Despite these challenges, remittance inflows and export earnings have provided some relief. The balance of payments has improved, and foreign exchange reserves have stabilised. Yet, private investment remains subdued, and the banking sector continues to grapple with high levels of non-performing loans.

When Nobel Laureate Professor Muhammad Yunus assumed leadership of Bangladesh’s interim government in August 2024, the nation was brimming with hope. His appointment followed a historic student-led uprising that toppled a long-standing authoritarian regime. For many, it felt like the dawn of a new era—one that could replicate the transformative success of the Grameen Bank model, which had earned Professor Yunus global recognition for empowering the poor through microfinance. The expectation was clear: if Yunus could revolutionise rural finance, he could also steer Bangladesh toward inclusive governance, economic justice, and democratic renewal. His early initiatives—amnesty for political prisoners, formation of reform commissions, and promises of transparency—were welcomed as pragmatic steps toward rebuilding a broken state. While the initial momentum was strong—marked by the formation of 15 reform commissions and the repeal of controversial laws—progress has been uneven and often symbolic. Positive steps include restoring the independence of the Bangladesh Energy Regulatory Commission (BERC), cancelling politically motivated charges, and initiating electoral and constitutional reform processes. However, many commissions lack binding authority and bureaucratic resistance has stalled implementation. Reform agendas remain largely inspirational, with limited institutional follow-through.

However, as months passed, the dream began to unravel. The interim government underestimated the entrenched interests and institutional resistance that define Bangladesh’s political landscape. Reform commissions lacked enforcement power, and bureaucratic inertia stalled progress. What began as a people’s movement for justice and reform was soon hijacked by competing political factions. Opportunistic actors, some aligned with radical ideologies, used the transition period to consolidate influence. The interim government’s decision to delay elections until 2026, citing the need for reform, was met with fierce opposition from parties who feared a repeat of past manipulation. This power struggle eroded public trust and diverted attention from the reform agenda. The economic policies adopted by the interim government were widely criticised as poorly timed and misaligned with ground realities. VAT hikes on essential goods, a contractionary monetary stance, and lack of support for SMEs worsened inflation and unemployment. Instead of recovery, the economy slipped into stagnation, and the promise of inclusive growth faded.

A NATION AT A CROSSROADS: The initial optimism, that Bangladesh would be globally recognised for its bold reforms and democratic revival, has given way to frustration and fear. The very forces that once rallied behind Yunus now question the legitimacy of his leadership. The dream of a “New Bangladesh” is at risk—not because the vision was flawed, but because the political will to protect it was compromised by the very actors who sought power, not progress.

In the early days of the transition, the interim government articulated a reform agenda grounded in principles of transparency, equity, and civic participation. The establishment of multiple reform commissions, the release of political prisoners, and the commitment to judicial independence signalled a departure from the repressive practices of the previous regime. The metaphor of the nation as a family, invoked by Yunus in his inaugural address, resonated deeply with a population yearning for unity and justice. However, the trajectory of reform has since encountered significant obstacles, revealing the complexities of governance in a deeply polarized and institutionally fragile state.

BANGLADESH’S ECONOMIC TRAJECTORY —  GROWTH DECELERATION SIGNALS STRUCTURAL STRAIN: Bangladesh’s real gross domestic product (GDP) growth has slowed from 5.78 per cent in 2023 to 4.22 per cent in FY24, and further to 3.97 per cent in 2025. This deceleration reflects compounding pressures from post-COVID 19 recovery fatigue, global economic headwinds, and domestic structural weaknesses. Key drivers of the slowdown were external vulnerabilities, export demand softened amid global uncertainty, while remittance inflows fluctuated due to labour market shifts in host countries. Inflation and currency stress, persistent inflation and taka depreciation eroded purchasing power and investor confidence. Financial Sector Fragility, governance failures, rising non-performing loans (NPLs), and weak regulatory enforcement undermined credit flows and capital formation. Public investment bottlenecks, delays in infrastructure projects and fiscal constraints limited multiplier effects from government spending. Bangladesh stands at a pivotal juncture, while short-term growth has slowed, strategic reforms can unlock long-term resilience and inclusive prosperity. The policy path forward must balance stabilisation with transformation — based on transparency, innovation, and youth empowerment. In FY25, the sectoral composition of Bangladesh’s GDP was: agriculture 10.94 per cent, industry 37.44 per cent, and services 51.62 per cent. In FY24, these shares were 11.02 per cent, 37.95 per cent, and 51.02 per cent respectively—indicating a continued shift toward services and industry. The declining share of agriculture reflects urbanisation, labour migration, and productivity stagnation in rural areas. Industry’s modest rise signals resilience in manufacturing and construction, despite global headwinds. Services continue to dominate and driven by finance, education, health, ICT, and informal urban employment. Bangladesh’s economic transformation over the past two decades has been remarkable. From a low-income agrarian economy, it has emerged as a lower-middle income country with a vibrant manufacturing base and growing service sector. However, recent trends signal a risk of stagnation.

