![]() President Trump's trade war has upended the process of globalisation in a manner that has raised the question of whether it has any future. The backdrop to this is widespread discontent about its outcome that has spread from the developing to the developed world and from the left to the right of development discourse. As we shall see below, the process has already been under strain, as indicated by fluctuations in global trade for more than a decade. And the tariff war appears to have put the last nail in the coffin. But the recent developments are not without discomfort and questions. One basic question is whether globalisation has really become history or whether it still has a chance of surviving. Even before the tariff war started, there were talks about deglobalisation and reglobalisation. Has that discussion become irrelevant in the present situation, or can one still talk about a revival of the process? What does the current tariff war mean for the future of globalisation? How is Bangladesh going to be affected, and how should the country adjust and prepare for such a future?

President Trump's trade war has upended the process of globalisation in a manner that has raised the question of whether it has any future. The backdrop to this is widespread discontent about its outcome that has spread from the developing to the developed world and from the left to the right of development discourse. As we shall see below, the process has already been under strain, as indicated by fluctuations in global trade for more than a decade. And the tariff war appears to have put the last nail in the coffin. But the recent developments are not without discomfort and questions. One basic question is whether globalisation has really become history or whether it still has a chance of surviving. Even before the tariff war started, there were talks about deglobalisation and reglobalisation. Has that discussion become irrelevant in the present situation, or can one still talk about a revival of the process? What does the current tariff war mean for the future of globalisation? How is Bangladesh going to be affected, and how should the country adjust and prepare for such a future?

Discontent about globalisation among both liberals and conservatives: Globalisation had its golden age during the last three decades of the twentieth century but started to face shocks from the beginning of the twenty-first century. Interestingly, this came basically from developed countries - those who were once the main proponents of globalisation. And the major players in this were not only conservative politicians; others also had a role.

Discontent about globalisation among both liberals and conservatives: Globalisation had its golden age during the last three decades of the twentieth century but started to face shocks from the beginning of the twenty-first century. Interestingly, this came basically from developed countries - those who were once the main proponents of globalisation. And the major players in this were not only conservative politicians; others also had a role.

While discontent about globalisation is not new, major shocks like the financial crisis of 2008 and the upheavals caused by the COVID-19 pandemic exacerbated it. The initial discontent was about the unequal distribution of the benefits and the rise in inequality - both between and within countries. And that was behind the protests against international organisations like the WTO. Such discontent culminated in the "Occupy Wall Street" movement of 2011. Recent years have witnessed discontent about globalisation in the conservative camp as well. They look at the issue mainly from the perspective of the developed countries of the West and think that, due to uncontrolled globalisation, their supply chains have become excessively dependent on the global market (read: China). Supply bottlenecks during the COVID-pandemic and the subsequent high inflation helped fuel this kind of view.

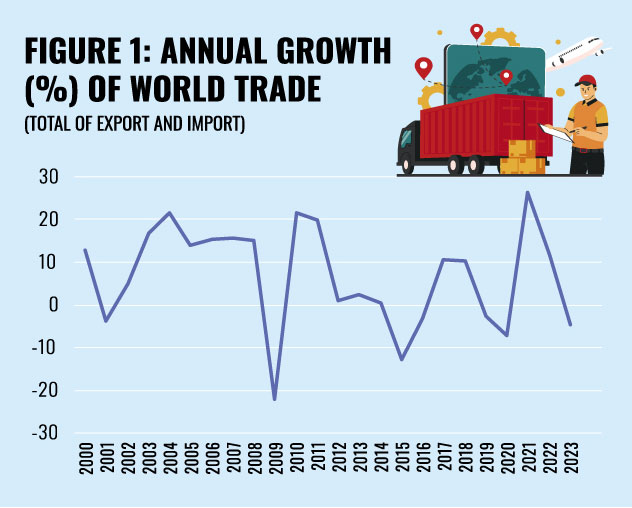

Recent trends in commodity trade and international capital movement show globalisation in strains: Three basic dimensions of economic globalisation are trade in commodities and international movement of capital and labour. Figure 1 provides a picture of the trend in commodity trade. Data presented in this graph basically provide a picture of instability in this indicator of globalisation since 2010. Some ideas about the issue can be formed from knowledge of the basic drivers of the global economy.

