![]() The widely accepted view is that the local government system brings the government’s decision making closer to the people. A strong local government can ensure good governance through transparency, accountability, effective participation and equal opportunities for all. Most importantly, the system ensures that developmental transformations can start at the grassroots level. The functioning of strong local government institutions (LGIs) strengthens democracy, ensures good governance, and at the same time quickens the pace of political and socioeconomic development of a country.Effective local government system is the primary agent and gatekeeper for shared rule, and is responsive and accountable to local citizens. For ensuring the creation of effective LGIs in the context of Bangladesh, three basic principles are important in performing their responsibilities:

The widely accepted view is that the local government system brings the government’s decision making closer to the people. A strong local government can ensure good governance through transparency, accountability, effective participation and equal opportunities for all. Most importantly, the system ensures that developmental transformations can start at the grassroots level. The functioning of strong local government institutions (LGIs) strengthens democracy, ensures good governance, and at the same time quickens the pace of political and socioeconomic development of a country.Effective local government system is the primary agent and gatekeeper for shared rule, and is responsive and accountable to local citizens. For ensuring the creation of effective LGIs in the context of Bangladesh, three basic principles are important in performing their responsibilities:

• Responsive governance: The LGIs need to perform the right activities that is, to deliver services consistent with citizen preferences.

• Responsible governance: The LGIs would have to perform their responsibilities in the right way that is, manage their fiscal resources prudently. They would have to earn the trust of the local residents by working better and costing less and by managing fiscal and social risks for the communities. They need to strive to improve the quality and quantity of and access to public services.

• Accountable governance: The LGIs need to be accountable to their electorate. They would have to adhere to appropriate safeguards to ensure that they serve the public interest with integrity. Legal and institutional reforms may be needed to enable LGIs to deal effectively with accountability.

Despite the long history of local governance since the British colonial rule and post-independence decentralisation efforts, the LGIs in Bangladesh still play a limited role in delivering essential and mandated quality services to the citizens mainly due to inadequate decision making and limited financial authority; lack of resources and staff; and weak capacity. A key to Bangladesh’s progress towards inclusive and sustainable development is to empower the country’s LGIs through effective and well-articulated administrative and fiscal decentralisation. Further, the LGIs suffer from weak pubic financial management practices which hinder their service delivery capabilities.

Although the total spending of the LGIs in Bangladeshhas increased over the years to around 1 per cent of the country’s GDP in recent years, it remains about five times lower than the developing country’s average. In Bangladesh, spending by LGIs accounts for around 7 per cent of total government expenditure whereas, on average, it is 19 per cent in developing countries and 28 per cent in developed countries. The relatively low share of LGIs’ spending in government’s total expenditure indicates limited fiscal decentralisation in Bangladesh.

Fiscal Decentralisation: Decentralisation is the devolution or reassignment of specific powers ‘with all of the administrative, political, and economic attributes that these [powers] entail’ from the central government to subnational governments which are autonomous within their own geographic and functional spheres of authority. Instead of being accountable to a higher level of government, local governments are accountable primarily to the local electorates. However, the central government does still have a policy role in a decentralised system, including setting standards, providing guidance to the local governments, and monitoring how well local governments are delivering.

Fiscal decentralisation is the public finance dimension of intergovernmental relations. It specifically addresses the reform of the system of expenditure functions and revenue source transfers from the central to the local governments. It is the key element of any decentralisation programme. Without appropriate fiscal empowerment, the autonomy of the local governments cannot be ensured and, hence, the full potential of decentralisation cannot be realised.

For fiscal decentralisation, ‘finance should follow function’ is often cited as the key rule. This means that LGIs need to have adequate resources to carry out the functions they have been assigned. In cases where LGIs are assigned responsibilities but not the allocation of required resources or funding sources, this may be called an ‘unfunded mandate’. Further, the source of LGIs financing also matters. The degree to which LGIs are financed by their own revenues rather than transfers is likely to affect how accountable they are to their residents. The rule that ‘finance follows function’ thus also means considering the balance between locally raised taxes and centrally provided transfers in the revenue mix of the LGIs.

Fiscal decentralisation needs therefore to ensure, to the extent possible, that LGIs are provided with a local revenue base of some significance so that they are not completely dependent on inter-governmental fiscal transfers. However, significant dependency on transfers is unavoidable (except probably the richest LGIs in large and rich cities/municipalities/upazilas) in Bangladesh if they are to provide required level of service delivery. When designing fiscal decentralisation, the national government needs to implement well-designed inter-governmental fiscal transfers that provide for some equity between local governments, do not dis-incentivise local revenue collection, and ensure that the functions assigned to the LGIs are fully funded. Therefore, the key areas for fiscal decentralisation to address are: locally-generated revenues; inter-governmental fiscal transfers; and local public financial management.

