![]() The European Union (EU), as an economic bloc, has been the single largest destination for Bangladesh's exports. Leveraging the EU's generous Generalised System of Preference (GSP) scheme for Least Developed Countries (LDCs), known as Everything But Arms (EBA), Bangladesh has rapidly expanded its exports from less than $2 billion in FY01 to $25.2 billion in FY23, thanks primarily to apparel or ready-made garment items. Such an overwhelming reliance on a single broad export category can pose serious challenges, as any shocks to the sector could severely impact export revenues. Additionally, within the apparel sector, Bangladesh's exports are concentrated to cotton-based garment items, contrary to the current global market trend favouring man-made fibre-based clothing products. This article explores Bangladesh's opportunities for export diversification in the EU market, both in the garment sector and in non-RMG sectors, with the aim of expanding exports.

The European Union (EU), as an economic bloc, has been the single largest destination for Bangladesh's exports. Leveraging the EU's generous Generalised System of Preference (GSP) scheme for Least Developed Countries (LDCs), known as Everything But Arms (EBA), Bangladesh has rapidly expanded its exports from less than $2 billion in FY01 to $25.2 billion in FY23, thanks primarily to apparel or ready-made garment items. Such an overwhelming reliance on a single broad export category can pose serious challenges, as any shocks to the sector could severely impact export revenues. Additionally, within the apparel sector, Bangladesh's exports are concentrated to cotton-based garment items, contrary to the current global market trend favouring man-made fibre-based clothing products. This article explores Bangladesh's opportunities for export diversification in the EU market, both in the garment sector and in non-RMG sectors, with the aim of expanding exports.

