![]() The 1992 Cricket World Cup saw a novel stratagem, as the powerful Mark Greatbatch was promoted to opening to disrupt the bowling attack and give birth to the idea of pinch-hitting, destroying the opponent bowlers, rather than the usual taking-your-time-out in the middle. The Cricket World Cup 1996 followed the suit with the maestro, Sanath Jayasuriya. Moments like this redefined the history. Made us look from a new angle. Made us think from a new angle. Gilchrist, Afridi, and Sehwag made slogging very common. Finance had its fair share of innovation and spotlight innumerable times. In the last 4 to 5 years, fintech led to the financial renaissance. Even the person who has the zero clue about fintech knows that this is the rendezvous of finance and technology. Plus it is the mélange of even cooler buzzwords like blockchain, machine learning, artificial intelligence, crypto, and so on. Chatbots like ChatGPT or Bird, using LLM (large language models) also became immensely popular in these last 2 years, which is no surprise, given their vast power and broad applicability.

The 1992 Cricket World Cup saw a novel stratagem, as the powerful Mark Greatbatch was promoted to opening to disrupt the bowling attack and give birth to the idea of pinch-hitting, destroying the opponent bowlers, rather than the usual taking-your-time-out in the middle. The Cricket World Cup 1996 followed the suit with the maestro, Sanath Jayasuriya. Moments like this redefined the history. Made us look from a new angle. Made us think from a new angle. Gilchrist, Afridi, and Sehwag made slogging very common. Finance had its fair share of innovation and spotlight innumerable times. In the last 4 to 5 years, fintech led to the financial renaissance. Even the person who has the zero clue about fintech knows that this is the rendezvous of finance and technology. Plus it is the mélange of even cooler buzzwords like blockchain, machine learning, artificial intelligence, crypto, and so on. Chatbots like ChatGPT or Bird, using LLM (large language models) also became immensely popular in these last 2 years, which is no surprise, given their vast power and broad applicability.

Every knowledge hub keeps on innovating perpetually more or less, but the root always stays the same. Well, that is what we thought. In the idyllic scenario, that concept made the authors add a completely different section to the finance books, which is why we are saying fintech is a disruptive technology. Who thought that the stereotypical nerdy finance could act as an inn to the enthusiastic tenant of technology? There have been times when people thought it to be balderdash, or it won't last long but now it has become a must, it has catapulted itself from the fringes to the centre. It has branched out to give birth to not only new leaves but overall, a new forest.

Every knowledge hub keeps on innovating perpetually more or less, but the root always stays the same. Well, that is what we thought. In the idyllic scenario, that concept made the authors add a completely different section to the finance books, which is why we are saying fintech is a disruptive technology. Who thought that the stereotypical nerdy finance could act as an inn to the enthusiastic tenant of technology? There have been times when people thought it to be balderdash, or it won't last long but now it has become a must, it has catapulted itself from the fringes to the centre. It has branched out to give birth to not only new leaves but overall, a new forest.

A very common notion is to somehow play the fault-finding game and come to the conclusion that our country is not good for anything (hint: 2023 Cricket World Cup). In terms of fintech we emerged as an exciting market so far. Fintech in Bangladesh is thriving on the back of digital payments, mostly mobile financial services and the NBFIs (non-bank financial institutions). The largest segment of the fintech market in Bangladesh is digital payments, with a projected total transaction value of US$11.10 billion in 2023, accounting for 94 per cent of the total market.  While the global fintech market is expected to grow at a compound annual growth rate (CAGR) of 16.8 per cent from 2023 to 2032, reaching a value of US$ 917.17 billion by 2032, Bangladesh is projected to reach US$ 11.92 billion in 2023, growing at a CAGR of 18.78 per cent from 2023 to 2027. These stats show that even though the growth has been fast and furious, Bangladesh being Bangladesh has not been lagging that behind. Yes, according to a report by the International Monetary Fund, Bangladesh ranks 72nd out of 189 countries in terms of the digital financial inclusion index, which measures the extent and quality of digital access to and use of formal financial services. Compared to other countries, Bangladesh has a relatively low level of digital financial inclusion, but also a high potential for growth and innovation. But still, it is adapting to the new normal, where even the pandemic played its role. Ergo, our country is riding well the wave of this paradigm shift. Well, other than one key arena. Let me not traipse anymore around the topic, and just say it. Stocks. Share market. Or, capital market.

