Mohammad Abu Yusuf and AKM Sohel | November 26, 2023 00:00:00

An elderly woman sits on the eroded river bank in Munshiganj district, Bangladesh. The photo was taken on September 19, 2022. — Xinhua

An elderly woman sits on the eroded river bank in Munshiganj district, Bangladesh. The photo was taken on September 19, 2022. — Xinhua ![]() Bangladesh’s current contribution to global greenhouse gas (GHG) emissions is about 0.4 per cent of total global emissions. But it is one of the most endangered countries in the world due to global warming and climate change. Bangladesh ranks 7th in terms of the most climate-vulnerable countries. Recent findings suggest Bangladesh is facing even more problems from sea level rise, drought, heating, cyclones and floods. The World Bank (2022) observes that: about 13.3 million people in Bangladesh could become internal climate migrants due to climate impacts on agriculture, water scarcity, and rising sea levels, with higher impacts on women by 2050. In case of severe flooding, GDP could fall by as much as 9 per cent. Average tropical cyclones cost Bangladesh about $1 billion annually.

Bangladesh’s current contribution to global greenhouse gas (GHG) emissions is about 0.4 per cent of total global emissions. But it is one of the most endangered countries in the world due to global warming and climate change. Bangladesh ranks 7th in terms of the most climate-vulnerable countries. Recent findings suggest Bangladesh is facing even more problems from sea level rise, drought, heating, cyclones and floods. The World Bank (2022) observes that: about 13.3 million people in Bangladesh could become internal climate migrants due to climate impacts on agriculture, water scarcity, and rising sea levels, with higher impacts on women by 2050. In case of severe flooding, GDP could fall by as much as 9 per cent. Average tropical cyclones cost Bangladesh about $1 billion annually.

By 2050, one-third of agricultural GDP may be lost due to climate variability and extreme events. According to the study titled “Impacts of climate change on health in Bangladesh” (2023), around 1430 aged 65 and up, died between 2017 and 2021 from heat-related causes accelerated due to climate change. This is 148 per cent higher than what it was between 2000 and 2004. The study also reveals that health risk to millions of people has been on the rise in Bangladesh. This is an impact of climate change. Apart from heat waves, climate change has also other effects including droughts (there was an average of 1.7 months of drought in the 2012-2021 period, which was 0.3 months on average between 1951-1960), floods, and cyclones. These are negatively impacting food security. The study finds that food insecurity in Bangladesh is expected to rise by 7.4 per cent between 2041 and 2060. It has also been found that extreme weather events increased by 46 per cent in Bangladesh since the year 2000. Dengue outbreaks in Bangladesh during 2022-23 were found linked to high rainfall and temperature in Dhaka. Overall, climate change has emerged as a big threat to our economy. It is estimated that Bangladesh incurs a loss of about 1 per cent to 2 per cent of its GDP due to climate change (FRS, Ahmed, 2023).

Only 2 per cent of the climate finance generated so far through funds created under UNFCCC (mainly GCF), and the remaining 98 per cent are being distributed mainly through bilaterally and the private sector. It was decided in COP16 (in 2010) that developed countries will generate an amount of $100 billion annually from 2020. Against this promise, climate finance generated in 2020 stands at about $80 bn (OECD). Oxfam downplayed the estimated figure, claiming the amount to be $20 billion. About 53 per cent of this amount is given as loans and in most cases, the interest rates on these loans are similar to that of ordinary investible loans. Oxfam mentions that climate finance — if continued in its current forms (mainly loans, a small amount is in grants) — will make countries more vulnerable to being stuck in a debt crisis.

Moreover, it is feared that the global temperature will increase by 2.8 degrees Celsius (2°C above pre-industrial level even if the initiatives to reduce temperature between 1.5°C to 2°C above pre-industrial level) are implemented. That will result in the necessity of more funds for adaptation. As Bangladeshis are one of the major victims of climate change despite not being a major emitter of GHGs, we need grants and very concessionary climate finance instead of ordinary loans.