In Bangladesh, fiscal decentralisation is challenging because it involves a wide number of dispersed actors across the central government and LGIs as well as agencies spread throughout the country. In practice, public finance management (PFM) system involving a large number of actors across different levels of government tend to be weaker than those that involve fewer players. Furthermore, the key actors in the process typically share different objectives and interests, often in the context of generally low capability throughout the public sector. Decentralisation in Bangladesh involving a large number of actors therefore requires a carefully considered implementation strategy. More importantly, reforms are unlikely to be successful if implementation is driven by a fixed and comprehensive top-down blueprint approach decided by a few central actors who then rapidly impose it across the system.

Instead, the decentralisation process dealing with complex problems in Bangladesh needs to be ‘problem-driven’. This involves a process of ‘muddling through’, motivated by identifying agreed problems and seeking solutions through experimentation and learning led by multiple agents, in the overall direction of the agreed policy goals. This suggests that instead of having a single ‘once-and-for-all’ decentralisation strategy designed to be implemented over a short period, the government needs to have a clear direction to move forward but follow a flexible plan that can be reviewed, updated and amended in the light of on-going experience in implementing reforms. This will require continuous dialogue between the key agencies involved in steering the decentralisation process to facilitate an ‘organic’ process of resolving policy issues within and across sectors in pursuit of broad policy goals.

LGIs in Bangladesh - An Overview: Development through the LGIs is a process to better understand the communities, and be more responsive to the perceived aspirations and constraints of the local people. The LGIs are more successful in promoting local participation and empowerment, democracy and development. The logic is that bringing decision making closer to the grassroots improves its applicability to local conditions, removes options for corruption, and improves accountability to beneficiaries. Development needs flexibility, accommodation, adaptability and learning which do not exist in a centralised blueprint approach. This is particularly the case in Bangladesh where it is difficult to administer effectively from the centre when problems are poorly understood, resources are scarce, and management systems inappropriate.

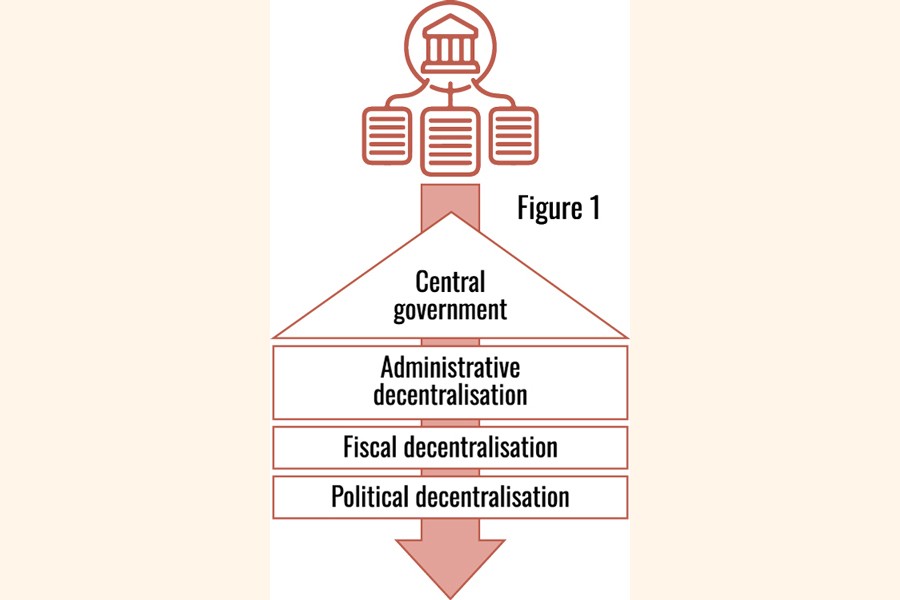

The process of decentralisation carries at least three distinct dimensions (Figure 1): political, administrative and fiscal. The political dimension refers to the transfer of authority from central to local authorities; the administrative dimension is the transfer of functional responsibilities from central to local authorities; while the fiscal dimension is concerned with the financial relationship between all levels of government. However, there are considerable overlaps between these dimensions. For instance, in order for economic gains from decentralisation to be realised, political decentralisation in terms of decision-making authority is a pre-condition.

The process of decentralisation carries at least three distinct dimensions (Figure 1): political, administrative and fiscal. The political dimension refers to the transfer of authority from central to local authorities; the administrative dimension is the transfer of functional responsibilities from central to local authorities; while the fiscal dimension is concerned with the financial relationship between all levels of government. However, there are considerable overlaps between these dimensions. For instance, in order for economic gains from decentralisation to be realised, political decentralisation in terms of decision-making authority is a pre-condition.