While the global fintech market is expected to grow at a compound annual growth rate (CAGR) of 16.8 per cent from 2023 to 2032, reaching a value of US$ 917.17 billion by 2032, Bangladesh is projected to reach US$ 11.92 billion in 2023, growing at a CAGR of 18.78 per cent from 2023 to 2027. These stats show that even though the growth has been fast and furious, Bangladesh being Bangladesh has not been lagging that behind. Yes, according to a report by the International Monetary Fund, Bangladesh ranks 72nd out of 189 countries in terms of the digital financial inclusion index, which measures the extent and quality of digital access to and use of formal financial services. Compared to other countries, Bangladesh has a relatively low level of digital financial inclusion, but also a high potential for growth and innovation. But still, it is adapting to the new normal, where even the pandemic played its role. Ergo, our country is riding well the wave of this paradigm shift. Well, other than one key arena. Let me not traipse anymore around the topic, and just say it. Stocks. Share market. Or, capital market.

Yes, this remains as that one place where all the voodoo seems to work. Where the big players seem like shamans with their magic. Mass people still tie this to the place where a scam happens. Everyone even remotely tied to the capital market is either seen as a hero (who can hand over some items and save the investor in particular) or a villain (who went there solely to be a Rainman in the scam of making money) depending on perspective. These beliefs, well, are constructed on the bulwark of the massive market crashes and the tears and suffering of the investors, true. Fintech being like that disruption with its AI, ML and all, why can't we disrupt this to bring a smile on the face of the investors? Can't we?

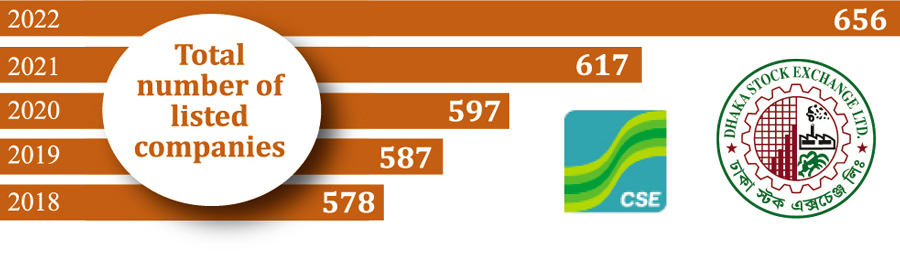

Let's hold this thought. Let's take a look at how the dreaded stock market is doing. Time for some stat sprinkling. The total number of trading rights entitlement certificate (TREC)-holder companies under the Dhaka Stock Exchange is 309, of which, 270 are in operation. Currently, there are 1.9 million (19 lakh) Beneficiary Owner (BO) accounts that are required for stock market trading in the country. Approximately 60 per cent of the total citizens in the USA participate in the stock market, whereas we are barely 3.0 per cent. The total number of actively operating dealers and brokers is 258 and 290 respectively. Now, let us see, how the listed securities are increasing in number with time. Yes, we aren't like our neighbouring superpower which makes certain multinational companies be listed in their stock exchange, and the quality of the listed companies is also in question from time to time (as per the stereotype), but the growth should mean something, right? At least it shows that the playing field is ever-expanding!

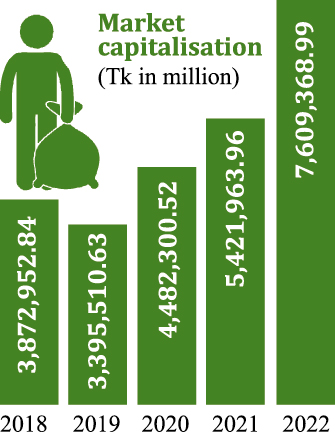

If we look at the market cap, this also shows a tad bit of promise with somewhat steady growth. Then again, these two stats are not all that can be shown, obviously, and people can bring a hundred other ratios and graphs to show the opposite, but let's not lose the sight here.

Artificial Intelligence has the dexterity to create investment recommendations, conduct intricate simulations, and scenario analysis, and meticulously monitor a spectrum of investment parameters. Businesses use AI for a plethora of tasks, including financial planning, supply chain management, accounting tests, and risk assessments. AI may be integrated into family offices' tech stacks to save expenses and boost productivity. After all, developing client connections, boosting innovation, and growing market share may be more worthwhile uses of an adviser's time than, say, the mundane endeavour of data modeling. This increases productivity without necessarily replacing human labour as AI works as the catalyst. Family offices reallocating their human capital are thus envisaged as a discerning maneuver to where it adds the greatest value by utilising AI.

