Fahmida Khatun, Syed Yusuf Saadat, Afrin Mahbub and Zazeeba Waziha Saleh | November 10, 2025 00:00:00

![]() Bangladesh has long maintained an impressive record of external debt servicing, standing out among least-developed countries for its fiscal discipline and strong export performance. For decades, the country has met its repayment obligations with relative ease, reflecting prudent financial management and a robust export sector. However, in recent years, Bangladesh’s economic landscape has become increasingly fragile. The government’s push to finance several large-scale infrastructure megaprojects through foreign borrowing has significantly expanded external-debt levels. At the same time, macroeconomic management has weakened, and a series of distressing indicators now point to mounting economic strain.

Bangladesh has long maintained an impressive record of external debt servicing, standing out among least-developed countries for its fiscal discipline and strong export performance. For decades, the country has met its repayment obligations with relative ease, reflecting prudent financial management and a robust export sector. However, in recent years, Bangladesh’s economic landscape has become increasingly fragile. The government’s push to finance several large-scale infrastructure megaprojects through foreign borrowing has significantly expanded external-debt levels. At the same time, macroeconomic management has weakened, and a series of distressing indicators now point to mounting economic strain.

Revenue collection has fallen short of targets, while inflationary pressure is on the rise. The banking sector is grappling with liquidity shortages and rising non-performing loans or NPLs. Limitations in foreign -exchange reserves amid a persistent dollar shortage lead to a depreciating exchange rate and import constraints that disrupt domestic production. Meanwhile, governance challenges and inefficiencies in public expenditure have further aggravated fiscal stress.

Adding to these vulnerabilities, the growing economic toll of climate change, through loss and damage to infrastructure, agriculture, and livelihoods, poses a new and formidable threat. Climate-induced shocks could further destabilise the external sector and jeopardise Bangladesh’s debt sustainability, compounding an already-fragile situation. These interconnected problems signal a deep-seated macroeconomic imbalance that demands urgent and comprehensive policy reform. To safeguard its economic future, Bangladesh must now focus on strengthening the external sector, enhancing fiscal discipline, and integrating climate resilience into its development and debt -management strategies. Only through such coordinated reforms can the country ensure sustainable growth and protect its people from the converging crises of financial stress and climate vulnerability.

