Bangladesh Bank headquarters in Motijheel, Dhaka. — FE photo

Bangladesh Bank headquarters in Motijheel, Dhaka. — FE photo ![]() It has been more than a year since the economy of Bangladesh started to face the current phase of macroeconomic instability. The story is familiar. A sharp rise in trade deficit combined with the slow growth of remittances put pressure on the current account balance. With the exchange rate coming under pressure, the government continued its policy of keeping Taka strong by selling foreign exchange. As a result, there has been a continuous depletion of the foreign exchange reserve and further pressure on Taka. Reserves of foreign exchange declined from US$ 46.39 billion in 2020-21 to US$ 21.06 billion in September 2023. While the former was equivalent to 6.1 months of import bill of that year, the latter is about 3.5 months of imports (on the assumption of USD six billion per month). Minor tinkering with the exchange rate failed to correct the situation, and the flow of remittances never became normal.

It has been more than a year since the economy of Bangladesh started to face the current phase of macroeconomic instability. The story is familiar. A sharp rise in trade deficit combined with the slow growth of remittances put pressure on the current account balance. With the exchange rate coming under pressure, the government continued its policy of keeping Taka strong by selling foreign exchange. As a result, there has been a continuous depletion of the foreign exchange reserve and further pressure on Taka. Reserves of foreign exchange declined from US$ 46.39 billion in 2020-21 to US$ 21.06 billion in September 2023. While the former was equivalent to 6.1 months of import bill of that year, the latter is about 3.5 months of imports (on the assumption of USD six billion per month). Minor tinkering with the exchange rate failed to correct the situation, and the flow of remittances never became normal.

The rate of inflation started to rise in 2021-22. From 5.56 per cent in 2020-21, the rate rose to 9.92 per cent in August 2023 before falling slightly to 9.63 per cent in September. Even during the earlier episode of macroeconomic instability in 2011 and 2012, inflation rate did not exceed nine per cent.

POLICY MISTAKES WERE MADE BY THE GOVERNMENT: In the face of the challenges mentioned above, there have been public pronouncements from high level policy makers that not only demonstrated the ambivalence of the government about its policy stance but also created confusion at times. The major policy mistakes made by the government in recent years may be summed up as follows: (i) keeping the exchange rate fixed when economic fundamentals warranted adjustments, (ii) fixing interest rates on deposits and lending, thereby providing wrong signals to economic actors, (iii) raising administered prices (e.g., of petroleum products and electricity) at a time when the monster of inflation was already raising its head, (iv) not making proper assessment of supply of and demand for key commodities and arranging their timely imports, and (v) not making appropriate use of tariff policy to counter the price effects of currency depreciation and to provide competition to domestic producers.

Independent policy analysts (including the present author) have pointed out such mistakes and provided suggestions on how the situation could be handled. Their suggestions range from orthodox to heterodox, with most belonging to the former that recommend leaving the exchange rate and interest rate to be determined by the market. Such thinking and recommendations are based on a few assumptions like the following.

Left to the market, the exchange rate will find its correct level at which imports will be discouraged and exports encouraged automatically. So, trade balance should improve. On the remittance front, more Taka for a unit of foreign currency will encourage remitters to send more money or make more use of official channels to remit money. As a result of these, current account balance should improve.

On the use of interest rate (and monetary policy as a whole) to fight inflation, the assumption is that it is basically due to excess demand which will be discouraged by higher interest rate. So, a rise in interest rate will lead to a decline in inflation rate.

The government resisted devaluation of the currency, adopted measures to discourage imports of so-called non-essential items, and tried to compel exporters to bring back export receipts within the stipulated time limit. On the side of monetary policy, the fixed interest rate regime was retained for quite some time, although other instruments like the repo rate was used. But these measures were not successful in bringing the desired results either on the external account or domestic inflation.

THE GOVERNMENT TURNS TO IMF FOR LOAN: As foreign exchange reserves continued to decline and the inflationary pressure remained unabated, rather than trying to meet the challenges on its own, the government went for the relatively easy solution of taking loan from the International Monetary Fund (IMF). A credit programme for $4.7 billion was agreed upon in January 2023. The duration of the loan is 42 months, and it is to be disbursed in seven instalments - subject to satisfactory review by the agency.

This is the 11th time Bangladesh has gone for loan from the IMF - the last being in 2012. As is well-known, credit from the IMF comes with strings attached - usually for market oriented "reforms". And the latest one is no exception. Categorised under: (i) Quantitative Performance Criteria (QPC), (ii) Indicative Targets (IT), and (iii) Structural Benchmarks (SB), they include floors on net international reserves - to be raised to the level of four months' import by 2026, fiscal deficit to be limited to 3.6 per cent of Gross Domestic Product (GDP), scrapping of the fixed interest rate regime and moving to an interest corridor system, move to market determined exchange rate, calculation of net international reserves according to the IMF method, estimation of GDP on a quarterly basis, and periodic adjustments in the prices of petroleum products and electricity - among others. In addition, the MOU mentions inflation target of 5-6 per cent and limiting public debt to 45 per cent of GDP.

