![]() The global trading regime facing Bangladesh’s export-oriented sectors is changing at a fast pace. The recently imposed Trump Reciprocal Tariffs and the likely implications of the Least Developed Country (LDC) graduation are two important considerations in this connection. However, yet another development that Bangladesh should be aware of is the European Union (EU)’s carbon border adjustment mechanism (EU-CBAM) which ought to figure on the radar screen of Bangladesh’s policymakers and also export-oriented apparels exporters.

The global trading regime facing Bangladesh’s export-oriented sectors is changing at a fast pace. The recently imposed Trump Reciprocal Tariffs and the likely implications of the Least Developed Country (LDC) graduation are two important considerations in this connection. However, yet another development that Bangladesh should be aware of is the European Union (EU)’s carbon border adjustment mechanism (EU-CBAM) which ought to figure on the radar screen of Bangladesh’s policymakers and also export-oriented apparels exporters.

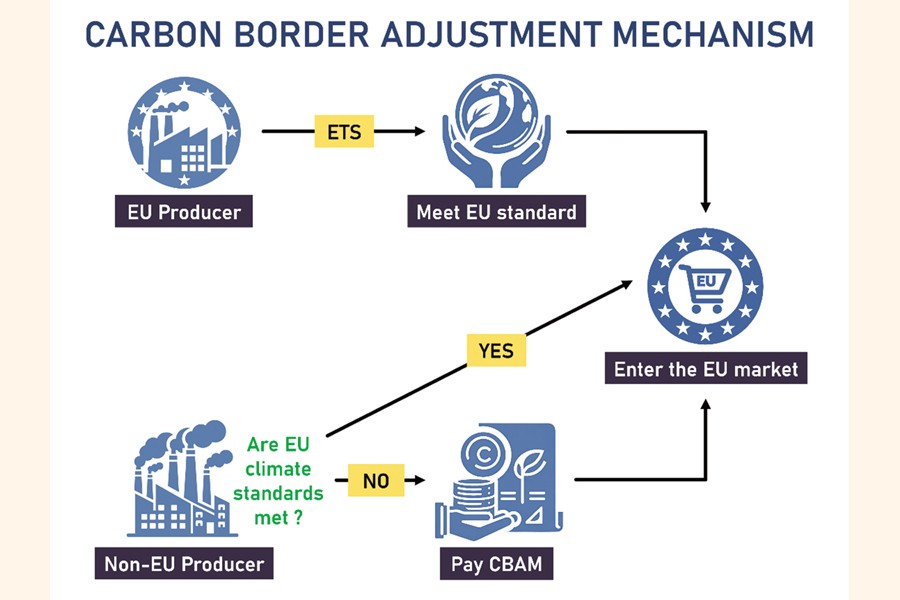

As is widely known, sustainability concerns have come to dominate global discourse in recent times and for valid reasons. Global commitments in this regard are embedded in the sustainable development Goals (SDGs) adopted by the United Nations in 2015. Against the backdrop, issues of reducing carbon emission (CO2 e) have emerged as existential concern for our planet. Efforts are being taken at various levels, and in different platforms, to bring down CO2 emission, to ensure a sustainable planetary future. EU has been playing a leading role in these endeavours. In recent years, EU has been pursuing a range of proactive policies and developing an array of tools with a view to reduce CO2 emission, including in areas of intra-EU trade and in view of EU trade with countries from outside the region. So, the Carbon Border Adjustment Mechanism (CBAM) introduced by the EU on imported items entering the EU markets demands particular attention. The Fit for 55 initiative of the EU is a legislative package proposed by the EC in 2021 with the aim of reducing GHG emission by 55 per cent by 2030 (Council of the European Union, n.d.). The central idea informing the CBAM is to align carbon costs of EU’s domestic production with those of imported goods.The idea is to both discourage companies that emit CO2 in production processes from doing so and encourage and incentivise those that adopt environment-friendly production processes and practices.

The EU-CBAM works as a carbon tax on companies and producers doing business with the EU countries for CO2 emission that takes place along their value/supply chains. The CBAM has significant implications for developing countries (DCs) and least developed countries (LDCs) because of the likely impacts of this ontheir export performance and competitivenessin the EU market. Whilst for the time being the coverage of imported items under the CBAM is limited, there is a plan to broaden the list to include all imported products by 2030. Thus, in foreseeable future it is likely to also include apparels imported to the EU. It goes without saying that this has serious implications for Bangladesh 84 per cent of Bangladesh exports constitute apparels and about half of this is destined for the EU market. EU’s position is that EU’s own non-compliant greenhouse gas (GHG)-producing producers are penalised for CO2 emission in their production practices and value chains.It is thus only fair that a mechanism of carbon pricing should be set for goods produced outside of the EU that are exported to the EU, to create a comparable competitiveness situation and a level playing field.

