But it came down in the subsequent three years. The question, however, is whether the situation will improve as quickly as before or the experience will be different this time. That will depend on a variety of factors like how quickly import volume can be reduced, what has been the real extent of capital flight from the country and whether it can be controlled, etc.  DEPLETION OF FOREIGN EXCHANGE RESERVE AND DEPRECIATION OF TAKA HAS CREATED INSTABILITY AND UNCERTAINTY: The other side of the external account is the reserve of foreign exchange. There was a time (during the 1970s and 1980s) when the country had very little foreign exchange reserve. It was during the 1990s that the situation started improving as both exports and remittances were growing. By 2000, the reserve was equal to about two and half months of import bill, and by 2009-10, the amount grew to about five

DEPLETION OF FOREIGN EXCHANGE RESERVE AND DEPRECIATION OF TAKA HAS CREATED INSTABILITY AND UNCERTAINTY: The other side of the external account is the reserve of foreign exchange. There was a time (during the 1970s and 1980s) when the country had very little foreign exchange reserve. It was during the 1990s that the situation started improving as both exports and remittances were growing. By 2000, the reserve was equal to about two and half months of import bill, and by 2009-10, the amount grew to about five

As the import bill started to rise in 2022, the amount of reserve started to decline; and for the fiscal year 2021-22, it fell to the equivalent of 5.1 months' import bill.In recent weeks (September-October 2022), it has fallen further. But if three months' import bill is considered to be the threshold, the amount of reserve can still be regarded as within the comfort zone. It may, however, be noted that as the country has graduated from low-income country to lower middle-income category and is in the process of coming out of the LDC status, its opportunities and challenges are likely to change considerably.Hence, rather than looking at the lower end of the threshold, the sight should be on a higher level and efforts should be to maintain such levels. It is from that point of view that the current situation appears to give rise to some concern.

This, of course, does not mean that the situation is critical. Developments during a few months do not necessarily represent a trend. Moreover, the extent to which the rise in import bill is due to transitory factors like increases in transport cost and sudden increases in food and fuel prices or due to structural factors needs to be carefully monitored. Rather than creating a perception of crisis (which may fuel further instability), the approach should be one of careful monitoring, review and adoption of appropriate measures to address the challenges.

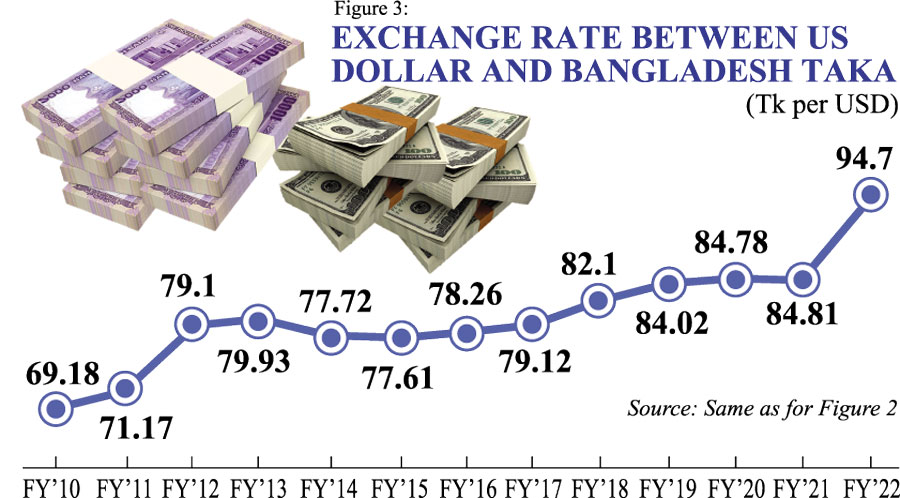

The fall in foreign exchange reserves led to a depreciation of Taka (Figure 3) and instability in the foreign exchange market. This happened after a period of stability, and the central bank attempted to prevent a slide in the value of the currency by selling US Dollars in the market. That resulted in further fall in foreign exchange reserves, and the exchange rate became volatile. From Tk.85 for one US Dollar in early 2022, it rose to Tk. 95 in August and over Taka (Tk) 100 in September. But the rate was worse in the open market, and at times the difference between the two was found to range between Tk10 - Tk15 (in contrast to the usual range of two to three Taka). Also, the rates fluctuated sharply - thus indicating uncertainty.

In view of the fall in reserves and depreciation of the currency, the government undertook a variety of measures to control imports and save foreign exchange in other ways. As the impact of such measures was not visible immediately, some economists advised an immediate free float of the exchange rate. However, the matter should not be looked at in such a simple manner.