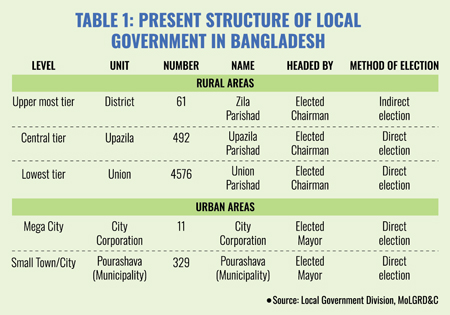

Bangladesh has two spheres of government—national and local. The local government system is enshrined in the Constitution and the main legislative texts include the Acts covering zila parishads (2000), upazila parishads (1998, amended 2009), union parishads (2009), pourashavas (2009), city corporations (2009) and hill district councils (1989). The Local Government Division (LGD) of the Ministry of Local Government Rural Development and Cooperatives (MOLGRD&C) is responsible for local government, with the exception of the hill district councils, which are under the Ministry of Hill Tract Affairs. There are 64 administrative districts, below which a tiered system of local government exists comprising single-tier urban authorities made up of 11 city corporations and 329 municipalities (pourashavas); and a three-tiered rural local government system comprising 61 zila (district) parishads, 492 upazila (sub-district) parishads, 4,573 union parishads, and three hill district parishads. All local governments have the power to levy taxes and rates and the range of functions for which the responsibility of each type of local government varies widely: from public health and hospitals, education and social welfare for city corporations and municipalities to the implementation of development activities, public libraries and roads for upazila and union parishads.

Thus, five LGIs function in the country. In the rural areas, Zila Parishad (ZP), Upazila Parishad (UZP) and Union Parishad (UP) function while, in the urban areas, City Corporation and Pourashavas operate (Table 1). Within the local government tier in the rural areas, the UZPs serve as the bridge between the central government and the roots level rural government and it can be a hub of people’s participation, leadership building as well as the testing laboratory of democracy in the country.

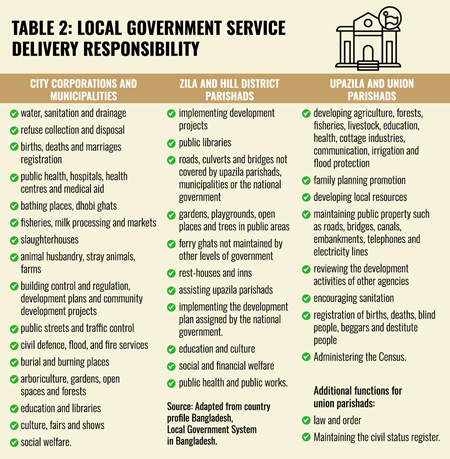

All local governments have the power to levy taxes and rates and the range of functions for which each type of authority is responsible varies widely: from public health and hospitals, education and social welfare for city corporations and municipalities to the implementation of development projects, public libraries and roads for upazila and union parishads (Table 2).

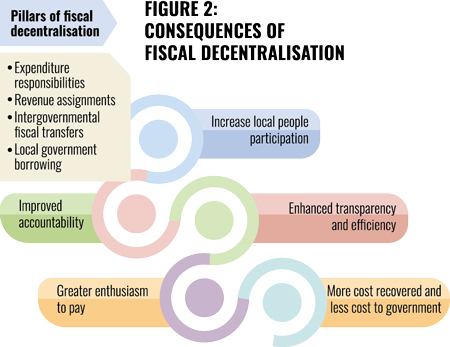

Programming Fiscal Decentralisation & Four Pillars: For effective fiscal decentralisation, a clear conception on four pillars is necessary. These are: (i) distribution of functions among different government levels; (ii) distribution of financial resources among different levels of government; (iii) designing intergovernmental transfers; and (iv) structuring sub-national borrowing/debt (Figure 2).

I. Distribution of functions among different government levels: The allocation of expenditure responsibilities is important to enhance accountability (who is responsible for what), avoid unproductive overlap, duplication of authority and legal challenges. The principle is: financing should follow functions. For distribution of functions, several criteria may be evoked: (i) efficiency criteria (or subsidiarity principle): providing goods and services at the lowest level of government that can efficiently deliver the good or service; (ii) service (or benefit) area: delivering services across political boundaries; (iii) economies of scale: extent to which the provision of a service at a smaller or larger scale affects the cost of the service; (iv) for some services (e.g. education and health) geographic and population size and diversity and high cultural value may require more centralised or controlled delivery. There is a clear choice in the case of national public goods (e. g. national defense, macroeconomic stability, etc.) and local public goods (e.g. municipal services such as waste collection, water distribution etc.).

I. Distribution of functions among different government levels: The allocation of expenditure responsibilities is important to enhance accountability (who is responsible for what), avoid unproductive overlap, duplication of authority and legal challenges. The principle is: financing should follow functions. For distribution of functions, several criteria may be evoked: (i) efficiency criteria (or subsidiarity principle): providing goods and services at the lowest level of government that can efficiently deliver the good or service; (ii) service (or benefit) area: delivering services across political boundaries; (iii) economies of scale: extent to which the provision of a service at a smaller or larger scale affects the cost of the service; (iv) for some services (e.g. education and health) geographic and population size and diversity and high cultural value may require more centralised or controlled delivery. There is a clear choice in the case of national public goods (e. g. national defense, macroeconomic stability, etc.) and local public goods (e.g. municipal services such as waste collection, water distribution etc.).

