![]() Like any essential service, investing is a necessity to secure the future. Most people in Bangladesh mainly invest their savings in Sanchaypatra, bank deposits, real estate or a combination of those. In this time of looming global recession, geopolitical tensions, inflationary pressures and many uncertainties, safeguarding wealth has become more important.

Like any essential service, investing is a necessity to secure the future. Most people in Bangladesh mainly invest their savings in Sanchaypatra, bank deposits, real estate or a combination of those. In this time of looming global recession, geopolitical tensions, inflationary pressures and many uncertainties, safeguarding wealth has become more important.

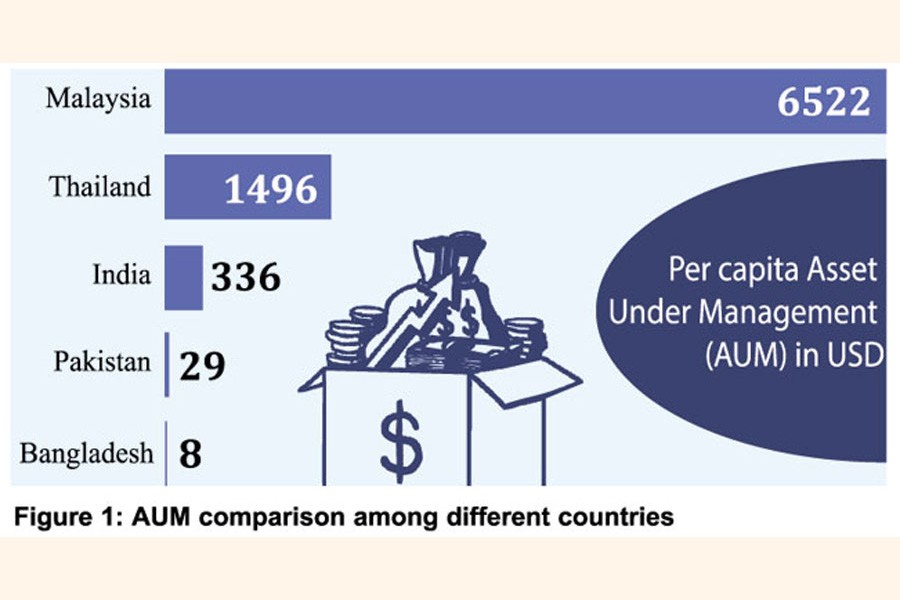

In Bangladesh, the idea of investing in mutual funds began in 1978 with the introduction of the ICB Unit Fund. The first ICB Unit Fund was a major success. However, the industry has not kept up with its potential over the years. If we compare the per-capita AUM (asset under management) of mutual funds among various nations in figure 01, we can understand that Bangladesh has clearly lagged behind.

Though the GDP of Pakistan is lower than that of Bangladesh, a Pakistani citizen invests three times a Bangladeshi does. The multiple is significantly higher for Pakistan, Thailand and Malaysia. Multiple factors explain why Bangladesh's investment-management industry has not grown properly. However, we will only limit this discussion to taxation. Getting taxation right for mutual funds is of immense importance because the same logic broadly applies to other investment products such as Exchange Traded Funds, Index Funds, Real Estate Investment Trusts, Alternate Investment Funds etc.

The existing tax treatment of mutual funds stifling growth: In Bangladesh, the tax authorities have been promoting direct investing in the stock market. For individuals, capital-gain tax is zero, and dividend income is also exempted to a certain extent. This has helped the market grow to a significant size over the years. However, the market is heavily dependent on retail investors who are momentum-driven and do speculative investing. The investment-management industry's small size leads to price-discovery inefficiency.

The existing tax treatment of mutual funds stifling growth: In Bangladesh, the tax authorities have been promoting direct investing in the stock market. For individuals, capital-gain tax is zero, and dividend income is also exempted to a certain extent. This has helped the market grow to a significant size over the years. However, the market is heavily dependent on retail investors who are momentum-driven and do speculative investing. The investment-management industry's small size leads to price-discovery inefficiency.

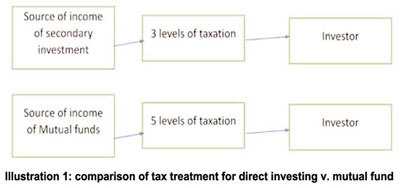

Regarding the tax treatment of direct investing versus using a fund manager, we have found two types of discrimination:

• Tax treatments that massively favour direct secondary investment encourage risky behaviour.

• In addition to that, the tax treatment is not equal for closed-end and open-end funds.

