Md Arifur Rahman, FHM Humayan Kabir, Md Rafiqul Islam and SM Salahuddin | November 23, 2022 00:00:00

A bird’s eye view of the Inland Container Depot (ICD) at Kamalapur in Dhaka

A bird’s eye view of the Inland Container Depot (ICD) at Kamalapur in Dhaka ![]() Bangladesh is a development surprise to many global economic researchers and policy makers. In the last 50 years after the independence from Pakistan in 1971, Bangladesh has steadily accelerated its economic growth which helps achieve its human development and reduce colossal rate of poverty. During its golden jubilee of independence in 2021, many renowned media outlets from the US, the UK and other parts of the world lauded the success stories of Bangladesh's economic development. The surprising economic advancement is still a puzzle to many of the economists who continue their research to unearth the factors behind such astonishing accomplishments.

Bangladesh is a development surprise to many global economic researchers and policy makers. In the last 50 years after the independence from Pakistan in 1971, Bangladesh has steadily accelerated its economic growth which helps achieve its human development and reduce colossal rate of poverty. During its golden jubilee of independence in 2021, many renowned media outlets from the US, the UK and other parts of the world lauded the success stories of Bangladesh's economic development. The surprising economic advancement is still a puzzle to many of the economists who continue their research to unearth the factors behind such astonishing accomplishments.

A war-ravaged economy in 1971, once infamously labelled as an international basket case, has made a slow start but has steadily outperformed its South Asian neighbours on the economic and social fronts. Nobel laureate economist Amartya Sen in his write-up pointed out that when Bangladesh's per capita GDP was a half of that in India in 2007, the former's social indicators such as gender equity, women's empowerment, mortality rate, life expectancy, immunization, etc. were remarkably better than the latter's. A decade later in 2016, Bangladesh overtakes Pakistan in terms of per capita GDP. In 2019, Bangladesh's GDP becomes larger than that of Pakistan. In the same year, every Bangladeshi citizen becomes richer than Indian citizen in terms of per capita GDP. In the Human Development Index (HDI), Bangladesh beat India for the first time in 2020. Bangladesh's persisting economic and social performances over the decades are complemented further by the events unfolded in the end of 2010s.

Many of the experts perceive that Bangladesh is following the East Asian development model of export-led growth which helps it accelerate economic growth particularly in the recent past decade in 2010s. There are a number of researches that have found strong positive relationship between export and GDP growth in Bangladesh. However, there are some other studies where it has failed to establish the above relationships. Amid the perplexing arguments, experts, civil society, think-tanks and development partners including the World Bank, the Asian Development Bank (ADB) are prescribing policy suggestions in the hope that Bangladesh eventually can harvest the outcome of its export-led growth (ELG).

According to Bangladesh Bank data, export receipts doubled in 10 years from US$20.31 billion in FY2010-11 to US$ 40.11 billion in FY2021. During the same period, the GDP of Bangladesh grew 1.9 times in constant 2015 US dollar rate and 3.2 times in current US dollar terms, the World Bank data showed. A wide-eyed observation leads to the conclusion that Bangladesh's phenomenal GDP growth in the decade of 2010s is driven by its export during the period. Since, this observation is a key postulate of the export-led growth hypothesis (ELGH), it seems that the ELGH has been applicable to Bangladesh's economic growth. However, the ELGH advocates that if a nation wants to become an export-led economy, it needs to open up its market to the international trade. In simple terms, the ELGH is determined by two characteristics: firstly, the export will be the main contributor to the growth and secondly, tariff and trade will have to be liberalised.