While some of these goals and targets are quite reasonable and the government should have been working on them anyway, there are those that can be questioned. For example, there was no need to submit to the IMF for the target of raising foreign exchange reserve to a more comfortable level, raising tax revenue (low tax-GDP ratio of the country has long been a subject of discussion), abandoning the fixed interest rate and fixed exchange rate regimes, etc.

The recommendation of limiting the budget deficit to 3.6 per cent of GDP is also questionable because fiscal policy will have to be used to complement monetary policy in addressing the current macroeconomic challenges. That may require reduction of import duties on selected items, increase of public expenditure, especially in infrastructure, and increase of expenditure on social safety nets to protect the poor from the negative effects of stabilisation.

By signing the agreement, the government agreed to the package of conditions that included the very measures it was resisting for quite some time. Although these measures are due for implementation in 2023, major conditions like allowing the market to determine the exchange rate and interest rate have not yet been met.

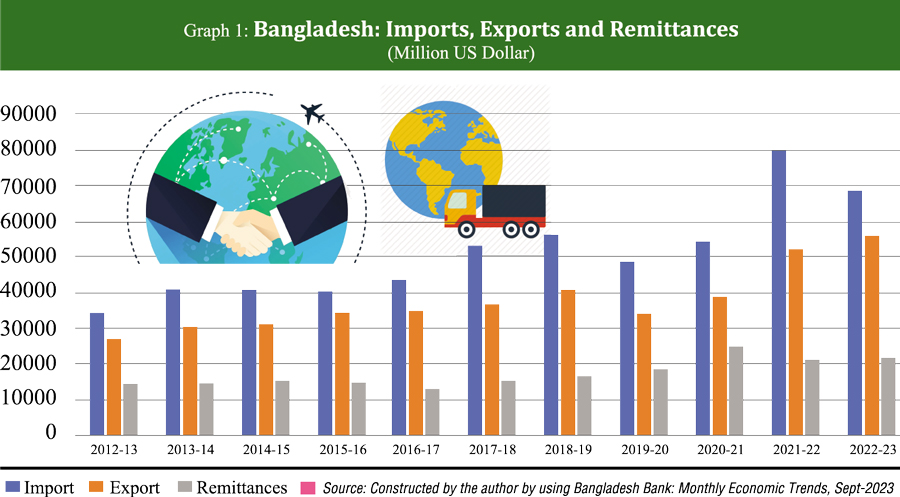

MACROECONOMIC INSTABILITY CONTINUES: Despite the loan from the IMF, the challenges on the macroeconomic front that surfaced in 2022 continue till today. Some indicators on the external accounts of the country and exchange rate of the currency are shown in Graphs 1 through 3. A few points in this regard would be worth noting. First, after a sudden jump in 2021-22, imports declined in 2022-23, but remained at a much higher level compared to the levels of recent years. While the primary reasons for this sharp rise include the post-pandemic revival of economic activities and the rise in the prices of commodities in the global market, over-invoicing of imports and capital flights through use of the import channel are also suspected to have played a role.

Second, remittances declined in 2021-22 and remained sluggish in 2022-23 as well. The importance of remittances can be seen from the fact that despite increase in exports in 2021-22 and 2022-23 (Graph-1), the slide in foreign exchange reserves is continuing. Remittances play an important role in balancing the external account; and unless there is a sustained turnaround in its flow, imbalance will continue. The flow in October 2023 indicates a turnaround, but one month's figure does not represent a trend.

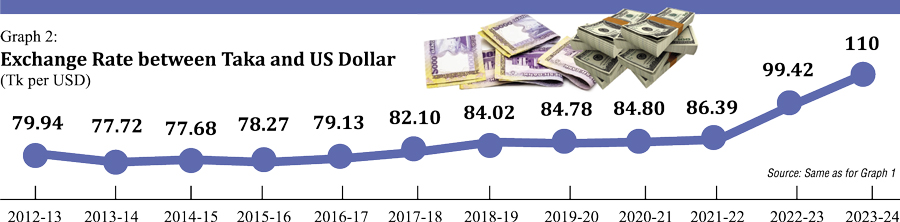

Third, with a continuous slide in foreign exchange reserve for more than a year now, exchange rate between Taka and US Dollars came under pressure and the latter became 27 per cent more expensive vis-à-vis Taka in a little over a year. As the government tried to tackle the situation by restricting imports, the result was a kind of double whammy in the domestic market for imported goods - rise in their Taka value coupled with supply bottlenecks. This policy made inflation fighting difficult and had a negative effect on economic activities dependent on imported inputs.