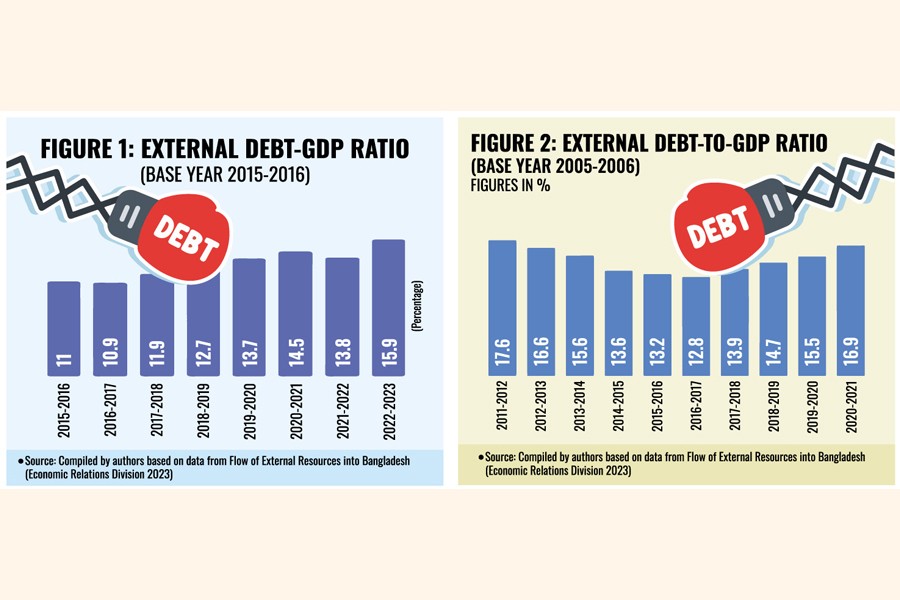

Rising Risks in Bangladesh’s External Debt Landscape: According to the IMF, Bangladesh’s debt burden is sustainable so far. Bangladesh has effectively maintained a low risk of external-debt distress and total debt distress, with a notable absence of defaults on debt payments or requests for rescheduling. However, this success has been facilitated due to the country allocating a larger portion of its revenue toward external debt repayment, as Bangladesh’s ability to service its rapidly growing external debt is severely compromised by its low tax-GDP ratio. This trend raises concerns about a potential trade-off, as the increasing allocation to debt repayment may limit the funds available for investments in sectors crucial for economic growth. In recent years, Bangladesh’s external borrowing pattern has undergone a notable transformation. The country is gradually moving away from concessional loans toward borrowing on standard commercial terms. At the same time, the composition of lending sources has shifted, with bilateral arrangements now taking precedence over multilateral financing.

Another trend is the growing reliance on supplier credit, which often carries higher costs and shorter repayment windows. A rising share of Bangladesh’s external loans is now tied to variable interest-rate benchmarks such as the Secured Overnight Financing Rate (SOFR), the Euro Interbank Offered Rate (EURIBOR), and the London Interbank Offered Rate (LIBOR). These rates fluctuate with global financial conditions, exposing the country to greater interest-rate risk. Compounding this, newer loan agreements increasingly feature tighter terms, characterised by shorter grace periods and reduced maturities. These are factors that could heighten repayment pressures and further strain the country’s external-debt profile.

Bangladesh’s debt -sustainability challenge is complex and evolving. The country’s declining foreign -exchange reserves and widening balance- of -payments deficit have created serious concerns about its capacity to service the large volume of external debt accumulated in recent years. While Bangladesh’s debt position has so far been deemed manageable, this confidence may soon be tested as the repayment schedules for several major loans begin to take effect.