One-taka income from direct secondary investing is taxed at 3 levels compared to 1.0-taka income for mutual funds to investors taxed at 5 levels. The illustration 1 visualises the tax burdens:

Following table details the current tax practice in Bangladesh: A study in 2021 was conducted on three main sources of income of a mutual fund. On average, a mutual fund earns dividend income from securities (26%), interest income (12%) and capital gains (62%), respectively.

As per Bangladesh Securities and Exchange Commission Mutual Fund Rules 2001, a mutual fund has to pay a cash dividend. When capital gains along with all incomes are summed and declared as a dividend, the entire capital gains are taxed as mentioned in table 01. Therefore, investors will be rationally better off by not investing in mutual funds.

In addition, the dividend exemption of Tk 50,000 is applicable to closed-end funds in comparison to Tk 25,000 for open-end funds. Though both are governed under the same rules of BSEC and have the same modus operandi, the motivation for investment in closed-end funds remains strong.

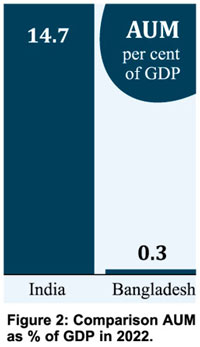

Regional tax practices: In India, the income of mutual funds at the fund level is tax- exempted under the Income Tax Act. The income received by the investors is taxed only at the investors' hands. There is no double taxation. When a company gives a dividend, there is no tax at the fund level because the mutual fund is deemed a pass-through vehicle, and the main beneficiaries are investors.

Policymakers in India understood the importance of keeping the golden goose alive, and now they are enjoying the nested eggs, which is seen by the relative size of AUM in GDP. India gave special tax benefits to the mutual-fund industry for many years to grow the industry. Once it matured, it removed the privileges but continued a fair tax policy.

How growth of mutual fund industry benefit country: The investment options for investors are very limited and poorly governed. The scams of e-commerce companies and multi-level marketing are a few examples. Investment in Sanchaypatra is capped because it bears a higher cost to the government, which was eventually financed by more public debts.

How growth of mutual fund industry benefit country: The investment options for investors are very limited and poorly governed. The scams of e-commerce companies and multi-level marketing are a few examples. Investment in Sanchaypatra is capped because it bears a higher cost to the government, which was eventually financed by more public debts.

For business activities to flourish, the interest rate is kept low, which leads to lower deposit rates. The present real rate of returns on deposits is negative as they do not cover the inflation rate. Investment in real estate is out of reach of the average population. That investment is also illiquid. When one needs to sell properties, it becomes difficult and often forced to sell at prices far below the expected price.

In addition, the whole savings industry is in a primitive state as there is no formal pension system. People had to either prolong their service period or become dependent on other family members.

A mature mutual fund and investment- management industry can remove most problems. Fixed-income mutual funds can provide a better return than that of bank deposits for an investor who wants regular cash flows. Equity mutual funds can provide an inflation hedge. Real-estate mutual funds (REITs) can provide access to the property with smaller investments. In the USA, there is a centralised retirement- management system, which is very popular, called 401 (k) plan. It tries to secure retirement by investing in a combination of mutual funds per each employee's needs and circumstances.

In this study by Costanzo, G. (2011), "The Contribution of the Asset Management Industry to Long-term Growth", OECD Journal: Financial Market Trends, vol. 2011/1, it is shown that asset-management companies, by allocating capital efficiently, by providing liquidity and by fair pricing can accelerate financial intermediation. Efficient financial intermediation leads to sustainable economic growth.

Assuming a mutual fund pays a 10-percent dividend each year if the total mutual industry doubles in size from Tk 14,000 crore to Tk 28,000 crore, dividend income will increase from 1400 crore to Tk 2800 crore. Revenue collection for the NBR from dividend income will increase significantly.

Bangladesh clearly suffers from a lack of effective investment intermediation where people with a surplus can invest in good viable projects and assets. A well-regulated investment-management industry solves this problem.

In conclusion it can be emphasised that it's important that we solve the tax issues surrounding managed-investment vehicles such as mutual funds. In our opinion, the treatment of managed-investment vehicles should be the same as direct investing. If possible, policymakers can consider giving some extra incentives to promote the sector and later phase it out, like in India. The incentives can also be targeted to small savers who realise bank deposits are giving a negative real return at present.

The issue is of national significance as the country moves to greater heights and our policymakers introduce various newly managed investment products. While many other issues need to be resolved to truly take the country to the levels seen in our neighbouring countries, righting tax treatment will be a good start.

Kazi Ahsan Maruf, CFA, is Managing Director at Ekush Wealth Management Limited and Asif Khan, CFA, is Chairman at EDGE AMC Limited. All views expressed are personal.

ahsan.maruf154@gmail.com, asif@edgeamc.com

© 2026 - All Rights with The Financial Express