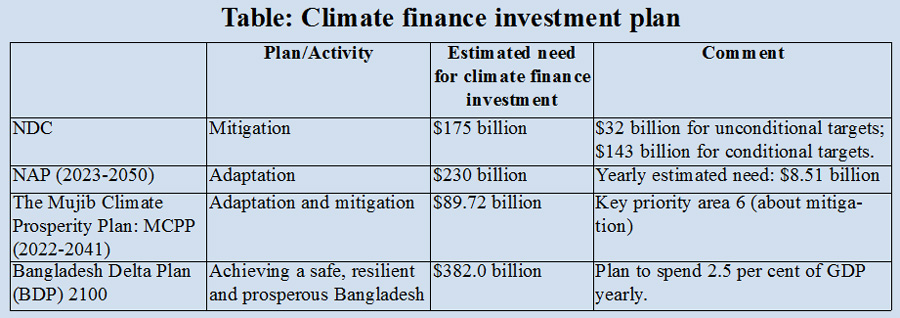

Bangladesh developed climate policies, strategies, and a climate fiscal framework to address climate change. The climate change plans/activities stated in policy documents clearly indicate that Bangladesh needs huge climate investment to address the adverse consequences of climate change and mitigate GHG emissions. The climate finance needs of the country have been estimated in different documents. These are:

Climate finance needs of Bangladesh

The table presents the investment need for climate finance.

The estimated climate needs are huge for Bangladesh as is evidenced in the table. About $8.5 billion is needed yearly to fund the adaptation projects only identified in the NAP 2023-2050. More financing is needed to finance NDCs, MCPP and other climate-relevant activities. The required amount for climate change investments is much higher than Bangladesh’s total allocation for climate change (e.g., in 2023-24, Bangladesh’s climate finance tracked amount is Tk 37,051.94 crore (about $3.7 billion). That means there is a big gap in climate financing.

Bangladesh’s climate change funding is predominantly from domestic sources, especially from government sources such as the annual national budget, Bangladesh Climate Change Trust Fund (BCCTF) and Refinancing Scheme of Bangladesh Bank for Renewable Energy and Green Financing. Till 2022-23, a total amount of Tk 3919 crore was allocated to the Climate Change Trust fund. The yearly allocation for climate causes has been increasing each year. However, as stated in the previous paragraph, more funding is needed from international as well as domestic sources to narrow the climate financing gap. Currently, Bangladesh accesses climate finance from global funds, including the Green Climate Fund (GCF), LDCF, MDBs and bilateral sources. Among these, most of the funds or projects are funded by the GCF funds. Since 2014, Bangladesh received $ 503.16 million to implement 08 climate projects from GCF and other development partners. In 2022-2023, Bangladesh received $1 billion SDR as budget support from the IMF under its Resilience and Sustainability Facility (RSF) fund. The RSF, supported by the convening power of the IMF, can act as a catalyst by bringing together governments, MDBs and the private sector to generate private sector funds for climate change purposes. It is pertinent to mention that the lack of investment ratings (grade) of most LDC/developing countries by rating agencies is one of the biggest barriers to having climate investment from global investors and the private sector.

Bangladesh’s climate change funding is predominantly from domestic sources, especially from government sources such as the annual national budget, Bangladesh Climate Change Trust Fund (BCCTF) and Refinancing Scheme of Bangladesh Bank for Renewable Energy and Green Financing. Till 2022-23, a total amount of Tk 3919 crore was allocated to the Climate Change Trust fund. The yearly allocation for climate causes has been increasing each year. However, as stated in the previous paragraph, more funding is needed from international as well as domestic sources to narrow the climate financing gap. Currently, Bangladesh accesses climate finance from global funds, including the Green Climate Fund (GCF), LDCF, MDBs and bilateral sources. Among these, most of the funds or projects are funded by the GCF funds. Since 2014, Bangladesh received $ 503.16 million to implement 08 climate projects from GCF and other development partners. In 2022-2023, Bangladesh received $1 billion SDR as budget support from the IMF under its Resilience and Sustainability Facility (RSF) fund. The RSF, supported by the convening power of the IMF, can act as a catalyst by bringing together governments, MDBs and the private sector to generate private sector funds for climate change purposes. It is pertinent to mention that the lack of investment ratings (grade) of most LDC/developing countries by rating agencies is one of the biggest barriers to having climate investment from global investors and the private sector.