In the latest Export Policy 2021-2024, the government claims that the Ministry of Commerce is pursuing an export-led growth (ELG) strategy. The main objectives of the strategy are: create massive employment accelerating export, make sure foreign trade (export and import) is judiciously balanced, and facilitate economic development. An open-eyed analysis may discover that the massive employment generation is only possible through export-led industrialisation (ELI). In FY2021, Bangladesh's export receipts from services sector were less than 20 per cent and from the agriculture sector nearly 3.0 per cent. The data proved that Bangladesh's export was heavily dependent on the industrial sector which mainly comes from the manufacturing sub-sector. So, growth in export has, therefore, necessitates growth in industrialisation. Since the country's manufacturing sector is contributing to the overall export earnings a lot, the government would try to achieve its second objective of judiciously balanced export-import trade. Here, the government may not pursue aggressive trade liberalisation policy within a shorter period.

Dr M.A. Razzaque, an applied trade and development expert from the Policy Research Institute of Bangladesh (PRI) at an interview with media recently said that Bangladesh neither persuaded the export-led growth paradigm in the past nor in the current period. However, Centre for Policy Dialogue (CPD) Executive Director Dr Fahmida Khatun opined that Bangladesh experienced a remarkable growth in ELI. The ELI strategy is often synonymously used for ELG strategy, especially by the government in its export policy as both of them imply strategies opposite to import substitution. However, the subtle difference between ELI and ELG could be an interesting discourse especially when the government claims to pursue an ELG strategy while the think tanks assert the opposite.

Nonetheless, unpredictability, impulsiveness and instability of exchange rates pose severe threats to the ELG strategy. Overseas demand which is uncontrollable for any country is another key factor determining the volume of export. In addition, some countries often intend to compete with their trading partners by devaluating own currencies to gain comparative advantages.

In view of the above challenges, it is not clear yet whether the government is pursuing an ELG strategy in a correct way, or whether it is implementing its own version of ELG. Amid the debate, we have tried to analyse economic data collected from the World Bank, the Bangladesh Bureau of Statistics (BBS), the Bangladesh Bank and from other sources. Without applying any economic model or econometric analysis to find the statistical significance of the coefficients, our approach is more descriptive here than an inferential one. We have opted for beginning a discourse on the GDP equation. According to the equation, the GDP is the sum of total consumption, investment, government spending and net export (i.e. exports minus imports). These four components of GDP and the dynamics of their shares are analysed here. We have tried to show empirical data of several decades of Bangladesh's GDP and of some other competing economies in the South and Southeast Asian region in a bid to decide on whether Bangladesh is following an ELG strategy or it is far away from adopting the strategy.

The first argument will be the trade liberalisation, marked by a stalemate in the tariff structure. According to economist Dr Zaidi Sattar, the average nominal tariff rate sharply declined in the 1990s. However, in the first two decades of 21st century, the average nominal tariff had not declined any more rather ascended to some extent. Some trade economists argue that tariffs on import substitute production are the indirect subsidies and it undermines the support to the export which creates an anti-export bias. So, the success of export-led growth is dependent on the opening up of the country's economy and Bangladesh should continue pursuing trade liberalisation policy at such a pace as pursued in the 1990s. On the other hand, a study conducted by economists Dr Selim Raihan of SANEM in 2008 showed that the pace of rapid liberalisation in the 1990s demanded a very careful approach for further trade liberalisation in the country. The study also showed that although international financial institutions such as the World Bank and the IMF were consistently pursuing for trade liberalisation in Bangladesh, conducive to achieving high economic growth and alleviating poverty, some local economists do not endorse it. The trade liberalization, being a contentious debate in the country, the government is watchful about taking steps further.

The first argument will be the trade liberalisation, marked by a stalemate in the tariff structure. According to economist Dr Zaidi Sattar, the average nominal tariff rate sharply declined in the 1990s. However, in the first two decades of 21st century, the average nominal tariff had not declined any more rather ascended to some extent. Some trade economists argue that tariffs on import substitute production are the indirect subsidies and it undermines the support to the export which creates an anti-export bias. So, the success of export-led growth is dependent on the opening up of the country's economy and Bangladesh should continue pursuing trade liberalisation policy at such a pace as pursued in the 1990s. On the other hand, a study conducted by economists Dr Selim Raihan of SANEM in 2008 showed that the pace of rapid liberalisation in the 1990s demanded a very careful approach for further trade liberalisation in the country. The study also showed that although international financial institutions such as the World Bank and the IMF were consistently pursuing for trade liberalisation in Bangladesh, conducive to achieving high economic growth and alleviating poverty, some local economists do not endorse it. The trade liberalization, being a contentious debate in the country, the government is watchful about taking steps further.