Challenges: Many goods may not fit these extreme categories; many goods may have to be evaluated on a multi-dimensional basis (e.g. producing a good or delivering a service; providing or administering the service; financing a service; setting standards, regulations or policies guiding the provision of services); unclear division of functions by level; economies of scale/spillovers; distribution may change over time.

Potential strategies: (i) Ensure clear and stable allocation of responsibilities; (ii) Keep focus on core services, and then devolve additional responsibilities incrementally; (iii) Link allocation of expenditure responsibilities to capacity; (iv) Identify performance indicators as sub-national governments are different in terms of population, expenditure capacity and revenue sources; (v) Phase in additional responsibilities to more competent sub-national authorities; (vi) Adopt a ranking system to classify the sub-national governments on the basis of technical financial, administrative, planning and policy capacities; and (vii) Regularly monitor implementation and adjust as necessary.

II. Distribution of financial resources among different levels of government: Efficient distribution ensures sub-national autonomy, promotes accountability and ownership, realises decentralisation efficiency gains, and facilitates cash flow management.

Principles for distribution of revenue sources: (i) Revenue potential (e.g. taxes that can respond to changes in population, income and inflation, and those that can provide a stable revenue base); (ii) Economic efficiency (revenue instruments to minimise economic distortions in investments, production, consumption, and local decisions); (iii) Equity (as equitable as possible, according either to the ability to pay principle, or to the benefits revenue principle); (iv) Administrative feasibility; and (v) Political acceptability (acceptable to various groups in the society).

Indicative pattern ofrevenue distribution: Central government source (corporate income tax, personal income tax, VAT, custom duties, etc.); Sub-national government sources (property tax, retail sales tax, motor vehicles, motor fuel tax, user charges etc.).

Key issues: Real revenue autonomy to sub national governments is likely to enable them to exercise their discretion over the tax base and rate.

Challenges: Weak revenue administration is the primary obstacle to successful sub-national revenue mobilisation. The problems include: lack of citizen credibility; lack of political will; absence of enforcement; incomplete, dated, or nonexistent revenue base information.

III. Designing intergovernmental transfers: The intergovernmental fiscal transfers from the central government to lower government levels may take a variety of forms:

(i) General purpose or unconditional transfers (transfers provided as general budget support)

(ii) Specific purpose or conditional transfers (transfers provide to undertake specific activities)

—matching vs. non-matching (matching-requires sub-national government to finance a portion of the expenditure through own revenue sources).

—open-ended vs. closed-ended matching (matching requirement open-ended—the sub-national government matches whatever level of funding provided by the central government; matching closed-ended—the sub-national government matches the funding provided by the central government only up to a pre-specified limit).

—input based conditionality vs. output based conditionality (input based conditionality—conditional transfers that specify the type of expenditure that can be financed; output based conditionality—conditional transfers that suppose sub-national government to attain a certain level of service delivery).

(iii) Revenue sharing (it is also considered as a transfer because local governments do not have control over the tax base, tax rate, tax collection or the sharing rate)

Avoid perverse incentives for fiscal management and accountability: Design the intergovernmental fiscal transfers in such a way that:

—keeps the transfer simple (this refers among others to the transfer formula that must be transparent)

—is based on credible factors and is as simple as possible

—focuses on single transfer objective

—introduces sunset clauses (especially in transitional arrangements)

—introduces output based conditional transfers

—introduces fiscal equalisation transfers

—develops an institutional arrangement for broad based consultation

The institutional framework to overlook fiscal transfers may be the grant commission, intergovernmental forum, or intergovernmental forum with participation of the civil society.

IV. Structuring sub-national borrowing/debt: Sub-national borrowing/debt refers to the capacity for sub-national governments to borrow money to cover their expenditure responsibilities.

Sources of borrowing: (i)Direct borrowing by central government and on-lending to sub-national tiers; (ii) Through a public intermediary or a state-owned financial institution; (iii) Direct borrowing from capital markets, national or foreign markets; and (iv) Through market decentralisation of public services, where possible. The key element to overcome the negative effects of sub-national borrowing is the design of the regulatory framework under which borrowing powers are decentralised.

Existing State of Fiscal Decentralisation: At present, all LGIs have the power to levy taxes and rates; and they are responsible for performing various functions and providing a range of services for which the mandate of each type of LGIs varies widely: from public health and hospitals, education and social welfare for city corporations and municipalities to the implementation of development projects, public libraries and roads for upazila and union parishads. Effective fiscal decentralisation, through earmarking revenue sources and providing revenue-earning power and authority to the LGIs, ensures that these institutions function effectively and efficiently and fulfill their mandates and service delivery responsibilities.

However, the existing state of fiscal decentralisation in Bangladesh is far from satisfactory. The introduction of decentralisation processes in the past allowed vast extension of central bureaucratic control and facilitated the stretching out of its authority to the sub-national level. Moreover, the LGIs paved the way of buttressing associations between the centrally and locally dominant classes. The arrangement of local government finance also reveals the very nature of resources accretion in a societal foundation where the political framework plays a powerful role in production activities. In addition, the gap between the works to be implemented by the local institutions and the existing resources (both from own sources as well as transfers from the central government) is huge and thereby the LGIs in Bangladesh are not very effective mainly due to the negligence of the concerns of fiscal decentralisation.

