![]() Monetary steps have been taken but inflation is still surging in Bangladesh. Needless to say that bringing down the rising inflation is now the crying need of the country. How to combat it presupposes deeper analyses. Several strategies are needed, as triggers are many and multifarious. We overlook many minor causes that together make a major trigger. Little is known as to whether or not an in-depth investigation of all possible triggers has already been carried out. A synthesis of experts' opinions is required for designing appropriate strategies to cure the serious unhealthiness of the economy. At the same time, government's commitment and compliance with utmost steadfastness are essential.

Monetary steps have been taken but inflation is still surging in Bangladesh. Needless to say that bringing down the rising inflation is now the crying need of the country. How to combat it presupposes deeper analyses. Several strategies are needed, as triggers are many and multifarious. We overlook many minor causes that together make a major trigger. Little is known as to whether or not an in-depth investigation of all possible triggers has already been carried out. A synthesis of experts' opinions is required for designing appropriate strategies to cure the serious unhealthiness of the economy. At the same time, government's commitment and compliance with utmost steadfastness are essential.

To mitigate inflationary pressure a hasty drive in adopting measures is undesirable. Pursuing a strategic approach to resolving the problem entails inclusive and introspective considerations.

In the above-mentioned context, we can focus on some important considerations which must precede formulating right strategies to contain the worsening inflationary situation.

Monetary as well as Fiscal Policy and Monetary Aggregates: As already mentioned, the central bank already took some steps in order to contain inflation, but has been of no effect. Money supply is a basic and internal determinant of inflation level .Excessive issue of high-powered money is bound to accelerate money supply and result in an inflationary pressure. An analytical examination on a regular basis is crucial for optimal management of monetary aggregates. Fiscal initiatives include targeting reduction in public expenditure and deficit, raising tax-GDP ratio by reforming revenue governance based on collectors' adequate incentive system and specialized skills, digitally integrating overall revenue-collection system with an iron hand. Research and development relating to all courses of actions-policies, and strategies-- monetary and fiscal-- are a must.

Monetary as well as Fiscal Policy and Monetary Aggregates: As already mentioned, the central bank already took some steps in order to contain inflation, but has been of no effect. Money supply is a basic and internal determinant of inflation level .Excessive issue of high-powered money is bound to accelerate money supply and result in an inflationary pressure. An analytical examination on a regular basis is crucial for optimal management of monetary aggregates. Fiscal initiatives include targeting reduction in public expenditure and deficit, raising tax-GDP ratio by reforming revenue governance based on collectors' adequate incentive system and specialized skills, digitally integrating overall revenue-collection system with an iron hand. Research and development relating to all courses of actions-policies, and strategies-- monetary and fiscal-- are a must.

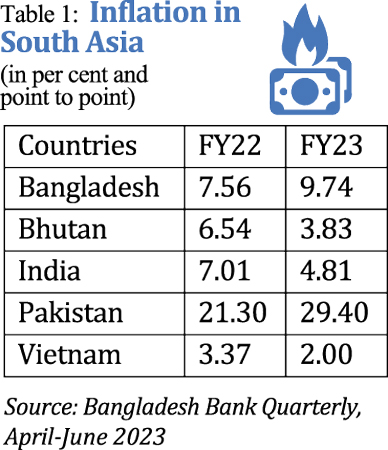

Learning from Other Countries' Inflation Management: Inflationary pressure affects the entire globe, but the quality of economic management differs from country to country. Can we not look at the rates of inflation in our neighbouring countries? The nearest one is India. As observed from Table 1, India's inflation is less than 5.0 per cent while ours is more than double of India's rate. Inflation of Vietnam and Bhutan is far lower. Do we contemplate over how India, Vietnam and Bhutan outperform us? We always claim to play a role model for the rest of the world. Why does our model fail to cure the economy from the disease of inflation, one of the most influential macro- indicators?