GROWTH DECELERATION SIGNALS STRUCTURAL STRAIN: Bangladesh’s real gross domestic product (GDP) growth has slowed from 5.78 per cent in 2023 to 4.22 per cent in FY24, and further to 3.97 per cent in 2025. This deceleration reflects compounding pressures from post-COVID 19 recovery fatigue, global economic headwinds, and domestic structural weaknesses. Key drivers of the slowdown were external vulnerabilities, export demand softened amid global uncertainty, while remittance inflows fluctuated due to labour market shifts in host countries. Inflation and currency stress, persistent inflation and taka depreciation eroded purchasing power and investor confidence. Financial Sector Fragility, governance failures, rising non-performing loans (NPLs), and weak regulatory enforcement undermined credit flows and capital formation. Public investment bottlenecks, delays in infrastructure projects and fiscal constraints limited multiplier effects from government spending. Bangladesh stands at a pivotal juncture, while short-term growth has slowed, strategic reforms can unlock long-term resilience and inclusive prosperity. The policy path forward must balance stabilisation with transformation — based on transparency, innovation, and youth empowerment. In FY25, the sectoral composition of Bangladesh’s GDP was: agriculture 10.94 per cent, industry 37.44 per cent, and services 51.62 per cent. In FY24, these shares were 11.02 per cent, 37.95 per cent, and 51.02 per cent respectively—indicating a continued shift toward services and industry. The declining share of agriculture reflects urbanisation, labour migration, and productivity stagnation in rural areas. Industry’s modest rise signals resilience in manufacturing and construction, despite global headwinds. Services continue to dominate and driven by finance, education, health, ICT, and informal urban employment. Bangladesh’s economic transformation over the past two decades has been remarkable. From a low-income agrarian economy, it has emerged as a lower-middle income country with a vibrant manufacturing base and growing service sector. However, recent trends signal a risk of stagnation.

Policy priorities by sectors need to invest in climate-resilient farming and irrigation. Promote agro-processing and rural entrepreneurship. Expand digital access and market linkages for farmers. Improve energy reliability and logistics infrastructure. Streamline industrial policy to attract foreign direct investment (FDI) and support SMEs. Strengthen technical education and labour productivity. Services sectors need to formalise informal sectors through digital registration and taxation. Scale up freelancing, ICT exports, and creative industries. Enhance service delivery in health, education, and finance. Bangladesh’s economy is increasingly service-oriented, with industry gaining ground and agriculture declining in relative weight. Strategic investment in productivity, innovation, and human capital across all sectors is essential to sustain inclusive growth. To escape the low-middle income trap, Bangladesh must boost productivity, diversify exports, invest in human capital, and reform institutions to sustain inclusive, innovation-driven growth.

BREAKING THE LOW-MIDDLE INCOME: Bangladesh’s transition from a low-income to lower-middle income country is a remarkable achievement. However, sustaining momentum and reaching high-income status requires overcoming structural barriers that often stall progress at the middle-income level. It’s a development plateau where countries experience slowing productivity and income growth after reaching middle-income status—unable to compete with low-wage economies in manufacturing or high-income economies in innovation.

STRATEGIC PILLARS FOR BANGLADESH’S ESCAPE:

Productivity-Led Growth. Need to upgrade technology and processes in agriculture, manufacturing, and services. Promote automation, digitization, and lean production in export industries. Encourage research and development through public-private partnerships.