Research reveals that the lackluster local resources mobilisation performance of the LGIs does not lie in lack of commitment, rather in a lack of realistic fiscal devolution policy of the central authority to persuade LGIs in support of local revenue generation efforts. There exist untapped revenues that can be exploited with comprehensive efforts and incentive mechanisms. The central and the local governments can prioritise local resource mobilisation by recognising local probable sources, encouraging local people and creating a stake of local proprietorship on development schemes together with executive and regulatory supports. It is observed that, due to low tax collection and inadequate grants from the central government, LGIs cannot carry out and implement development activities as per their needs and deliver quality basic services to the local communities. This creates disappointments with the LGIs among the communities. The present fiscal decentralisation scenario lacks several basic features, such as efforts aiming to intensifying revenue sources, developing a pro-tax organisational culture and inclusion of citizens that are essential to empower the LGIs. Along with capacity building efforts, these are necessary to stimulate greater devolution of administrative and financial power to the LGIs.

In addition, the public financial management (PFM) practices in LGIs are fundamentally weak in relation to public expenditure and financial accountability (PEFA) standards. These weaknesses are spread across the board. While there are adequate laws and regulations and LGIs often make good effort to comply with these regulations, actual implementation is weak owing to severe financing constraint, major staffing and implementation capacity constraints, and inadequate monitoring, review and feedback processes. These constraints are over-arching and not specific just to PFM concerns; and these tend to lower the effectiveness of LGIs as a source of public service delivery.

Issues and Challenges: The history of local government in Bangladesh is characterised by heavy dependence on central government’s grants and strong bureaucratic domination because of asymmetric growth of bureaucratic power of the central government compared with the structure of the LGIs, despite some sporadic efforts to reorganise the relationships in the spirit of devolution of authority. Lack of accountability, such as open budget hearings and meetings and disclosure of LGIs information, is also responsible for corruption and weak administration at the local level. Moreover, dual accountability of the LGIs to the central government and the local constituency creates conflicts hindering the growth of the successful local government system.

Further, tension and conflicts between the Members of Parliament (MPs) and the local government representatives often aggravate due to the desire of the MPs to control local development efforts for their political benefits. According to upazila parishad and zila parishad laws, the MPs in their respective upazila and zila parishad constituencies have been made advisers. Hence, conflicts arise if the advice by the MPs is not accepted. The lack of commitment among different tiers of the government regarding the effective decentralised local government including lack of political commitment of the government on the desired structure of decentralisation and devolution of political and economic powers is also responsible for hindering the growth of the LGIs. The LGIs are established more to serve the partisan interests of the ruling system, rather than as true democratic institutions, to consolidate its narrow power base and respond to prevailing political compulsions.

The dominance and power of the local elite is also a major impediment for promoting good local governance and institutionalising democracy at the local level. The interest and power of the local political and economic elite act as a major force to create avenues for them to ensure favourable conditions for accessing the LGIs and participating in the local level decision-making process to serve their motives.As a result, despite decentralisation efforts of local government in Bangladesh, the LGIs mostly provide services under a centralised system like as in traditional top-down approach. Therefore, LGIs in Bangladesh play only a limited role in delivering services to its citizens due to limited decision-making and financial authority; lack of resources and staff; and weak capacity. Consequently, the LGIs fail to meet citizens’ needs and aspirations. But the global scenario is different where the LGIs provide basic services such as health, education, water supply and sanitation, and local law and order, along with many other local services. Bangladesh must empower the LGIs through administrative and fiscal decentralisation. Moreover, the LGIs suffer from weak public financial management practices, hindering their service delivery capabilities. In case of spending, the LGIs account for only about 7 per cent of total government expenditure. This relatively low share of LGIs spending in government total expenditure indicates limited fiscal decentralisation although decentralisation is a key component of the reform agenda in Bangladesh. Decentralisation has important implications on poverty alleviation, governance, and macroeconomic stability in Bangladesh.

There are three important issues in fiscal decentralisation: (i) revenue mobilisation and expenditure responsibilities; (ii) intergovernmental grants; and (iii) subnational borrowing. Generally, intergovernmental transfers are the most important source of revenues or all tiers of LGIs in Bangladesh. Several tax and charge back options are available to LGIs, but the revenue potential of these instruments and ability to collect taxes seriously constraint own revenue generation. Therefore, fiscal decentralisation requires taxing power at the local level to link benefits (services) and costs (taxes).

Citizens who pay taxes directly to the local government are more likely to hold local politicians and bureaucrats accountable. For improving accountability and avoid duplication, expenditure responsibilities at each level of government could also be defined as clearly as possible.