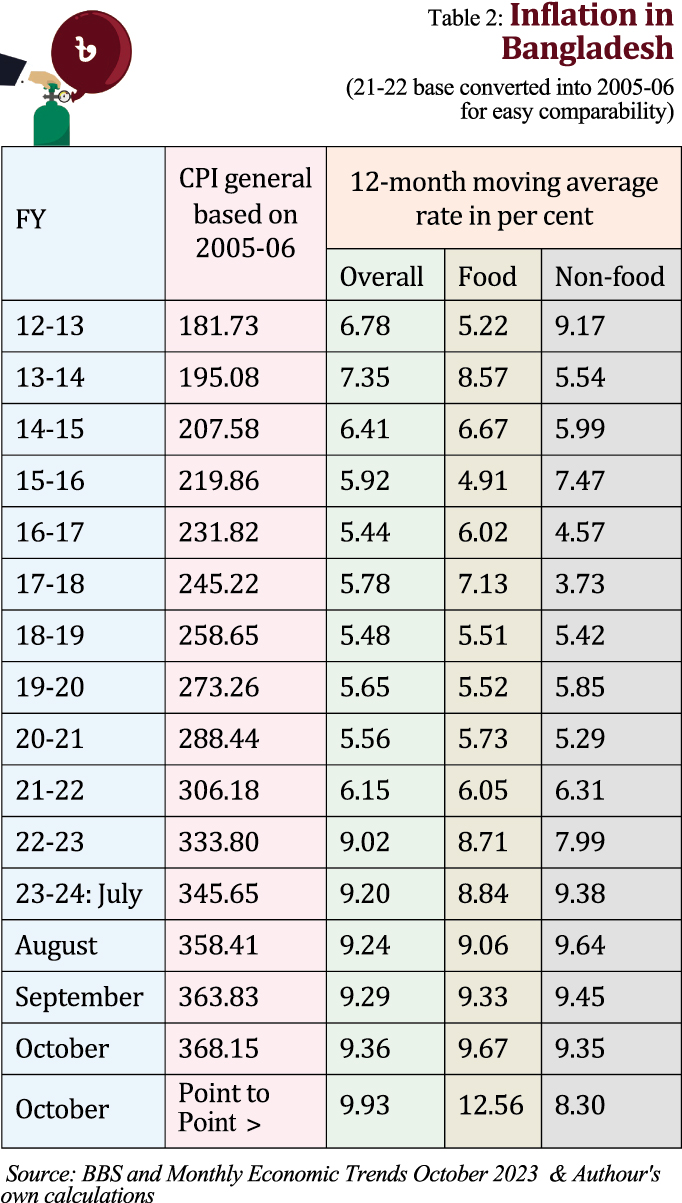

Insight into Our Inflation Trends: Table 2 shows that inflation in the country has been persistently increasing after the fiscal year 2020-21.Food inflation is greater than overall inflation most of the time ( 2012-13 to October 2023) while our agricultural sector registered spectacular growth despite some pitfalls. GDP growth rate has been positive and started increasing since 2020-21 though declined in FY2022-23.But total GDP has continued to grow. A combined analysis of production, demand, supply and trends of inflation can give new inputs for making strategies. Apart from this, we should go back to examine previous less-than-6.0- percent-inflation data ( from FY16 to FY 21) to discover the reasons for lower inflation.

Insight into Our Inflation Trends: Table 2 shows that inflation in the country has been persistently increasing after the fiscal year 2020-21.Food inflation is greater than overall inflation most of the time ( 2012-13 to October 2023) while our agricultural sector registered spectacular growth despite some pitfalls. GDP growth rate has been positive and started increasing since 2020-21 though declined in FY2022-23.But total GDP has continued to grow. A combined analysis of production, demand, supply and trends of inflation can give new inputs for making strategies. Apart from this, we should go back to examine previous less-than-6.0- percent-inflation data ( from FY16 to FY 21) to discover the reasons for lower inflation.