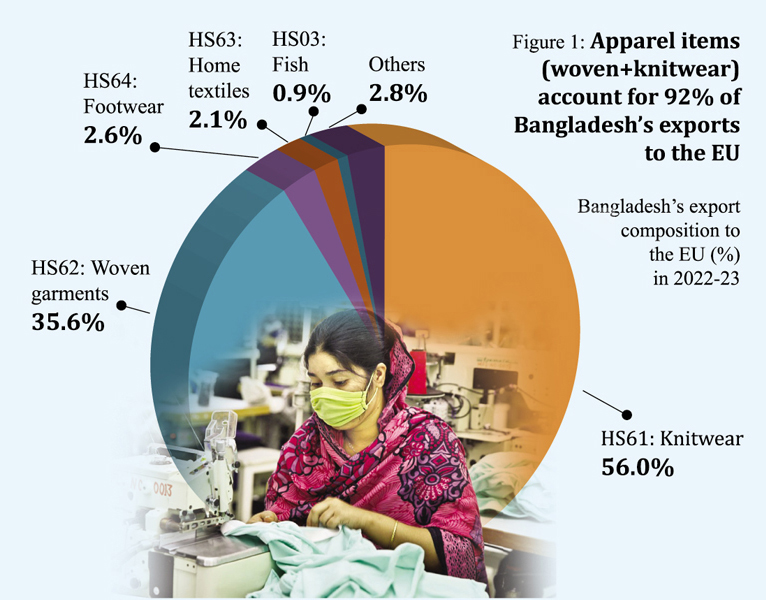

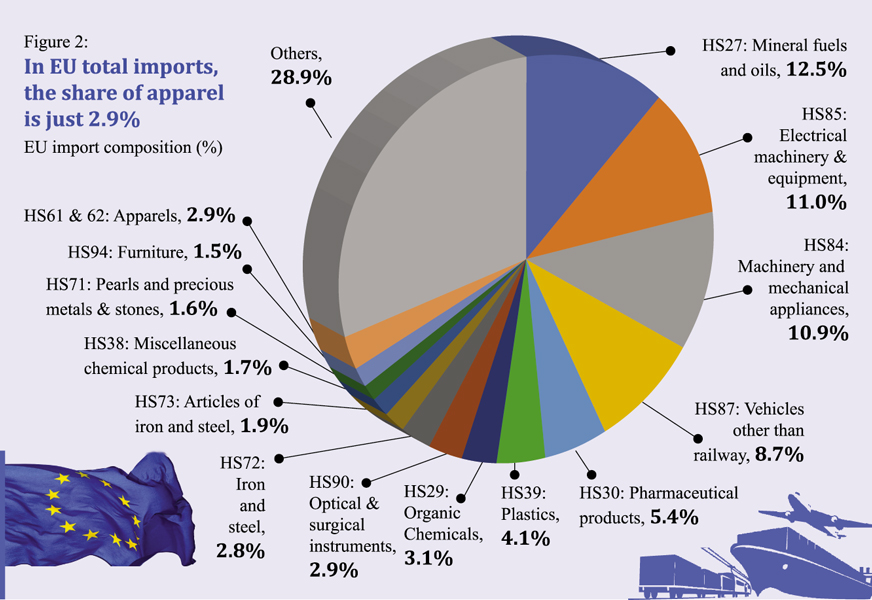

BANGLADESH-EU TRADE RELATIONSHIP AND THE PROPOSED EU GSP 2024-34: The EU accounts for 45 per cent of Bangladesh's export earnings. Apart from apparel products, Bangladesh also exports products such as footwear, home textile, frozen fish, bicycles, etc. But it is the apparel products that have overshadowed the significance of other sectors. Apparel, comprising both woven and knitwear items, constitutes more than 92 per cent of Bangladesh's exports to the EU. However, in the vast import market of $7.0 trillion, the share of apparel products, imported from all extra-EU countries combined, is just 2.9 per cent. In non-apparel categories, Bangladesh's export presence in the EU is almost non-existent.

BANGLADESH-EU TRADE RELATIONSHIP AND THE PROPOSED EU GSP 2024-34: The EU accounts for 45 per cent of Bangladesh's export earnings. Apart from apparel products, Bangladesh also exports products such as footwear, home textile, frozen fish, bicycles, etc. But it is the apparel products that have overshadowed the significance of other sectors. Apparel, comprising both woven and knitwear items, constitutes more than 92 per cent of Bangladesh's exports to the EU. However, in the vast import market of $7.0 trillion, the share of apparel products, imported from all extra-EU countries combined, is just 2.9 per cent. In non-apparel categories, Bangladesh's export presence in the EU is almost non-existent.

In the past decade, Bangladesh rose as the EU's second-largest supplier of apparel, capitalising on China's declining market share of the same product. While the market share of China dwindled from 44 per cent in 2010 to 29.2 per cent in 2022, Bangladesh saw its share double to 22 per cent during the same period.

It is a widely-held view that the duty-free access and relaxed rules of origin provisions granted to the LDCs contributed significantly to the apparel export success of Bangladesh in the EU market. Given Bangladesh's impending graduation from the group of LDCs, this preferential market access is expected to last until November 2029.

Bangladesh is scheduled to graduate from the group of least developed countries in 2026 while still retaining the LDC-related trade preferences in the EU market for an additional three-year period until November 2029. Following graduation, Bangladesh will have the opportunity to apply for the EU GSP-plus scheme, the second-best preferential tier after EBA, which provides duty-free access accounting for 66 per cent of EU tariff lines. To be eligible for GSP-plus preferences, a country must meet two sets of pre-specified conditions known vulnerability criteria and sustainable development criteria. However, even if Bangladesh meets those two criteria, EU safeguard measures associated with textiles and clothing imports would exclude Bangladesh's apparel exports from being benefited from the duty-free market access. This is because Bangladesh has a much larger apparel market share specified in the proposed EU GSP 2024-34 scheme, which was supposed to come into effect from the beginning of 2024, but its adoption has been deferred. This delay has now opened an important window of opportunity for Bangladesh to engage with the EU to relax the GSP-plus provisions for clothing exports.

