![]() Humans are not always rational, and the decisions they make are often imperfect. When it comes to personal finance, people have self-control limitations and are easily influenced by assumptions, emotions, and perceptions. These biased and irrational behaviours seldom go without costs.

Humans are not always rational, and the decisions they make are often imperfect. When it comes to personal finance, people have self-control limitations and are easily influenced by assumptions, emotions, and perceptions. These biased and irrational behaviours seldom go without costs.

Financial behaviour is the personal management of financial situations such as savings, investments, money, and credit. It is the capability to understand the impact of financial decisions on one's circumstances and whether the person makes the right choices.

Getting wealthy and financially independent requires a great deal of patience

Most people don't want to get wealthy slowly. Rather, they want the fast track of winning a lottery or picking a hot stock. They don't see how saving a mere 5,000 Taka per month matters, so they don't bother saving anything at all.

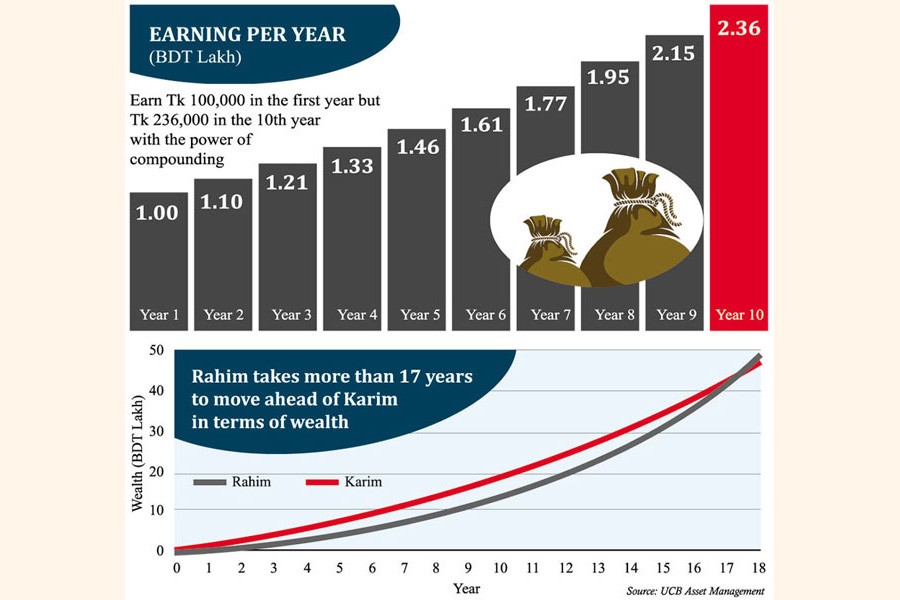

When a person invests, s/he needs to be patient. An investment is unlikely to reap significant benefits overnight. If we look at the most successful investors in the world, we can see that they have remained patient in different market cycles. It is not "timing the market", but "time in the market", which has been proven true over the years. Those who stay invested over a long time generally do better than those who try to profit from turning points in the market. Besides, the longer a person remains invested, the more the effect of compounding. For instance, if someone invests 10 Lac Taka today and generates a 10% return every year, s/he will earn only 1 Lac Taka in the 1st year but will earn 2.36 Lac Taka in the 10th year. This magic will only work if the person is patient enough to keep the money invested for a long period.

The amount saved is more important than the rate of return

Warren Buffet, arguably the greatest investor of all time, said:

"Successful investing takes time, discipline, and patience."

While the rate of return on investment is often not under the control of investors, the investment amount is. Consider two investors - Rahim invests 5,000 Taka per month and Karim invests 10,000 Taka per month. Rahim generates a rate of return of 15% per year, while Karim generates 8%. Since Karim sets aside a higher amount every month, the base of his wealth grows faster in the initial years. To put it simply, it takes more than 17 years for Rahim to move ahead of Karim in terms of accumulated wealth. This happens even though Rahim generates twice the rate of return than Karim does. The real impact of returns is felt only when the portfolio has crossed a reasonable size. Till then, it is more about the amount saved or invested. Also, having decent savings can give the person financial independence and help him turbo-charge his future aspirations.

Behavioural biases can lead to making poor investment decisions

Behavioural biases can influence a person's judgment about how he spends his money and invests. Understanding these biases can help overcome them and make better financial decisions.

A common bias is mental accounting, which means people treat money differently depending on where it came from and what they think it should be used for. For example, most people are inclined to spend the money earned from unexpected sources (like a lottery, inheritance, etc.) on luxury items but would save that same money if they had earned it. Another example can be the tendency to hold the piece of family land no matter what its opportunity cost is. Many families consider their ancestral land as something that should not be sold even if they are debt-ridden.

Another bias is herd behaviour when investors follow and copy others rather than making their own decisions based on information and facts. People follow the herd because it feels safer, and also because of a fear of missing out. Herd behaviour can create bubbles like the 2010 stock market bubble in Bangladesh. Investors got severely hurt when that bubble burst.

Overconfidence is another behavioural bias which means the tendency to see oneself as better than one really is. This can lead to poor investment decisions. For example, overconfidence in investing skills can lead someone to believe they can accurately time the market cycles and price movements every time.

Perhaps one of the most common behavioural biases is loss aversion. A loss is perceived by people as psychologically or emotionally more severe than an equivalent gain. For example, the pain of losing 10 lac taka is often far greater than the joy gained in gaining the same amount. However, this behaviour somewhat depends on a person's risk appetite - which we discuss next.

The ability to take risks is very different from the willingness to take risks

Some people are willing to take financial risks but might not have the ability to do so. On the other hand, some may have a high financial ability to take risks, but due to their preference to be risk averse, they are not willing to take high risks.

The ability to take risks can be quantified through an investor's net worth, age, inherited wealth, and future earning potential. For example, an investor who is in his late 20s with a stable earnings stream is able to invest more in risky assets like stocks. However, an investor who is 50+ and closer to retirement may want to allocate a higher proportion of his investment to fixed-income vehicles such as Shonchoypotro and FDR.

On the other hand, the willingness to take risks refers to the degree of investment risk one is comfortable taking. In the end, it all comes down to how a person will react when his/her investment portfolio loses its value. The willingness to take risks depends on an investor's personality type, past experience with investing, and resilience.

Many of the financial behavioural biases are imprinted into the way people process, think, and feel. Still, there's more good than harm in addressing these behaviours. An effective way to face these biases can be by establishing logical decision-making processes related to one's finances. It is always better to have a long-term financial plan that suits an individual's specific goals. A long-term financial plan may include building an emergency fund, paying down debt, getting life insurance, and most importantly, saving enough money to retire. Proper retirement planning considers i) how much time is left until retirement and ii) how much the expenses during retirement will be. If these two points can be determined, it is easy to find out how much needs to be invested every month. A retirement calculator that considers the return generated on investment, the rate of inflation, and life expectancy can be quite helpful. However, If these nitty-gritty calculations seem complicated, some rules of thumb can be followed instead. For example, by the age of 30, it is ideal to have a savings balance equivalent to one's annual income. Going forward, the savings balance should ideally be 3x (at the age of 40), 6x (at the age of 50), and 8x (at the age of 60) of annual income.

Keeping track of financial decisions, revisiting them at least once a year, and reflecting on the mistakes can go a long way to keep the common behavioural pitfalls in check.

The author is working as the Senior Investment Analyst at UCB Asset Management. risalat.huda@ucbasset.com

© 2026 - All Rights with The Financial Express