Export Diversification. Move beyond RMG (ready-made garments) to IT services, agro-processing, pharmaceuticals, and light engineering. Improve trade logistics, customs efficiency, and regional connectivity. Negotiate preferential trade agreements to access new markets.

Human Capital Investment. Reform education to focus on skills, creativity, and digital literacy. Expand vocational training and freelancing platforms for youth employment. Improve healthcare access and nutrition to support a productive workforce.

Institutional Reform. Strengthen governance, rule of law, and anti-corruption mechanisms. Enhance public financial management and regulatory transparency. Foster policy continuity and investor confidence through inclusive dialogue.

Innovation And Entrepreneurship. Support startups and SMEs with access to finance, mentorship, and incubation. Build digital infrastructure and e-governance to reduce friction. Promote creative industries and knowledge economy sectors.

Urbanisation and Infrastructure. Develop smart cities, transport corridors, and energy grids. Ensure inclusive urban planning to absorb rural-urban migration. Invest in climate-resilient infrastructure to mitigate environmental risks. Bangladesh’s path to high-income status hinges on transformative reforms that unlock productivity, innovation, and institutional strength. Escaping the trap is not just about growth, it’s about quality, equity, and resilience.

Investment Requirements. Escaping the middle-income trap requires sustained, high-quality investment in infrastructure, human capital, innovation, and institutional reform. While there is no single “magic number,” global experience and economic modelling suggest the following: Target Investment-to-GDP Ratio: Current investment rate: ~27 per cent of GDP (as of FY24). Required rate: 30–35 per cent of GDP sustained over the next 10–15 years.

To break free from the middle-income trap, Bangladesh must not only increase the quantity of investment but also improve its quality and efficiency. Strategic allocation toward productivity-enhancing sectors, especially human capital, innovation, and infrastructure will be critical.

FINANCE & BANKING: Bangladesh’s banking sector is grappling with a deep-rooted structural crisis, starkly reflected in the alarming rise of defaulted loans. The proportion of defaulted loans in total outstanding credit climbed from 8.96 per cent in June 2022 to 24.13 per cent by March 2025. By September 2024, this figure had surged to nearly Tk 2.85 trillion, accounting for 16.93 per cent of total outstanding loans. This dramatic escalation underscores the man-made nature of the crisis, driven by a deeply entrenched culture of wilful default. Successive governments have reportedly enabled politically connected individuals and influential business figures—many implicated in money laundering—to evade accountability for financial misconduct.

Post-Interim Government Reforms And Capital Erosion. Following the formation of the interim government on August 8 2024, efforts were initiated to streamline Bangladesh’s banking sector, which had long been plagued by persistent structural challenges. One of the most alarming indicators of systemic fragility was the sharp decline in the capital-to-risk-weighted asset ratio (CRWA)—from 10.64 per cent in June 2024 to just 6.86 per cent by September 2024 (Bangladesh Bank, 2024). This steep drop signals a diminished ability of banks to absorb financial shocks, undermining their solvency and threatening the security of depositors’ funds. Under the BASEL III framework, Bangladesh Bank mandates that all banks maintain a minimum CRWA of 10 per cent, along with an additional capital conservation buffer of 2.5 per cent—bringing the total requirement to 12.5 per cent (Bangladesh Bank, 2024). The current shortfall thus places the sector well below regulatory thresholds, exposing it to heightened systemic risk. Specialized banks (SBs) and state-owned commercial banks (SCBs) have been key contributors to this capital erosion, largely due to their disproportionate exposure to high-risk assets. Their weakened capital positions not only reflect poor asset quality but also raise concerns about governance, risk management, and the long-term resilience of the banking system (Bangladesh Bank, 2024). High NPLS - a Structural Crisis. Non-performing loans (NPLs) defined as loans that are either in default or nearing default (Bangladesh Bank, 2017) have reached alarming levels in Bangladesh’s banking sector. As of September 2024, total NPLs stood at BDT 2.84 trillion, representing nearly 17 per cent of all outstanding loans (Bangladesh Bank, 2024). State-owned commercial banks (SCBs) reported the highest NPL ratio at 40.35 per cent, followed by specialised banks (SBs) at 13.21 per cent and private commercial banks (PCBs) at 11.88 per cent. Foreign commercial banks (FCBs) maintained the lowest NPL ratio at 4.99 per cent .