Issues in revenue mobilization. The common picture of LGIs is inadequate revenues to meet the targeted expenditures. Own revenues are constrained by several factors including: low revenue potential of LGI tax instruments; poor land record, low valuation and assessment rates; weak tax administration and unwillingness to pay. The national government holds almost all potent sources of tax revenues. The LGIs have access to only one major tax instrument: property tax in urban areas and land tax in rural areas. Both instruments are severely underdeveloped owing to poor land records, weak valuation techniques and very low tax rates. These tax rates and property valuation approach are regulated by the national government. The most important challenge in the area of revenue collection is unwillingness of taxpayers in complying with their tax obligations. This may be because of taxpayers’ lack of awareness and inability of tax collectors in explaining the tax obligations to the taxpayers. So for appropriate fiscal decentralisation, two main areas need to be emphasised: willingness to pay and improvement of LGI tax administration.

Issues in revenue mobilization. The common picture of LGIs is inadequate revenues to meet the targeted expenditures. Own revenues are constrained by several factors including: low revenue potential of LGI tax instruments; poor land record, low valuation and assessment rates; weak tax administration and unwillingness to pay. The national government holds almost all potent sources of tax revenues. The LGIs have access to only one major tax instrument: property tax in urban areas and land tax in rural areas. Both instruments are severely underdeveloped owing to poor land records, weak valuation techniques and very low tax rates. These tax rates and property valuation approach are regulated by the national government. The most important challenge in the area of revenue collection is unwillingness of taxpayers in complying with their tax obligations. This may be because of taxpayers’ lack of awareness and inability of tax collectors in explaining the tax obligations to the taxpayers. So for appropriate fiscal decentralisation, two main areas need to be emphasised: willingness to pay and improvement of LGI tax administration.

Issues in expenditure management. Since government transfers are the predominant source of funding for most LGIs, the predictability of these transfers and their timely release are a major determinant of the effectiveness of the budget execution and service delivery. Low own resources and delayed release of funds create tremendous budget implementation challenges for concerned LGIs. The quality of services are determined by the quality of expenditure management and it has several dimensions such as the adequacy of revenues, proper planning and setting of expenditure priorities and capacity to implement projects well. However, inadequate budget resources and delays in fund release create major problems in expenditure management.

Issues of accounting, recording and reporting. The current practice of LGIs accounts are mostly on a cash basis, which is not the best international practice. In addition, LGIs still largely maintain transaction records manually. They need to expand the use of ICT in accounting system. Further, ICT technologies need to be adopted in administration and service delivery monitoring.

Planning and budgeting issues. As decentralisation is important not just for specialists in governance-related areas, but also for sector specialists tasked with processing projects and technical assistance, so in the case of designing operations with decentralised government structures, the sector specialists need to consider local government capacities, local planning and budgeting practices, community or stakeholder involvement, and fiscal arrangements between various levels of government. In Bangladesh, there is no concept of asset management in the LGIs. City corporations and pourashavas own land and rentable assets that are not managed well including illegal occupation of city corporation and pourashava lands, questionable ways of renting assets, improper use of vehicles, and inadequate operation and maintenance practices to preserve office buildings and assets. In the case of budget execution, there are uncertainties in revenues owing to low own sources, weak tax compliance, large tax arrears, low government transfers and delays in transfer payments. Unpredictability of revenues weakens expenditure management and causes delays in implementation of development projects.

A Model for Fiscal Decentralisation: Globally, no unique model for fiscal decentralisation exists as diverse historical incidents are mostly responsible for fiscal decentralisation. Various countries have different structures and, therefore, fiscal decentralisation model of one country is not fully applicable for another. Developing applicable and effective fiscal decentralisation model for any country has to be research-based and country-specific.

Accordingly, various types of fiscal decentralisation exist in different countries such as, (i) self-financing or cost recovery through user charges; (ii) co-financing or co-production arrangements through which the users participate in providing services and infrastructure through monetary or labour contributions; (iii) expansion of local revenues through property or sales taxes, or indirect charges; (iv) intergovernmental transfers that shift general revenues from taxes collected by the central government to local governments for general or specific uses; and (v) authorisation of municipal borrowing and the mobilisation of either national or local government resources through loan guarantees. Worldwide, local government of some countries holds legal authority to impose taxes; however, in those cases, high dependence on central government transfers and limited scope to acquire tax revenues make the model unattractive. Certainly, investment by the public authorities needs to be well managed for encouraging higher private investment and making the best use of money.

Fiscal decentralisation is a widespread movement and can be segmented into administrative, fiscal, economic and political decentralisation. Fiscal decentralisation would have to be affiliated with administrative decentralisation but comparatively free from political and economic decentralisation. To develop a decentralised local government system in Bangladesh, descendent, strongly linked local and central government institutions system and good governance through local people’s participation and prioritising local needs are essential. Decision making and directly dealing with financial expenses is a key part of fiscal decentralisation. For conducting decentralised tasks, sufficient revenues are required by the local government through local revenue generation or transmitted from central government. While implementing a sound system of fiscal decentralisation requires macroeconomic stability, fiscal sustainability, a well-designed system of inter-governmental transfer and political consensus. For choosing a model which can run effectively and smoothly, simplicity of design and simplicity of role of different levels of governments are required.