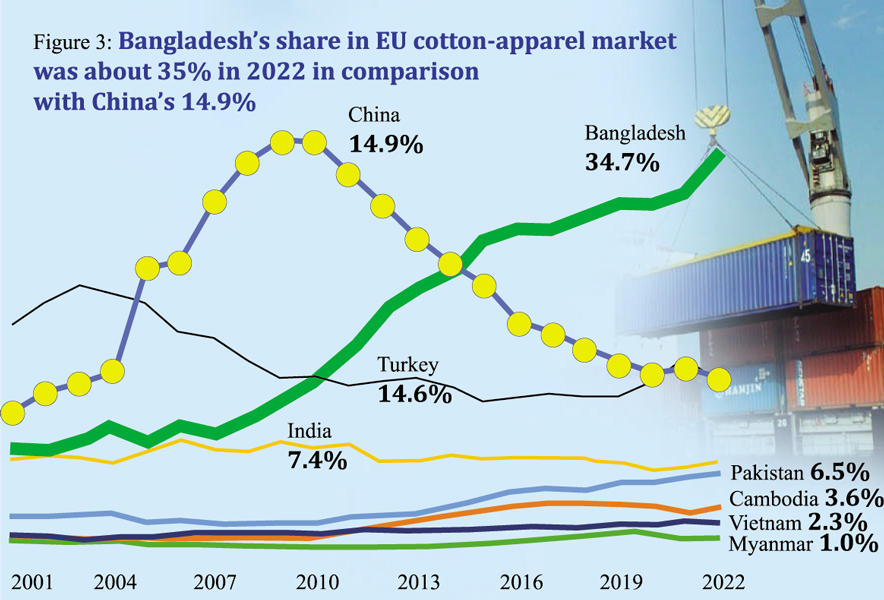

IDENTIFICATION OF POTENTIAL PRODUCTS FOR EXPORT EXPANSION AND DIVERSIFICATION: The EU market offers tremendous export diversification opportunities both for RMG as well as non-RMG sectors. Apparel products are categorised into two types: cotton and non-cotton apparel. Bangladesh has been the largest cotton apparel supplier to the EU since 2015, with the country's market share in the same category rising to about 35 percent in 2022. The global trend is however shifting towards non-cotton items, predominantly man-made fibres-based clothing products as non-cotton apparels currently capture close to 60 per cent of all global exports. In contrast, less than 30 per cent of Bangladesh's apparel products are in the non-cotton category. Amongst others, the massive dependence on the EU-bound cotton apparel has made Bangladesh's exports limited to such items.

Non-cotton items are dominated by man-made fibre-based products that many consumers prefer for their characteristics like moisture-wicking, wrinkle resistance, and easy for day-to-day usages. These fibres promise durability, longer lifespan, and easier maintenance, appealing to today's practical consumers. Environmental policies, especially in regions like the EU, are steering the textile industry towards sustainable fibres. MMFs have several sustainability advantages including polyester items' requiring less water than cotton, and their perceived smaller ecological footprint in terms of soil erosion and land use. The global focus is also shifting towards recycled fibres, with polyester leading the recycled fabric market. Therefore, not expanding exports of MMF items could shrink export opportunities in the future.

