Mohammad Masudur Rahman and Anna Strutt | November 23, 2022 00:00:00

![]() LDC graduation is a watershed moment for any emerging economy. The Least Developed Countries (LDCs) are very specific low-income developing countries that are more vulnerable compared to other developing countries. The United Nations Committee for Development Policy (UNCDP) classified the LDCs in the 1960s in the UN resolution 2768 (XXVI). The WTO and the World Bank follow this classification for their different preferential tariffs and loan arrangements. The UNCDP reviews and monitors the status of LDCs and makes recommendations on graduating from the category.

LDC graduation is a watershed moment for any emerging economy. The Least Developed Countries (LDCs) are very specific low-income developing countries that are more vulnerable compared to other developing countries. The United Nations Committee for Development Policy (UNCDP) classified the LDCs in the 1960s in the UN resolution 2768 (XXVI). The WTO and the World Bank follow this classification for their different preferential tariffs and loan arrangements. The UNCDP reviews and monitors the status of LDCs and makes recommendations on graduating from the category.

There are currently 46 LDCs on the United Nations' (UN) list, 35 of which have become members of the World Trade Organization (WTO). These 46 LDCs consist of 986 million people but account for only 1.3 per cent of global GDP and 0.9 per cent of global trade (World Bank 2020). Interestingly, a number of these countries will be graduating in a few years, marking a significant development achievement. For example, Bhutan is set to graduate in 2024 while Bangladesh, Lao PDR and Myanmar will do so in 2026.

Bangladesh has been recommended for graduation after meeting all three thresholds for LDC graduation, namely Gross National Income (GNI) per capita, Human Asset Index (HAI), and Economic Vulnerability Index (EVI), as reviewed by the Committee for Development Policy (CDP) of UN Economic and Social Council in 2021. Bangladesh has been a frontrunner among LDCs in South Asia, with an average economic growth rate approximating 6.5 per cent over the last decade, including a growth rate of 6.9 per cent in 2021, during the Covid-19 pandemic (Bangladesh Economic Review, 2022). Bangladesh has become a global role model for its socio-economic development miracle from a "basket case" as dubbed by Henry Kissinger in 1971.

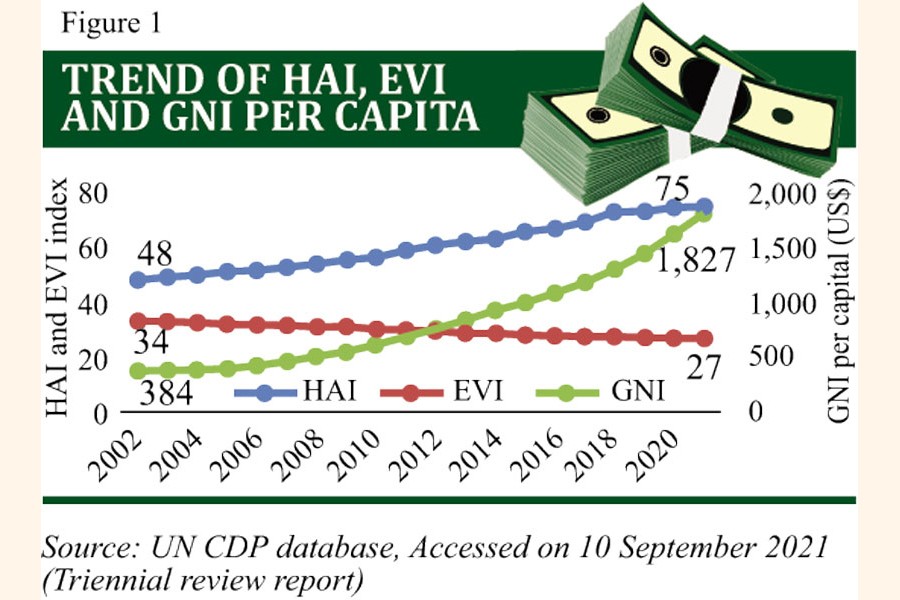

Bangladesh has made significant progress in the GNI per capita, HAI, and EVI. The GNI per capita has increased five-fold over two decades (Figure 1). With respect to GNI per capita, the graduation threshold is US$1222, and Bangladesh's was at US$1827 in 2021. The country has also surpassed Pakistan and India in GNI per capita. However, compared to the developing country average (US$ 6666), it is still much lower. Bangladesh has also made remarkable progress in its socioeconomic development. The adult literacy rate has increased sharply over the decades and the mortality rate has also dropped significantly. As reviewed by the CDP, the HAI index for Bangladesh accounted for 75.3 in 2021, when the threshold level for graduation is 66. However, Bangladesh remains behind the developing countries' average HAI of 78.3.

The EVI shows how vulnerable a country is in terms of economic and environmental shocks. Although the GNI per capita and HAI have substantially increased over the decades, the EVI has not decreased considerably, due to ongoing environmental vulnerability. The EVI index was 34 in 2000 and 27 in 2021 while the threshold is 32 or below. As Bangladesh continues to face different types of environmental shocks -- both natural and man-made disasters -- there is a huge scope for reducing environmental vulnerability.

