These were summarised in the regular IMF Executive Board Assessment (December 2023) as follows: "Directors called for a calibrated monetary policy tightening supported by a neutral fiscal stance and for greater exchange rate stability to restore near-term macroeconomic stability and bolster exchange resilience."

This deceptively short statement contains a number of suggestions, or what are sometimes called conditionalities, for some difficult policy changes in the monetary and fiscal sector which must be undertaken by Bangladesh Bank (henceforth BB) and the Ministry of Finance. The monetary and fiscal policy changes suggested are: (a) Monetary Policy tightening; (b) Neutral fiscal stance; (c) Exchange rate flexibility; (d) Macroeconomic stability; and (e) External resilience.

There were many other suggestions. The focus of this paper is only on the policy changes suggested for the monetary sector such as that fiscal changes are not discussed. Suffice it to say that the fiscal performance so far has been routine. The economic arguments in favour of these policies are succinctly narrated below. Monetary policy tightening essentially implies raising the interest rate and lowering the monetary growth. These should reduce the aggregate demand as some components of aggregate demand are interest sensitive and also less money reduces spending. Hence, an increase in the interest rate and lower monetary growth should contain the price level and bring down the inflation rate, which is the most important objective of the tightened policy.

The economic arguments in favour of these policies are succinctly narrated below. Monetary policy tightening essentially implies raising the interest rate and lowering the monetary growth. These should reduce the aggregate demand as some components of aggregate demand are interest sensitive and also less money reduces spending. Hence, an increase in the interest rate and lower monetary growth should contain the price level and bring down the inflation rate, which is the most important objective of the tightened policy.

A macroeconomic balance requires that aggregate expenditure equals aggregate income and foreign exchange receipts equal foreign exchange expenditure. The former maintains balance in the domestic market while the latter maintains balance in the external market. If these obtain there will be no pressure to push up inflation or disturb the balance of payments.

When the current account is in deficit and the import of goods and services exceeds the export of goods and services, the situation could be improved by a proper exchange rate management just as the proper management of price movements helps to reduce any market imbalance. Thus, exchange rate flexibility is an automatic stabiliser of the exchange market which ensures greater external resilience of the economy. It also helps to maintain the internal market stability.

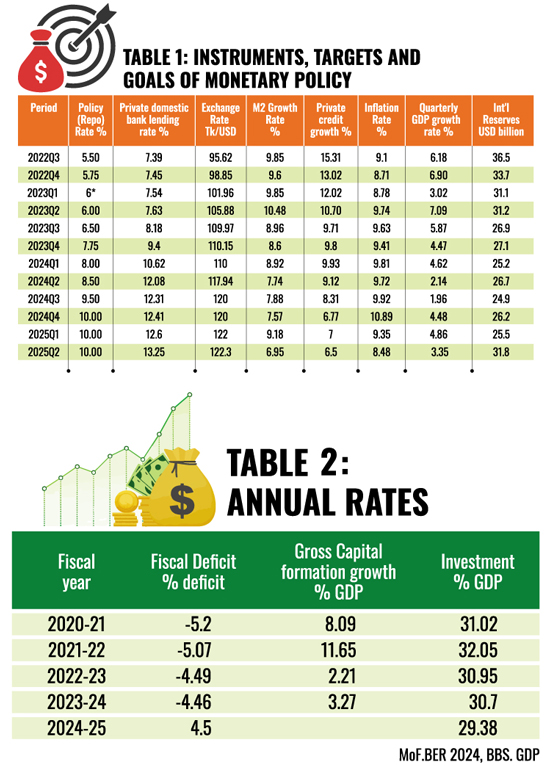

The government has only three instruments to stabilise a disequilibrium situation. These are interest rate, exchange rate, and fiscal measures. The first two are exercised in the policy domain of Bangladesh Bank while the third is the responsibility of the Ministry of Finance. Since the Agreement with IMF was signed two years and nine months ago, we have both quarterly and annual data of this period published by BB and Bangladesh Bureau of Statistics (BBS). We can utilise these data for a preliminary enquiry if the instruments at the disposal of Bangladesh Bank were appropriately utilised to move the economy toward the desired equilibrium path with minimum cost.