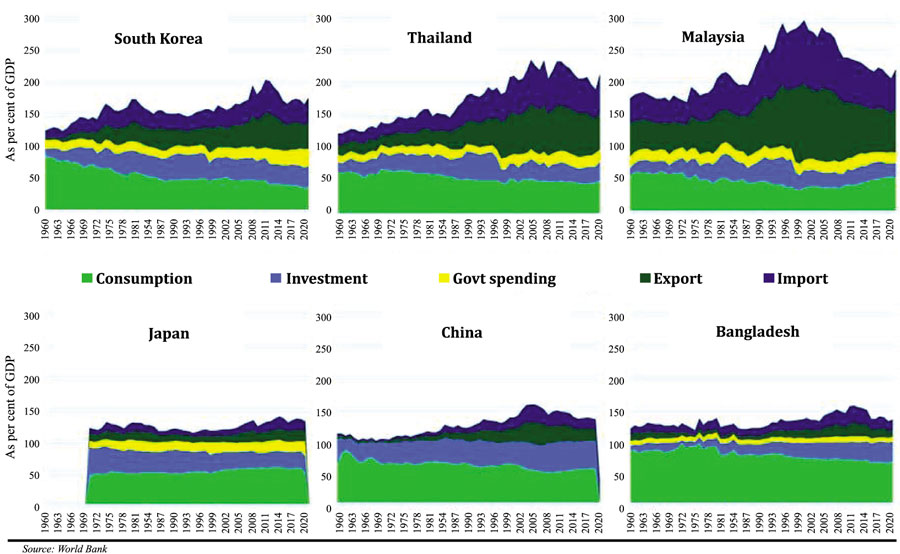

The second argument of the ELG strategy is that export is the main driver of economic growth. To analyze this argument, we used the GDP data and compared Bangladesh's economy to its comparator countries. Since there were remarkable economic growth experienced in East Asia during 1960s, 1970s, and 1980s, we took Japan, South Korea, Singapore, Taiwan and Hong Kong, and China as our samples. Almost the similar kind of development model was followed by other Southeast Asian nations in 1980s, 1990s and 2000s. We selected Malaysia and Thailand from Southeast Asia. The East and Southeast Asian nations are said to be benefited from the ELG strategy in the close regional proximity to Bangladesh.

Using the World Bank data, we have tried to measure the components of GDP here in percentage of GDP to make those comparable with each other. Actually, the consumption, investment, export and import data for the selected countries are available since 1960 except Japan. But the statistics of all the variables in all the sample countries are available since 1970. The government spending data are partially available for most of those countries except China and Hong Kong. When there was unavailable data for any particular year or years, the missing values of government spending are replaced by three year moving averages back and forth. We have deducted the government consumption data from the overall consumption in the selected countries in our GDP calculation.

According to the statistical analysis, we have found the ELG in South Korea, Singapore, Taiwan, Hong Kong, Malaysia, Indonesia, Thailand and some other countries in the region. The international trade of those countries was the main driver of their macro-economy.

In South Korea, the international trade accounts for 75 to 100 per cent of its GDP. In case of Thailand in 2000s, the international trade accounts for 150 per cent of its GDP. Malaysia is ahead of both South Korea and Thailand. In the 1990s and 2000s, Malaysia's international trade was 200 per cent of its GDP. We had not reflected here the graph and data of Singapore and Hong Kong, since it makes the figure incomparable to other economies. The international trades of Singapore and Hong Kong are about five times higher than their respective GDPs. Moreover, all of these countries maintain a healthy balance of trade in favour of their economies.