Carbon Tax and Bangladesh’s Apparels Export to the EU: As a beginning, the CBAM has brought under its ambit six sectors: cement, electricity, fertilizers, iron and steel, aluminium and hydrogen. These were selected based on their relatively high contribution to GHG emission, and higher risks of carbon leakage. However, CBAM was to be achieved in phases. The CBAM has been operationalised since October 2023, with a transitional phase following which the importers of the six carbon intensive sectors mentioned above will need to report about CO2 emissions.All items of import including apparels, are to be brought under the ambit of the CBAM by 2030.

Exports of the six items from Bangladesh, included in the EU-CBAM list, are rather negligible. However, as was noted, inclusion of apparels would no doubt be a game changer. For example, in Europe, the average prices of a cotton T shirt imported from India and China are € 5.4 and € 6.5 respectively. The average imported prices for a pair of cotton jeans from India and China are € 5 and € 6.7 respectively. Based on the differences in Carbon emissions in India and China in the production of both goods to Europe, exporters from India and China will pay an additional 3.4 per cent and 0.9 per cent of the imported price equivalent for exporting 1 kg of cotton T-shirts respectively. To export, 1 kg of cotton jeans to Europe, India and China will be required to pay an additional price to the tune of 31.8 per cent and 13 per cent (GreenStitch, 2024). Estimates carried out by the author indicates that, under the current scenario, the carbon tax on Bangladesh’s exports of apparels to the EU could be as high as 4.0 per cent.

The aforementioned likely scenario should transmit cautionary note to Bangladesh’s producers and policymakers, particularly against the backdrop of Trump Tariffs and the upcoming LDC graduation. As is to be noted, the attendant focus areas are not delimited to enterprise-level activities only. Sustainable sourcing, digitalisation of trading activities, cross-border paperless trade, introduction of single window and other environment-friendly sourcing and trade facilitation measures will be necessary to reduce CO2 emission all along the supply and value chains. This is more so because Bangladesh, like the other countries in South Asia, faces significant challenges in advancing digital, green and sustainable trade facilitation.Various major brands and buyers which are sourcing from Bangladesh are already taking various flanking measures in anticipation of the changing global trading regime, and as part of their own green-friendly sourcing practices and supply chain management. For example, major brands and buyers dealing with Bangladesh’s export-oriented apparels sector such as H&M, Walmart and Zara have set up their own targets as part of their supply chain management stipulation concerning such areas as water usage reduction, use of electricity from renewable sources, use of recycled and sustainably sourced materials, reduction of GHG emission and net-zero emission and reduction of emission along the supply chain. What is of interest to note is also that many such targets aim at 2030, a clear sign that brands and buyers are aware of the possibility of inclusion of textiles and apparels in the CBAM list by 2030.

Bangladesh’s Readiness: It needs to be noted in view of the above that the export-oriented knitwear apparels industry of Bangladesh has been playing a pioneering role in pursuing sustainable practices and positioning itself as a global leader in eco-friendly garment production. To note, knitwear exports constitute 43.4 per cent Bangladesh’s global export. In the EU market, share of Bangladesh’s knitwear export is about 60 per cent of the country’s total RMG exports (FY 2023-24). Bangladesh has the world’s highest number of LEED (Leadership in Energy and Environmental Design) certified garment units. 56 of the world’s top 100 LEED-certified industries are operating in Bangladesh and 7 out 10 Platinum certified units as well. As of June 2025, Bangladesh had 248 LEED-certified government enterprises of which 105 were Platinum, 129 were Gold and 10 Silver and 4 Basic Certified (TDS, 2025).

Bangladesh’s Readiness: It needs to be noted in view of the above that the export-oriented knitwear apparels industry of Bangladesh has been playing a pioneering role in pursuing sustainable practices and positioning itself as a global leader in eco-friendly garment production. To note, knitwear exports constitute 43.4 per cent Bangladesh’s global export. In the EU market, share of Bangladesh’s knitwear export is about 60 per cent of the country’s total RMG exports (FY 2023-24). Bangladesh has the world’s highest number of LEED (Leadership in Energy and Environmental Design) certified garment units. 56 of the world’s top 100 LEED-certified industries are operating in Bangladesh and 7 out 10 Platinum certified units as well. As of June 2025, Bangladesh had 248 LEED-certified government enterprises of which 105 were Platinum, 129 were Gold and 10 Silver and 4 Basic Certified (TDS, 2025).