Worldwide, there are four types of fiscal decentralisation model, such as, de-concentration, delegation, devolution and mixed models. For an effective decentralisation process, developing a road map and an appropriate work plan is very useful. With the existing challenges in the LGI’s structures and actions, both short and long term reforms are necessary in Bangladesh. In this context, several areas of reforms may be identified:

• Reduce dual taxation: Double taxation imposes high tax burden, which increases the cost of capital, reduces investment, and distorts business decisions. Synchronising local and central government taxation system can diminish dual taxation and inconsistent policies.

• Restructure resource allocations to LGIs: At present, there exists a huge gap between per head resource allocation between UPs and CCs or municipalities whereas, UZPs work with a large number of people and varied development related issues. Based on the significance of issues in UPs, the resource allocation of UZPs needs to be revised and enlarged.

• Enhance allocations to LGIs: The expenses of LGIs in Bangladesh are much below the average for the developing countries, still this is five times lesser than the average expenses in developing countries. This indicates inadequate fiscal decentralisation. Therefore, resource allocation for local government activities through own revenue or allocation from central government needs to be significantly increased.

• Strengthen monitoring of LGIs’ activities and audits: Local government’s taxation arrangements and financial issues need close monitoring and attention, as they directly deal with a large group of people and often may become corrupt and non-transparent. Each local government level needs to submit economic and physical performance reports to its higher level. For improving responsibility, the central government could issue orders focusing on financial transparency of local authorities.Verification of fixed assets needs to be carried out at least once a year and a fixed asset register has to be properly maintained. Often the audit reports of LGIs seriously lack quality and there is no supervision from higher level government on implementation of audit findings. Audits of LGIs’ accounts need to be conducted by recognised firms.

• Strengthen taxation power and capacity of LGIs: Often, actions taken by the LGIs face difficulties due to limited revenue earnings. By increasing the taxing power of LGIs, their working capacity can be increased corresponding to the localities’ demographics and specific requirements. In most cases, LGIs’ revenue earnings or taxing power remain static. The situation needs to be changed e.g. through ensuring regular updating holding and property tax and improving service delivery; sharing a higher proportion of the land transfer tax with the LGIs; enforcing more stringent legal measures for non-payment of taxes/fees; and discouraging the public legislative bodies to hinder tax collection process for fear of losing the electorates.

• Digitise land record keeping: For transparent land records and effective land markets, digitisation of land records saves time, cost and harassment. The digitisation process offers easier to administer contracts, paving the way for rapid development of a modern land market. In the absence of digitisation of land records and systematic updating of land values, tax earned at the time of land transaction becomes extremely understated. The process of digitisation of land records needs to be completed at the earliest for suitable administration of land or property holding tax.

• Introduce budget planning and forecasting: LGIs are required to provide superior services under limited budgets generated from local revenues, allocation from central government and various development partners. But often the LGIs remain unclear or out of the loop about the budgetary allocation from the central government or development partners. Sometimes late delivery of funds by the central government risks the project and incurs additional cost. This creates difficulties to plan upcoming development works by the LGIs. Therefore, the situation requires refining the way the central government or donors finance various projects of the LGIs. One approach could be to include a section in the national budget giving probable amount of financial allocations/transfers to the local governments along with the timeframe. In addition, financial forecasting is very crucial while preparing any plan. The purpose of the financial forecast is to evaluate current and future fiscal conditions to guide programmatic decisions. Local government staffs need to be highly skilled and have good knowledge about the local community requirements to forecast and plan financial matters according to the availability of fund.

• Ensure regular dissemination of information: Financial statements related to revenue (in terms of total collection and outstanding taxes) and expenses could be disseminated on a regular basis via local government’s web-site, so that the central government can allocate their funds accordingly.

• Improve understanding of financial matters by local government staffs: Imperfect resource mobilisation results for lack of skilled evaluators, loopholes in delivering tax invoices and futile tax collection processes. To avoid any miscalculation, staffs of local government need to be well trained and must have strong knowledge and capacity to develop effective budget planning. Local government authorities could also invest in staff capacity development programmes.

• Ensure better performance and service delivery by LGIs: For ensuring better service delivery, reforms are needed from the bottom to the top level. The specific strategies to improve service delivery include reforms in administrative management, increasing coordination among administration and elected representatives, developing institutional capacity and human resources, strong monitoring by the central government, skill and value development training of staff and enforcing law against corruption. Active participation of the local people in development programmes and increasing public-private partnerships can generate employment opportunities and improve service delivery.

• Motivate and strengthen supervisory committees: Properly functional supervisory committees can improve service delivery in response to specific demands of the communities. It can contribute to quality of administrative management, monitoring and supervision of the LGIs. For example, although as per regulation every UPs has 13 member standing committees, in most cases they are formed as procedural rather than requisite basis.