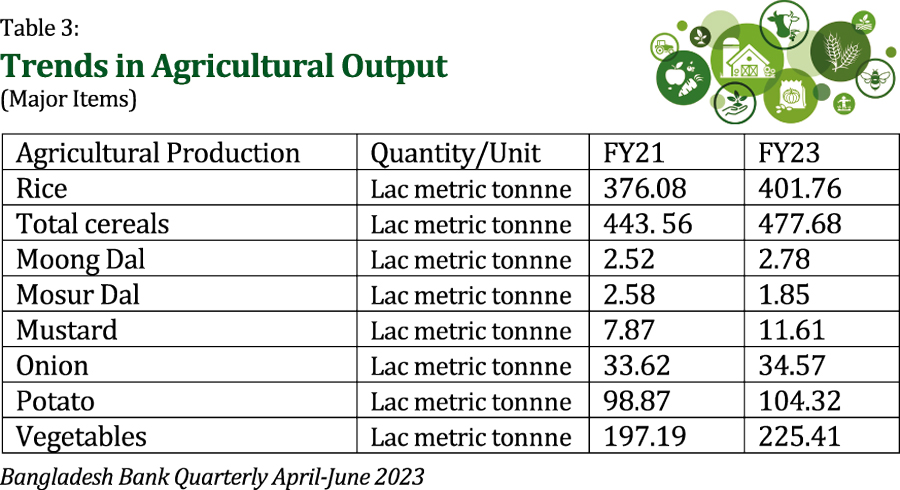

Demand Gap and Supply Side Analysis: We lack reliable data on our people's demand on a product-by-product basis, and inventory position and hence it is impossible to determine our demand gap from supply-side analysis. We should examine production in all sectors of the economy. Table 3 shows growth of agricultural production. But we have to determine how far the production level can meet demand .

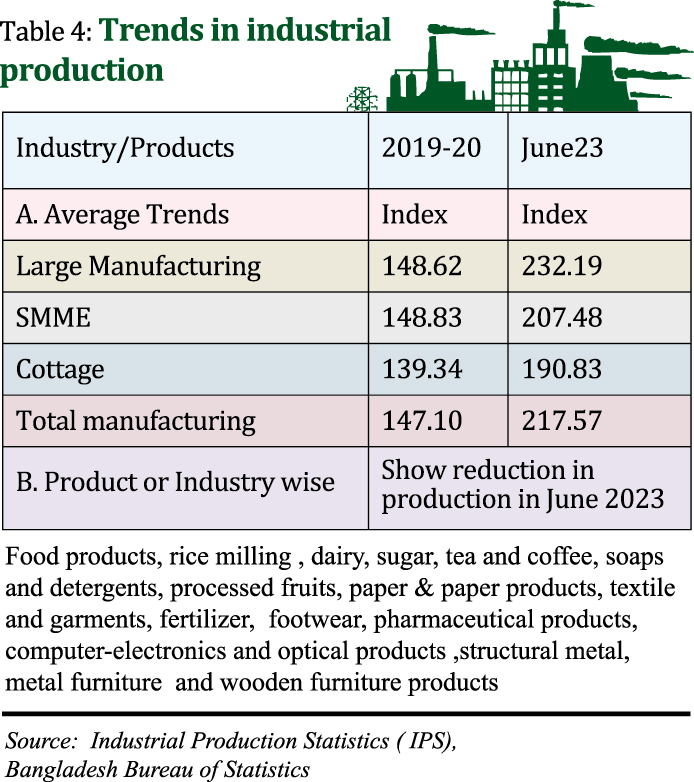

On the other hand, we observe from Table 4 that manufacturing ( overall) industry registers growth over the period of 3 years. This is also consistent with GDP-growth data. We need to find out how far the gap in industrial and agricultural production is responsible for rising inflation. We are also importing scarcity-marked goods such as green chili, onion, egg, sugar, soyabean oil etc. The authority has to monitor the market response to such steps.