If one looks at the share of the major countries in global GDP, one can see that in 1980, the combined contribution of the United States and the European Union was 47 per cent. But that share declined gradually during the subsequent decades and stood at 30 per cent in 2024. During the same period, the share of China rose sharply from 2.26 per cent to 18.73 per cent (Figure 2). One can thus conclude that during the past four decades or so, the USA and EU countries were the major drivers of growth in the global economy, although China has been gradually making its presence. Of course, the issue of whether China can delink its economy from the developed world and play an independent role in the global economy does come up for discussion from time to time.

If one looks at the share of the major countries in global GDP, one can see that in 1980, the combined contribution of the United States and the European Union was 47 per cent. But that share declined gradually during the subsequent decades and stood at 30 per cent in 2024. During the same period, the share of China rose sharply from 2.26 per cent to 18.73 per cent (Figure 2). One can thus conclude that during the past four decades or so, the USA and EU countries were the major drivers of growth in the global economy, although China has been gradually making its presence. Of course, the issue of whether China can delink its economy from the developed world and play an independent role in the global economy does come up for discussion from time to time.

From actual experience, one can see that the trends in the global economy are closely associated with fluctuations in the US economy. If the USA gets into a downturn or recession for some reason, its impact reverberates through the global economy. It can be seen from Figure 1 that in 2001, 2009, 2015, and 2019-20, there were sharp declines in global trade. Records of economic growth in the USA show that the economy of the country faced recession in those years. The health of the global economy is clearly dependent on that of a few countries, especially the USA.

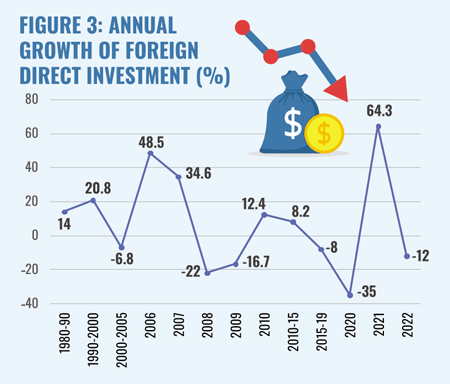

Data on the international flow of capital also shows instability (Figure 3). Important from the point of view of developing countries are grants, loans, and investment in different forms. The latter, in turn, can be through the financial market or through investment in economic activities. Although the financial markets of some developing countries are open to foreign investment, it is foreign direct investment that is regarded as particularly important from the point of view of long-term development of a country. And not all countries are able to attract this kind of investment. Although the internal conditions of the receiving countries are important in this regard, the root of instability usually lies in the economic condition of the investing country and the global economy.

Regional trade agreements have been rising in number: Another development that is worth noting is the rising trend in regional trade agreements - especially since the 1990s. It is the US, countries of EU and China who have played a more important role in shifting towards regional trade agreements. While regional trade agreements can be executed within the framework of WTO rules, it goes without saying that regional or bilateral trade agreements are not fully consistent with the spirit of multilateralism. Such agreements may have the potential for including issues relating to protecting the climate or promoting democracy. But it also needs to be acknowledged that they may also be used to promote political interests and exert influence over developing, small and less powerful countries.

Rise of China and fear about China: China is often cited as a success story of globalisation. With a large population, the country has succeeded in attaining high growth on a sustained basis and in reducing poverty substantially. And one major factor behind this success is the country's effective participation in international trade. Some data can make it clear (Source: WTO Director General's address in 2022).

Rise of China and fear about China: China is often cited as a success story of globalisation. With a large population, the country has succeeded in attaining high growth on a sustained basis and in reducing poverty substantially. And one major factor behind this success is the country's effective participation in international trade. Some data can make it clear (Source: WTO Director General's address in 2022).

• When the country joined the WTO in 2001, the share of the country's GDP in global GDP (in current prices) was 3.9 per cent which rose to 18 per cent in 2022. In that year, the share of the USA was 24.7 per cent.

• Per capita income of China (in PP Dollar) in 2001 was $3,200 - about 9 per cent of USA's $37,000. In 2022, the figure rose to $19,000 - about 28 per cent of USA's $69,000.

• China's share in global trade rose from 4.3 per cent in 2001 to 15.1 per cent in 2021. During the same period, the share of USA declined from 11.8 per cent to 7.9 per cent.