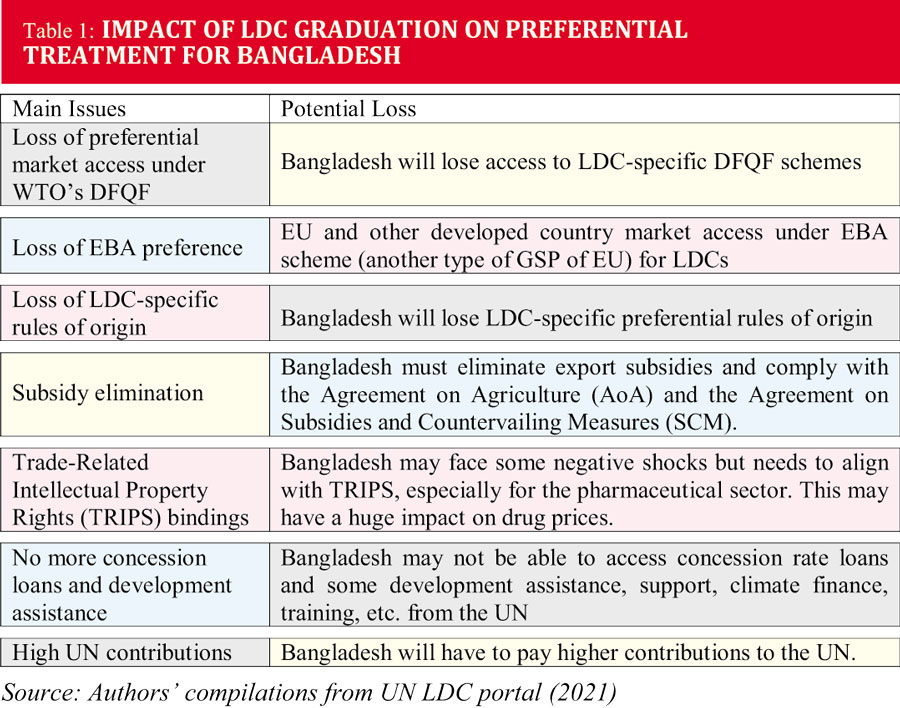

Against this background, Bangladesh is set to graduate from the LDC category by 2026. On one hand, graduation from the LDC category may give Bangladesh more self-dignity and some economic benefits, including an improved credit rating and a more attractive environment for foreign investment. However, on the other hand, Bangladesh will lose preferential market access to many countries. It must also eliminate domestic trade-restrictive policies, especially export subsidies and the country may no longer enjoy some concessional official development assistance or loans (WTO & EIE, 2020).

The WTO (2020) analyses the varying impacts resulting from LDC graduation, including summarising smooth graduation options. Specific to Bangladesh, the United Nations Department of Economic and Social Affairs (2019) qualitatively analyses the possible effects of LDC graduation which relate to trade and development cooperation. The Economist (2018) observes that although Bangladesh will miss out on concessional financing and preferential market access to export markets upon graduation, the graduation will help attract foreign investments as it stands as a testament to Bangladesh's good growth performance over the years.

When Bangladesh graduates from the LDC status to a developing country, it will in principle lose most of its preferential market access. The country will not only lose preferential market access but also lose preferential rules of origin reserved for LDCs. However, Bangladesh would remain eligible for standard Generalised System of Preference (GSP) which are preferential tariffs that are lower than Most Favoured Nation (MFN) tariffs in the EU and some other developed markets.

The EU is the biggest trading bloc which provides three types of GSP for developing countries: standard GSP, GSP plus (+), and Everything but Arms (EBA) arrangement. [Under the standard GSP and GSP plus(+) arrangement, the EU grants tariff reductions for products covered by about 66 per cent of tariff lines originating from developing countries, depending on countries' socioeconomic performance.] Under the EBA, the EU grants duty-free market access for all imported products except arms from LDCs like Bangladesh, which will be eliminated after graduation and standard GSP will be in place, instead. Moreover, as an LDC, Bangladesh has also been enjoying duty-free market access to most developed markets under the Duty-Free, Quota-Free (DFQF) arrangement of the WTO. Recently China has offered duty-free market access for 98 per cent of tariff lines under the Asia Pacific Trade Agreement (APTA) and DFQF. Bangladesh has also been enjoying different preferential access to markets in India and other South Asian markets under the South Asian Free Trade Agreement (SAFTA). Therefore, Bangladesh has been enjoying preferential access to most key global markets under GSP, DFQF, or regional free trade agreements.

Bangladesh has significantly benefited from the EU's preferential treatment over the decades, even in the post-MFA era. Bangladesh's exports to the EU were US$ 1.5 billion in 2001, which increased to US$ 26 billion in 2019 (Europa, 2020). The utilisation rate of the GSP in the EU market is about 96 per cent which indicates that Bangladesh has been very successful in exporting its products to the EU market.

However, this also implies that Bangladesh is highly dependent on the EU's GSP, and any preference erosion may have a significant negative impact on Bangladesh's exports to the EU. The EU has also benefited from lower prices when importing from Bangladesh, which increased economic welfare in the EU (World Bank, 2020).

However, this also implies that Bangladesh is highly dependent on the EU's GSP, and any preference erosion may have a significant negative impact on Bangladesh's exports to the EU. The EU has also benefited from lower prices when importing from Bangladesh, which increased economic welfare in the EU (World Bank, 2020).

Additionally, many other regulatory issues must be compatible with the global trading system. Export subsidies, especially for industrial products, have to be eliminated after graduation, at least in principle. [The WTO prohibits most direct export subsidies, except for LDCs. However, it is evident that many countries provide different subsidies and may not inform the WTO regularly.] Other WTO members could -- if subsidies are not eliminated -- take action against Bangladesh under Article 4 of Subsidies and Countervailing Measures (SCM) of the WTO and ask for the withdrawal of the subsidy.

Bangladesh has been using different instruments to support its export sector. The main tools are bonded warehouse facilities, duty drawbacks, direct export cash incentives, various tax concessions, tax holidays scheme, and export credits. Three main support measures were duty drawbacks, a bonded warehouse, and cash subsidies which comprised about 3.7 per cent of GDP in 2018. Bangladesh's main export item is ready made garment (RMG), which comprised about 87 per cent of Bangladesh's total exports in 2019 (Bangladesh Bank, 2020). Therefore, most of these export subsidies of about US$11 billion goes to the apparel sector. [The apparel industry in Bangladesh is mainly readymade garment (RMG), the finished products. The average MFN import duty is about 10 per cent on RMG products, which most countries will impose on imports from Bangladesh.]

Bangladesh has been using different instruments to support its export sector. The main tools are bonded warehouse facilities, duty drawbacks, direct export cash incentives, various tax concessions, tax holidays scheme, and export credits. Three main support measures were duty drawbacks, a bonded warehouse, and cash subsidies which comprised about 3.7 per cent of GDP in 2018. Bangladesh's main export item is ready made garment (RMG), which comprised about 87 per cent of Bangladesh's total exports in 2019 (Bangladesh Bank, 2020). Therefore, most of these export subsidies of about US$11 billion goes to the apparel sector. [The apparel industry in Bangladesh is mainly readymade garment (RMG), the finished products. The average MFN import duty is about 10 per cent on RMG products, which most countries will impose on imports from Bangladesh.]