In terms of international trade, comparatively a modest performance is showcased by China and Japan. However, China's economy is so massive that, being the leading exporter of the world, its export to GDP ratio is modest. Similarly, Japan is a large economy and its export is also massive in volume.

Meanwhile, Bangladesh's international trade volume compared to its GDP also displayed a similar performance. In case of these three countries (China, Japan and Bangladesh), the international trade remains less than 50 per cent of their GDP. The international trade's share of global GDP is gradually increasing which reached 60 per cent at the end of 2000s. In the case of Bangladesh, the country has a big opportunity to upgrade its export for catching up with fellow Southeast Asian counterparts aimed at pursuing the ELG strategy effectively. More importantly, though the volume of international trades of China and Japan are not gigantic enough compared to other East and Southeast Asian nations, they have successfully maintained a favourable trade balance for a very long period of time. On the other hand, Bangladesh has been on a negative trajectory for long. To achieve an export-led growth, Bangladesh can and should closely watch the economic policies pursued by Malaysia, South Korea and Thailand. The level of development in Thailand and Malaysia can be targeted in the medium-term and the level of South Korea in the longer-term.

Currently, most of the economists work in isolation without collaboration or coordination with the experts from other sectors segments in society like politics, sociology. Economic models are elaborated with minimal attention to the institutional framework. Policy choices should not be chosen as exogenous, rather efforts should be made to understand why the policies are adopted and in which circumstances.

Malaysia: Since the late nineteenth century, Malaysia has been a major supplier of primary products like tin, rubber, palm oil, timber, oil, liquefied natural gas, etc. to the industrialised nations. Rubber and tin accounted for more than two-thirds of its export basket until the 1960s. From 1970s, the export-oriented manufacturing industries such as textiles, electrical and electronic goods, rubber products, etc. played a vital role in its development. The Malaysian government introduced an attractive incentive for foreign investment in the 1980s. As a result, its manufactured goods accounted for more than 70 per cent of total exports in the 1990s.

Thailand: From 1960s, Thailand's economy had been showing a steady growth absorbing oil supply shocks in the 1970s. A new acceleration in GDP growth was observed during the 1980s which rose highest to 13.2 per cent in 1988. In the first (1961-66) and second (1967-71) National Economic Development Plans, Thailand focused on an import substitution industrialisation (ISI) policy. But in its 3rd National Economic Development Plan (1972-76), a policy reorientation was observed where the country opted for promotion of export-oriented and labour-intensive industries along with the import substitution mechanism. Its policies were shifted further in the 5th and 6th National Economic and Social Development Plans (1982-86, 1987-91), where a greater emphasis was laid on international competitiveness and industrial restructuring, without emphasizing any particular sector. Once in 1960s, about 86 per cent of Thailand's export income came from the agriculture sector which fell to 18 per cent in 1990s. On the other hand, the share of manufactured goods in the export income swelled to 81 per cent.

South Korea: There was no formal trade policy before 1960 in South Korea. In its first five-year plan (1962-66), Korea embarked on a path of export-oriented industrialisation with a protectionist economic policy. To promote development, a policy of export-oriented industrialisation was applied, closing the entry of all kinds of foreign products, except raw materials into the country. The strategy promoted economic growth through the labour-intensive export-oriented manufacturing industries aimed at attaining a competitive advantage. In the early 1970s, the third five-year plan (1972-76) focused on heavy and chemical industries. Hence the new growth engine shifted from light manufacturing to heavy manufacturing industries. Meanwhile, Korea continued its export promotion and import restriction policies. An important transformation occurred in Korea's trade policy in its sixth five-year plan (1987-91). In this policy, the East Asian nation started to produce export-oriented consumer products, including electronics and high tech in a shift from its heavy industrial production model. Foreign investment policies were relaxed in response to a decrease in domestic investments. The cross-border capital movement increased significantly. Restrictions on imports were removed, but a variety of non-tariff barriers were dominating the foreign trade.