Bangladesh Economic Review ( BER) 2023 reveals that production of fish, meat, milk and eggs had increased gradually till FY 22. But a sharp decline occurred in FY23, excepting fish which continued to rise in FY 23, too. Food-grain output is increasing but we cannot but import. Fortunately, import of food-grains is on the decrease. The BER 2023 also discloses that production volume in cottage, micro, small, medium and large manufacturing sectors constantly grew during the period after FY16 to FY23. Besides, GDP growth continued to be positive till FY23. Supply side is, therefore, grossly free from disruption. Demand-supply gap cannot be so big that it can be a cause of prevailing higher inflation rate.

Currency Depreciation: Bangladesh currency (BDT) experienced a too big depreciation against the US dollar in particular. Was the event of depreciation totally uncontrollable? Unfortunately, the deprecation is 13.8 percent (current rate is sure to escalate much more) while neighbouring country's (India) currency depreciated just 4.3 per cent. China, Malaysia and Indonesia also experienced depreciation much lower than that of Bangladesh. Do we lack prudent management of foreign exchange and trade? Are we not lagging behind many countries near us ? We should learn to enrich us.

Currency Depreciation: Bangladesh currency (BDT) experienced a too big depreciation against the US dollar in particular. Was the event of depreciation totally uncontrollable? Unfortunately, the deprecation is 13.8 percent (current rate is sure to escalate much more) while neighbouring country's (India) currency depreciated just 4.3 per cent. China, Malaysia and Indonesia also experienced depreciation much lower than that of Bangladesh. Do we lack prudent management of foreign exchange and trade? Are we not lagging behind many countries near us ? We should learn to enrich us.

Impact Analysis of Higher Import and Other Costs: When import cost, or input cost in particular, increases, it should be analysed by the government and private agencies, where required, jointly to calculate its exact impact on pricing of finished products-- both in further processing and direct trading. Supposedly, imported fuel-price hike has happened. Now it is necessary to determine how much cost of production in several industries will go up ,and also to set the new price of final products. A burning example is that transport operators, in most cases, raise the transport fare to a level more than the actual rise in fuel or other costs. Similarly, industry owners as well as traders reset the prices of their goods in the event of rise in inputs or other incidental costs. Thus, people as buyers are overtaxed by the impact of rise in cost of inputs or other elements of cost.

Our Severe Indebtedness and Waste: Flood of projects have changed the country's landscape, no doubt. Among them, there are many projects which have been abandoned and huge sunk of cost was wasted, and still wastage goes on unabated, giving no genuine production of goods and services. Do we account for them? It would continue as long as we are largely dependent on credits. Credit leakage by way of corruption and consumption creates inflationary pressure. An effective framework for accountability and transparency is not working at all .We have to contemplate over gradual reduction in credit-dependence as it has a natural tendency to be misused. We feel not concerned enough since the government as a sovereign debtor can borrow always. Imperceptibly, borrowing has become an addiction, wasting being our habit amidst insatiate wants.

Our Severe Indebtedness and Waste: Flood of projects have changed the country's landscape, no doubt. Among them, there are many projects which have been abandoned and huge sunk of cost was wasted, and still wastage goes on unabated, giving no genuine production of goods and services. Do we account for them? It would continue as long as we are largely dependent on credits. Credit leakage by way of corruption and consumption creates inflationary pressure. An effective framework for accountability and transparency is not working at all .We have to contemplate over gradual reduction in credit-dependence as it has a natural tendency to be misused. We feel not concerned enough since the government as a sovereign debtor can borrow always. Imperceptibly, borrowing has become an addiction, wasting being our habit amidst insatiate wants.