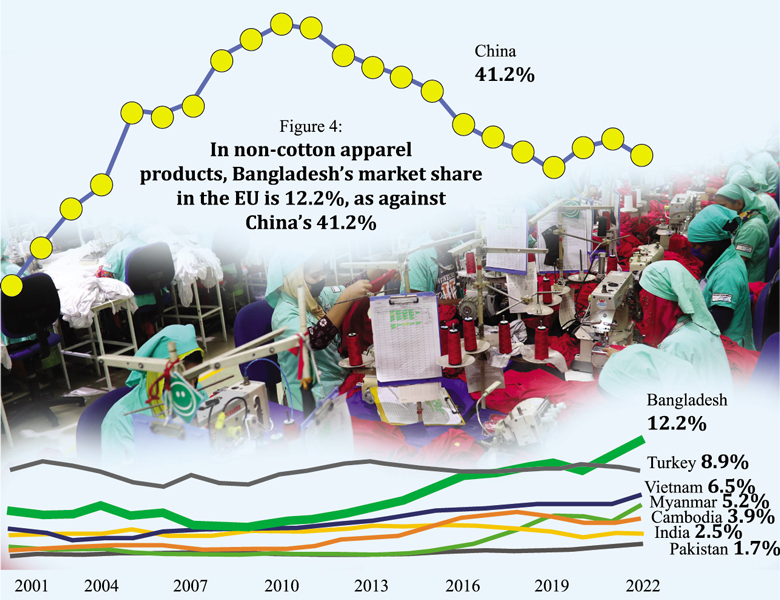

There exists a vast potential to boost the export of non-cotton apparel in the EU. In this particular segment, Bangladesh is currently the second-largest exporter, but it holds only a 12 per cent market share, significantly lagging behind China's dominating 41 per cent. It is anticipated that the market share currently enjoyed by China will fall leaving plenty of space for other countries to fill in. If Bangladesh can manage to secure duty-free access for apparel products for an extended period (i.e., beyond 2029) after LDC graduation, this can lead to a much stronger export response to MMF apparel.

The potential for non-RMG exports is also massive. As mentioned above, in the EU's total import outlay (of $7 trillion), the share of apparel is just 2.9 per cent. In non-apparel EU imports of $6,800 billion, Bangladesh's exports accounted for just $2 billion in 2022, or just 0.014 per cent. This minimal export presence is somewhat perplexing as various analyses indicate Bangladesh's having a comparative advantage in terms of many items where current exports are limited.

The potential for non-RMG exports is also massive. As mentioned above, in the EU's total import outlay (of $7 trillion), the share of apparel is just 2.9 per cent. In non-apparel EU imports of $6,800 billion, Bangladesh's exports accounted for just $2 billion in 2022, or just 0.014 per cent. This minimal export presence is somewhat perplexing as various analyses indicate Bangladesh's having a comparative advantage in terms of many items where current exports are limited.

ASSESSING EXPORT POTENTIAL: Economists often use the so-called Revealed Comparative Advantage (RCA) in assessing the comparative advantage of a country in exporting products. It is based on the observed trade patterns rather than the factors of production that are typically used in other comparative advantage frameworks. This concept is used to help identify a country's competitive advantage in a specific sector using the sector's share in the country's overall exports vis-à-vis the same for the rest of the world or any comparator. Despite its limitations, being a simple indicator that can be implemented with export data, which are usually available for most countries, the appealing factor of RCA continues to be prominent in applied international trade research. The RCA approach can also be applied to assess export potential from Bangladesh emanating from different sets of products under four scenarios: viz., (i) products for which Bangladesh has the revealed comparative advantage (RCA) in the EU market (thus Bangladesh should be able to expand exports), (ii) products for which Bangladesh has

RCA in the rest of the world but not in the EU (i.e., these are the products where Bangladesh can try building RCA in the EU), (iii) products with no RCA for Bangladesh but such comparator countries such as India, China and Vietnam have bilateral RCA (therefore, Bangladesh could build export competitiveness in some of these products), and (iv) products currently not exported from Bangladesh but have high export potential based on their similarity to currently exported items (that is, based on what is known as product-space proximity to current export products).

Using the above assessment framework, it is possible to identify more than 600 products (at the HS 6-digit level) that can generate additional export revenues for Bangladesh. These products fall within sectors such as agriculture, engineering goods, leather goods and footwear, non-leather footwear, home textiles, fish and shrimp, readymade garment, etc.