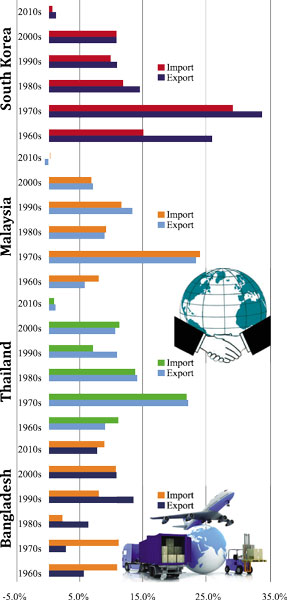

Bangladesh: Bangladesh's economy is mainly consumption-driven, though the share of investment (or capital formation) increased substantially in 2010s. In 2019, gross capital formation (or investment) was 32 per cent of GDP. The contribution of investment to the country's GDP growth is gradually increasing while the contribution of export to GDP remains very poor. So, it could be assumed that the driver of rapid economic growth of Bangladesh in 2010s was the investment, not the export. Actually, Bangladesh is in the very early stage of export-led growth. In this stage, it is very difficult to conclude that the export is the main driver of economic growth here. Moreover, a severe challenge is posed by the declining share of export and import in respect to GDP since the beginning of the year 2011. The declining trend in export's contribution to GDP is not only the case for Bangladesh, also for others too. International trade has started losing its contribution to GDP after the recession in 2009. The share of international trade is declining globally. Given the scenario, increasing the contribution of export to GDP is a real challenge for Bangladesh. Whereas, export-led growth can only be achieved by increasing growth of exports and exports' contribution to GDP. In the 1960s, South Korea's export grew at a compounded annual rate of 25 per cent which further increase to 33 per cent throughout the 1970s. Malaysia and Thailand enjoyed such high growth rates in 1970s when Malaysia's export grew at a compounded annual rate of 23.1 per cent and Thailand's export at 22.0 per cent. Bangladesh never noticed such a golden decade. The highest export growth was recorded in the 1990s when the average annual rate was 13.4 per cent and in 2000s it was 10.9 per cent. However, in the 2010s, the export growth rate stabilized to an average annual rate of 7.8 per cent.