Against this backdrop, the main objective of this study is to quantify some key aspects of the economic impact of Bangladesh's graduation from LDC status. This represents an important case study of an emerging economy that may have valuable policy insights for other LDCs. We deploy the MyGTAP framework developed by Walmsley & Minor (2013), an extension of the standard GTAP model (Hertel, 1997). This framework allows us to incorporate country-speci?c information to investigate the impacts of trade policies on different household groups (Walmsley & Minor, 2013). We include ten rural and urban regional households, which enables us to explore the potential economic impact of LDC graduation on the national economy as well as households' incomes and consumption.

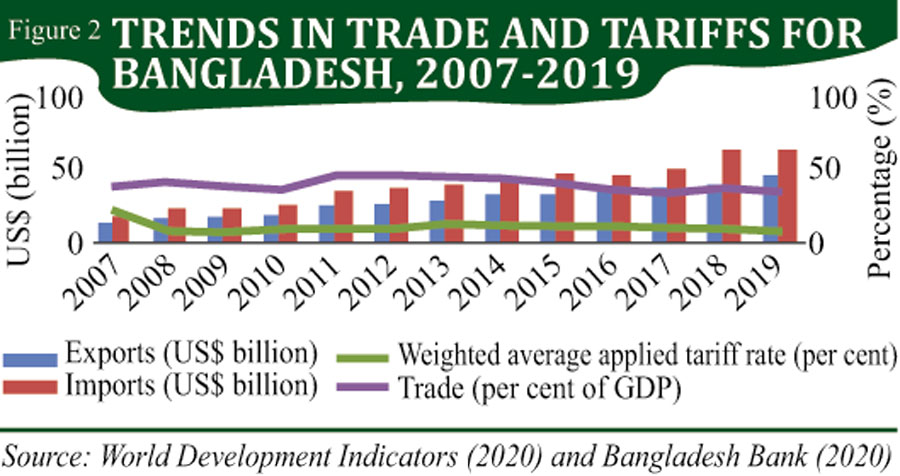

BANGLADESH TRADE REGIME AND PREFERENTIAL MARKET ACCESS: Bangladesh trade regime. In 2019, Bangladesh had a real GDP growth rate of 8.2 per cent, compared to the South Asian average of 5.5 per cent (WDI, 2020). Bangladesh's total trade increased from US$ 27 billion in 2006 to US$111 billion in 2019, with a trade openness ratio of about 38 per cent in 2019, which reflects how integrated the country is with the global economy (Figure-2). Bangladesh exported US$47.4 billion to the world in 2019, with top destinations being the EU, the US, Japan, Canada, and India. Bangladesh's weighted average applied tariff rates decreased moderately over the decade from 21 per cent in 2006 to 10 per cent in 2019 (World Bank, 2020).

Bangladesh's main export items are knitwear (HS61), woven garments (HS62) and home textiles (HS63), which together accounted for 86 per cent of total exports in 2020, as shown in Appendix Figure A3. Bangladesh also exports some jute and jute products, footwear, agricultural products and frozen food products. Bangladesh's leading export destination is the EU which accounted for about 56 per cent of its total exports in 2020, followed by the USA (17 per cent) and Japan (4 per cent). Bangladesh's export to its neighbours, especially China and India, is less than one billion dollars..

Over the past decade, Bangladesh's export boom, particularly in the ready-made garments sector, has helped Bangladesh achieve signi?cant economic growth. This success in the apparel industry is linked with an abundance of low-skilled labour, positively related to backward linkages in global value chains (GVCs). According to the United Nations Economic and Social Commission for Asia and the Pacific, Regional Integration and Value Chain Analyzer (UNESCAP RIVA) 2017 database, Bangladesh's forward linkages constituted 13.2 per cent and backward linkages 14.1 per cent of its gross exports to the world. The main sector that leads Bangladesh's GVC participation in both forward and backward linkages is the textiles and clothing sector. About 16.1 per cent of RMG sector's gross exports to the world comprise imported content and 10.9 per cent of RMG sector's gross exports to the world are used in further export production. The textile sector is by far the most important sector for Bangladesh that participates in GVCs.

The World Bank's (2020) report on GVCs shows that Bangladesh has successfully integrated its apparel sector using its large pool of low-skilled, low-cost labour. The report also indicates Bangladesh has successfully utilized its preferential market access in the global apparel industry, which plays a critical role in the country's economic growth miracle. However, Bangladesh has higher backward GVC participation of imported intermediates and capital goods than its forward GVC participation, reflecting a pattern of exports largely focused on final goods rather than intermediates (UNCTAD, 2020). As the country prepares to graduate from being an LDC, upgrades from the firm level are needed in terms of efficient process and functions, more sophisticated products, and overall value chain linkages.

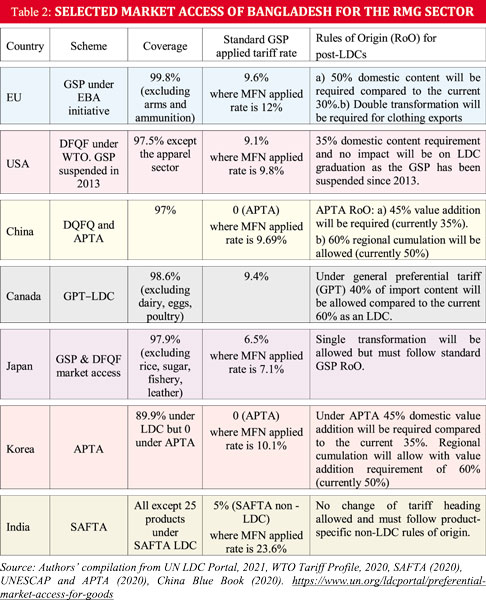

Preferential market access. Table 1 summarises the ways in which Bangladesh will lose preferential market access and other preferential treatment with graduation. Table 2 shows the current level of preferential market access that Bangladesh and many other LDCs have been enjoying over the decades. The EU, Canada, Japan, Australia and some other countries mostly offer duty-free market access when importing from LDCs.