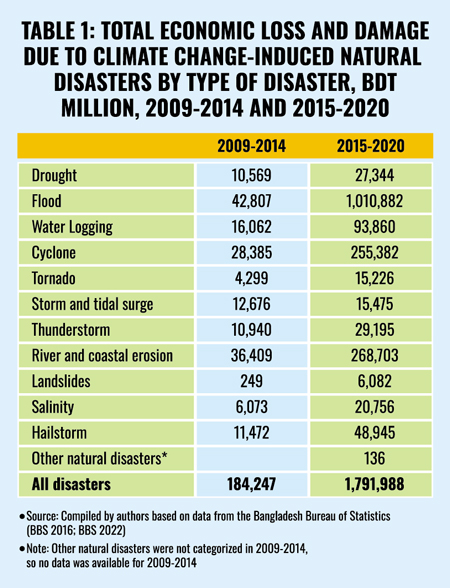

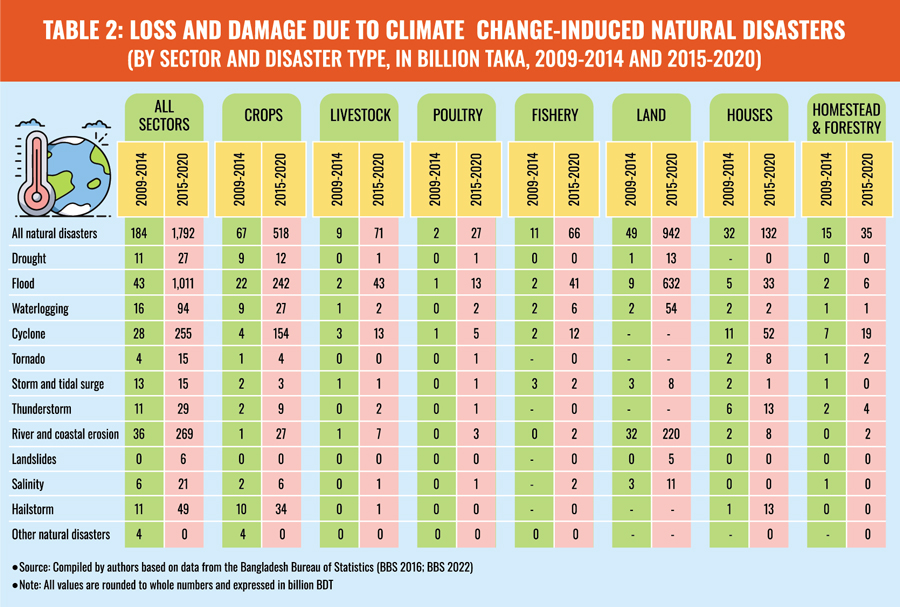

Rising Climate Losses and Debt Pressure in Bangladesh: Compounding these financial pressures is the growing threat of climate change. Bangladesh remains one of the world’s most climate-vulnerable countries, facing increasingly frequent and severe natural disasters such as floods, cyclones, and river erosion. These calamities cause widespread economic losses, destroying infrastructure, depleting income sources, and eroding capital, particularly among the most vulnerable communities. The economic toll of climate change on Bangladesh has risen dramatically, leading to total losses and damages that surged nearly tenfold, from BDT 184,247 million during 2009–2014 to BDT 1,791,988 million between 2015 and 2020. This significant surge indicates a heightened impact of climate change-induced natural disasters on Bangladesh’s economic landscape during the latter period. As a result, the government is compelled to allocate significant resources toward relief, rehabilitation, and rebuilding efforts, in addition to funding long-term adaptation and mitigation initiatives to bolster climate resilience.

Yet, a critical financing gap persists in meeting the country’s climate-related needs. To bridge this gap, Bangladesh continues to rely heavily on external borrowing from bilateral and multilateral partners. While such financing is often essential for development and adaptation, it also deepens long-term debt vulnerabilities, potentially amplifying the risks to the country’s overall debt sustainability.

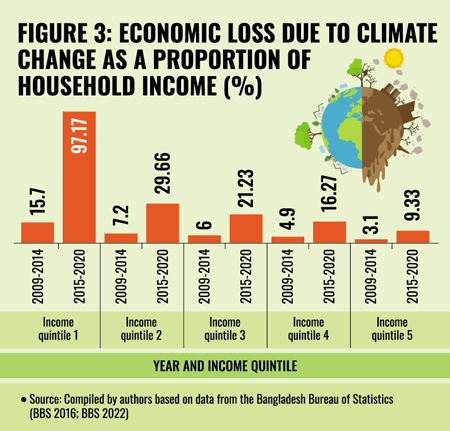

The widening disparities in economic losses reveal the deeply unequal burden of climate change across income groups. For households in the poorest quintile, the economic loss caused by climate-related events surged from 15.7 per cent of their income during 2009–2014 to an alarming 97.17 per cent in 2015–2020, almost equivalent to their entire earnings (Figure 1) (BBS, 2016; BBS, 2020). In stark contrast, for households in the richest quintile, the corresponding figure rose more modestly from 3.1 per cent to 9.33 per cent over the same period (BBS, 2016; BBS, 2020). These figures underscore the disproportionate impact of climate change on lower-income households, whose limited financial buffers make them far more vulnerable to shocks and losses, thereby deepening existing inequalities and threatening poverty -reduction gains.

The widening disparities in economic losses reveal the deeply unequal burden of climate change across income groups. For households in the poorest quintile, the economic loss caused by climate-related events surged from 15.7 per cent of their income during 2009–2014 to an alarming 97.17 per cent in 2015–2020, almost equivalent to their entire earnings (Figure 1) (BBS, 2016; BBS, 2020). In stark contrast, for households in the richest quintile, the corresponding figure rose more modestly from 3.1 per cent to 9.33 per cent over the same period (BBS, 2016; BBS, 2020). These figures underscore the disproportionate impact of climate change on lower-income households, whose limited financial buffers make them far more vulnerable to shocks and losses, thereby deepening existing inequalities and threatening poverty -reduction gains.