Some of the green-friendly practices pursued by these units include the followings: Use of solar power; reuse of heat losses to reduce carbon emission; management of wastewater through effluent treatment plant; repurposing of exhaust air from generators to boil water efficiently; raising energy efficiency and reduction of energy consumption and CO2 emission in dyeing and finishing processes with help of environment-friendly technology; greater use of sustainable materials and recycling practices; use of organic and recycled cotton and recycled polyester; reuse of plastic bottles, and recycled yarn and fabrics; ensuring biodegradability and compatibility standard (EN13432). A number of Bangladesh’s manufacturers of apparels have joined such initiatives as Partnership for Cleaner Textile (PaCT) and are also collaborating with other stakeholders. Such partnerships are geared to sustainable water resource management and zero discharge of hazardous chemicals.

However, as far as Bangladesh is concerned, ensuring compliance with EU-CBAM requirements, as was noted earlier, will call for a host of initiatives and measures, at macro, meso-sectoral and enterprise levels. The smart way to go forward is to undertake concrete measures in anticipation of the EU-CBAM coming into force in 2030.

Recommended Initiatives:

Develop a monitoring mechanism in view of EU-CBAM. To deal with this emergent challenge, the Government of Bangladeshshould set up a special and dedicated CBAM Compliance Wing at the Ministry of Commerce which would be tasked to monitor the situation as regardsinclusion of apparels sector in the CBAM list and the consequent requirements.

Incentivise adoption of clean energy technologies. Bangladesh should encourage RMG enterprises to adopt technologies that are environment-friendly and green. In case of apparels, these would include, among others, use of renewable energy, recycling of water, setting up ofEffluent treatment plants (ETPs), and adoption of energy-saving technologies.

Proactively engage with initiatives in the WTO: WTO has developed a database of environment-friendly technologies, a number of which are critical to saving energy and reducing GHG emission in the production of apparels. A fund may be created as part of WTO’s aid for trade programme to help LDCs and developing countries access such technologies.

Develop and put in place a domestic carbon pricing mechanism. A number of developing countries (e.g. India, China, Vietnam), which are Bangladesh’s major competitors in the EU apparels market, are in the process of putting in place domestic carbon pricing mechanism. In absence of such measures, Bangladesh’s exporters of apparels (and by implication EU importers of apparels from Bangladesh) will face higher costs in comparison with countries that will have such mechanisms in place.

Consider CBAM-compliance from a broader perspective. CBAM-type of border measures, as also environment-sustainable production and supply chain practices in general, are likely to become the new normal in global trade in foreseeable future. Disclosing carbon emission is not confined to justthe EU requirement. The global movement favouring disclosure of carbon emission, carbon pricing, launching of carbon market, environmental rehabilitation, transition to renewable energy and emission-trading schemes is gaining increasing traction. Many of developing countries are joining this wave.

Introduce supportive fiscal-monetary measures. Bangladesh has introduced a number of incentives in its fiscal and monetary policies to encourage adoption of green practices and CO2 emission-reducing production processes. These include: lower (zero) import duties on green-friendly capital machineries (e.g. VAT exemptions on solar panels/batteries); introduction of environment protection surcharge (of 1 per cent) on polluting industries; lower tax rate (of 2 per cent) to be paid by exporting businesses that are operating from green factory buildings. Bangladesh Bank has also taken a number of initiatives in this regard

Pursue renewable energy policy more proactively. A lot in view of Bangladesh’s CBAM-compliance would depend on the country’s overall energy policy. If the share of renewable energy is not increased at a fast pace, Bangladesh’s apparels industry will remain dependent on fossil-fuel driven energy sources which will in turn be reflected in the sector’s CO2 emission track record.

Prioritise implementation of the RMG emission- reducing dedicated project. Bangladesh is at present implementing a US$ 340.5 million worth project titled ‘Promoting private sector investment through large scale adoption of energy-saving technologies and equipments for textiles and RMG sectors of Bangladesh. The project is earmarked to be implemented between 2020-2034, with integrated package of concessional financing for textile and RMG manufacturers.

Engage with other countries so that CBAM is not used as a protectionist measure. There is a debate as to whether the CBAM is a protectionist measure by the EU to secure the interests of its own producers and the EU economy in general. Whether CBAM violates WTO regulations is also an issue. Bangladesh should remain engaged with other countries in relevant discussions so that CBAM is not weaponised as a trade restrictive tool

Concluding Remarks: As the preceding discussions bear out, for Bangladesh, ensuring sustainability and responsible practices all along the value and supply chain has emerged as a necessity and is no longer an option. While EU is taking the lead, through trade-related measures such as CBAM, it could emerge, as a new normal in the global trade of the future.

Ensuring EU-CBAM compliance ought to be seen as a priority national agenda for action by Bangladesh’s policymakers. At the same time, this will call for international support measures towards strengthened global integration of relatively weaker economies such as Bangladesh.

Professor Mustafizur Rahman Ph.D is a Distinguished Fellow at the Centre for Policy Dialogue (CPD).

mustafiz@cpd.org.bd

© 2026 - All Rights with The Financial Express