Fourth, several aspects of the movement in the exchange rate over time are noticeable. On the one hand, it was kept unchanged for three years from 2019-20 - a glaring policy mistake. That was also the period of low inflation in the global market, and the economy of Bangladesh also enjoyed a period of low inflation. But since April 2022, Taka started its slide and that has continued since then (Graph-2). As a result, prices of imported goods in the domestic market have been rising continuously. Rather than a one-off price rise that would have resulted from one-shot devaluation, the economy is seeing creeping inflation associated with a continuous slide of Taka.

Uncertainty in the economic environment is having an impact on the foreign exchange market, and even after a substantial depreciation of Taka, the difference between the official exchange rate and the informal rate has widened. Moreover, with the way in which the exchange rate is being determined and the incremental approach to adjusting the rate, a "depreciation expectation" has been created. This, coupled with the big difference between the official and informal rates, is having a deleterious effect on the flow of remittances through official channels. Unless and until the flow of remittances becomes normal, a rise in exports alone will not be able to build back the foreign exchange reserves.

The expectation of depreciation is having an adverse effect on foreign exchange reserve through another route: reluctance of exporters to bring back their earnings into the country within the stipulated period.

ONE-SIZE-FITS-ALL APPROACH IS NOT USEFUL: For stabilising the exchange rate, the going orthodoxy until recently was to leave it to the market so that the forces of supply and demand could determine the market clearing rate. But the present author, in an article in 2022 (The Financial Express, November 10, 2022), had suggested the method of "crawling peg" as a possible alternative - especially for avoiding a possible adverse effect on inflation. Interestingly, during its periodic review of the economy in October, the IMF is reported to have advised the government to adopt this method. It needs to be noted, however, that if this method is applied now and that continues to fuel the "depreciation expectation", the desired impact on remittances through the official channel may not materialize. Whatever method is used, it would be important to ensure a unified exchange rate and to minimise the difference between the official and informal exchange rate. Only then can the flow of remittances through official channels be expected to become normal.

The challenge of fighting inflation is more intractable. Although monetary policy tools, especially interest rate are being used worldwide, and examples of other countries are often cited in support of this tool, their effectiveness cannot be taken for granted. A lot depends on the specific situation and the factors involved. A few examples may be useful in this context.

• In the USA, interest rate has been raised continuously (from near-zero to a record high of 5.25 per cent) for over two years since 2021. Although the rate of inflation has fallen from over nine per cent to 3.7 per cent (in September 2023), it is still far above the pre-pandemic level of two per cent (which is also the target of Federal Reserve). Moreover, there are views that a large part of this decline is due more to the easing of pandemic time supply bottlenecks. Also, growth of the economy has not yet been adversely affected primarily because of the personal wealth accumulated by consumers during the pandemic, which, in turn, is ascribed, at least partially, to the huge stimulus programme implemented by the government during the pandemic.

"In UK, from less than 1.0 per cent in 2019, the interest rate was raised to 5.25 per cent, and yet, the rate of inflation has remained high at 6.7 per cent (in September 2023). GDP growth has dipped below 1.0 per cent in 2023 (from 4.3 per cent in 2022).

• Sri Lanka, under the tutelage of IMF has been able to fight inflation successfully by raising interest rate. But the economy has contracted sharply, with negative GDP growth throughout 2022 and the first quarter of 2023. The economy contracted by 7.4 per cent, 11.5 per cent, 12.4per cent and 11.5 per cent in the second, third and fourth quarters of 2022 and the first quarter of 2023 respectively.

• Thailand's story is somewhat similar. The country's GDP growth in 2021 and 2022 (1.5 per cent and 2.6 per cent) was nowhere near the pre-pandemic level of 4.2per cent.

A few conclusions can be drawn from the above experiences. First, one single tool (e.g., interest rate) cannot be equally applicable in all cases. It can produce divergent results depending on the background, context, and circumstances. One can legitimately ask whether interest rate is the appropriate tool for fighting the price volatility of consumer goods like edible oil, eggs, onions, and green chillies. Second, even if the tool can produce the desired result, it could be accompanied by "side effects" that are not desirable. In fighting inflation, Bangladesh may have to accept a degree of growth moderation. But it is important to ask if an outright recession and economic contraction (of the kind Sri Lanka is experiencing) is acceptable.