A major challenge in the management of exchange rate is avoiding the adverse effects of both overvalued and undervalued currency. A sudden and sharp devaluation of the domestic currency can create inflationary pressure by raising the domestic prices of imported goods. In a situation where prices of a number of commodities in the international market had already risen, and inflation has already started to rise, one has to be careful before taking any step that may fuel the process. Moreover, a sharp depreciation of the currency may unleash forces leading to a contraction of the economy.

ALTERNATIVE APPROACHES TO EXCHANGE RATE MANAGEMENT MAY BE CONSIDERED: It is important to consider alternatives to sudden and sharp depreciation of the domestic currency. And in that context, it may be useful to consider the method of "crawling peg" that involves gradual adjustment of the exchange rate to reflect the real strength of the currency. In this arrangement, necessary adjustments are made in the exchange rate on the basis of changes in the real effective exchange rate. However, an efficient use of this method would require the central bank to work on the basis of objective criteria and without political interference. This may be quite a challenge, especially in situations where the central banks are not fully independent. Perhaps it is because of the difficulty of applying this method, the conventional view is to opt for a market-determined system of exchange rate. In fact, the recent record of exchange rate management in Bangladesh also shows the fault line.

It can be seen from Figure 3 that during 2009-10 to 2020-21, the exchange rate changed substantially only once and there was no change in three years from 2018-19 to 2020-21. Although a floating exchange rate system was adopted in 2003, it is quite clear that the currency was not allowed to find its own value in the market. During this period, the currencies of a number of other developing countries of Asia, e.g., India, Pakistan, Vietnam, etc. underwent substantial depreciation. A look at the movement of the real effective exchange rate of Bangladesh's currency indicates that the exchange rate needed to be adjusted substantially. Instead, efforts were made to keep the exchange rate unchanged by selling US Dollars in the market. And that led to a further depletion of the foreign exchange reserve. It is thus clear that inefficiency in the management of exchange rate and failure to undertake needed steps on a timely basis resulted in the instability that is being witnessed currently.

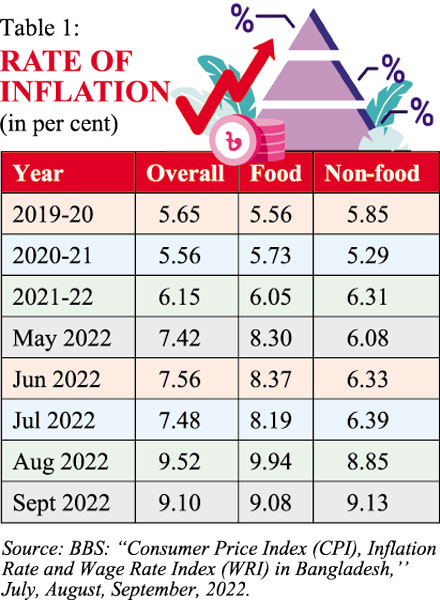

RISE IN INFLATION RATE HAS MADE THE MACROECONOMIC CHALLENGE HARDER: When inflation started rising globally during 2021, it was ascribed basically to the pandemic induced disruption in the supply chain and shortages of commodities resulting from such disruptions. Although it was generally thought that the tendency for commodity prices to rise would be short-lived, that has not been the case. In fact, many countries in the developed world are witnessing rates of inflation not seen during the past four decades (eight to nine per cent as opposed to less than 2% till 2020).

If one looks at the experience of Bangladesh since 2009-10 (Figure 4), it can be seen that except for a few years of fluctuation, inflation has remained under control - between five and six per cent - for much of the period. That trend was disrupted in the second half of 2022. There are at least two reasons for worrying about rising inflation. First, it is bad for the economic environment, for investment decisions and hence, for growth. Second, it creates misery for the poor and low-income people - especially in situations where their incomes cannot rise in tandem with price increases. But the key questions in this respect are: at what level inflation starts affecting growth adversely, (ii) what instruments are appropriate for fighting it, and (iii) what can be done to provide protection to the poor and low-income people against its adverse effects?

The answer to the first question has to be based on carefully conducted research. But recent experience shows that even when inflation rates went up to about 7%, there was no adverse effect on economic growth. Research by the present author covering data for the period 2000-2001 to 2015-2016 did not show the expected negative relationship between inflation and GDP growth. Of course, that period did not witness very high rates of inflation (like over ten per cent). Other research has shown that the relationship between economic growth and inflation is not linear; both very low and very high rates of inflation are bad for growth. At what rate inflation starts hurting an economy have to be established on the basis of carefully conducted research.

