The numbers tell the story. In 2023, U.S. imports from China fell by nearly 25 per cent compared to their peak. European investment in Chinese manufacturing has plummeted to levels not seen since the early 2000s. The CHIPS Act's US$52.7 billion investment in domestic semiconductor production, coupled with the EU's Net Zero Industry Act and America's Inflation Reduction Act, represents more than just industrial policy - it's a fundamental reimagining of global supply chains.

But as the West races to "de-risk" its economic relationships with China, a crucial question emerges: who will fill the vacuum? While Vietnam and Mexico have captured headlines as alternative manufacturing hubs, an unlikely contender is emerging from South Asia. Bangladesh, long pigeonholed as merely a textile powerhouse, should position itself to become a key beneficiary of this great economic decoupling.

When Sheikh Hasina's Awami League consolidated power in 2009, they introduced what they called a "Development First" paradigm - a distinctive blend of state-led capitalism with authoritarian characteristics. The theory was seductively simple: political stability, even at the cost of democratic freedoms, would create the conditions for rapid economic growth. This "Bangladesh Model" drew inspiration from both the East Asian developmental states and China's market authoritarianism, but with a crucial difference - it relied heavily on a single-party-patronage network rather than a professional bureaucracy.

The model delivered impressive headlines: GDP growth averaged over 6.0 per cent annually, poverty rates halved, and Bangladesh's ready-made garment sector became a global powerhouse. But beneath these achievements lay structural weaknesses that became increasingly apparent during Hasina's third and fourth terms. This is made even worse as we get to know that the majority of the numbers may have been cooked up.

First was the paradox of infrastructure. The government's signature megaprojects - from the Padma Bridge to the Dhaka Metro Rail - while impressive in scale, suffered from what economists call the "white-elephant syndrome." The Payra Deep-sea Port, designed to rival Singapore and Colombo, operates at a fraction of its capacity. The Rooppur Nuclear Power Plant, Bangladesh's most expensive infrastructure project at US$12.65 billion, faces questions about its economic viability in a country with chronic transmission and distribution problems.

Second was the banking- sector crisis. The political-business nexus led to unprecedented levels of non-performing loans, reaching nearly 10 per cent of total loans by 2023. The practice of "special rescheduling" - essentially extending bad loans to politically connected borrowers - created a zombie banking sector that couldn't effectively allocate capital to emerging sectors.

Third was an innovation gap. Despite establishing numerous high-tech parks, Bangladesh's attempt to move up the value chain remained largely aspirational. The Digital Bangladesh initiative, while successful in basic digitisation, failed to create a robust technology ecosystem. The country remained trapped in low-value manufacturing, even as Vietnam and India attracted investments in electronics and advanced manufacturing.

The most significant missed opportunity was perhaps in export diversification. Despite numerous policies and incentives, Bangladesh's export basket remained dangerously concentrated in garments. Promising sectors like pharmaceuticals, light engineering, leather, agro-processing and software services never achieved their potential, hampered by a combination of regulatory complexity, infrastructure bottlenecks, and skills shortages.

The model's fundamental flaw lay in its inability to transition from a relationship-based economy to an institutions-based one. The same political stability that initially attracted investment eventually became a barrier to necessary reforms. The result was a classic case of "premature middle-income stagnation" - growth without structural transformation.

Beneath Bangladesh's success story lurks an uncomfortable truth: the model that got Bangladesh here won't take it much further, especially not in the race to benefit from China's manufacturing fallout. To uncover this uncomfortable truth, we can take a look at the data from carefully selected Asian countries, both in terms of comparative peers and evaluation metrics. We can think of a framework which would pit potential countries and their competitive advantages from where we can draw learnings. We can start with a framework which focuses on eight countries - India, the Philippines, Pakistan, Vietnam, Bangladesh, Indonesia, China, and Malaysia - that represent distinct stages of manufacturing evolution in Asia. These nations weren't chosen merely for their geographic proximity, but rather for their strategic significance in global supply chains and their potential to absorb manufacturing capacity shifting from China.

