![]() During his recent visit to Malaysia, Professor Muhammad Yunus, the Chief Advisor of the Government of Bangladesh, met with the Prime Minister, Dato' Seri Anwar bin Ibrahim, to discuss about developing Bangladesh's Halal industry. Professor Yunus also proposed establishing a dedicated Halal Economic Zone outside Dhaka to attract crucial Malaysian investments. Following this important initiative, we at IDEAS FOR DEVELOPMENT (IFD) are presenting a complete roadmap for building Bangladesh's Halal sector. Before we delve into the strategy, we first introduce the basic principles of the Halal industry.

During his recent visit to Malaysia, Professor Muhammad Yunus, the Chief Advisor of the Government of Bangladesh, met with the Prime Minister, Dato' Seri Anwar bin Ibrahim, to discuss about developing Bangladesh's Halal industry. Professor Yunus also proposed establishing a dedicated Halal Economic Zone outside Dhaka to attract crucial Malaysian investments. Following this important initiative, we at IDEAS FOR DEVELOPMENT (IFD) are presenting a complete roadmap for building Bangladesh's Halal sector. Before we delve into the strategy, we first introduce the basic principles of the Halal industry.

WHAT IS HALAL: "Halal" is an Arabic word that means "permissible". It denotes any item or action allowed for Muslims under Islamic law. The opposite term of Halal is "Haram", or "prohibited," which refers specifically to acts and consumables restricted by Sharia laws.

The International Islamic Fiqh Academy of the Organization of the Islamic Conference (OIC) provides comprehensive rulings to determine which foods and consumables are considered Haram. These rulings specify the following general conditions that must apply if a Muslim wishes to consume anymeat, drink or any other product:

• For meat consumption, the animal must be slaughtered while pronouncing Allah's name (Tasmiya), an act that cannot be replaced by a recorded invocation. For multiple animals, a single Tasmiya is permissible if the process is continuous; otherwise, the invocation must be repeated after any interruption;

• The slaughter must follow a prescribed method, i.e., cutting the animal's throat (for cattle, sheep, goat, and poultry) or plunging a knife into the base of the neck (for camels);

• The person performing the slaughter must be a Muslim or belong to the People of the Book (Jews or Christians);

• Mercy and gentleness must be shown toward the animal before, during, and after the slaughter. The sharpening of the instrument must not be done in front of the animal, nor should one animal be slaughtered in the presence of another;

• Slaughtering with a non-sharpened instrument is forbidden, and the animal must not be tortured. No part of the body should be cut off, skinned, thrown into boiling water, or plucked until it is confirmed to be completely dead;

• The animal must be free from any contagious diseases that would alter the quality of its flesh or pose a health risk to the consumer;

• Consumption is prohibited for animals killed by suffocation, a blunt object, a deadly fall (from an elevated spot or ravine), a blow from another animal's horn, or those devoured by untrained wild animals or birds of prey;

• Lawful slaughter should, in principle, be carried out without stunning. However, consuming the meat of a stunned animal is permissible only if it is technically certified that the animal did not die from the stunning operation before the final act of slaughter;

• In addition to the above, the consumption of blood, the flesh of dead (non-slaughtered) animals, and pork (pig meat) is explicitly Haram.

Apart from the general rulings on meat, the following standards apply to other consumables, derivatives, and services:

• The consumption and use of alcohol in food preparation, including cooking, are strictly prohibited (haram). However, exceptions exist for certain derivatives and external uses. There is no objection to using vinegar derived from alcohol. Furthermore, ethyl alcohol (ethanol) or other types of alcohol are permissible for cleaning equipment and tools used in food production and cosmetics, provided the equipment is subsequently washed with boiled water to ensure cleanliness.

In the realm of personal care, adding ethanol or other alcohols in the manufacturing of halal cosmetics is permissible, as long as the final product is not harmful. Alcohol is also permitted in oral and dental care products, such as mouthwash;

• Products derived from humans are strictly impermissible. This includes all substances extracted from the bodies of permissible animals-whether live or dead (e.g., cows, sheep, chickens)-for cosmetic manufacturing, such as embryos, cartilage, body fluids, amniotic fluid, umbilical cord, stem cells, and placenta;

• Products derived from permissible animals are generally acceptable. However, products from impermissible animals (e.g., pigs) are forbidden. Specifically, the use of pig-derived gelatin in foods is not allowed;

• Any animal-derived components used in food processing (e.g., glucose, amino acids, fatty acids, or additives) are only permissible if the source animal was slaughtered in compliance with Shariah standards;

• Manufacturing facilities for Halal and non-Halal foods must be strictly separated and distinct;

• Components from otherwise permissible animals are prohibited for use in cosmetic manufacturing if the animal was not slaughtered according to Shariah;

• Halal Tourism requires all associated facilities (hotels, restaurants, etc.) to adhere to the above ingredient and manufacturing guidelines. Additionally, these facilities must ensure that all food served is Halal, the availability and service of alcohol must be restricted, and prostitution or other illicit activities, such as, consumption of drugs and narcotics are strictly forbidden within the premises.