Preferential market access. Table 1 summarises the ways in which Bangladesh will lose preferential market access and other preferential treatment with graduation. Table 2 shows the current level of preferential market access that Bangladesh and many other LDCs have been enjoying over the decades. The EU, Canada, Japan, Australia and some other countries mostly offer duty-free market access when importing from LDCs.

Tariffs on the apparel sector are much higher in the EU, USA, China, Japan, and Canada compared to the average applied tariff on industrial products. Table 2 shows the average standard GSP tariff on the apparel sector in selected markets. The MFN-applied tariffs and standard GSP on the apparel sector are comparably higher in most countries (WTO Tariff Profile, 2020) compared to manufacturing products. The MFN tariffs on the apparel sector are much higher in the EU than the average applied tariffs on industrial products. The EU has tariff protection of about four per cent for  fabrics, eight per cent for semi-finished garments and 12 per cent MFN rate for clothing (Europa, 2020). As 87 per cent of Bangladesh's exports are garments, most of these would face standard GSP tariffs of 9.6 per cent in the EU (WTO, 2020). This indicates that Bangladesh may face high tariffs exporting to most of the developed market after graduation. However, the USA had suspended GSP importing from Bangladesh in 2013 and offered a 97 per cent tariff line under DFQF but did not provide any duty-free market access for the apparel goods imported from Bangladesh.

fabrics, eight per cent for semi-finished garments and 12 per cent MFN rate for clothing (Europa, 2020). As 87 per cent of Bangladesh's exports are garments, most of these would face standard GSP tariffs of 9.6 per cent in the EU (WTO, 2020). This indicates that Bangladesh may face high tariffs exporting to most of the developed market after graduation. However, the USA had suspended GSP importing from Bangladesh in 2013 and offered a 97 per cent tariff line under DFQF but did not provide any duty-free market access for the apparel goods imported from Bangladesh.

Table 2 also shows a major erosion of preference of the post-graduation rules of origin scenario for the major markets. In the EU market, 50 per cent domestic contents will be required compared to the current 30 per cent, and double transformation  will be required for clothing exports (e.g., from yarn to fabric to clothing) compared to the current single transformation (e.g., from fabric to clothing). Similar rules of origin requirement will apply to most developed markets, which will negatively impact Bangladesh's exports.

will be required for clothing exports (e.g., from yarn to fabric to clothing) compared to the current single transformation (e.g., from fabric to clothing). Similar rules of origin requirement will apply to most developed markets, which will negatively impact Bangladesh's exports.

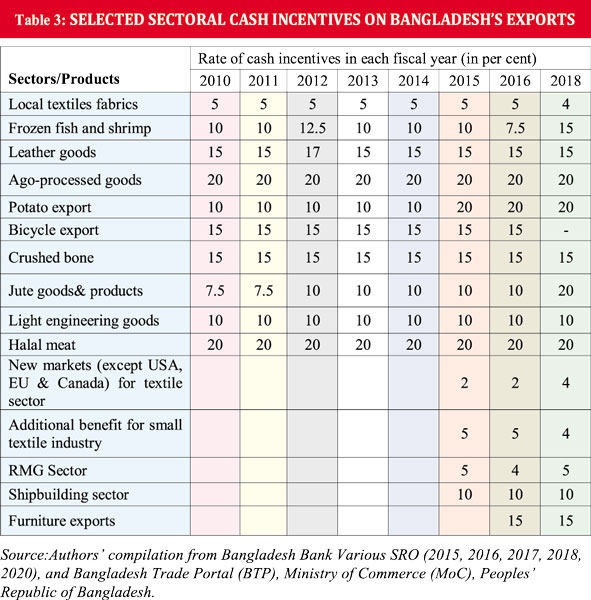

Export subsidies scenarios. Bangladesh has been using different supporting instruments to boost its export over the years. The main mechanisms are the bonded warehouse facilities, duty drawbacks, direct export cash incentives, various tax concessions, tax holidays scheme, and export credits. Table 3 shows the different export incentives ranging from five per cent to 20 per cent of exports in various sectors over the decades.

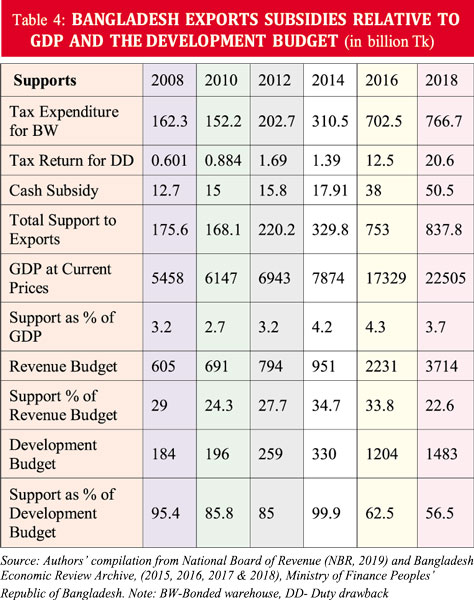

The three main support measures for exports, i.e. duty drawbacks, bonded warehouse facilities, and cash subsidies, accounted for about 3.7 per cent of GDP in 2018, 22.5 per cent of the revenue budget and 56.5 per cent of the development budget (Table 4). Recently, the government of Bangladesh has declared an additional US$ 560 million cash subsidy to rescue exports from the COVID-19 pandemic.

MODELLING FRAMEWORK: To comprehensively model the economy-wide impacts of Bangladesh's graduation, we employ computable general equilibrium (CGE) modelling, using the 10a version of the Global Trade Analysis Project (GTAP) database and model. The detailed structure of the GTAP model assumptions, equations, standard closure, elasticities, and parameters, are presented in Hertel (1997), with details of the current database provided in Aguiar et al. (2019).The GTAP framework includes detailed interactions between different sectors within and across countries, as well as regional households and governments.