Weak monitoring of regular, rescheduled, and restructured loans, coupled with sluggish recovery efforts; (b) External shocks, including the Russia–Ukraine war, the Israel–Palestine conflict, and broader global and domestic economic pressures, which have eroded borrowers’ repayment capacity; (c) Governance failures, such as inadequate oversight and poor credit evaluation, which have enabled fraud and mismanagement; (d) Lax due diligence, with banks frequently extending credit to borrowers of questionable financial integrity; (e) Political interference, which has pressured banks into approving loans for non-creditworthy individuals; and (f) Ineffective recovery frameworks, which have failed to ensure timely and efficient debt collection. Many defaulters have reportedly transferred illicit funds to offshore accounts, allowing NPL volumes to persist and expand.

Reform Measures by Bangladesh Bank. In response to the deepening crisis in the banking sector, Bangladesh Bank has initiated a series of sweeping reforms aimed at restoring stability, integrity, and public trust as follows

Governance Overhaul. The boards of several banks have been reconstituted to curb the influence of politically connected business groups. This led to the removal of corrupt individuals from 14 bank boards.

Task Force Mobilisation: Three specialised task forces have been established to address systemic vulnerabilities: (i) Banking Sector Reforms Task Force; (ii) Central Bank Operations Task Force; and (iii) Stolen Asset Recovery Task Force. These bodies are focused on strengthening institutional accountability and operational resilience.

Asset Quality Review. A comprehensive review has been launched for banks with histories of corruption and malpractice to assess the extent of financial losses.

Asset Freezes & Recovery Efforts. Substantial liquid and tangible assets belonging to loan defaulters and suspected money launderers have been frozen to facilitate loan recovery.

Legal Strengthening. The Bank Resolution Ordinance of 2025 was introduced to reinforce the legal framework for managing banking crises.

Leadership Restructuring. Bangladesh Bank’s governor and board of directors have been newly appointed and reorganized to enhance governance and regulatory efficiency.

Institutional Capacity Building. A separate task force has been formed to bolster Bangladesh Bank’s enforcement capabilities and ensure regulatory compliance.

Preventive Measures Against Flight of Capital. Travel bans and account freezes have been imposed on all bank directors until full disclosure of stolen funds is made, preventing financial offenders from fleeing the country.

Data Transparency and Reporting Standards. To improve data accuracy and align with global best practices, Bangladesh Bank has adopted international standards for data management and shortened the overdue loan classification period from six months to three months.

Liquidity Support. The central bank has extended Tk 235 billion in special liquidity support to banks facing operational challenges.

CAPITAL MARKET REFORM AMID VOLATILITY: Bangladesh’s capital market comprises two fully automated stock exchanges—the Dhaka Stock Exchange (DSE) and the Chittagong Stock Exchange (CSE)—regulated by the Bangladesh Securities and Exchange Commission (BSEC). Over the past fifteen years, the DSE has experienced pronounced volatility, shaped by political transitions, economic policy shifts, regulatory interventions, and global market dynamics. Bangladesh’s capital market remains cautious but reform-driven, with recent policy measures such as margin rule updates, budget incentives, and structural reforms aimed at restoring investor confidence and regulatory integrity.

Following the July Revolution in 2024, the DSE’s performance from mid-2024 to early 2025 remained largely stagnant or slightly declining. This standstill was driven by the absence of bullish market catalysts, a lack of major initial public offerings, and delayed government responses. Although the interim government pledged to revitalize the capital market and reform BSEC operations, early implementation lagged, weakening investor sentiment. Retail investors, wary of policy uncertainty and market volatility, began reducing their holdings or exiting the market altogether. The benchmark DSEX index fell sharply in 2024, closing the year at 5,216.44 points—a 16.5 per cent decline from the previous year. Investor confidence continued to erode into early 2025, prompting many small investors to close their beneficiary owner (BO) accounts.