Consequently, achieving Halal status for consumables requires a comprehensive assessment of all production and manufacturing methods.

Ensuring this compliance depends on the relevant personnel-including butchers, chemists, engineers, and entrepreneurs-having the necessary specialised training.

Furthermore, certifying a product as Halal demands a robust blend of both religious and scientific knowledge in areas like chemistry, food sciences, and veterinary sciences. To guarantee integrity, government oversight is essential; thus the critical responsibility of monitoring Halal compliance should not be left solely to private parties.

THE SIZE OF GLOBAL HALAL INDUSTRY: The global Halal industry primarily encompasses the food, cosmetics, pharmaceuticals, and tourism sectors. While current global market size estimates are frequently cited at US$ 2.3 trillion, with projections reaching above US$ 4.0 trillion by 2030, these numbers must be viewed with caution. Such high estimates are not produced by any globally recognized body or organisation, and their derivation methodology often lacks clarity.

For example, simply aggregating the total meat production and consumption of the 57 member countries of the Organization of the Islamic Conference (OIC) to denote a "Global Halal Meat Market" would be grossly misleading. This misrepresentation stems from the fact that only 26 of these 57 member countries possess government-administered Halal Certification bodies, and only 14 of those maintain strict compliance monitoring.

Bangladesh, for instance, is one of the 26 countries with a government-run body to issue Halal Certificates. However, the nation currently lacks any domestic mandate requiring butchers, restaurant owners, cosmetics producers, and other private players to obtain this certification. The Islamic Foundation, the state-run body under the Ministry of Religious Affairs, reports that only 254 companies have received the certificate to date. Consequently, general citizens in Bangladesh consume domestic food and other items based merely on the assumption of Halal compliance.

A similar ambiguity exists in other OIC member countries like Pakistan, Afghanistan, and Turkiye. While Afghanistan does not have a government certification body at all, Pakistan and Turkiye-which do maintain such bodies-have not established domestic regulations compelling private businesses serving food, cosmetics, or tourism services to obtain Halal certificates.

Furthermore, demographic complexity affects market size calculation as well. In Malaysia, a country with a government-run certification body, the market cannot be entirely considered Halal due to its varied ethnic population. The same holds true for Uganda, an OIC member with a government-monitored system, where only 14 per cent of the population is Muslim; therefore, the entire meat, cosmetics, pharmaceutical and tourism markets in Uganda cannot be classified as Halal.

Despite these significant complexities in market estimation, it remains clear that the global Halal industry is large, dynamic, and continuously growing. More countries, including non-Muslim nations like China and Thailand, are actively showing interest in participating in the global Halal economy.

To avoid the complexities of estimating the size of the global halal industry and its growth dynamics, we will now shift our focus only to specific country examples to understand the market size and future growth outlook. Here we concentrate solely on the Halal meat market dynamics of two countries, Saudi Arabia and Pakistan.

SAUDI ARABIA: Saudi Arabia is one of the few Muslim countries that maintains robust government oversight of Halal compliance throughout its economy. The state-owned Saudi Food and Drug Authority (SFDA) enforces stringent monitoring mechanisms for ensuring Halal compliance across all domestic production and imports of food, cosmetics, and pharmaceuticals.

Exporting countries must adhere strictly to the import requirements set by the SFDA. The SFDA Halal Center manages certification, issuing Halal Certificates to both importers and domestic producers. If a certificate is issued by a third party, that entity must first receive formal recognition from the SFDA Halal Center.

Furthermore, SFDA regulations grant the authority the right to officially audit the operational procedures of exporting countries. This verifies that the exporting nation's legislative and regulatory systems comply with Saudi Arabia's extensive food law, technical regulations, standards, and animal and plant health codes.

The Saudi Arabian red meat market is robust, valued at US$ 5.66 billion in 2022, with an estimated 15 per cent increase in consumption during the year. In 2023, the Ministry of Environment, Water and Agriculture reported a significant increase in red meat production, surpassing 270,000 tons.

This domestic growth bolsters food security and aligns directly with the objectives of Saudi Vision 2030. The Kingdom has already achieved a 61 per cent self-sufficiency in red meat production, demonstrating its commitment to reducing import reliance. Further strengthening this goal, the government recently unveiled a US$ 2.4 billion mega project-an 11 million square meter livestock city. This ambitious development will include advanced facilities for raising livestock, feed factories, a veterinary hospital, and state-of-the-art processing plants, positioning Saudi Arabia to reach full self-sufficiency in meat production soon.