It is possible to illuminate the magnitude of export potential. A pertinent approach in this context involves adopting a methodology formulated by the International Trade Centre (ITC). This quantitative method estimates the potential export value in a target market by considering the exporters' supply capabilities, the prevailing demand in the pertinent market, and the conditions for market access. The ensuing potential export values are subsequently juxtaposed with actual export revenues, unveiling latent opportunities. Implementing this technique reveals that Bangladesh harbours an untapped export potential in the EU amounting to $19 billion (in contrast to the $25 billion realised from the EU in 2023). The unexploited export potential for non-apparel items stands at an estimated $2.5 billion.

It is possible to illuminate the magnitude of export potential. A pertinent approach in this context involves adopting a methodology formulated by the International Trade Centre (ITC). This quantitative method estimates the potential export value in a target market by considering the exporters' supply capabilities, the prevailing demand in the pertinent market, and the conditions for market access. The ensuing potential export values are subsequently juxtaposed with actual export revenues, unveiling latent opportunities. Implementing this technique reveals that Bangladesh harbours an untapped export potential in the EU amounting to $19 billion (in contrast to the $25 billion realised from the EU in 2023). The unexploited export potential for non-apparel items stands at an estimated $2.5 billion.

Germany exhibits the most significant absolute disparity between potential and actual exports, indicating an opportunity for additional export earnings of $3.8 billion. In other words, approximately 35 per cent of the potential remains untapped in the market of Bangladesh's largest EU partner country. Elsewhere among EU partners, unutilised export potential for Bangladesh includes 38.5 per cent in France, 36 per cent in Spain, 43 per cent in Poland, 47 per cent in Italy, and 53 per cent in the Netherlands.

According to the ITC methodology, apparel items predominantly characterise the unexploited export potential, with over one-third of the apparel export potential remaining untapped. Bangladesh currently exploits just 48 per cent of its export potential in footwear amongst non-apparel items, suggesting potential for an additional $570 million in export earnings from these products. In terms of other categories, leather goods exhibit an untapped export potential exceeding 70 per cent, home textiles 40 per cent, and fish and shrimp 60 per cent.

When the existing export base is small, quantitative exercises will show relatively small export potential, which can be quite unrealistic as well. For the same reason, the suggestion of just $2.5 billion worth of potential exports from Bangladesh's non-RMG sector to the EU's vast market is somewhat misleading. Therefore, a useful approach could be to use Bangladesh's current market share for individual items and then to consider a reasonable expectation about their future market share. This is somewhat subjective in nature but can offer useful directions for the significance of policy and firm-level efforts for export expansion. The most promising export products can be chosen from the set of 600 mentioned above. These products are selected based on factors such as the size of the EU market, the growth of imports into the EU, Bangladesh's current exports, and Bangladesh's share of the EU. An analysis of such most-promising 45 products, which can help achieve the reasonable expected market share, results in an estimated export potential of $8.6 to $22.5 billion. This shows the extent of untapped export potential that Bangladesh must try to materialise.

PREFERENCE MARGINS AFTER LDC GRADUATION: When the market access conditions for potential export diversification items and tariff preferences in the EU for the identified products are examined, the significance of securing the GSP-plus after the LDC graduation becomes clear. For the identified potential agricultural products, Bangladesh currently enjoys zero tariff rates while under GSP-plus, the same tariff rate on average will be 2.7 per cent. Despite the increase, when compared with the EU MFN rate, the GSP-plus scheme will provide Bangladesh a margin of preference (compared with MFN tariff) of 6.1 percentage points. Apart from agriculture, almost zero tariff rates will be applicable under the GSP-plus schemes for other potential sectors. This implies that Bangladesh's current market access under the GSP-plus will continue even after 2029 for the identified potential goods.

However, it is crucial to note that if the safeguard measures (as in the proposed GSP 2024-34) are maintained, the RMG and home textile products will not receive any tariff preference. Instead, they will face an average MFN tariff of about 12 per cent. This will put a significant pressure on Bangladesh's export competitiveness, potentially hurting the export diversification prospect within the RMG sector.