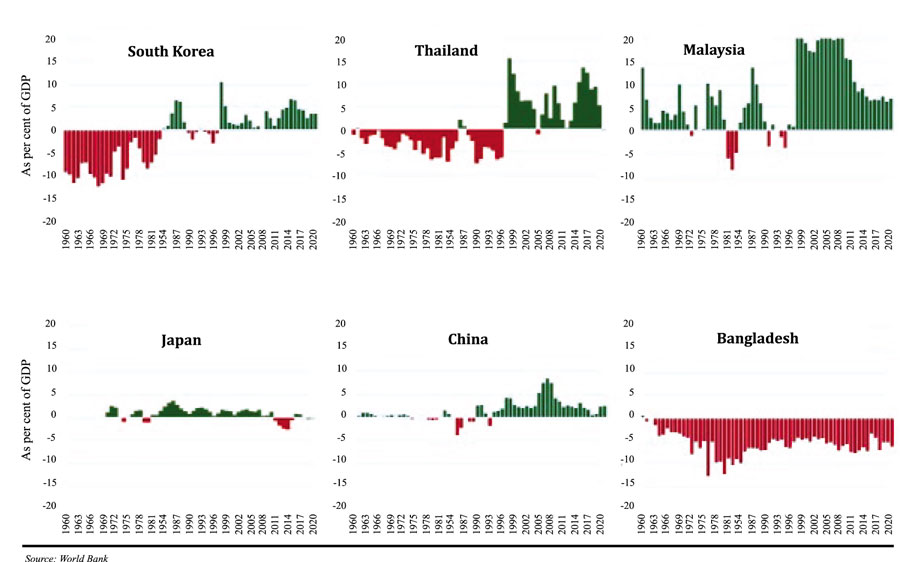

In addition, a balance between export and import is also very crucial for the country. Bangladesh is maintaining an unfavourable trade balance for decades. A persisting unfavourable trade balance is also seen in the cases of Thailand and South Korea. That means maintaining an unfavourable trade balance is not an obstacle to achieving export-led growth. Having said that, an unfavourable trade balance implies a negative net-export and inversely affects the GDP. Both South Korea and Thailand moved to a favourable trade balance after 1999. It is not problematic to find out that both the countries were severely affected by the East Asian financial crisis in 1997. The unfavourable trade balance jeopardised their crisis further. As Bangladesh is pursuing or wants to pursue an ELG strategy, it is gradually being exposed at an incremental rate to the risk of international trade. Even due to the Russia-Ukraine war following the COVID-19 pandemic, Bangladesh's depleting foreign exchange reserve has been creating enormous strains. On that account, finding out an effective policy intervention for maintaining a favourable trade balance is crucial.

After the East Asian financial crisis in 1997, both the economies of South Korea and Thailand did not take long to rebound, thanks to the adequate inflow of foreign direct investment (FDI). Due to an effective foreign investment policy, the cross-border capital movement increased significantly. Not

After the East Asian financial crisis in 1997, both the economies of South Korea and Thailand did not take long to rebound, thanks to the adequate inflow of foreign direct investment (FDI). Due to an effective foreign investment policy, the cross-border capital movement increased significantly. Not  only in South Korea and Thailand, all the countries in East Asia were able to attract FDI successfully. The inflow of FDI has a direct and favourable impact on enhancing export. Within three decades, the rank in China's global exports rose from 32nd in 1978 to 1st in 2009. During this period, China was one of the world's top recipients of FDI. Export competitiveness depends on the level of foreign technology and knowledge assets that can lead to deepening the level of product sophistication and market diversification. The level of FDI inward stock in each sector is related to the export capacity of each sector.

only in South Korea and Thailand, all the countries in East Asia were able to attract FDI successfully. The inflow of FDI has a direct and favourable impact on enhancing export. Within three decades, the rank in China's global exports rose from 32nd in 1978 to 1st in 2009. During this period, China was one of the world's top recipients of FDI. Export competitiveness depends on the level of foreign technology and knowledge assets that can lead to deepening the level of product sophistication and market diversification. The level of FDI inward stock in each sector is related to the export capacity of each sector.

Based on the above analysis it can be said that an effective ELG strategy for Bangladesh means: (1) substantially increase the share of export as percentage of GDP, (2) maintain a favourable trade balance, (3) pursue an effective policy to attract more FDI, and (4) deepen the level of product sophistication and market diversification. If it comes to quantifying the target so that the effects of policy interventions can be measured in terms of predefined milestones, the following arguments and narratives may be found helpful to the policymakers.

The volume of export should be increased at such a pace that the volume of international trade can exceed 60 per cent of GDP which is currently around 40 per cent. Since Bangladesh's economy is growing at a nominal rate of around 12 to 15 per cent, export growth should be at least 15 per cent or more to reach the desired level of export to GDP ratio. Secondly, a favourable balance of trade should be maintained. The export policy of the government also intends to judiciously balance export and import. The goods exports are highly dependent on imported raw materials. In addition to that, capital machinery for the manufactured exports is also imported from overseas market. Therefore, import of luxury goods should be discouraged, though the import substitution policy creates an anti-export bias. South Korea, Malaysia and Thailand have successfully pursued a blended policy of export-oriented industrialisation and import substitution during their high growth regimes. Chinese economy is also maintaining such a policy blend. Bangladesh can also maintain such a policy blend for some years. It also requires a deadline for moving away from an unfavourable trade balance. The existing export-import gap should be reduced by 30 per cent every year.

To induce FDI, only attractive incentives for foreign investors are not enough. Adequate infrastructure such as: sufficient close-by transport facilities (airport, ports), adequate and reliable supply of energy, provision of an adequately skilled workforce, facilities for the vocational training of specialised workers, etc. are very important. Since 2015, the net FDI inflow to Bangladesh has been decreasing, therefore it's share as percentage of GDP is declining faster. The FDI should be raised up to 5.0 per cent of GDP.