Despite the prolonged downturn, signs of short-term recovery emerged. The DSEX surged by 197 points (3.77 per cent) in a single session to reach 5,426 points—its largest one-day gain in over three years. The DS30 index, tracking blue-chip stocks, rose by 75 points (4 per cent) to 1,934. These movements signalled a temporary rebound in investor optimism, though the broader market environment remained cautious.

Calm before the Storm. The DSEX hovered around 6200, reflecting cautious optimism. Post-COVID recovery, remittance inflows, and stable monetary policy kept investor nerves in check during the period of December 2022 – October 2023.

Confidence Cracks: A sharp decline to 5200 signalled deepening concerns during November 2023 – April 2024. Rising inflation, currency depreciation, and banking sector irregularities eroded trust. Foreign portfolio outflows intensified the slide.

A modest rebound to ~5600 hinted at corrective measures—possibly central bank interventions or fiscal stimulus during May – July in 2024. But the rally lacked depth, with low trading volumes and tepid investor sentiment.

Gains reversed as structural issues—loan defaults, liquidity crunch, and governance gaps—resurfaced during August– October 2024. The market settled around 5300.

The index stabilised between 5200–5300 during November 2024 – May 2025. Investors adopted a wait-and-see stance, anticipating reforms ahead of the national budget and possible IMF program reviews.

To address structural weaknesses and restore confidence, several policy measures have recently been introduced:

Margin Rule Reform. The Capital Market Reform Task Force submitted final recommendations to modernize the Margin Rules, 1999. Investors must now have at least six months of experience and a minimum capital of Tk 10 lakh to qualify for margin trading.

Budgetary Support. The 2025–26 national budgets incorporated five key directives from the Chief Adviser, aimed at capital market development. These include tax incentives, regulatory streamlining, and liquidity support mechanisms, which BSEC has hailed as positive for market recovery.

Structural Reforms. The interim government has initiated decisive policy shifts, including loosening rigid administrative controls on interest rates, exchange rates, and stock prices. These reforms are expected to improve market dynamics and attract long-term investors. Together, these measures reflect a reform-driven approach to stabilising the capital market. While investor sentiment remains fragile, the alignment of regulatory action, fiscal incentives, and structural reforms offers a foundation for gradual recovery. Bangladesh’s capital market reforms in 2025 focus on restoring investor confidence, improving regulatory governance, and aligning with global standards. Key measures include BSEC restructuring, margin rule updates, tax incentives, and enhanced transparency.

Key Capital Market Reforms in Bangladesh (2025). The interim government and Bangladesh Securities and Exchange Commission (BSEC) have introduced a series of reforms to address prolonged stagnation and restore vitality to the capital market.

Institutional Restructuring. Reconstitution of BSEC leadership to reduce political influence and improve regulatory independence. Strengthening BSEC’s enforcement capacity through new task forces focused on compliance, surveillance, and investor protection. Margin Rule Modernization: The Margin Rules, 1999 have been revised to require investors to have at least six months of trading experience. Minimum Equity Requirement: Investors must have at least BDT 10 lakh in equity to qualify for margin loans. Experience Requirement: Investors must also have at least six months of trading experience in the secondary market. Risk Profiling: Institutions offering margin loans must conduct mandatory risk profiling before approving loans. Exclusions: Individuals without stable earnings—such as students, homemakers, and retirees—will generally be excluded unless they are classified as high-net-worth individuals. These proposals aim to promote responsible lending and reduce risk exposure in the capital market. Previously, margin loans were available to any investor regardless of investment size, typically at a 1:1 ratio of investment to loan.

Budgetary Incentives. The 2025–26 national budgets incorporated five key capital market directives: Tax incentives for listed companies. Reduced corporate tax rates for firms that go public, Incentives for long-term institutional investors; streamlined IPO approval processes. Liquidity support mechanisms for struggling brokerages.

Structural Reforms. Relaxation of administrative controls on, Interest rates, Exchange rates, Stock price movements. These reforms are designed to improve market efficiency and attract foreign investment.

Investor Protection. Travel bans and account freezes imposed on directors of troubled financial institutions to prevent capital flight; enhanced disclosure requirements for listed companies and intermediaries.