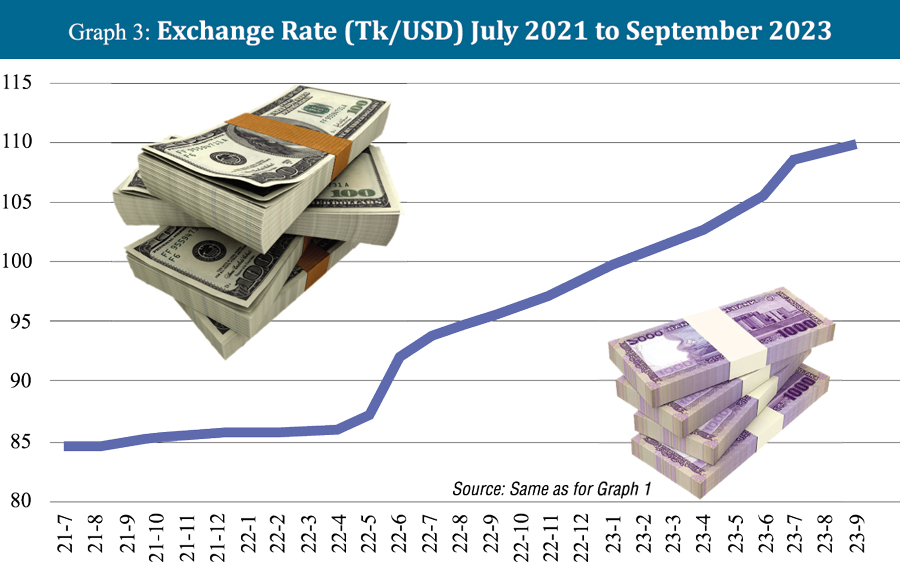

Anyone with some familiarity with the recent inflationary situation in Bangladesh would know that price increases of many items are due to a variety of factors other than excess demand. As the data on exchange rate movement (presented in Graph-3) shows, the depreciation of Taka has been a continuous process rather than a one-off devaluation. The impact of that on the domestic prices of imported goods has naturally remained persistent. And this trend is likely to continue until the exchange rate stabilises.

Anyone with some familiarity with the recent inflationary situation in Bangladesh would know that price increases of many items are due to a variety of factors other than excess demand. As the data on exchange rate movement (presented in Graph-3) shows, the depreciation of Taka has been a continuous process rather than a one-off devaluation. The impact of that on the domestic prices of imported goods has naturally remained persistent. And this trend is likely to continue until the exchange rate stabilises.

Second, measures needed to address shortages will have to be planned and executed before price increases hit the market. Recent episodes show that management of imports and supply has been inefficient to say the least. Decisions to import some items came only after their prices had raised several folds; and even after decisions were made, their actual arrival in the market took place when it was too late.

Third, tariff rates can be adjusted, even if for short periods, for imported goods whose prices contribute to inflationary pressure. This of course will give rise to a trade-off between budget balance and inflation control because of the negative impact on revenue collection. Hence such a measure will have to be temporary.

BOLD AND QUICK DECISIONS ARE REQUIRED TO ADDRESS THE CHALLENGES: Measures needed to restore macroeconomic stability are by now known with a reasonable degree of clarity. What remains to be done is to adopt and implement the selected measures with urgency and efficiency. And there comes the political aspects of policy making. It appears that no major new measures are going to be undertaken before the upcoming national elections in early 2024. That would mean at least another three months of uncertainty and continuation of "depreciation expectation" in the foreign exchange market which, in turn, may delay the return of remittance flow to its normal level. So, the process of rebuilding the foreign exchange reserves is also likely to be delayed. If the depletion of reserves continues for a few more months, it may drop below three months' import bill - the threshold of comfort.

To fight inflation, timely and decisive action will be needed on multiple fronts. If interest rate is raised, its impact is likely to come with a time lag. During the interim period, supply side interventions will be needed, especially for items that are sensitive to price fluctuations. Measures should be undertaken to protect the poor from the adverse effects of inflation, e.g., by bringing more people and more items in the government's open market sales programme and augmenting their supplies. Advance estimation of import requirements, and better planning and implementation of imports would also be important.

GDP growth already fell in 2022-23 (from 7.1 per cent in 2021-22 to 6.03 per cent in 2022-23); and the trend is going to continue in 2023-24. If the slide in foreign exchange reserves continues (a likely scenario if the flow remittances does not return to normal level), the flow of imports will also remain uncertain at best. That, coupled with a rise in interest rates, is likely to result in further reduction in output growth. In other words, stabilization will be associated with growth moderation.

When economic growth falters, the employment and labour market situation is bound to become more precarious. With wage growth already behind inflation rate for quite some time and the ominous prospect of inflation remaining high for a prolonged period, the plight of the poor and low-income people is almost certain to worsen. If the economic policy process gets entangled into the political process in this kind of a dire situation, the time needed for stabilisation of the economy will become longer. And with that, the suffering of common people will continue. Is anyone listening?

Dr Rizwanul Islam, an economist, is former Special Adviser, Employment Sector, International Labour Office, Geneva.

rizwanul.islam49@gmail.com

© 2026 - All Rights with The Financial Express