Summarising the Findings of the Paper: Against this backdrop, the study titled “Navigating Debt, Development and Disasters: Making Debt Sustainability Analyses Work for Bangladesh” seeks to shed light on how climate change could reshape the country’s debt dynamics. The research aims to go beyond conventional assessments by integrating climate-related risks and the financial resources needed for climate transition into Bangladesh’s debt -sustainability analysis. Drawing on the most recent loan-level and-disaster-specific data from both domestic and international sources, the study draws upon the International Monetary Fund’s (IMF) Debt Sustainability Framework (DSF) for Low-Income Countries (LIC). The LIC DSF is used as a foundation to assess the current state of debt-burden indicators for Bangladesh. This standardised framework evaluates the country’s ability to manage existing and future debt under both baseline and adverse scenarios. Using this approach, the study examines four key external -debt indicators, including two reflecting solvencies, i.e. external debt-to-GDP ratio and external debt-to-exports ratio, to gauge long-term debt sustainability, and two reflecting liquidities, which include the external debt service-to-exports ratio and external debt service-to-revenue ratio to assess short-term repayment capacity. By doing so, it offers a more nuanced understanding of how environmental vulnerabilities and fiscal realities intersect—and how Bangladesh can develop a debt strategy that remains resilient in an era of intensifying climate risks.

Four hypothetical scenarios were designed to assess the different impacts of indicators linked to climate change on Bangladesh’s ability to sustain its debt burden. This included (1) economic losses from climate change (2) converting climate-related loans to grants (3) a hypothetical decline in GDP, revenue, and exports due to the EU’s Carbon Border Adjustment Mechanism (CBAM) (4) a scenario of rising variable interest rates. The results from both the baseline-and stress tests were compared against a medium debt-carrying capacity threshold, consistent with the IMF’s 2024 debt-sustainability assessment for Bangladesh.

Four hypothetical scenarios were designed to assess the different impacts of indicators linked to climate change on Bangladesh’s ability to sustain its debt burden. This included (1) economic losses from climate change (2) converting climate-related loans to grants (3) a hypothetical decline in GDP, revenue, and exports due to the EU’s Carbon Border Adjustment Mechanism (CBAM) (4) a scenario of rising variable interest rates. The results from both the baseline-and stress tests were compared against a medium debt-carrying capacity threshold, consistent with the IMF’s 2024 debt-sustainability assessment for Bangladesh.

In terms of solvency, which reflects Bangladesh’s long-term capacity to repay its debts, the assessed indicators stayed below sustainable thresholds under both baseline- and hypothetical or stress- test scenarios, suggesting a low risk of long-term debt unsustainability from climate change. In contrast, liquidity indicators, reflecting the country’s short-term ability to meet financial obligations, were more sensitive. Even moderate reductions in export earnings or revenue, or increases in variable interest rates, could push these ratios above sustainable limits, particularly when combined with climate-related losses. This highlights Bangladesh’s vulnerability to short-term external shocks and the importance of maintaining stable finances to ensure immediate-term debt sustainability.

Conversely, when loans for climate-change mitigation and adaptation were treated as grants, the analysis indicated a much more favourable scenario. Both solvency and liquidity indicators remained well within sustainable thresholds, signalling a low risk of debt distress. Even under potential export declines due to the EU’s CBAM, debt -burden indicators may remain stable if climate financing were provided as grants. These results underscore that grant-based or highly concessional climate financing could significantly enhance Bangladesh’s debt -management capacity.

In this context, the paper spells out seven-point recommendations for policymakers.

First, enhanced methodologies are necessary to systematically collect consistent data on climate change’s loss, damage and economic impact. Such data are crucial to making pragmatic assessments of the true economic effects of climate change, thereby aiding in the development of comprehensive policy toolkits. Additionally, this data is essential for effectively managing climate finance, ensuring that funds are appropriately disbursed to the most vulnerable and affected areas. Proper management of climate finance is crucial to ensuring that external loans are utilised effectively to build resilience to climate change, reducing the need for additional borrowing. This will assist in maintaining financial stability for Bangladesh, potentially resulting in climate finance being provided on more concessional terms and thereby reducing the risk of debt distress.