The GCF finances through accredited entities. However, generating adaptation finance from the GCF is time-consuming#. Adaptation projects usually are not profitable (not bankable). So public financing and internationally sourced finance are needed in adaptation. In developing adaptation project proposals to access funds from the GCF, it is necessary to prove scientifically (link) that the impacts (or consequences) for which climate finance is sought are caused by climate change. In other words, climate rationale for adaptation projects (i.e., risk of climate-related impacts resulting from the interaction of climate-related hazards) is imperative.

Needed initiatives to scale up climate finance:

It is known that the amount of climate finance generated from international climate funds is limited. Accessing funds from these international funds is also complex and time-consuming. Besides, the multilateral development partners also have dedicated climate funds including the Climate Investment Fund (CIF) by the World Bank and the Climate Change Fund (CCF) by ADB. We need to attract funds from multilateral development banks and bilateral sources. For this, the Economic Relations Division (ERD) plays a vital role in both coordinating and catalysing climate finance from external sources into the country. It is pertinent to mention that as a contracting party to the Paris Agreement, we need to track climate financing from external sources into the country to analyse the utilisation of these funds in terms of location and sector, and components for more effective utilisation of scarce resources.

Given the limited amount of climate funds from public sources, private finance is key to addressing climate change as public budgets are limited due to competing priorities. De-risking of finance increases the private sector’s risk appetite for climate investments. Blended finance is useful to de-risk these investments, the objective being to encourage greater private-sector participation. This is especially applicable in the case of adaptation projects because adaptation projects often lack revenue streams that the private sector is interested in. Currently, the development partners emphasise private-sector engagement. We should encourage financing through non-bank financial institutions (NBFIs) like IDCOL that are working for climate action and create an enabling environment for them. On the one hand, this will channel more external finance towards climate action, strengthen the NBFIs and encourage resource mobilisation from the private sector towards a lasting partnership.

An equity, concessional loan, grant or guarantee to cover a set amount of first loss in the event of losses can also act as an instrument for de-risking (also known as risk sharing tools) of private investment. Such grants or guarantees improve the private investor’s risk-return profile and act as catalytic first-loss capital (CFLC). Public sector (national governments), multilateral development banks (MDBs), and international climate funds have a crucial role in de-risking climate, especially, adaptation investments. Development finance institutions (DFIs) such as the World Bank, philanthropists and donors have a higher tolerance for risks, and they can provide first-loss guarantees to absorb risk in sectors that are yet to reach commercial scale. For countries like Bangladesh, climate change adaptation is necessary for building a more climate-resilient economy. The Adaptation Gap Report of the UNEP estimates that costs to adapt in developing countries are five to ten times greater than current public adaptation finance flows.

Blended finance includes a mixture of commercial market-based finance, concessional donor funds, guarantees, subordinated debt and performance-based incentives, in combination with advisory and technical assistance. Blended finance mitigates specific investment risks for undertaking projects that otherwise cannot proceed solely with commercial funding. The significant role of blended finance can be realised from India’s GreenCell Express Private Ltd case: A blended financing package with Asian Development Bank (ADB) assistance will enable India’s GreenCell Express Private Ltd to develop 255 electric battery-powered buses (e-buses/green transport). The package, put together by ADB, includes an ADB loan of $20.5 million (in equivalent Indian rupee), ADB’s administration of a $14 million loan from the Clean Technology Fund (CTF), grants worth $325,000 from the CTF and $5.2 million from the Climate Innovation and Development Fund (CIDF) supported by Goldman Sachs and Bloomberg Philanthropies.

Apart from these sources, other innovative financing mechanisms are taking shape gradually. For example, the G7 and V20 are working together on the Global Shield Against Climate Risk. Another alternative for debt-distressed countries like Afghanistan, Lao PDR, Kiribati etc. is debt-for-climate swaps. In debt-for-climate swaps, creditors grant debt relief in return for a government commitment to, say, decarbonise the economy, invest in climate-resilient infrastructure, or protect biodiversity. Debt-for-climate swaps can be a solution to simultaneously reduce sovereign debt burdens and increase financing to scale up investments in climate mitigation and adaptation projects. Debt-for-climate swaps could be superior to conditional grants when they can be structured in a way that makes the climate commitment de facto senior to debt service. This instrument could be useful to increase fiscal space for climate investment when grants or more comprehensive debt relief are just not on the table.

