There is a growing demand for bonds in the country's financial market, and the existing tiny corporate bond market has still a long way to go to meet demand. Government bonds are also inadequate in meeting the growing appetite for bonds, though fixed-income government securities almost entirely dominate the bond market in Bangladesh. The need for corporate bond market diversification is urgent, as a lot of work is needed to widen the corporate bond market in Bangladesh to create a vibrant debt market. Diversifying the government bond segment of the debt market may help in this connection.

A bond is a fixed-income securities or debt instrument and is considered a low-risk option for investors. Return on the bond is generally low and fixed, so the bond market can function as a counterweight for a relatively high-risk equity market from where investors expect higher returns. The bond market is also less volatile and entirely predictable. The bond market has two parts: government and corporate or private. There is no doubt that without a more diversified corporate bond segment, no bond market can be vibrant, and government bonds alone can't create a competitive bond market.

Tradability is not just a desirable feature, but an essential one of a market that allows investors to buy and sell bonds freely or before maturity, providing liquidity and flexibility. In other words, a secondary bond market is not just necessary, but crucial for the bond market's functionality and growth.

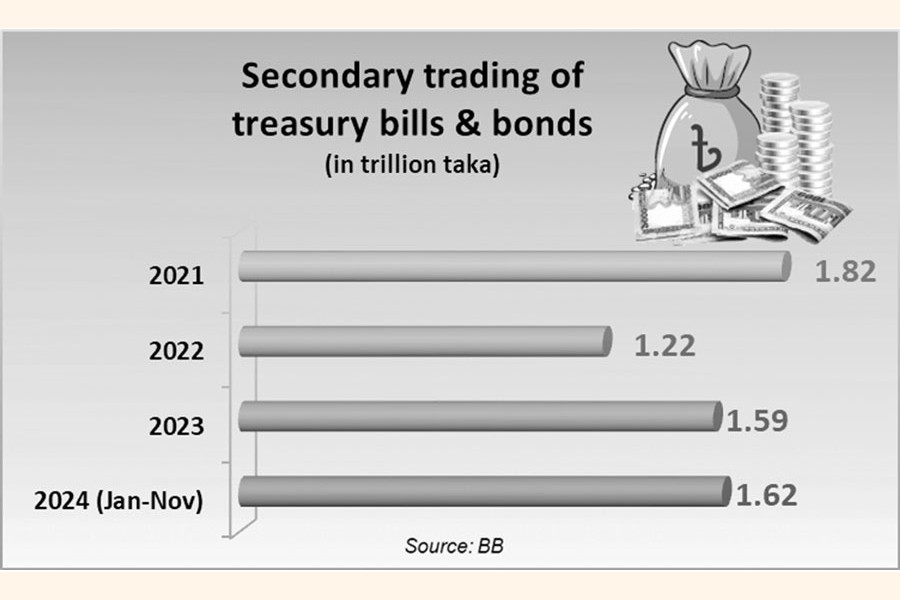

In Bangladesh, the ratio of outstanding fixed-income government securities stood around 20 per cent of the country's gross domestic product (GDP), of which around 12 per cent is tradable at the secondary market. In the 11 months of the current year, the total value of secondary transactions of these securities stood at Tk 1.62 trillion against Tk 1.59 trillion in the last year. Treasury bills and bonds with various maturity periods are tradable, fixed-income government securities.

At present, 14-day, 91-day, 182-day, and 364-day treasury bills and 2-year, 5-year, 10-year, 15-year, and 20-year treasury bonds are fixed-income tradable securities, which means all these bills and bonds are traded in the secondary market. Bangladesh Bank, on behalf of the government, uses these debt securities to borrow from banking sources to finance a significant portion of the budget deficit.

Non-tradable securities include four types of savings certificates (Sanchayapatras), Sanchaya bonds, and Prize bonds. These securities are used to borrow from the public to finance another major portion of the budget deficit. The ratio of outstanding savings certificates to GDP is around 8 percent.

A small amount of the budget deficit is being financed by foreign debt.

To diversify the government debt market, the government has already introduced Sukuk or Islamic bond. The first-ever Bangladesh Government Investment Sukuk (BGIS) was issued on December 28, 2020. The first one, an Ijarah (lease) Sukuk, was issued in 2020 to fund a project to provide safe drinking water to the public. The second one, also Ijarah (lease) Sukuk, was issued in 2021 for the development of infrastructure in government primary schools. The third, istisna'a (manufacturing) and Ijarah (lease) Sukuk, was issued in 2022 to finance the implementation of the Important Rural Infrastructure Development Project (IRIDP)-3 for social impact. The central bank is both the Special Purpose Vehicle (SPV) and the trustee of these Sukuks, which attracts those who want to invest in Sharia-complaint tools. Earlier in 2004, the Bangladesh Government Islamic Investment Bond (BGIIB) was issued.

A significant limitation of the government debt market is the lack of more tradable tools. For instance, there has been no initiative to make the various savings certificates tradable in the secondary market. These instruments, confined to the primary market, carry higher profit rates, creating a fiscal burden for the government in terms of interest repayment.

Making the savings certificates tradable in the secondary market will increase the number of tradable securities and also make the yield competitive by abandoning the administered mechanism of interest rate structure of these securities. At present, the minimum profit rate of these securities is 7.81 per cent in the first year, while the maximum rate is 11.56 per cent at maturity or the fifth year. Over the years, the government has rationalised the profit rates significantly and aligned them with the medium- and long-term government fixed-income tradable securities. For instance, the average yield of a 5-year treasury bond stood at 12.28 per cent in October this year. Thus, there is now adequate room to bring the saving certificates into the secondary market so that any investors can buy and sell it.

The government also needs to actively consider floating local government bonds to finance various development works of city corporations. This step not only enhances the local governments' accountability but also provides them with some financial independence. Municipal bonds, also known as 'muni bonds' or 'muni', are popular in many countries of the world and are issued by a government municipality, township, or state to finance its governmental projects. The potential for local government bonds in Bangladesh is promising and can significantly contribute to the bond market's growth.

The ousted Hasina government undertook a number of infrastructure projects in the last one and half decades. Instead of issuing bonds to finance some of these projects, it went for costly foreign financing. The costs of many of such projects had been inflated artificially to extract undue benefits by cronies. The net result is heavy debt burden on the country for long. If the government used these projects to diversify the debt market along with good governance, the financial market of the country might see some vibrancy.

asjadulk@gmail.com

© 2026 - All Rights with The Financial Express