In this paper, we use the MyGTAP augmentation of the GTAP model, developed by Walmsley & Minor (2013). MyGTAP is a customized and extended version of the GTAP model that enables us to incorporate country-specific data to investigate the impacts of different domestic policies on the household level, with a focus on generating insights for country-specific analysis. While the standard GTAP model assumes a single regional household, in the MyGTAP model, we eliminate the single 'regional' household for each country, instead incorporating private households and a government (Walmsley & Minor, 2013). The model we employ also permits incorporating factors of production and multiple private households as well as incorporating income from remittances, foreign aid, foreign capital, and government income. In the MyGTAP framework, the government collects income from taxes, duties revenue and foreign aid, spending this income on public consumption, transfers to households, foreign aid outflow, and subsidies. Similarly, private households receive and accumulate their income from factors of productions, transfers from the government and other households and foreign remittances. This accumulated income could be spent on consumption from different sectors, transfers, remittances outflow, and some savings. [Details of the econometric exercise is skipped here. To get the full paper, please see: www.doi.org/10.1080/09535314.2022.2138271]

SIMULATION SCENARIOS: Given that Bangladesh is set to graduate from being an LDC by 2026, Bangladesh must prepare for the post-graduation environment in which it will not be able to access preferential market access under the WTO's DFQF framework and preferential GSP, including EBA arrangement in the EU market. We simulate the following four scenarios to generate insights into the potential impact of graduation on Bangladesh:

l Under scenario one, we explore the potential impact if the EU, UK, Japan, Canada, and Australia impose standard GSP tariffs on imports from Bangladesh. As Bangladesh has been enjoying preferential tariffs under SAFTA, we also apply SAFTA non-LDC tariffs. We do not consider Korean and Chinese MFN tariffs as they give about 97 per cent tariff lines duty-free under APTA and DFQF. We also do not consider changes in USA tariffs in this simulation as the USA has suspended GSP imports from Bangladesh since 2013.

• Under scenario two, in addition to the tariff changes from the first scenario, we introduce the elimination of export subsidies to selected sectors including textiles and clothing, light manufacturing and agricultural sectors exporting from Bangladesh.

• Under scenario three, we investigate the impacts of only the EU imposing standard GSP tariffs on imports from Bangladesh as the EU is the largest export destination of Bangladesh. The EU standard GSP on readymade garments is 9.6 per cent (Europa, 2020).

• Under scenario four, in addition to the tariff changes from scenario 3, we also introduce an elimination of export subsidies to all these selected sectors exporting from Bangladesh.

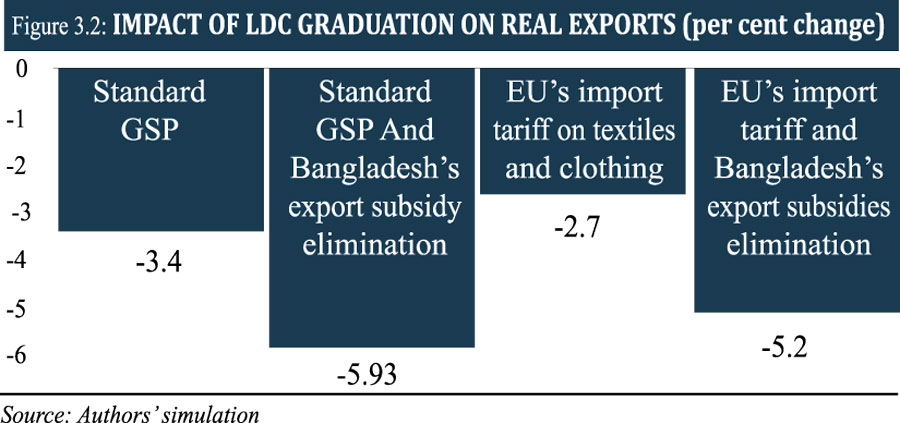

ANALYSIS OF THE SIMULATIONS RESULTS: Macroeconomic impact. The impact of introducing new tariffs and eliminating export subsidies can be investigated at both the macroeconomic and household levels of analysis. This section presents the simulation results that show the potential impacts on macroeconomic indicators, industry outputs, trade, and households' income and consumption. The overall macroeconomic impacts of the new standard GSP tariffs and elimination of export subsidies modelled are presented in Figure 2. It is evident from the simulations that the increased tariffs and elimination of export subsidies will reduce exports and imports substantially under all four scenarios. The simulation results show that if the EU, Japan, Canada, Australia introduce standard GSP tariffs (Table 3), GDP reduces by 0.28 per cent. If complete elimination of export subsidies also takes place for Bangladesh it may further negatively impact real GDP (0.38 percent), exports, imports and household income.

The analysis shows that shrinking exports from Bangladesh could lead to a negative balance of trade impact that could affect GDP. Total exports reduce by about 5.9 per cent under scenario two. This analysis indicates that Bangladesh will face a challenging situation after graduation with this new environment.

The analysis shows that shrinking exports from Bangladesh could lead to a negative balance of trade impact that could affect GDP. Total exports reduce by about 5.9 per cent under scenario two. This analysis indicates that Bangladesh will face a challenging situation after graduation with this new environment.

In contrast, if the EU only introduces their standard GSP  tariff importing from Bangladesh and at the same time if Bangladesh eliminates its export subsidies, real GDP may decrease by about 0.27 per cent. Bangladesh exports fall by 5.2 per cent in this scenario (Figure 4). The analysis indicates that the overall change in the balance of trade is negative and there is a significant negative impact on terms of trade.

tariff importing from Bangladesh and at the same time if Bangladesh eliminates its export subsidies, real GDP may decrease by about 0.27 per cent. Bangladesh exports fall by 5.2 per cent in this scenario (Figure 4). The analysis indicates that the overall change in the balance of trade is negative and there is a significant negative impact on terms of trade.