It is clear from the data mentioned above that the gap between the average income of China and the developed countries of the world has narrowed, while its presence in the global market has become much more visible. The latter has happened particularly in the case of manufactured goods - so much so that the country is now regarded as the factory of the world.

Alongside the country's success in the economic field, its political influence has started to grow. On one side, there is a desire to get on an equal footing with developed countries, while on the other, there are initiatives to strengthen friendship with developing countries through economic cooperation. Notable among the latter is the Belt and Road Initiative (BRI) - a programme that is also dubbed as the new silk road. Initiated in 2013, it focuses mainly on infrastructure and targeted investment in 150 countries and international organisations. The fields of investment include roads, railways, ports, energy, digital infrastructure, etc. By 2024, the programme spread to 140 countries accounting for 75 per cent of the world's population and half of global GDP.

The potential contribution of BRI to promoting global trade and growth in developing countries has been recognised internationally - for example, by the World Bank. But it has also come under criticism - especially from considerations like adverse effects of the projects on environment, violation of human rights, and adoption of large projects without regard for the ability of the recipient countries to repay the loan.

Interestingly, criticisms of China's BRI programme often come from countries like India and the USA.

There may certainly be some criticism of a huge and ambitious programme like BRI. But it cannot be denied that there is some discomfort about China that is giving rise to suspicion about the intentions of the country. As the country started making rapid strides after a long period of absence from the global economic scene, and succeeded in reducing the distance from developed countries, the world has become aware of its presence and possible implications. On the one hand, the world is getting the benefits of its high growth and capability to supply goods to the global market. But on the other hand, the growing influence of the country in the arena of international relations is generating some discomfort - even fear.

It seems that the trade war between China and the USA has its roots in the discomfort and suspicion about China mentioned above. The Trump administration started this war in 2018 by imposing tariff on imports from China and cited what was called China's "unfair practices" and "stealing of intellectual property" as the reason. By the end of 2019, tariffs were imposed on about 350 dollars of imports from China. In response, China retaliated by imposing tariffs on 100 billion dollars of imports from the USA. It must also be noted that the European Union also started to impose restrictions on imports from China.

President Trump's tariff war is broader, sometimes going beyond trade: The trade war that started during President Trump's second term is much broader in scope and coverage, and it can be called global. Extraordinarily high tariffs were imposed not only on China but also on many other countries -- apparently on those with whom the USA has a trade deficit. The countries covered extend beyond developed countries to middle income and low income countries including those (e.g., Lesotho) with whom the volume of trade is minuscule. Of course, provision has been kept for separate negotiations on a bilateral basis. In fact, doing bilateral "deals" appears to be the basic strategy of President Trump's current approach.

The way President Trump is using tariff as an instrument (or one could say, a weapon) is unprecedented in modern day policy making. Landmarks of his actions include setting tariff rates at extremely high levels and then postponing their implementation for some time, allowing exemptions in specific cases (e.g., IT products), encouraging bilateral negotiations, getting into conflicts with his own legal authorities, and creating uncertainties by making contradictory and/or vague statements. In addition, issues other than trade deficit are brought in - indicating that the goals being pursued are not only to close the trade gaps but also to pressure countries to tow US policies in matters of geopolitics.

The impact of tariffs on the global economy is going to be negative: The above actions are not only affecting global trade adversely but are also creating a negative environment for investment, production and employment. Not surprisingly, the outlook for the global economy is reflective of that environment. While international agencies like the IMF and the World Bank have lowered their growth forecasts, the ground realities in countries like China and the USA also point in that direction. Rise in the prices of treasury bonds, fluctuations in stock markets, softening of the labour market are all indicative of growing uncertainties. Likewise, news of decline in the growth of industrial production and lay-offs in the sector do not augur well.

IMF's World Economic Outlook, October 2025 projected a decline in the growth of real GDP for the world as a whole as well as for major economies like those of the US and China (see Table 1). For India, the projected impact is less significant - perhaps because of its lower dependence on exports. The decline for Vietnam is very substantial.