Legislation on Unethical business Practices and Strict Compliance: Indulged by government laxity, unscrupulous businessmen have been engaged in pricing manipulation and profiteering drive. Uncompromising crackdown on them leaves no other alternative. Authority's leniency and inactivity are a great favour to them.The government must commit to safeguarding public interest , not the interest and motives of the few damaging the economy and market discipline.New legislation to regulate the criminal activities of the syndicates ( here defined as a group of dishonest businesspeople and hence new act should insert the definition of 'Syndicate' to meet the demand of time) is very crucial. More important is strict compliance. Reforming all the existing laws, acts, policies and rules on marketing and price control is also necessary. Administered pricing and free-market mechanism are contradictory. Government intervention to fix maximum prices ( as per The Essential Articles Act 1953) sometimes may be misinterpreted to be siding with the interest of the syndicates ( actually behaving as cartels).

Amendment of Agricultural Marketing Rules 2021: Profit making is ethical and reasonable, but profiteering is totally an economic crime. The government framed the Agricultural Marketing Rules 2021 providing for a pricing method of agricultural produce. Unusually big profit margin has been officially approved for the middlemen like wholesalers and retailers engaged in the distribution channel. How far is it logical and ethical? As compared to primary producers, the middlemen together gain the largest share of profit margin as per the rules. It is to be pointed out that primary producers or farmers' annual frequency of sales turnover is single while middlemen enjoy multiple sales turnovers a year. However, we cannot term the rules as farmer-friendly and consumer - favouring .Rather, the pricing method has added fuel to the fire and it is also reflected in our market. Of course, there is a supply crisis of some goods to some extent, but the motive for unbridled profiteering and exploitation has been fuelled by the rules. Anarchy has vitiated the market. Steps should be taken forthwith to amend the rules in consultation with the stakeholders concerned.

Database on Production, Inventory, and Import: Comprehensive data base on production of goods, imports, and inventory level needs to be used to examine supply, demand and scarcity for properly evaluating and identifying inflationary situation. But in this analytical work, data insufficiency, inconsistencies, and periodical asymmetry are a major obstacle. There should be coordination among the data systems used by different government agencies like Bangladesh Bureau of Statistics (BBS), Bangladesh Bank, the Ministry of Finance and so on. There is another problem of frequent change of base year in economic reporting. Strategic fit is an important factor for fruitfulness of any strategy. Reliable and easily comparable data is a vital component of strategic management.

Business-Politics-Government Nexus: The government is people's representative but its practical role, activities and behaviour are indicative of its being largely aligned with private-sector interests. If the relationship is based on safeguarding public interest, that sounds better. Of course, the relationship of the government and the businesses must be based on mutual cooperation and benefit, not at the cost of public interest and people's welfare and rights. The nexus, if used otherwise, is sure to indulge illegal and unethical activities perpetrated by some influential members of the business community. This dimension should be given top priority to smooth other ways.

Credit Utilization: Banks and other financial institutions provide huge credits for production, trade and other purposes. Production credit, if not utilized for the designed purposes, would accelerate money supply without value addition. Credit utilization by both public and private sectors matters a lot . Do banks and other financial institutions strictly monitor credit utilization in borrowers' firms or businesses? Actually, lenders emphasize recovery rather than proper utilization of credits. In fact, utilization is not strictly supervised. This creates a big source of rising inflation. COVID- time incentive packages led to significant credit flows at a subsidized interest. Recovery performance of such credit as well as previous loan disbursements is poor. Default loans have been ballooning alarmingly. Diverted funds might have been largely spent for unproductive purposes.

It is true that first COVID impacts and then Russia-Ukraine war contributed to the rise in inflation rate. But they are not the exclusive triggers. Intentionally or unintentionally, we tend to describe the Russia-Ukraine war as major catalyst for inflationary heat. Can we defy that failures as well as imprudent, and trivial behaviours at the government , policymaker, and businessman levels continue to contribute to the increasing trend in inflation ? However, we hope to get relief from oppressive inflation soon first by the grace of new agricultural crops, and then by government's compatible and farsighted strategies.

Haradhan Sarker, PhD, is an ex-Financial Analyst, Sonali Bank, and retired Professor of Management.

sarkerh1958@gmail.com

© 2026 - All Rights with The Financial Express