First, we can include established manufacturing powerhouses (China, Malaysia) to set performance benchmarks. Second, we incorporate rapidly industrialising economies, like Vietnam and Indonesia, that have already demonstrated success in attracting relocating manufacturers. Thirdly can we have large-population countries (India, Pakistan, Bangladesh) that possess significant demographic potential. Finally, we can include the Philippines as a crucial test case of services-manufacturing hybrid development.

Our analytical framework will rest on four pillars that comprehensively capture manufacturing competitiveness:

Quantity of Labour: We track both current workforce size and projected growth through 2040 using UN population data. This dual measure captures not just static labour availability but future demographic dividends - crucial for long-term investment decisions. The 2040 projection specifically aligns with the typical 15-20-year planning horizon of major manufacturing investments.

Quality of Labour: The three-pronged assessment of labour quality - literacy rates (UNESCO), English proficiency (Education First), and engineering capabilities (World Economic Forum) - reflects the full spectrum of skills required in modern manufacturing. Basic literacy indicates workforce trainability, English proficiency matters for global integration, and engineering scores predict capacity for technical absorption.

Wage Competitiveness: Manufacturing wages, sourced from JETRO for consistency, serve as our cost benchmark. We specifically use monthly wages rather than hourly rates, as this better reflects total labour costs in Asian contexts where overtime and shift work are common.

Regulatory Environment: The regulatory assessment combines FDI restrictiveness (OECD) and labour-market rigidity (World Bank) metrics. These parameters matter because they affect both initial investment decisions and operational flexibility. The weeks-of-salary metric for labour regulation provides a quantifiable measure of employment flexibility.

The framework was used by Natixis in a report titled Youthful Asia in 2022, which is updated with current data in Table-1.

This framework generates two distinct rankings - basic and capital-intensive manufacturing competitiveness - acknowledging that different types of manufacturing have different factor intensities. The dual ranking system helps explain why some countries excel in labour-intensive sectors while others lead in advanced manufacturing. The numbers tell a sobering tale. Despite impressive GDP growth averaging 6.0 per cent annually, the country's engineering capabilities score a mere 3.8 out of 10, significantly below India's 4.6 and Malaysia's 5.3. Foreign direct investment, critical for technological upgrading, remains constrained by one of Asia's most restrictive regulatory environments. The banking sector, burdened by political lending, is  struggling with non-performing loans that would make even the most optimistic investor pause.

struggling with non-performing loans that would make even the most optimistic investor pause.

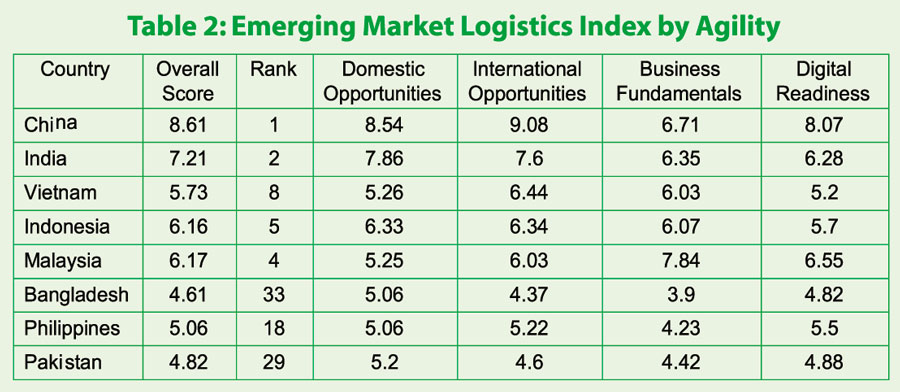

Logistics efficiency acts as a decisive factor in FDI decisions, functioning as the invisible thread that connects investment to profitability. Modern manufacturing, built on just-in-time inventory and global value chains, requires seamless movement of goods. Poor logistics creates hidden costs - delays at ports, unpredictable delivery times, inventory stockpiling, and damaged goods - that can quickly erode any labour-cost advantages. For example, while Bangladesh offers wages at one-third of China's, its logistics-performance index ranks 100th globally, adding 4.5-5 per cent to product costs. For potential investors, this logistics gap often becomes the dealbreaker, particularly in time-sensitive industries like electronics or fast fashion. Agility, a middle- eastern research organisation, ranked the countries in our framework based on their logistics performance. Domestic Opportunities measures internal market potential and business environment, International Opportunities assesses global trade potential and infrastructure, Business Fundamentals evaluates regulatory transparency and contract enforcement, while Digital Readiness examines technological infrastructure and e-commerce capabilities.