• Promote social responsibilities of LGIs: Along with tax collection or service charges by providing and refining public services, the LGIs could also build social structures, such as parks, markets, community centres, children’s play grounds, public halls etc., which can also facilitate revenue generation. This satisfies local social requirements along with generating revenues. Regular maintenance of these facilities is also very crucial. Efforts need to be made by the LGIs for creating green spaces and planned plantation to provide healthy environment and create sustainable and livable societies.

Concluding Remarks: Fiscal decentralisation holds many promises in Bangladesh – including democratisation at the local level and improved service delivery for the poor. But fiscal decentralisation is yet to deliver its promises; the positive impacts on citizen wellbeing, better governance and deeper democratisation are yet to be visible. The key to these can largely be found in ineffective implementation of fiscal decentralisation, which lags far behind the political rhetoric.

Concluding Remarks: Fiscal decentralisation holds many promises in Bangladesh – including democratisation at the local level and improved service delivery for the poor. But fiscal decentralisation is yet to deliver its promises; the positive impacts on citizen wellbeing, better governance and deeper democratisation are yet to be visible. The key to these can largely be found in ineffective implementation of fiscal decentralisation, which lags far behind the political rhetoric.

The effective delivery of fiscal decentralisation promises depends on a range of conditions and specific local contexts. It is much more than technical adjustments of the division of responsibilities between different levels of government; it is much about power and politics in the country. As such, it deserves much more attention from the policymakers in Bangladesh. It is true that many of the LGIs in Bangladesh have shown significant degrees of inefficiency, unaccountability and unresponsiveness in the past as providers of public services at the local level. Many LGIs also depend significantly on fiscal transfers from the central government. Since such fiscal dependency is likely to continue in the near future, it is important to make the transfers more predictable and transparent. Improving the coordination between the central government and the LGIs is an important aspect of fiscal decentralisation reforms in the country. Further, there is good scope for enhancing own revenues of the LGIs especially for city corporations, municipalities, and upazila parishads by improving the cost effectiveness of collection and reducing losses through evasion and corruption. For the purpose, a multifaceted approach and strong political support from the central government is necessary to improve administration capacity, encourage compliance, and reduce the scope for corruption and political interference.

Several key measures may be conceived:

• Improve the availability of good quality information, enhance opportunities for citizens to demand accountability;

• Establish a Local Government Financial and Fiscal Commission (LGFFC) that can coordinate, compile data, analyse and advice the LGIs and the central government;

• Simplify revenue collection processes and fee structures, for example for business licenses;

• Adopt a more pragmatic approach to property tax, taking account of the limited capacity of the relevant LGIs to undertake valuation and enforcement;

• Harmonise central and local government taxation to reduce double taxation and inconsistent policies.

The need is to better understand the technical issues and the political and economic dynamics influencing specific subnational contexts and revenue sources. Fiscal decentralisation in Bangladesh needs also to be based on more in-depth knowledge on the links between taxation, improved service delivery and accountability; and political economy of different revenue sources and their implications for business development and taxpayer compliance. The Implementation of the reforms needs also to recognise the benefits and costs of fiscal decentralisation and the preconditions necessary for successful reforms. The LGIs, on their part, have weak capacities relating to public financial management. These include, for example, limitations in planning and executing budgets, inadequate book keeping and financial reporting, lack of internal controls over cash management, and weaknesses in audit management process.

In addition, the LGIs still largely maintain transaction records manually. They need to expand the use of IT in accounting system and integrate with the government IBAS ++ system. Further, IT technologies could be used in administration and service delivery monitoring. Moreover, there could be further administrative and fiscal decentralisation; adequate staffing; stronger monitoring capacity; improved understanding of budget; multi-year budgets; timely release of budget transfers; expanded revenue collection efforts; and strengthened LGI audits. In view of the piece meal progress so far, this is probably the time for Bangladesh to come up with a national decentralisation policy encompassing all aspects— political, administrative, fiscal and economic—decentralisation in an integrated manner.

The available options and own source revenues differ across various kinds of local governments. Each government generally has a long list of potential revenue instruments comprising of various taxes, fees, and other income sources. However, in reality, many of these can generate little revenue and may cost as much to collect as they raise. Yet, the perception exists that local governments are failing to use their revenue raising ability. Even if the relative importance of these receipts vary according to the tier of the local government concerned, all of them, by and large, heavily depend on the transfers from the central government, partly due to the narrow base on which to raise their taxes, and partly inefficiency in collecting taxes, rates from these bases. Of the local resources, taxes constitute an important source of revenue for the local governments in Bangladesh. There are two ways of collecting local taxes and rates: by the local bodies themselves, and by the national government on their behalf. The central government then shares a portion of the revenue collected in the jurisdictions to the concerned local government. The list of the sources of revenues for the local governments based model tax schedules promulgated under different ordinances since 1976 is quite comprehensive. But, the actual exploitations of these sources by the respective local bodies are a far cry due to inappropriate choice of the tax base and the nature of grant these local bodies receive from the central government.

Dr Mustafa K Mujeri is Executive Director, Institute for Inclusive Finance and Development (InM). mujeri48@gmail.com

© 2026 - All Rights with The Financial Express