![]() The consumption of unhealthy products is increasing globally, contributing to non-communicable diseases. The intake of sugar-sweetened beverages (SSBs) correlates with less healthy behaviours, such as smoking, insomnia, less exercise, frequent consumption of fast food, and increased screen time among adults and adolescents.

The consumption of unhealthy products is increasing globally, contributing to non-communicable diseases. The intake of sugar-sweetened beverages (SSBs) correlates with less healthy behaviours, such as smoking, insomnia, less exercise, frequent consumption of fast food, and increased screen time among adults and adolescents.

There is an association of increased soft-drink intake with obesity and increased health problems, such as Type II diabetes, tooth decay, kidney diseases, cardiovascular diseases, and gout. Keeping other things constant, if one consumes an SSB daily, s/he can gain weight by 5 pounds in a year. One who drinks one to two cans daily possess a 26-percent higher risk of developing type- II diabetes mellitus disease with other metabolic syndromes.

The consequences of drinking SSBs are obesity with chronic diseases, which can even result in premature death. Regular consumption of SSBs can reduce academic performance and increase body-mass index (BMI) among students.

Tobacco use is another major public health problem, leading to an increased risk of cancers and deaths due to cardiovascular diseases. Tobacco consumption during pregnancy is associated with low birth weight and stillbirths. More than 11.4 million premature deaths annually (20 per cent of all global death) could be prevented by reducing the consumption of tobacco, alcohol and sugar-sweetened beverages. Consumption of these unhealthy products includes direct (out-of-pocket expenditure) and indirect costs (public health cost) to the consumer and society in treating diseases.

Health taxes on unwholesome products

Health taxes are taxes applied to products adversely affecting public health. Excise taxes are one of the most cost-effective policy tools to tackle the consumption of unhealthy products: higher rates can lead to higher prices and reduce affordability, curbing use and raising revenues. Sugar-sweetened beverages or 'sugary drinks' subject to tax may include refreshing, nourishing, stimulating, soothing and appetizing ones. Increasing the price of SSB by 20 per cent through tax implementation can help reduce the consumption of the same as much (20 per cent). Raising tobacco taxes is also considered most cost-effective measure for reducing its use. Evidence shows that a well-administered tobacco tax leads to the desired result of lowering consumption, particularly among the youth and the poor. They also reduce the health and economic devastation caused by tobacco. At the same time, raising tobacco taxes can bring in new revenues to finance health and development efforts.

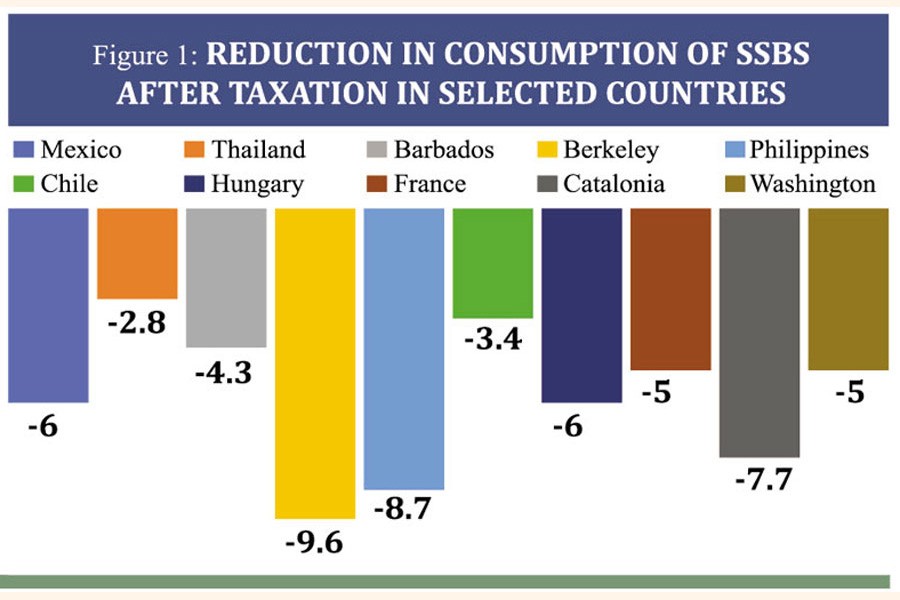

Around 40 countries have implemented taxes on SSB to date. The most common form of taxes used for SSBs is ad valorem excise taxes. Several countries also impose a specific tax on volume or sugar content, which applies various rates depending on the sugar content. Taxes coupled with advertising regulation have brought down both sugar- and sugary-drink consumption in Norway to the lowest level in the last 44 years.