Table-1 provides quarterly data on the variables of interest since 2022Q3. As can be observed BB did not raise the policy interest rate (Repo) immediately after the signing of the agreement with IMF. It waited two quarters before increasing it to 6.5 per cent from the existing 6 per cent suggesting some initial doubts and anxiety about the consequences of raising the rate. Thereafter, the incremental changes became larger and quicker. By 2024Q4 the policy rate was pushed up to 10 per cent, a whopping 53.8 per cent increase in five quarters. It has not changed since then.

The policy rate had a cascading effect on all other interest rates. A rate of great concern to business is the domestic bank lending rate. It increased incrementally from 7.5 per cent in 2023Q1 to 13.25 per cent in 2025Q2, a substantial increase in seven quarters. The interest cost of business, especially investment, was thus raised considerably.

These changes helped to bring down the growth rate of broad money from 9.13 per cent in 2023Q1 to 7.88 per cent in 2024Q3, and further down to 6.95 per cent in 2025Q2. A similar trend is also observed for private credit growth during the same period. It declined from 12.02 per cent to 8.31 per cent and eventually to 6.5 per cent.

The Tk/USD exchange rate was fairly steady at just below Tk85/USD during the period of 2017-18 to 2020-21. But the next year it jumped to TK 93.45, and then to Tk 106 per US dollar. The large depreciation was perhaps due to the rapid worsening of the current account balance (deficit) which jumped to US$11.63 billion in 2021-22 from $9.57 billion in 2017-18.

The monetary policy changes have apparently succeeded in improving the macroeconomic balance in some respects. The international reserves rose to US$31.8 billion in June 2025 after falling precipitously to US$24.2 billion in May 2024. The current account improved from the very large deficit in 2021-22 to a modest surplus of US$149million by the end of 2024-25. Banks are more disciplined now than they were before because of better management and control. BB is also making efforts to rescue as many troubled banks as it can from the abyss of non-performing loans and limitless corruption to viability and recover at least some of the stolen money.

A close look at the table should convince anyone that the policies of BB have broadly followed the 'advice' of IMF. Unfortunately, despite all these difficult changes neither of the two major goals of its monetary policy was achieved in the last two and three-quarter years nor is IMF wholly satisfied. The inflation now is only marginally less than what it was when the agreement with IMF was signed. In between the inflation rate was always considerably higher exceeding double figure in several months. Even more worrying is the fact that gross domestic product (GDP) growth has declined steadily from 7.09 per cent in 2023Q2 to only 3.35 per cent in 2024-25Q4. World Bank data shows that the growth rate of gross capital formation in Bangladesh has sharply declined from 11.7 per cent in 2021-22 to 3.3 per cent in 2023-24. The investment rate fell steadily from 32.05 per cent in 2021-22 to only 29.38 per cent in 2024-25. This suggests a bleak outlook for output growth in the near term. It has steadily fallen from 7.1 per cent in 2021-22 to 3.97 per cent in 2024-25. Sporadic surveys by local organisations have revealed that a large section of the people has been pushed down into extreme poverty or poverty while a small number of people have vastly increased their fortunes. Thus, BB incurred the cost of implementing the suggested policy changes upfront, but yet to show any benefit.

Many countries that have taken such conditional loans from IMF have fallen into similar traps and consequently faced similar difficulties. This has given IMF a bad reputation. IMF would perhaps say that their recommendations were not fully realised and that it is always bad policies that gave rise to such economic problems. Unless such policies are rectified, the crisis situation would continue and might even get worse. Hence, the bitter pill of reform has to be administered.

The crisis that Bangladesh faced toward the end of the last regime was hardly due to any advice of IMF, it happened mainly because of the incompetence, lack of oversight and egregious criminal activities of people in power or in positions of strength. Although these people might appear to have disappeared from the country, there is no guarantee that they may not return again, or a similar group may not arise with support from both within and without. Only a competent government and unity of the people could prevent such an occurrence.

The author is an Adjunct Professor of Economics at Independent University of Bangladesh and a former Professor of Economics at University of Dhaka.

m_a_taslim@yahoo.com