Skills development and capacity building of national and local actors (including public officials) in the field of climate finance is needed to develop project proposals (incorporating theory of change for projects, climate rationale of projects, determination of NPV, IRR and the impact of the proposed project in addressing climate change as well as the overall economy of the country) for accessing climate finance from the GCF, and other international funds and sources. Continued efforts are also necessary to access funds from UN organisations, Multilateral Development Banks (MDBs) and bilateral development partners. The Sharm el-Sheikh Implementation Plan (COP 27, 2022, paragraph 20) highlights the role of the LDCF and SCCF in supporting actions by developing countries to address climate change. Developed countries need to contribute more to these funds.

Climate policies and finance are complementary (IMF, 2022)#. It is necessary to establish the right climate policies, including price signalling (carbon pricing) to scale up climate finance. Better policies incentivise private investment. Carbon markets generate private finance although this is not a preferred option at the moment for Bangladesh given our limited GHG emissions.

Bangladesh also needs to have an updated climate-related database. For instance, the GCF adaptation projects need to demonstrate the need for the proposed project, by providing among others, historical climate data (say 30 years of observed variability, + events), projected climate data, future risks and proposed adaptation activities.

Results-based climate finance (RBCF) can be used to incentivise climate action and help achieve Nationally Determined Contributions (NDCs) of Bangladesh. RBCF hinges on achieving pre-agreed results, thereby also increasing the likelihood that a project will be successful. These payments could: support the restoration of mangroves by generating Emission Reduction Credits and accelerate the phase-out of coal-fired power plants by monetising (such monetisation helps bring private finance), in the carbon markets.

Issuance of local currency green bonds may be considered for climate financing. Such local currency bond markets are in place in South Africa and Nigeria. For this bond to be issued, regulatory and institutional frameworks are needed.

ADB and private funds:

The role of ADB is commendable in generating private funds for climate change. Asian Development Bank’s (ADB) Private Sector Operations Department (PSOD) is engaged in project management. ADB has philanthropic funds to support climate causes. Climate Innovation and Development Fund (CIDF) is ADB’s first private sector philanthropic fund with commitments to provide grants by Goldman Sachs and Bloomberg Philanthropies. This fund was launched in February 2022 with $25 million in grants from the said private institutions to support sustainable low-carbon development in South Asia and Southeast Asia through investments in innovative private sector projects. These projects support renewable power development; energy efficiency, storage, and management; carbon capture and storage; sustainable transport; climate-resilient agriculture, forestry, land, and water use and waste management; by providing concessional finance to reduce risks, CIDF is aiming to leverage up to $500 million in project finance from the private sector. (p.47). (ADB, May 2023, p. 27). Bangladesh may consider forging a strengthened relationship with ADB to access more climate finance from the private sector. In 2022, the Asian Development Bank (ADB) committed $7.1 billion to climate finance ($4.3 billion for mitigation and $2.8 billion for adaptation). ADB also mobilised $548 million in climate finance from the private sector.

MDBs could be another vital source to support green infrastructure projects by increasing their capital base and bringing changes in their approaches to risk appetite via partnerships with the private sector. MDBs could make greater use of equity finance (currently, this is only about 1.8 per cent of their commitments to climate finance in emerging markets and developing economies). In 2022, $60.7 billion of MDB climate finance (63 per cent for mitigation, 37 per cent for adaptation) was allocated for low-income and middle-income economies. The amount of mobilised private finance stood at $16.9 billion. In addition to its own equity investment, ADB will also administer $10 million from the Australian Climate Finance Partnership Trust Fund, a concessional blended financing facility funded by the Government of Australia to catalyse private sector investments in climate projects in the Pacific and Southeast Asia.