CHALLENGES TO EXPORT DIVERSIFICATION IN THE EU: Facing a multitude of barriers, Bangladesh's journey toward a diversified export outlay in the EU is fraught with challenges, ranging from policy barriers to information deficits to infrastructural constraints. First and foremost, Bangladesh's longstanding trade policy stance, by creating a deeply protective environment, has contributed to a disincentive for exports. An impressive economic growth trajectory of the country over the past few decades has been accompanied by a protectionist trade policy regime, characterised by high tariffs and further compounded by the imposition of para-tariffs, including supplementary and regulatory duties on top of customs duties. The resultant support provided to the domestic import-competing sectors has inadvertently skewed the business landscape, making the domestic market irresistibly lucrative for local enterprises, particularly for the non-garment sectors, thereby dampening the impetus to venture into international markets. As a result, these industries remain ensconced in the comfort of local sales, leaving the country's export response lacklustre and heavily tilted towards the garment sector. The allure of the domestic market, bolstered by these protectionist policies, has created a complacency about overall economic growth, hindering diversification efforts and stifling the growth potential of other promising sectors on the global stage.

The high protectionism granted to local enterprises in Bangladesh has been significantly reinforced by the country's weak adherence to product quality and working environment standards, particularly when benchmarked against the rigorous requirements in international markets. This has resulted in a majority of local establishments finding themselves at a distinct disadvantage, as they are unprepared to meet the stringent requirements necessary for global trade. This situation has created a dependence on the domestic market, as local enterprises continue to rely on government support and the lenient regulatory environment, inhibiting innovation and improvement. The lack of exposure and adaptation to international standards has stymied their competitive edge, resulting in missed opportunities and a limited presence in the global market.

Furthermore, many Bangladeshi potential exporters grapple with a lack of comprehensive market information, leaving them ill-equipped to navigate the complex terrain of EU market demand, quality expectations, and competitive dynamics. The scenario is particularly dire for small and medium enterprises (SMEs), which remain tethered to outdated manual technologies, reducing productivity and competitiveness, a stark contrast to their counterparts in technologically adept nations like China and Vietnam. Additionally, these SMEs are often unfamiliar with international standards, with limited capacity for compliance or improvement.

Most enterprises in Bangladesh are also confronted with a severe shortage of skilled labour, evident in sectors like light engineering, leather goods, footwear, and garments, where the skills gap is widening. Access to finance is regularly reported as a major constraint while trade logistics and infrastructural facilities are plagued by inefficiencies, leading to prohibitive costs and lengthy lead times, thereby eroding the overall export competitiveness. The business environment is rendered hostile by governance challenges, including lax enforcement of labour standards and infrastructural lapses, all of which constrict industrial production for exports, introduce compliance barriers, and compromise product quality.

Bangladesh's limited foray into the global value chain (GVC) curtails its export diversification ambitions, necessitating a more integral engagement with value chains to unlock access to new markets, technologies, and opportunities for value addition, all critical for enhancing the competitive edge in the international arena.

WHAT NEEDS TO BE DONE FOR SUPPORTING EXPORT DIVERSIFICATION IN THE EU: For exploring diversification opportunities in the EU, it is vital to undertake a comprehensive approach covering various aspects of the export sector. On the supply side to boost export response, addressing the highly protective domestic environment is crucial in promoting export incentives, as it will encourage local enterprises to enhance their competitiveness on the global stage. By reducing over-reliance on the domestic market, businesses are motivated to innovate, improve product quality, and adopt international standards, ultimately fostering a more resilient and diversified economic landscape capable of thriving in the competitive global market.

WHAT NEEDS TO BE DONE FOR SUPPORTING EXPORT DIVERSIFICATION IN THE EU: For exploring diversification opportunities in the EU, it is vital to undertake a comprehensive approach covering various aspects of the export sector. On the supply side to boost export response, addressing the highly protective domestic environment is crucial in promoting export incentives, as it will encourage local enterprises to enhance their competitiveness on the global stage. By reducing over-reliance on the domestic market, businesses are motivated to innovate, improve product quality, and adopt international standards, ultimately fostering a more resilient and diversified economic landscape capable of thriving in the competitive global market.