CONVENTIONAL TOOLS FOR FIGHTING INFLATION MAY NOT BE APPROPRIATE IN ALL SITUATIONS: As for instruments to fight inflation, conventional economics would tell us to use monetary policy - and more specifically, interest rate. The current experience also shows that central bankers around the world are relying on this tool. But inflation can be caused by a variety of factors, and there is not much justification for using the same instrument without due regard for the causes. Interestingly, the tightening of monetary policy through interest rate increases has not yet produced the desired result even in the developed world. But it is already producing a negative effect on output growth, if not outright recession. And as monetary policy normally works with a time lag, the outlook for 2023 appears to be worse - both in terms of economic growth and unemployment. The ripple effects of such developments are bound to affect growth, exports and employment in Bangladesh. Hence, policymakers in the country need to be extra careful before adopting measures to fight inflation. The responsibility of the central bank is not simply to maintain macroeconomic stability but also to ensure that economic growth and employment are not adversely affected.

Interestingly, the tightening of monetary policy through interest rate increases has not yet produced the desired result even in the developed world. But it is already producing a negative effect on output growth, if not outright recession. And as monetary policy normally works with a time lag, the outlook for 2023 appears to be worse - both in terms of economic growth and unemployment. The ripple effects of such developments are bound to affect growth, exports and employment in Bangladesh. Hence, policymakers in the country need to be extra careful before adopting measures to fight inflation. The responsibility of the central bank is not simply to maintain macroeconomic stability but also to ensure that economic growth and employment are not adversely affected.  THE CURRENT POLICY STANCE INDICATES AMBIVALENCE ON THE PART OF THE GOVERNMENT: The policy alternatives available to address the macroeconomic challenges being faced by the country may be briefly outlined as follows. Those following conventional economic theory would recommend (i) a one-time devaluation of the currency and use of market mechanism to determine the exchange rate; and (ii) the use of monetary policy, and more specifically, rate of interest for fighting inflation.

THE CURRENT POLICY STANCE INDICATES AMBIVALENCE ON THE PART OF THE GOVERNMENT: The policy alternatives available to address the macroeconomic challenges being faced by the country may be briefly outlined as follows. Those following conventional economic theory would recommend (i) a one-time devaluation of the currency and use of market mechanism to determine the exchange rate; and (ii) the use of monetary policy, and more specifically, rate of interest for fighting inflation.

Alternatively, it should be possible to combine some variant of the above measures and adopt a more nuanced approach. That would include: (i) using the "crawling peg" approach to exchange rate determination, (ii) abandoning the fixed interest approach to savings and credit and allowing the market to determine them, (iii) close monitoring of the flow of credit and ensuring credit flow without hurdles and complications, and (iv) adopting measures needed to ensure competition in the market for key consumer goods and removing bottlenecks in the supply chains.

The steps taken by the government in recent weeks - both in the area of exchange rate and monetary policy indicate that it is suffering from a degree of ambivalence as to what policy path to follow. For example, while there have been attempts to support the value of Taka, at times there were signs that such efforts are being abandoned. There were also statements that the government would soon leave the exchange rate to be determined by the market. Likewise, in the area of monetary policy, although the fixed rates of interest on savings and credit have not been abandoned, the repo rate has been raised recently. Lack of consistency in the government's policy steps has not helped stabilize the macroeconomic situation.

THE LOW-INCOME PEOPLE MUST BE PROTECTED FROM THE ADVERSE EFFECTS OF STABILISATION MEASURES: As a further sign of ambivalence, the government has approached the IMF for credit in a bid to overcome the current macroeconomic instability.It is well-known that assistance from an organisation like this is usually associated with conditions based primarily on conventional economic theory. The past experience with such loans shows that they were associated with measures like raising administered prices (e.g., of fuel) and reducing subsidies. Prices of fuel have already been raised recently - a measure that has provided impetus to the growing inflationary pressures. As mentioned earlier, the poor and low- income people are bearing a greater brunt of the rise in inflation. It will be unfortunate if measures adopted for macroeconomic stabilisation further worsen their situation. Whichever policy path is followed by the government, the pursuit of stabilisation should be accompanied by measures to provide protection to the poor and low-income people. If necessary, fiscal policy should be employed for that purpose.

Rizwanul Islam, an economist, is former Special Adviser, Employment Sector, International Labour Office, Geneva.

rizwanul.islam49@gmail.com

[This article is based on parts of the new edition of the author's book in Bengali titled Unnayaner Arthaniti (Economics of Development), UPL, Dhaka (forthcoming). The author is thankful to Professor Mustafizur Rahman, Professor S.R. Osmani and Dr. M. Muqtada for valuable comments on earlier versions of the work. However, the usual disclaimer applies.]