Second, climate -change indicators, especially those that include a valuation of total damage incurred due to climate change, must be incorporated when making projections about debt sustainability. Such an assessment will facilitate the construction of Bangladesh’s profile of current and future risk of debt distress, closely mirroring the actual economic scenario. This will assist policymakers in formulating more effective debt-management strategies, strengthening infrastructure and building institutional capacities to mitigate further incremental economic loss, ensuring long-term economic and financial stability.

Thirdly, economic loss and damage due to climate change put Bangladesh at risk of failing to service its external -debt obligations in the event of a large climate change-induced natural disaster, which requires immediate and substantial government funding support. Hence, Bangladesh should actively seek support from the Loss and Damage Fund, announced at the 28th UN Climate Change Conference (COP28). Furthermore, borrowings intended to mitigate environmental damage must be prudently managed to take advantage of the Loss and Damage Fund.

Full implementation of the CBAM by the EU may pose significant threats to Bangladesh’s debt sustainability in the days ahead. Urgent and proactive steps are required to reduce emissions and ensure the resilience of Bangladesh’s exports in the face of the CBAM. To prepare for the imposition of the CBAM and similar measures from other trading partners, the government must formulate national emissions -measurement, reporting and -verification policies for every sector. Such policies should include quantitative mitigation targets for each industry so that environmental responsibility and adherence to international standards enable exporters to preserve their competitive advantage.

Full implementation of the CBAM by the EU may pose significant threats to Bangladesh’s debt sustainability in the days ahead. Urgent and proactive steps are required to reduce emissions and ensure the resilience of Bangladesh’s exports in the face of the CBAM. To prepare for the imposition of the CBAM and similar measures from other trading partners, the government must formulate national emissions -measurement, reporting and -verification policies for every sector. Such policies should include quantitative mitigation targets for each industry so that environmental responsibility and adherence to international standards enable exporters to preserve their competitive advantage.

The fifth point in the recommended must-dos stresses that climate finance should be secured as grants rather than loans. The findings from this study show that reclassifying climate loans as grants reduces the risk of debt distress for Bangladesh. Considering Bangladesh’s substantial need for climate finance to effectively implement mitigation and adaptation measures, securing adequate funding through domestic resources is not feasible. As such, Bangladesh must rely on external loans. Providing these loans as grants would significantly reduce Bangladesh’s debt burden while aiding the economy in addressing climate- change risks. Even if exports decline due to the CBAM, debt -burden indicators may remain stable if climate loans are converted to grants. Reclassifying climate loans as grants would enhance the country’s preparedness for future shocks while ensuring financial stability.

The sixth recommendation alerts that variable-interest loans in Bangladesh’s external-borrowing portfolio pose an exceptionally high risk for the country. This study’s findings show that even the slightest increase in the interest rate on these loans could create serious liquidity problems for Bangladesh, especially when juxtaposed with economic loss and damage due to climate change-induced natural disasters. To avoid such risks escalating further, Bangladesh must refrain from taking any more external loans with variable -interest rates attached.

Last, but not least by any means, is Bangladesh’s poor domestic- resource -mobilisation record implies its primary budget deficit is rising, making it increasingly challenging to service future external debts without new external borrowing. Bangladesh must urgently and vigorously increase its tax- revenue collection, expand its tax base, improve tax compliance and reduce illicit financial outflows to prevent falling into debt traps and vicious cycles of perpetual indebtedness.

Dr Fahmida Khatun is Executive Director, Centre for Policy Dialogue (CPD).

fahmidak.cpd@gmail.com. Syed Yusuf Saadat is Economist, UNDP. Afrin Mahbub is is a Research Associate at CPD. Zazeeba Waziha Saleh is a Master of Philosophy student in Economics at the University of Oxford

© 2026 - All Rights with The Financial Express