Bangladesh ranks last, 33rd, among regional peers in logistics competitiveness, with its lowest score in Business Fundamentals (3.90). While maintaining comparable Domestic Opportunities (5.06) with competitors like the Philippines, it significantly lags in International Opportunities (4.37) and lacks the institutional strengths needed for global supply-chain integration.

What Bangladesh needs isn't just reform - it needs reinvention.

Imagine a Bangladesh where economic success isn't determined by political connections but by innovation and efficiency, where the garment worker's daughter doesn't just operate a sewing machine but designs the next fast-fashion algorithm, where Dhaka's entrepreneurs don't just execute others' designs but create their own global brands, where we design and fabricate semiconductors, and top technology firms are racing to set up shop in our economic zones. This isn't fantasy. Vietnam, with a smaller population and similar starting point, has already moved up the value chain, attracting major electronics manufacturers. Malaysia transformed itself from a rubber exporter to a semiconductor hub. Even India, despite its bureaucratic maze, has built world-class IT services capabilities.

Bangladesh's advantage - its young, eager, and increasingly connected workforce - is real. By 2040, it will have 131 million working-age people, dwarfing Vietnam's 70 million. Its wages, at US$240 per month, are a third of China's, making it attractive for manufacturing relocation. But without urgent investment in skills and institutions, this demographic dividend risks becoming a demographic disaster. Now, upskilling has been offered as a silver bullet to many of Bangladesh's manufacturing problems, but the problem lies even beyond task-specific skills. Modern manufacturing success hinges on the balance between hard and soft skills. Hard skills encompass technical competencies: machine operation, quality control, digital literacy, and basic engineering principles. Equally crucial are soft skills: workplace effectiveness like time management and problem-solving, team integration (communication, cross-cultural awareness), and professional attitudes (reliability, continuous- learning mindset). In Bangladesh's context, while workers possess basic operational abilities, significant gaps exist in both domains. Technical deficits include limited exposure to modern machinery and weak digital literacy, while soft-skill challenges involve communication barriers and hierarchical mindsets. This dual gap helps explain Bangladesh's productivity challenges despite its wage advantages.

Bangladesh faces a critical Catch-22 in its manufacturing ambitions: the Skills-Investment Paradox. High-tech multinational companies hesitate to invest without a skilled workforce, but workers can't develop advanced skills without exposure to sophisticated industrial operations. With an engineering capability score of 3.8, well below regional competitors, Bangladesh remains trapped in this cycle. The solution lies in breaking this deadlock through coordinated intervention: attracting anchor industries like Vietnam did with Samsung, Malaysia with Intel, developing specialised industrial parks with training facilities similar to Malaysia's model, and establishing public-private partnerships for skills development similar to Singapore's approach. Success requires simultaneous action rather than linear solutions.

As global companies orchestrate their exodus from China, a complex matrix of opportunities and challenges emerges for Asia's aspiring manufacturing hubs. The data reveal a nuanced landscape where no single country perfectly replicates China's manufacturing ecosystem, but each offers distinctive advantages in the race to capture relocating industries. Bangladesh is not well-positioned to attract companies relocating from China. Its competitive labour costs, strategic location, and improving industrial infrastructure make it an attractive destination for manufacturers looking to diversify, but regulatory regime and skilled-worker availability are two of the biggest challenges in attracting investors.

To maximise this opportunity, Bangladesh must focus on improving logistical capabilities, workforce skills, and sustainable manufacturing practices to meet the expectations of international corporations. By strengthening trade relations with key markets such as the U.S., EU, and Japan, and implementing policies that favour foreign investment, Bangladesh can emerge as a viable alternative manufacturing hub in Asia.

The writer is a Partner at Inspira Advisory and Consulting Limited. Mohammed.

salman@inspira-bd.com