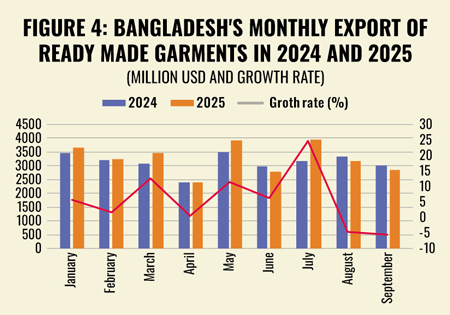

The picture for Bangladesh is complex. GDP growth declined in 2024 because of political transition. But the prospect of recovery from the decline of 2024 is now getting clouded by the uncertainties in the global economy. An indication of the results of such uncertainty is provided by the monthly export figures for the export of ready-made garments (RMG), the overwhelmingly major export item of the country (Figure 4). Alongside figures for growth over the corresponding months of the previous year, the absolute monthly figures are also shown in the figure. As 2024 was a year of political instability, a simple comparison of the 2025 figures with those of the previous year may not provide the full picture of the impact of global tariff war.

The picture for Bangladesh is complex. GDP growth declined in 2024 because of political transition. But the prospect of recovery from the decline of 2024 is now getting clouded by the uncertainties in the global economy. An indication of the results of such uncertainty is provided by the monthly export figures for the export of ready-made garments (RMG), the overwhelmingly major export item of the country (Figure 4). Alongside figures for growth over the corresponding months of the previous year, the absolute monthly figures are also shown in the figure. As 2024 was a year of political instability, a simple comparison of the 2025 figures with those of the previous year may not provide the full picture of the impact of global tariff war.

The figures presented in Figure 4 should be interpreted with the above caveat in mind.

Exports in June, July and August of 2024 were already low because of the political situation; and the performance in June and August of 2025 was worse than the lows of the previous year. Worse, negative growth continued in September as well. Unless exports recover fully, overall growth of the economy of the country cannot return to its normal growth path.

The IMF World Economic Outlook of April 2025 provided a number of explanations for the negative impact of the tariff war on global economic growth. First, tariffs not only distort trade, but also move resources inefficiently across sectors, thus resulting in loss of productivity and adverse effects on production. Second, disruptions in the global supply chain can cause an uptick in inflation which in turn may lead to a tightening of monetary policy and adverse effect on production. Third, tariff-induced effects on the global supply chains can also affect output adversely. All in all, the IMF projects a "large negative impact on global activity".

Developing countries like Bangladesh face multiple challenges: In the situation mentioned above, developing countries like Bangladesh face multiple challenges. First, tariffs are not only creating a difficult environment for the global economy but also have resulted in greater uncertainty and risk being faced by trade oriented economies. Although this may be thought to be a one-off issue, its impact is likely to reverberate through the medium- and long-term future. If IMF projections turn out to be real, their direct and indirect effects are likely to be negative on export-dependent economies like that of Bangladesh. Decline in demand in large markets like that of the USA may have an adverse effect on exports from countries like Bangladesh.

Second, in bilateral trade negotiations, developing countries are usually in a weaker bargaining position and are likely to face pressures and conditions of various kinds. For example, in trade negotiations with the USA and the EU, Bangladesh faces issues relating to environment and labour conditions in export-oriented industries. While they are important issues and Bangladesh should devote greater attention to compliance with labour standards and environmental considerations, conditionality in trade negotiations can be disruptive.

Third, concessions granted in one agreement may be cited by others in order to maximise benefits from a deal. Such bilateral agreements may lead to cost inefficiency and loss of productivity.

Abandoning globalisation cannot be good for the health of the global economy: Although there are discontents against globalisation and the global system needs a serious re-calibration, this cannot be an argument for abandoning it. Of course, a large number of countries have not been able to benefit from trade and capital movements. Even in countries that were able to get into the global market, benefits were not distributed equitably. Growth of real wages of workers often fall behind gains in productivity, and conditions of work remain unacceptable. Exporters often face unfair terms in price negotiations. These and such other issues remain to be addressed. But tariff wars and bilateral negotiations are unlikely to produce better results. It would be important to look at the possibility of re-globalisation and see how the issues that caused resentment against globalisation can be addressed.

The author, an economist, is Former Special Adviser, Employment Sector, International Labour Office, Geneva.

Email: rizwanul.islam49@gmail.com

© 2026 - All Rights with The Financial Express