To induce FDI, only attractive incentives for foreign investors are not enough. Adequate infrastructure such as: sufficient close-by transport facilities (airport, ports), adequate and reliable supply of energy, provision of an adequately skilled workforce, facilities for the vocational training of specialised workers, etc. are very important. Since 2015, the net FDI inflow to Bangladesh has been decreasing, therefore it's share as percentage of GDP is declining faster. The FDI should be raised up to 5.0 per cent of GDP.

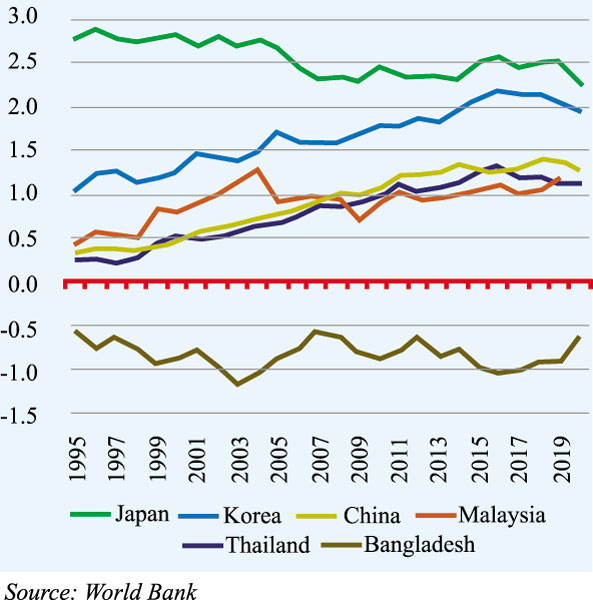

Last but not least, Bangladesh needs to deepen and diversify its export markets and its export products to a high end sophistication level. Export competitiveness depends on the level of foreign technology and foreign investments with high-end technologies. However, research and development should also be emphasized locally with special support from the government. A quantifiable yardstick for export product sophistication is the Economic Complexity Index (ECI), in which Bangladesh is consistently performing very poorly.

Bangladesh's performance is not comparable to any of the countries we have discussed above. Japan leads the world in ECI which implies that this country produces most sophisticated products in the world. South Korea is also one of the leading countries in ECI. China, Malaysia and Thailand have also developed by a huge margin. Bangladesh's ECI is hovering in the negative territory which implies the country can only manage to produce simplified manufacturing goods. The ECI should be targeted to be brought in to the positive territory.

Setting aside the debate, now we need to think whether Bangladesh is pursuing an ELG strategy or not. In the conclusion, it can be said that Bangladesh is in an early stage of ELG regime. As Bangladeshi economists have observed, ELI was rapidly taking place in Bangladesh especially during 2010s, but investment is becoming more dominant and contributing substantially to the economic growth of the country. A similar investment growth was found in case of South Korea, Thailand and Malaysia until the economies were hit by the Asian financial crisis. China however maintains a continuous growth in investment and becomes an investment-driven economy.

Bangladesh, in the beginning of 2020s, is an economy driven by investment and consumption, though consumption's contribution to growth is diminishing. The success of prudent policy formulation and their effective implementation will help ascertain whether export can be the main growth engine for Bangladesh's economy. For obvious reasons, the success is dependent on a number of controllable and uncontrollable issues including domestic political stability, global geopolitics, commodity price, foreign exchange volatility, declining international trade and many other factors. Despite the challenges, we expect to see exports grow at a rate of 15 to 20 per cent in the 2020s and become the main engine of growth.

Dr Md Arifur Rahman, FHM Humayan Kabir, Md Rafiqul Islam and SM Salahuddin are the honorary fellows of the Knowledge to Wisdom (K2W) Communications and Research, a local think-tank

© 2026 - All Rights with The Financial Express