Crucially, the government ensures rigorous Shariah compliance by administering Halal slaughtering through certified facilities across the Kingdom, many of which are state-owned. This structured approach means informal slaughtering is virtually non-existent in Saudi Arabia, resulting in a system that is highly compliant with Shariah requirements.

PAKISTAN: Pakistan is establishing itself as a major Halal meat exporter among OIC member states. The country's Halal Certification is overseen by the Pakistan Halal Authority (PHA), established in 2016 under the Ministry of Science and Technology.

The government first allowed meat exports in 1998, with shipments gradually picking up pace after 2003. Total meat exports were initially modest, valued at only US$ 14 million in 2003. However, the sector has seen explosive growth: in FY2024, Halal meat exports hit a record high of USD$ 512 million, marking a 20 percent increase from US$ 426 million in the preceding year. This surge is attributed to a 24 per cent rise in export volume, which climbed from 99,892 tonnes to 123,515 tonnes. Strong international demand and competitive pricing, following a significant devaluation of the rupee, have fuelled this rapid expansion.

Beef constitutes the largest export sector, contributing approximately 70 per cent of total meat exports of Pakistan. The primary destination countries are heavily concentrated in the Middle East: the UAE tops the list with a 51 per cent share, followed by Saudi Arabia (16 per cent), Kuwait (12 per cent), Qatar (9 per cent), Bahrain (5.5 per cent), and Oman (3.3 per cent).

In 2023, Pakistani meat exporters received an average export price of Rs 1,083/Kg (USD 3.78/KG) in Saudi Arabia, slightly higher than the average price of Rs 1,015/KG (USD 3.54/KG) fetched in the UAE. Notably, almost 97% of these meat exports consisted of chilled or fresh meat, with the remainder being frozen.

Total domestic meat production, including beef, mutton, and poultry, reached 5.8 million tonnes in 2024, maintaining a Compound Annual Growth Rate (CAGR) of 3.9 per cent. Given that the country's meat consumption in 2022 was 3.5 million tonnes, the considerable surplus makes exports very important to maintain domestic prices, thereby ensuring the profitability of local livestock farmers.

STATE OF BANGLADESH'S HALAL INDUSTRY: Bangladesh currently maintains a theoretically non-existent domestic Halal economy because it lacks regulations requiring local entities-including food importers and producers, cosmetics manufacturers, and tourism providers-to obtain Halal Certificates before selling their products. Since compliance is not mandated, it is not guaranteed that local butchers, restaurant owners, and service providers are offering Halal goods. Citizens merely assume products are Halal due to the country's predominantly Muslim population.

Despite this domestic gap, Bangladesh exported US$843 million worth of Halal goods in 2022-23, though this volume was composed almost entirely of confectionary items. In contrast, Halal meat exports totalled a mere US$ 0.64 million during the same period, highlighting the sector's minimal global presence.

Recognising the need for a Halal framework mainly to promote exports to the Middle Eastern countries, the Government of Bangladesh enacted a comprehensive Halal Certification Policy in 2023. Developed with the involvement of religious scholars, the policy designates the Islamic Foundation to issue certificates upon demand from various private parties.

Specifically, Article 15.1 of the policy mandates a rigorous inspection process for every applicant. A dedicated committee-comprising a Mufti, a product specialist, and a government representative-must visit the premise to scrutinise all operational processes before a certificate can be issued.

Implementing proper domestic regulations based on this policy would unlock significant employment opportunities for Madrasah graduates, chemists, pharmacists, and veterinary specialists. For example, mandating that all restaurant owners hold Halal certificates would require the Islamic Foundation to establish branch offices nationwide to handle mass-scale issuance and scrutiny. Given the comprehensive nature of Shariah regulations, this change would also broaden the market for private Halal advisory services.

Furthermore, promoting a nationwide Halal economy requires the government to actively discourage informal slaughtering and invest in establishing formal, licensed slaughterhouses across the country. This systemic shift would create substantial investment opportunities for both public and private enterprises. Ultimately, a fully regulated system would serve as a significant mechanism for revenue generation for the government as well.

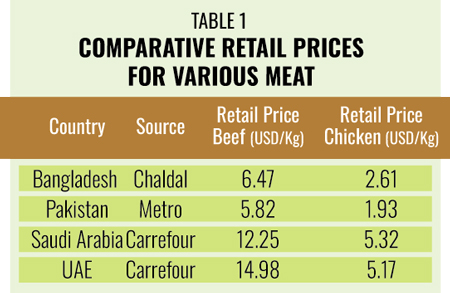

COMPETITIVENESS OF BANGLADESH IN HALAL MEAT INDUSTRY: Table-1 presents comparative retail prices for various meat products amongst Bangladesh and two major importing countries, i.e., Saudi Arabia and the UAE, and Pakistan, an emerging meat exporter to the Middle East. This allows us to assess Bangladesh's competitiveness in the global Halal meat industry. Although significant price differentials indicate strong export potential for Bangladesh in both markets, the analysis clearly shows that Pakistan offers more competitive rates.