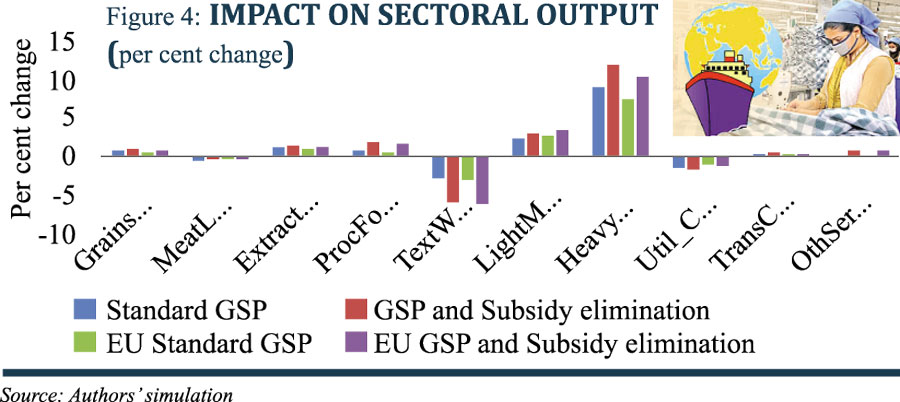

Sectoral output. The RMG industry has been enjoying not only duty-free market access, but also various stimulus supports, including cash incentives, duty drawbacks, and bonded warehouse facilities over the decades. If we eliminate the export subsidies and increase tariffs on exports to GSP tariffs when exporting to developed markets this will impact RMG production, as presented in Figure 4.

Under scenario two if we eliminate export subsidies and impose a 9.6 per cent tariff, the total production of textiles and clothing decline by about 6.1 per cent. But the tariff changes and subsidy eliminations may have a positive impact on the output of other sectors. The industrial sector will face lower tariffs (about 4.3 per cent) than the RMG sector (9.6 per cent) in the EU market, which may increase the output and export of the non-RMG sector. The other explanation is resource mobilisation, with resources moving away from the RMG sector to other industries, leading to higher production of non-RMG sectors. The light and heavy manufacturing sector would experience positive growth. Agricultural output may increase significantly as well, although, the contribution to exports by all these sectors is not very significant compared to the RMG sector. The analysis indicates that the removal of export subsidy may hurt the highly export-intensive apparel sector but will have a positive effect on the output of other sectors (Figure 5).

Under scenario two if we eliminate export subsidies and impose a 9.6 per cent tariff, the total production of textiles and clothing decline by about 6.1 per cent. But the tariff changes and subsidy eliminations may have a positive impact on the output of other sectors. The industrial sector will face lower tariffs (about 4.3 per cent) than the RMG sector (9.6 per cent) in the EU market, which may increase the output and export of the non-RMG sector. The other explanation is resource mobilisation, with resources moving away from the RMG sector to other industries, leading to higher production of non-RMG sectors. The light and heavy manufacturing sector would experience positive growth. Agricultural output may increase significantly as well, although, the contribution to exports by all these sectors is not very significant compared to the RMG sector. The analysis indicates that the removal of export subsidy may hurt the highly export-intensive apparel sector but will have a positive effect on the output of other sectors (Figure 5).

Impact on RMG sector. Textiles and clothing are the main export items of Bangladesh, constituting about 87 per cent of Bangladesh's total exports in 2019. Therefore, the RMG sector's exports could be affected adversely by post-LDC graduation under all four scenarios.  Exports of the ready-made garments sector could fall by 14 per cent under scenario two. However, due to overall increased efficiency through eliminating export subsidies, some of resources may move out from the RMG sector to other sectors which may increase exports of light engineering, processed foods, and the agricultural sector.

Exports of the ready-made garments sector could fall by 14 per cent under scenario two. However, due to overall increased efficiency through eliminating export subsidies, some of resources may move out from the RMG sector to other sectors which may increase exports of light engineering, processed foods, and the agricultural sector.

At the same time, imports might decrease substantially in all sectors under all four scenarios, especially intermediates inputs of the RMG sector, which constitutes about 20 per cent of Bangladesh's total imports. Elimination of export subsidies also reduces imports in the light manufacturing industry.

Impact on households. Given the MyGTAP modelling extension for Bangladesh developed in this paper, we are able to supplement the macroeconomic results with distributional analysis of household income. The estimated change in household income is shown in Figure 6. The simulation results reveal that real household income declines substantially for urban households under all four scenarios. The real income could decrease due to reduced income in the RMG sector, in particular, urban households are more linked with export-oriented industries than are rural households.

Our results suggest that income of urban households could decline on average by 3 per cent under scenario two due to a significant fall in RMG exports which will directly affect urban unskilled household income. Due to the elimination of export subsidies domestic prices may increase which lead to lower exports. However, rural household incomes may not fall significantly as their income is not so directly related to the export-oriented readymade garment industry.

Urban unskilled households contribute about 42 per cent to value added in the garment industry and are directly affected due to the lower exports that leads to lower output in the apparel sector. According to Haque and Bari (2021), about 4.2 million workers are employed in the apparel sector in Bangladesh. Table 5 shows the contribution of the apparel sector to GDP is about 7.16 per cent. This indicates that urban unskilled labour, about 4.2 million people, are particularly affected by the LDC graduation. The Bangladesh Garment Manufacturers and Exporters Association (BGMEA) indicates that women comprise 80 per cent of workers employed in member factories (World Bank, 2012). Rural households, whose main source of income is from agriculture and farming, are likely to be less affected than urban households as they are not so reliant on the RMG sector for their incomes.

Changes in household consumption under each scenario are presented in Figure 7 and show that consumption may fall by about 4 per cent in the urban area, but the reduction in rural consumption is much smaller. While consumption may decrease substantially among the urban employees who are directly employed in the garments industry, rural workers are more insulated from the impacts of the policy changes modelled.