Transparency and Reporting: Bangladesh Bank and BSEC have adopted international standards for data management. The loan classification period has been reduced from six months to three months, aligning NPL reporting with global norms. These changes aim to reduce speculative trading and protect retail investors.

HEALTH: Bangladesh’s health sector is constrained by a combination of chronic underinvestment, weak governance, and rising disease burdens undermining its ability to deliver equitable, quality care. Health spending has hovered around 1-2 per cent of GDP for years. Bangladesh ranks lowest in South Asia in terms of public health spending as a share of GDP. WHO recommends a minimum of 5 per cent of GDP for public health expenditure to achieve Universal Health Coverage (UHC). Development allocation in health fell by 13 per cent, while non-development spending rose by 15 per cent, indicating a shift toward recurrent costs over long-term capacity building. In the Annual Development Program (ADP), health received BDT 181.48 billion (7.89 per cent of ADP)—a higher share but lower absolute allocation than FY2025, due to a contraction in the overall ADP envelope.

This low fiscal priority limits infrastructure expansion, workforce development, and service quality. The sector suffers from fragmented planning, poor execution, and limited accountability. Political instability and governance failures obstruct long-term reforms and disrupt project continuity. Allocations utilisations fell from 94 per cent in FY2014 to 80 per cent in FY2024, indicating inefficiencies in fund absorption, procurement, and implementation. Non-development expenditure mainly operational costs have outpaced development spending, curbing investment in preventive care and infrastructure. With low public spending, citizens bear a disproportionate financial burden, pushing many into poverty and deterring timely care-seeking. Moreover, stroke is now the leading cause of death (14.7 per cent), followed by heart and lung diseases. A nationwide survey found 11.39 per 1,000 people suffer from stroke, underscoring the urgency of NCD-focused interventions. The Health Sector Reform Commission (2025) outlined a roadmap for equity and efficiency but lacked actionable timelines and institutional accountability. Without robust implementation, the sector risks remaining trapped in a cycle of underperformance and reactive spending.

Need To Increase Allocation And Utilisation Of Health Budget. Prioritising development expenditure can enhance infrastructure, digital health, and preventive services. Improved utilization addresses chronic inefficiencies (e.g., 80 per cent budget use in FY2024). However, Budget expansion requires political will and fiscal space, which may be constrained by competing priorities (e.g., debt servicing, subsidies). Without institutional reform, increased allocation may not translate into improved outcomes.

Strengthen Primary Healthcare For UHC. Reduces out-of-pocket costs and improves access, especially in rural areas. Aligns with WHO’s emphasis on primary care as the backbone of UHC.

Expand Shasthyo Shurokkha Karmasuchi (Ssk) Nationwide. SSK offers financial protection for low-income households, addressing equity gaps. Builds on existing infrastructure and pilot learning, scaling requires robust data systems, inter-ministerial coordination, and sustainable financing. Risk of exclusion errors and administrative bottlenecks without digital integration.

Introduce Capitation-Based Funding Model. Capitation (fixed payment per patient) incentivizes efficiency and preventive care. Indonesia’s model shows promise in cost containment and service rationalization. Bangladesh’s fragmented health system may struggle with implementation. It also requires strong regulatory oversight and provider accountability mechanisms.

Impose Higher Taxes On Tobacco And Sugary Beverages. This has proven public health tools to reduce NCDs like stroke, diabetes, and heart disease. Government needs to generate revenue that can be earmarked for health spending. As there is a possibility of political resistance from industry lobbies and potential regressive impact on low-income consumers, complementary awareness campaigns and enforcement capacity is necessary. Aligning with WHO’s Framework Convention on Tobacco Control (FCTC) sends a strong normative signal about public health priorities. Enforcement may be politically sensitive, especially where tobacco-linked entities have philanthropic visibility. Needs clear guidelines and institutional commitment to avoid selective application.

Technology In Bangladesh’s Health Sector. To modernise healthcare delivery, the Ministry of Health and Family Welfare (MoHFW) has introduced the Bangladesh Digital Health Strategy 2023–2027, a comprehensive roadmap to accelerate the integration of digital technologies in the health sector (MoHFW, 2024). This strategy builds on a growing portfolio of digital initiatives already underway, including mobile health services and telemedicine in community clinics and union information and service centres. SMS-based platforms for patient feedback, pregnancy care guidance, and dissemination of health statistics. Hospital automation, electronic health records (EHRs), and an online population health registry. Attendance monitoring systems; human resource databases; and digital admission processing for medical and dental education are introduced. Bulk SMS systems, digital training platforms, and expanded internet connectivity across health facilities.