As mitigation is the best form of adaptation and there is a limit to adaptation, Bangladesh may also consider ways to reduce emissions from major emitting sectors. Adoption of clean technology, an increase in the use of renewable energy and non-fossil fuel in the energy mix and a reduction of water use will reduce emissions. Bangladesh has undertaken a project where the “integrated rice advisory system model (IRAS)” is being piloted by the Department of Agricultural Extension (DAE) for use in agriculture. Under this model, the irrigation map of NASA will be used to provide forecasting to the farmers about the amount of water needed for irrigation in a given time. This model of irrigation forecasting is expected to result in a reduction of 30 per cent in water usage and 45 per cent in fuel usage. It will also be possible to reduce about 3 lakh tonnes of carbon emissions each year with the adoption of this forecasting model.

Initiatives taken so far to address climate change:

In addition to budgetary provisions for climate change by the government of Bangladesh, Bangladesh Bank (BB) has launched a number of refinance schemes at lower rates of interest such as Technology Development Fund (TDF) (Tk 10 billion), Green Transformation Fund (GTF) (Tk50 billion, $200 million, €200 million), Refinance Scheme for Green Products/Projects/Initiatives (Tk 4 billion) to enhance investment in green and sustainable finance.

With the aim of encouraging the issuance of green bonds, BB already issued a Policy on Green Bond Financing for Banks & Financial Institutions (2022). In this guideline, BB prescribes eighty-eight activities against which banks and financial institutions (FI) can issue green finance. The green bond taxonomy issued by the BB specifies green investment priorities that could be supported by the proceeds of a green bond.

Necessary laws, policies, strategies and action plans such as the Climate Change Trust Act 2010, Bangladesh Climate Change Strategy and Action Plan (BCCSAP) 2009, Nationally Determined Contributions (NDCs) 2021, Mujib Climate Prosperity Plan (MCPP), National Adaptation Plan of Bangladesh (2023-2050), Power System Master Plan 2016 (PSMP) are adopted. Steps have been taken for climate-smart agriculture (e.g., smart, and renewable-energy-powered irrigation, renewable energy cold storage, climate-resilient livestock feed, salinity tolerant variety etc.). In order to reduce the use of fossil fuels by facilitating the country’s transition to clean energy, Bangladesh has made steady progress in renewable energy (RE) sector development. Bangladesh has a target to produce 10 per cent of total power generation from renewable sources by 2030#. Currently, Bangladesh’s installed capacity of RE is 1194.7 MW (solar: 960.71, hydro: 230, wind: 2.9, biogas to electricity: 0.69; biomass to electricity: 0.4 MW) MW (http://www.renewableenergy.gov.bd/ 28 Oct 2023). The non-bank financial institution IDCOL (established by GoB) introduced many refinancing schemes and programs to diversify the renewable energy installations in biogas and biomass-based power and energy generation, solar irrigation and solar micro and mini-grid areas etc. As part of capacity building, 15 city corporation and municipality officials are trained on climate change project proposal development. Fifteen (15) officials have completed climate and sustainable finance-related courses at the Frankfurt School Autumn Academy. An interactive web portal for exploring international climate finance opportunities is developed by the ERD.

Bangladesh has led the way in adaptation and disaster risk management. Over the past 50 years, the country has reduced cyclone-related deaths 100-fold. Bangladesh’s success in promoting locally-led adaptation (LLA) by both the government and the NGOs (examples floating vegetable garden, community-based natural resource management (CBNRM), a climate-resilient migrant-friendly town through LLA) is also highlighted in the global climate discussion. But with ever-increasing climate risks, further adaptation efforts are vital, and the generation of additional climate finance from external and domestic sources is needed to undertake the needed adaptations. To conclude, the enhancement of the capacity to monitor climate finance received, track how it is being spent and assess overall outcomes is of paramount importance for transparency and accountability of climate finance.

Dr Mohammad Abu Yusuf is Additional Secretary, Finance Division, Ministry of Finance, Government of Bangladesh. ma_yusuf@hotmail.com

AKM Sohel is Joint Secretary, Economic Relations Division, Ministry of Finance, Government of Bangladesh.

© 2026 - All Rights with The Financial Express