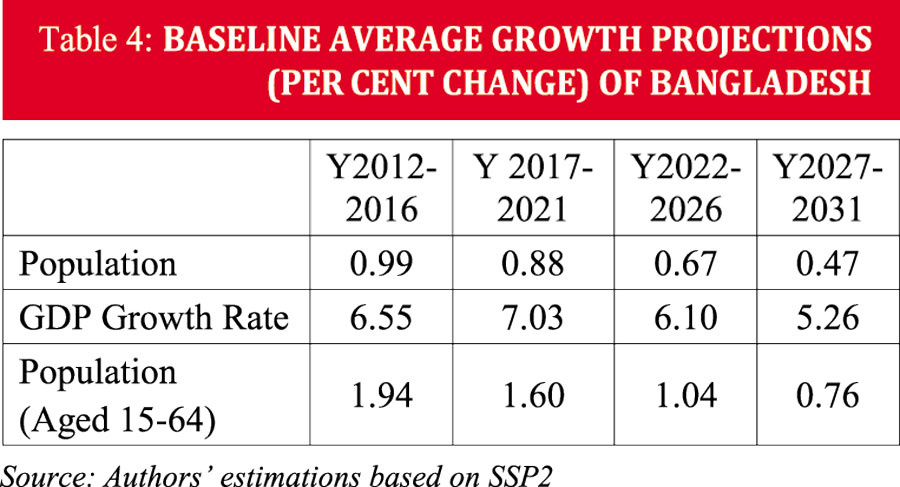

ROBUSTNESS AND SENSITIVITY ANALYSIS: Baseline Database for Long Term Impact Simulations. As Bangladesh is set to graduate from the LDC category by 2026, followed by another three years of transition grace period, we also simulate the impacts of the scenarios from a database that is projected to 2031. These simulations provide insight into how overall results may differ if modelled from a baseline that includes structural change in the Bangladesh and other world economies at the time the graduation will be implemented. [While useful for sensitivity analysis, given our focus in this study on household impacts which rely on data from the 2014 SAM for which projections into the future are not available, it would not be appropriate to draw detailed household insights from this updated dataset.] First, we develop a baseline projection of the global economy from 2014-2030. Starting with the GTAP version 10 dataset, with a base year of 2014, we exogenously apply growth to population, labour force, and GDP per capita growth to simulate changes in Bangladesh and the other global economies modelled over this period (following Anderson and Strutt, 2016). In particular, we use a middle of the road shared socio-economic pathways (SSP2) projection to estimate the growth rate projections shown in Table 8.

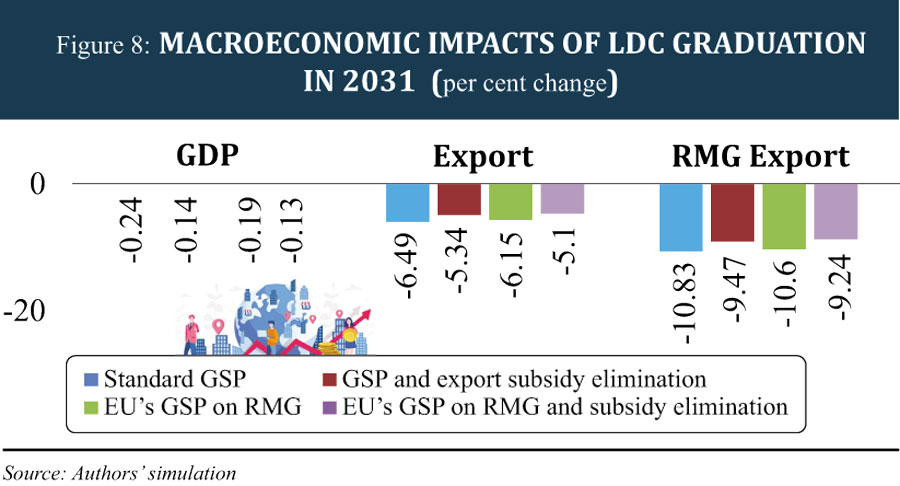

The macroeconomic impact of GSP tariff and elimination of export subsidies modelled from the updated 2031 baseline are presented in Figure 8. The simulations indicate a similar pattern of impact to the comparative static simulations. The results evince that Bangladesh economy will face challenges in export markets after graduation. The simulation results show that if the EU, Japan, Canada, Australia introduce standard GSP tariffs when importing from Bangladesh, real GDP could fall by 0.24 per cent and total exports may decline by about 6.5 per cent, while exports of the ready-made garments sector could fall by 10.8 per cent in 2031. However, the negative impact of LDC graduation could be lower in the long run due to increased resilience of the economy over the years.

Sensitivity of results to trade elasticities. As a check on the robustness of results, we undertake sensitivity analysis of some key parameters. Given our focus on the impact of increased tariffs and reduced export subsidies, we test the impact of assuming different trade elasticities in the modelling. In particular, we double the size of the substitution elasticity between Bangladesh and its trading partners for imported goods. The macroeconomic impact is shown in Appendix Figure A5. The quantitative results of the sensitivity analysis are similar to the main study. Real GDP falls and overall exports drop, particularly RMG exports. Consistent with other literature, we find that pattern of results is similar, but the magnitude of the results does change somewhat with changes in the values of parameters (Timilsina, et al., 2018).

Sensitivity of results to trade elasticities. As a check on the robustness of results, we undertake sensitivity analysis of some key parameters. Given our focus on the impact of increased tariffs and reduced export subsidies, we test the impact of assuming different trade elasticities in the modelling. In particular, we double the size of the substitution elasticity between Bangladesh and its trading partners for imported goods. The macroeconomic impact is shown in Appendix Figure A5. The quantitative results of the sensitivity analysis are similar to the main study. Real GDP falls and overall exports drop, particularly RMG exports. Consistent with other literature, we find that pattern of results is similar, but the magnitude of the results does change somewhat with changes in the values of parameters (Timilsina, et al., 2018).

Limitations of the Analysis. The economic impacts estimated by CGE models depend on many assumptions including with respect to parameters, data, model specifications and closures. For example, our model assumes perfect competition in all sectors. In the model closure we use, capital and labour are assumed to be fully mobile between sectors, whereas land is treated as moving sluggishly between sectors and government spending is assumed as a constant share of government income. Gilbert et al., (2018) provides a useful review of some strengths and limitations of CGE models for international trade policy analysis.