Despite these advancements, several structural and systemic barriers continue to hinder the full potential of digital health: such as budgetary allocations for digital innovation remain minimal, constraining the scale and sustainability of tech-driven reforms (Bangladesh Planning Commission, 2025). Limited digital literacy among health professionals: Many frontline workers lack the training to effectively use digital tools, reducing the impact of deployed technologies. Urban-rural digital divide, disparities in infrastructure and connectivity exacerbate health inequities, leaving rural populations underserved by digital health services. While the recommendations are well-aligned with global best practices, their success hinges on systemic reform, cross-sectoral coordination, and political commitment. Incremental implementation, backed by data and stakeholder engagement, will be key to translating these proposals into tangible health gains.

Education: Bangladesh’s education sector in 2025 is undergoing significant transformation yet faces persistent challenges. Despite increased budget allocations and policy reforms, issues related to quality, equity, and infrastructure remain prevalent. In the fiscal year in FY26, the government allocated Tk. 956.44 billion to the education sector, representing 12.10 per cent of the national budget and 1.72 per cent of GDP. This allocation is below UNESCO’s recommended 4–6 per cent of GDP and 15–20 per cent of the national budget. Primary and Mass Education received Tk 354.03 crore; Secondary and Higher Education Tk 475.63 billion; and Technical and Madrasa Education Tk 126.78 billion. Over 70 per cent of students in grades 2 and 3 struggle with basic skills, High dropout rates, especially among girls due to child marriage and socio-economic factors, quality of education, rote learning, outdated curricula, and lack of practical skills, infrastructure deficits, particularly in rural schools, teacher shortages and inadequate training, especially in STEM fields. Previous Initiatives: In the early 1990s Bangladesh made notable progress in advancing its education system through a series of key policy interventions, including the enactment of the Compulsory Primary Education Act of 1990, the introduction of the Female Secondary Education Stipend Programme, and the implementation of the Primary Education Development Programme (PEDP) (Khatun et al., 2025). According to the Annual Primary School Census (APSC) 2024, the country has a total of 118,607 primary schools (MoPME, 2025). Additionally, there are 21,086 secondary schools and approximately 171 universities across Bangladesh, comprising 55 public universities, 114 private universities, and 2 international universities (BANBEIS, 2024). Nevertheless, despite the large number of primary, secondary, and tertiary institutions, Bangladesh’s education sector continues to encounter multiple challenges. Bangladesh is currently experiencing signs of a youth bulge, indicating that the country stands at a critical juncture to harness the potential of its large young labour force and thereby realise the benefits of a demographic dividend (Khatun et al., 2025).

Previous Initiatives: In the early 1990s Bangladesh made notable progress in advancing its education system through a series of key policy interventions, including the enactment of the Compulsory Primary Education Act of 1990, the introduction of the Female Secondary Education Stipend Programme, and the implementation of the Primary Education Development Programme (PEDP) (Khatun et al., 2025). According to the Annual Primary School Census (APSC) 2024, the country has a total of 118,607 primary schools (MoPME, 2025). Additionally, there are 21,086 secondary schools and approximately 171 universities across Bangladesh, comprising 55 public universities, 114 private universities, and 2 international universities (BANBEIS, 2024). Nevertheless, despite the large number of primary, secondary, and tertiary institutions, Bangladesh’s education sector continues to encounter multiple challenges. Bangladesh is currently experiencing signs of a youth bulge, indicating that the country stands at a critical juncture to harness the potential of its large young labour force and thereby realise the benefits of a demographic dividend (Khatun et al., 2025).