Robo advisers or robot traders are here, which can be used to automate the investment based on the algorithm. Algorithmic trading or Algotrading is the avant-garde form of trading that has been executing the trades at such a speed that compared to traditional methods seems like Usain Bolt. This disruption not only altered the market liquidity but also orchestrated an opus of a far-improved and better price efficiency. The different LLMs like ChatGPT are far from perfect for now, their rapid expansion in terms of plugins (like Bing.ai) hints at the fact that their development will only accelerate in the months and years ahead. At the epicentre of the current AI hype cycle, everyone is nibbling at getting an edge in this fast-developing sector. How the investment industry or portfolio management will shape up owing to them is tough to anticipate accurately, but one thing is for sure, the playbook has completely changed. Blockchain technology, mostly being hand in gloves with the realm of crypto, has now outgrown its safe childhood home of cryptocurrency and moved out to the exciting world of trading. This is the Optimus Prime, spearheading in standing sentinel against scams and frauds which acts as a fortification in the capital market. All this disruption for now is co-piloting, but soon it will be autopilots, and what would happen to the brokers and dealers? The answer is simple. Even though auto cars are here along with manual cars, even though airplanes have autopilots, we still have someone at the helm. The brokers and dealers should update themselves with the wheel of time, because or else, soon they will see themselves being obsolete by some hungrier person waltzing along with the fintech to harness its power to his will and benefit.

But in our country, the investors are still facing the miasma and have that preconceived notion of the capital market being duplicitous. Then what is the missing link here?

First, let's take a look at the investors here. There are some common issues at play here. Mass investors fall in love with a certain stock. They want to show it a good time, wine and dine with it, get unhealthy attachment, and cannot get rid of it when it is time. The opposite of this is the panic sell or buy, where the investor wants to outsmart the market or time the market and beat it. Going against the current or riding the wave must not be at the expense of your investment! The other one is the stubbornness, chasing the loss. Just like a toxic partner, this loss chasing is like 'simping' as it eats away your time and investments. But on top of the list of problems from the investor's side is the knowledge or the lack thereof! People would go to great lengths and would make painstaking efforts to follow a rumour or use multiple expert opinions without actually analysing or taking the time to study what they are doing. Because it is very easy to blame everything on fate, government, and authority, and it is also easy to follow the herd mentality, by going for rumours, but when it comes to study and analyse or research, nuh-uh. Too much work can't be done. Just like a certain cricket team who didn't prepare well enough before the one global event that comes after every 4 years.

The premier bourse of this country, the Dhaka Stock Exchange, along with the Chittagong Stock Exchange has been conducting research works and awareness programmes, training even students and anyone willing to learn. Bangladesh Securities and Exchange Commission (BSEC), DSE, CSE, everyone is going for synergies. The red flag is waving where the investors are urged not to invest blindly, and all the signals and warnings are put in the right places. The regulatory affairs, in terms of monitoring, surveillance, financial reporting compliance, investor complaints, and listing of companies, all seem to be the cogs of a well-oiled machine. But still is that enough? No! What about the investors' trust? We can keep on pointing fingers at the lack of education in terms of investors, true, but what about the trust that has been severely broken from time to time? Other than your regular market playing incidents, there have been so many instances of trade being halted or the IT section showing its incompetence. It raises the question of even if fintech is integrated like that of the developed countries, and we keep on blaming investors and other stakeholders for not being educated enough.

This is the dark side of the moon. In the pas de deux between investors and regulators, this blame game of pointing will always be there. Finding the sweet spot of ensuring cybersecurity with regulatory compliance being vigilante, while allowing the market to breathe on its own, and see that the economy doesn't affect the market negatively, and ensuring that investors are aware, will in a nutshell, see the true Kafka-esque metamorphosis that fintech ought to do to the capital market.

Then again, we can always be hopeful. Even after our disastrous performance in the Cricket World Cup, and all of our promises of not watching cricket ever again, we all know, brazenly we will still watch the next matches and the next series. All because of hope. So, the capital market and fintech can expect some hope as well, no?

The writer is an engineer turned finance enthusiast.

galibnakibrahman@gmail.com

© 2026 - All Rights with The Financial Express