While our modelling captures bilateral trade flows between Bangladesh and other countries, the CGE model and database we use in this study do not focus on global supply chains, production processes that may shift rapidly between different locations or trade in unfinished goods relative to finished goods. Some limitations of global CGE models which do not fully capture global supply chains are discussed by Athukorala et al. (2018).

In the current study, we only consider the market access issue of LDC graduation, where we model standard GSP-related tariffs and export subsidies elimination scenarios. We do not consider rules of origin, trade-related intellectual property rights, development assistance, or any other issues Bangladesh may face after graduation. In addition, we do not model the potential benefits through increased investment that may occur on graduation, or the impact of future trade agreements, both of which may help offset any negative impacts.

CONCLUSION AND POLICY RECOMMENDATIONS: Graduation from the LDC category may give more self-dignity and some economic benefits through improved credit rating and attract more investment, but at the same time countries will lose preferential market access. Given the impending graduation, Bangladesh needs to have a smooth graduation transition strategy in place so that potential disruptions from the graduation are minimised and its long-term goals are realised.

Bangladesh has been enjoying preferential market access as an LDC in recent decades. The EU, UK, Canada, Japan, Australia and other developed countries offer mostly duty-free market access importing from LDCs like Bangladesh. The GSP utilisation rate of Bangladesh in the EU market is 96 per cent, indicating that Bangladesh has substantially benefitted from duty-free market access. Although MFN-applied tariffs on many industrial goods are relatively low in developed markets, the standard GSP rates for the textiles and clothing sector are relatively high in most developed countries (WTO, 2020), and these are the rates Bangladesh will face when exporting to these markets after graduation. Export subsidies are another critical policy issue. Bangladesh had been providing export subsidies of about US$10 billion in 2018, which accounted for about 3.7 per cent of its GDP or about 57 per cent of its development budget. Bangladesh's main export item is ready-made garments; therefore, most of this export subsidy goes to RMG sector. As Bangladesh is preparing to graduate from LDC to the DC status by 2026, export subsidies, including for industrial products, must be eliminated after graduation.

This study analysed the potential impact of LDC graduation using a computable general equilibrium framework incorporating household data from Bangladesh's social accounting matrix. In particular, we used the MyGTAP programme and model developed by Walmsley & Minor (2013) to incorporate country-specific data to investigate the impacts of different domestic policies at the household level. We then simulate four different policy scenarios to evaluate the potential impact of LDC graduation on Bangladesh, starting with imposing the standard GSP tariffs that Bangladesh will face in general as a developing country. We then added a complete elimination of the export subsidies. Under scenarios three and four, we introduced the EU's tariff imposition, without and with subsidy elimination.

The findings show that if developed countries (except the USA) impose tariffs when importing from Bangladesh and at the same time if Bangladesh eliminates its export subsidies, Bangladesh's GDP may fall by 0.38 per cent, and exports could fall by six per cent. The RMG sector could be affected severely, with exports of the RMG sector declining by 14 per cent. The analysis also indicates that the income of urban households could decline on average by three per cent. Real household income may decline substantially for urban households, particularly due to reduced income in the RMG sector and urban household consumption may fall by about four per cent.

The simulations also indicate that if the European Union (EU) only imposes standard GSP tariffs while importing from Bangladesh and if Bangladesh eliminates its export subsidies, Bangladesh's real GDP may fall by about 0.24 per cent. Bangladesh's total exports could fall by about 5.2 per cent, while exports of the apparel sector decline by about 7.2 per cent. Urban household incomes may decrease due to a significant reduction in RMG exports and production.

Graduation will bring some challenges, especially after phasing out of the transition period. Bangladesh has set a target to become an upper-middle-income country by 2031 and an aspiration to be a developed nation by 2041 (Perspectives Plan 2021-2041, Bangladesh Planning Commission). To achieve this ambitious goal, Bangladesh needs a graduation transition strategy to ensure that graduation does not cause disruptions in this long development journey. The economy has undergone substantial structural changes over the years. The share of agriculture in GDP declined from 17 per cent in 2010 to 13 per cent in 2020 (WDI, 2020), with the shares of industry and service sectors increasing steadily. While the economy is growing, an important challenge is the lack of export diversification, both in products and markets. In addition, the current COVID-19 pandemic has significantly impaired overseas employment, which may substantially impact the current account balance. The pandemic has also affected people's health, livelihoods, and employment, especially in the vast informal sector. Low productivity, the informal labour market, workplace safety issues, controlling disease outbreaks, and dealing with environmental disasters are critical issues the country needs to tackle to ensure sustained economic growth.

Our study indicates that if Bangladesh is unable to ensure continuity of market access, the costs of LDC graduation may be high. Bangladesh will face severe competition in export markets with economies such as Vietnam, India, Indonesia and China after graduation. Bangladesh should prepare a comprehensive transition strategy to make sure its export market access in the developed market can cope with the post-graduation environment. Bangladesh should try to ensure continued access to the EU market, a key export market. The GSP plus could be an option to ensure market access in the EU. Different preferential or free trade agreements with East Asian countries will also play a key role in integrating Bangladesh into the East Asian supply chain. The FTA strategy should be integrated into the national policy agenda, especially in the Five-Year Plan and the long-term Perspective Plan. Moreover, Bangladesh needs to play an active role in the WTO and UN LDC conference to make sure market access continues after graduation.

Dr Mohammad Masudur Rahman is with Institute of South Asian Studies (ISAS), National University of Singapore (NUS), Singapore; & School of Accounting, Finance and Economics (SAFE), University of Waikato, Hamilton, New Zealand. masudbfti@gmail.com

Anna Strutt is with School of Accounting, Finance and Economics (SAFE), University of Waikato, Hamilton, New Zealand

The article is a slightly-abridged version of the authors' paper on 'Costs of LDC graduation on market access: evidence from emerging Bangladesh' originally published in Economic Systems Research. www.doi.org/10.1080/09535314.2022.2138271

© 2026 - All Rights with The Financial Express