The government has recently adopted the National Tariff Policy, aimed at effective tariff rationalisation to bolster export incentives and create a more conducive environment for international trade. It is now important to implement this initiative both effectively and promptly, ensuring that the potential benefits are fully realised and contribute to the enhancement of the country's export competitiveness.

While in most successful exporting countries, foreign direct investment (FDI) plays a pivotal role, Bangladesh has struggled to attract substantial FDI in its export-oriented sectors. FDI brings not just capital but also introduces advanced technologies, managerial expertise, and opens access to global markets, all of which are integral for enhancing export competitiveness. A concerted effort is necessary to create an investment-friendly environment, addressing regulatory barriers, and promoting ease of doing business to attract more FDI into the country. Integrating non-RMG exporters into the EU supply chain is paramount, necessitating upgrades in industrial capacity and technological capabilities. Without FDI, this will be a very difficult task to achieve.

Adherence to stringent product standards and robust Environmental, Social, and Governance (ESG) practices will be a critical determinant of export success in the European Union, as these factors directly influence a product's marketability and appeal to the increasingly conscious and discerning consumer base within the region. Therefore, enhancing the capacity of the existing standards authorities and institutions such as the Bangladesh Standards and Testing Institution (BSTI) becomes imperative to provide globally recognised certifications and necessary testing facilities to exporters, ensuring compliance with stringent EU standards.

Enforcing robust standards at the local level can be catalytic in shifting the focus of firms from solely domestic sales to embracing international markets, making them export-ready and competitive on a global scale. By aligning local standards with international norms, businesses are compelled to upgrade their practices and product quality, thereby paving the way for a smoother transition into the demanding and diverse global trade landscape.

Ensuring the widespread dissemination of market-specific information stands crucial, equipping potential exporters, particularly in the non-RMG sectors, with knowledge on product-specific market access provisions including rules of origin, and required standards and certification procedures.

As Bangladesh approaches its LDC graduation, active engagement with the EU is necessary to secure favourable terms for the post-LDC graduation era, negotiating for more lenient rules of origin for non-RMG goods. Easing EU safeguard measures against the apparel sector under the EU GSP-plus regime after Bangladesh's LDC graduation can be a major boost for achieving diversification within the garment sector and expanding non-cotton apparel exports.

Addressing obstacles related to the sectors that have export potential in the EU should be considered as a priority policy decision. In the non-cotton-based apparel sector, introducing low-cost financing options and addressing skill shortages are essential. For the agriculture sector, the most pressing issue is enhancing product quality and complying with EU standards. In the fish and shrimp sector, initiatives such as cultivating high-yield shrimp species, improving product standards, and promoting sustainable production through certification can enhance competitiveness. For leather, leather goods, and footwear sectors, the focus should be on prioritising environmental standards, securing accreditations, and adopting traceability technologies. For the engineering sector, establishing a competent authority for global certification, facilitating material supply, investing in vocational training, and promoting innovation are key steps. It is also important for all these sectors to be well linked to EU supply chains accessing retailers in EU nations. Having a product is not enough for export success, taking it to the consumers and providing them with sales-related services is equally important.

Bangladesh has solidified its prominence in the EU market primarily through its garment exports, showcasing the country's capability to be a significant player in international trade. However, despite the EU's vast market potential, Bangladesh's export presence outside the garment sector remains minimal. To truly capitalise on the market familiarity and trade preferences in the EU, Bangladesh must now urgently develop and effectively implement a medium-term strategy aimed at achieving comprehensive export diversification.

The author is an economist and Chairman of Research and Policy Integration for Development (RAPID). This article is an outgrowth of a research project supported by the Friedrich-Ebert-Stiftung (FES), Bangladesh. The views expressed in the article are author's own. m.a.razzaque@gmail.com

© 2026 - All Rights with The Financial Express