Recent Government Initiatives: The government has launched several initiatives to address these challenges: School feeding programs in 150 upazilas to improve attendance and nutrition. Electronic Fund

SUMMARY AND INTER-CONNECTIONS: These sectors are deeply inter-linked: e.g., improved education (skills) supports technology and manufacturing; health supports workforce productivity; technology enables finance, trade, capital markets; a robust economy creates resources for social sectors. For Bangladesh to transition from middle income to high income (as per Vision 2041), progress across all these areas is essential — not just growth in one or two sectors. Many strategic imperatives emerge: diversify economy/trade, deepen financial sector, strengthen capital markets, improve education & health quality, build digital skills, promote innovation, ensure inclusive access (rural, women, disadvantaged).

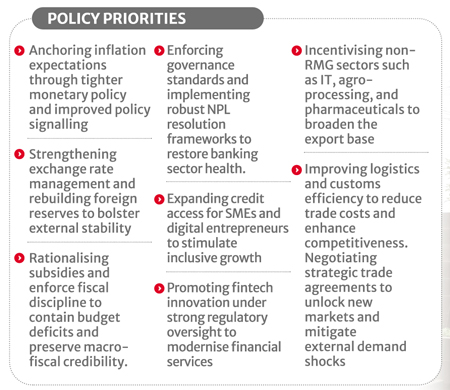

Policy Priorities For Recovery And Resilience. As Bangladesh navigates a challenging economic landscape, a coherent reform agenda is essential to restore stability and unlock long-term growth. The following policy priorities offer a roadmap for recovery and resilience:

Macroeconomic Stabilisation. Anchor inflation expectations through tighter monetary policy and improved policy signalling. Strengthen exchange rate management and rebuild foreign reserves to bolster external stability. Rationalise subsidies and enforce fiscal discipline to contain budget deficits and preserve macro-fiscal credibility.

Financial Sector Reform. Enforce governance standards and implement robust NPL resolution frameworks to restore banking sector health. Expand credit access for SMEs and digital entrepreneurs to stimulate inclusive growth. Promote fintech innovation under strong regulatory oversight to modernise financial services.

Export Diversification and Competitiveness. Incentivise non-RMG sectors such as IT, agro-processing, and pharmaceuticals to broaden the export base. Improve logistics and customs efficiency to reduce trade costs and enhance competitiveness. Negotiate strategic trade agreements to unlock new markets and mitigate external demand shocks.

Youth Employment and Freelancing Ecosystem. Scale up digital skill training and expand freelancing platforms to harness the demographic dividend. Provide seed funding and mentorship for tech startups to foster innovation and job creation. Integrate freelancing into national employment and education strategies to formalize and scale the sector.

Institutional Strengthening. Enhance transparency and accountability in public financial management to improve governance outcomes. Digitise service delivery and reduce bureaucratic friction to boost efficiency and citizen trust. Foster inclusive policy dialogue and reform ownership to build civic confidence and social cohesion.

Looking ahead, Bangladesh faces a pivotal moment. The upcoming LDC graduation in 2026 will redefine its global trade relationships, requiring strategic adaptation in compliance, competitiveness, and market diversification. The government must prioritise export diversification, especially in pharmaceuticals, IT services, and agro-processing.In the financial sector, restoring investor confidence will depend on regulatory reforms, transparency, and digital modernization. The capital market needs a robust framework to attract long-term investments and reduce volatility. Education and health must be treated as foundational pillars for inclusive growth. Increased budget allocations alone will not suffice—systemic reforms, accountability, and innovation are essential to improve outcomes. Technology offers a transformative pathway. With the right policies, Bangladesh can leapfrog into the global tech ecosystem, leveraging its young population and entrepreneurial spirit. Investments in AI, robotics, and biotech must be matched with capacity building and international partnerships.

Bangladesh stands at a crossroads in 2025. While economic challenges persist, the country is actively pursuing reforms across key sectors. With strategic investments in education, healthcare, and technology, and a renewed focus on transparency and innovation, Bangladesh has the potential to build a more resilient and inclusive future. Bangladesh’s path to resilience lies in bold, coordinated reforms that balance stabilization with transformation. The time to act is now. Without these corrective measures, the promise of a “New Bangladesh” risks becoming another missed opportunity.

Dr Sayera Younus is Senior Researcher, Centre for Policy Dialogue (CPD). sayera.younus@cpd.org.bd. She is indebted to Afrin and Ayesha, CPD, for their research assistance.