COMPETITIVENESS OF BANGLADESH IN HALAL MEAT INDUSTRY: Table-1 presents comparative retail prices for various meat products amongst Bangladesh and two major importing countries, i.e., Saudi Arabia and the UAE, and Pakistan, an emerging meat exporter to the Middle East. This allows us to assess Bangladesh's competitiveness in the global Halal meat industry. Although significant price differentials indicate strong export potential for Bangladesh in both markets, the analysis clearly shows that Pakistan offers more competitive rates.

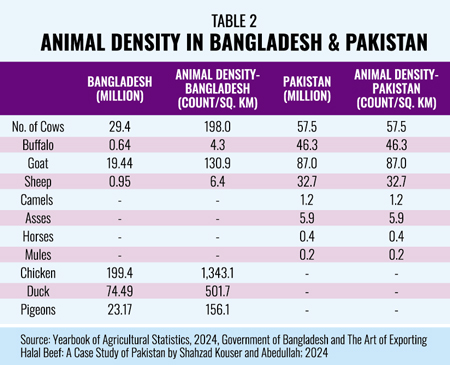

Table 2 shows that despite Pakistan being nearly 5.87 times the size of Bangladesh by land area, its animal density is much lower compared to Bangladesh for cows and goats, however, higher for buffaloes and sheep. This needs to be researched why Bangladesh's retail price for beef, a major potential export item, is higher than that of Pakistan despite having much higher density of cows. Moreover, Bangladesh significantly lacks capacity in number of buffaloes and sheep compared to Pakistan that also need to be analyzed.

A ROADMAP FOR BANGLADESH: To assess Bangladesh's strategy for penetrating the global Halal meat market, we propose the following roadmap.

A ROADMAP FOR BANGLADESH: To assess Bangladesh's strategy for penetrating the global Halal meat market, we propose the following roadmap.

Promote Domestic Halal Industry. To become a significant global player, Bangladesh must significantly increase the scale of its domestic Halal industry. Increasing scale is essential for driving production, creating demand, and ultimately reducing costs through economies of scale. Global footprint cannot be established with a handful of domestic actors; the number of market players will only grow with strong domestic demand. To meet this objective, our recommendations are as follows:

• The government must move past the current perception that Halal certification is purely a religious matter. Currently, the Islamic Foundation (under the Ministry of Religious Affairs) oversees certification. A better model is seen in Pakistan, where the Halal Authority operates under the Ministry of Science and Technology, reflecting a modern, scientific, and economic approach.

• Create a new, separate entity for issuing Halal certificates. This body must be equipped with Shariah scholars, product specialists, scientists, and veterinary experts. It should be led by an efficient, high-level government official.

• The government must enact and enforce regulations requiring private entities, importers, and service centres to obtain Halal certificates. This regulation should be phased in and encompass all relevant areas: Halal slaughtering, food service, cosmetic and pharmaceutical production/import, and Halal tourism services.

• Encourage religious scholars and government bodies to actively spread awareness through various media channels regarding Halal requirements as per Shariah law.

Raising Competitiveness of Halal Meat Industry. To improve the overall competitiveness of the domestic Halal meat industry, the Ministry of Commerce and Industries should immediately initiate a targeted research study. The preceding analysis indicates that while Bangladesh lags behind Pakistan in retail prices of meat, there may be significant room for improvement. This improvement is contingent on addressing the structural issues that prevent increased competition, which will be essential for realising cost-reducing economies of scale.

END NOTE: The global Halal industry became a subject of worldwide discussion primarily because Muslims in Western nations refused to compromise their religious requirements. When Muslims began migrating to countries like the US, the UK, and Europe in the 1960s and 1970s, there were few, if any, readily available Halal options. This scenario began to shift gradually as producers, manufacturers, and consumers became increasingly aware of this religious obligation and more sensitive to its compliance.

Today, Halal food is a recognised brand in major metropolitan centres like New York and London, where non-Muslims are also becoming regular consumers. The scale of this transformation is perhaps best shown through personal experience. The author recalls being a university student in the US in the early 2000s when finding a Halal restaurant required driving hundreds of miles. Most of the time having a McDonald's Fish Burger was the only viable option when eating out.

However, the world is dramatically different now. This market transformation is a direct consequence of strong consumer demand and the unwavering desire of Muslims all over the world to adhere to the requirements of their faith.

Mabroor Mahmood is the Founder of IDEAS FOR DEVELOPMENT (IFD). He can be reached at ideasfd@gmail.com

© 2026 - All Rights with The Financial Express