Many drink manufacturers in Ireland have reformulated their recipes and reduced their respective sugar contents to avoid the specific sugar tax. In France, the tiered specific tax is fully transmitted into soft drinks and partially into fruit juices.

The specific and tiered UK sugar tax induced significant decreases in the sugar content of SSBs.

In Chile, the purchase of higher-taxed sugary soft drinks significantly decreased, by 21.6 per cent. The 3-tiered SSB tax in Thailand motivated producers to bring novel versions of their drinks with less sugar content. SSB Tax in Malaysia has different rates for drinks containing different sugar levels. In the Philippines, SSB taxes have raised the prices by up to 20.6 per cent and reduced consumption by 8.7 per cent. This could prevent 24,000 premature deaths over the upcoming two decades.

Globally, 66 countries practice specifically only excise-taxation system. Of them, 19 were from higher-income countries, 19 from upper-middle income, 21 from lower-middle-income, and 7 were from lower-income countries. A mixture of both specific and ad-valorem excise taxes is being applied by 61 countries, 29 of them from higher-income countries, 19 from upper-middle income, 11 from lower-middle-income and 2 from lower-income countries.

Taxes on unhealthy products in Bangladesh

The following two general taxes tax SSBs that are domestically produced:

1. Value-added tax is levied at a single rate of 15 per cent.

2. Supplementary duty (SD) for domestically produced SSBs is 25 per cent for carbonated beverages, and SD for energy drinks is 35 per cent.

Though taxation is the most effective and cost-effective way of tobacco control, Bangladesh could not achieve the expected results for its faulty taxation system. Due to the complex multi-tiered ad-valorem tax structure, cigarettes remain cheap and affordable.

As a result, smokers are switching to cheaper cigarettes instead of quitting. Variation in the type of tobacco product (cigarettes, bidis, and smokeless tobacco) has made the situation more challenging. Low taxes and prices on bidis and smokeless tobacco keep these products highly affordable. In Bangladesh, myths regarding revenue earnings from tobacco tax and weak tax administration result in low tobacco taxation. Moreover, the ad-valorem tobacco-tax structure is the cause of unexpected profit growth of tobacco industries.

Comprehensive tobacco tax policy and policies for SSB

Raising taxes may not lead to an increase in prices, and the tax structure, which determines the type of tax imposed on the products and how it is collected, can make a significant difference in how a tax increase raises the prices of these products. Developing efficient and effective tax administration ensures that the impact of health taxes is maximized and not undermined by tax avoidance and evasion, including illicit trade.

The government of Bangladesh is facing multiple difficulties, including tax evasion as a consequence of the existing complex, multi-tiered tax structure and the inadequacy of the tax-collection and- monitoring system. A comprehensive tobacco-tax policy could be the wisest decision for the government to protect public health and generate the expected revenue. Different policies, acts and regulations are in place in Bangladesh, which can directly and/or indirectly influence tobacco tax. However, a comprehensive 'Tobacco Tax Policy' is a sine qua non, which can be a fundamental guideline describing a set of general plans of action.

Taxes on all SSBs need to be imposed so that people do not switch to low-price products as close substitutes. A standard classification of drinks based on sugar content and other ingredients can be defined. Consumer associations and academics across countries are coming up with the idea of imposing a general tax on sugar used in SSBs itself. This can be considered for Bangladesh as well.

The Ministry of Health and Family Welfare and Bangladesh Standards and Testing Institution (BSTI) can take the initiative to agree on the 'maximum' amount of sugar and other ingredients to be used in SSB. Similar to tobacco products, a health development surcharge on SSBs can be imposed, and the amount raised from health development surcharge for obesity control and other related diseases. Lessons can be learnt from existing health development surcharge on tobacco products.

The continuous growth of tobacco and SSB products at an affordable price will encourage consumption among lower socioeconomic groups and youths, leading to adverse health impacts on future generations, especially poorer people. Imposing specific tax, adjusted to inflation and income growth annually, can be effective for tobacco-and-SSB tax and price increases, thereby reducing consumption of these unhealthy products. A complex tax structure with multiple tax rates may create an administrative challenge for revenue generation due to widespread tax avoidance by producers and consumers. This, in turn, may limit the effect of tax increases on reducing tobacco and SSB consumption.

Bangladesh can potentially make major public health and revenue gains by adopting appropriate taxation on unhealthy products. A multispectral approach is needed for tobacco control, and the tobacco-tax policy can be formulated to ensure synergy among all stakeholders. The same applies to SBB as well.

Rumana Huque is a Professor at the Department of Economics, the University of Dhaka.

rumanah14@yahoo.com

© 2026 - All Rights with The Financial Express