Loan Default has a big impact on an economy. Obviously the impact is damaging to the financial institutions and to the economy of a country as well. As reported in December 2018, classified loans in the banking sector were to the tune of Tk 993.70 billion (99,370 crore) ; besides written-off loans were Tk 550 billion (55,000 crore) which means total classified loans amounted to about Tk 1.5 trillion (1,50,000 crore) only which is about one fourth of our national budget which is a matter of grave concern for our economy. Reasons of loan default are so many and negligence or improper creation of charge document is one of them. If proper charge creation is ensured over the assets of the borrower, a financial institution can take possession of the assets and execute sale to repay the loan.

A bank has to be very careful about documentation while disbursing loans and advances. Failing to ensure proper charge documents shall make the loans and advances legally unprotected. Moreover, (i) it procures a written evidence of transaction and hence cannot be disputed, (ii) it helps to identify the borrowers, co-borrowers and guarantors and their status, (iii) it helps identify security, (iv) it is acceptable as evidence in the court and (v) creation of charge documents gives a right to file suit. On the other hand, incomplete, inadequate or wrong documents affect a bank's interest adversely, recovery of advances becomes difficult and banks' position may be jeopardised in the court.

Inadequacies & complications which are common are in: (i) writing, (ii) format, (iii) signing, (iv) legal status, (v) date of document, (vi) stamping, (vii) witness/ guarantors, (viii) execution, (ix) verification of signature etc. So, bankers have to be cautious about charge documents such as (i) As far as possible, the charge documents should be hand-written with standard ink in an approved form in presence of bank officials, (ii) charge documents should not be handed over to the borrower/ any partner for obtaining signature, (iii) all charge documents should be signed in full signature and in the same style throughout the set. Initial or mark should not permitted at any place on the documents. (iv) all additions, insertions, alterations, cutting etc. must be properly authenticated under full signatures of the executors/borrowers. Overwriting, erasing in a document should not be allowed. (v) where document runs into several pages the borrower's signature should be obtained on each page, (vi) date of place of execution in each document should be mentioned invariably. The date of promissory note and the other relevant documents must be same, (vii) The column of the document should not be kept blank, (viii) the documents should be adequately and correctly stamped, (ix) if there is an annexure or schedule of securities in case of pledge or hypothecation, the same must be properly signed by the borrower, (x) if the borrower signs by left hand, a small note should be annexed to the documents regarding left hand signing, (xi) never obtain signature of the borrower on the guarantee form, (xii) the date of documents should be later than the date of stamp paper, (xiii) documents should neither be antedated nor postdated nor without date, (xiv) all executants should sign in a chronological order as per their name appearing on the face of the documents, (xv) the documents should not get punched, (xvi) all the documents' signature should be verified by wooden pencil. The concerned official of the bank must be well-trained with the process of documentation and execution to protect the bank's interest to avoid legal complications.

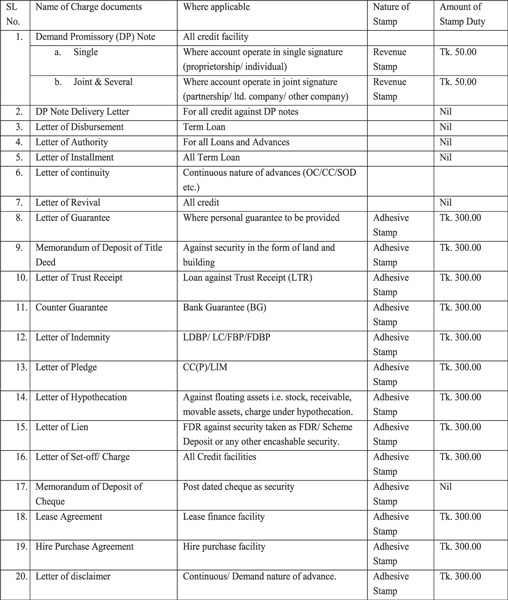

Some of the charge documents require stamp duty; stamp duty is a tax that is levied on documents. The duty rates vary depending on the types of instruments or nature of transactions and these may be flat charges or ad valorem charges (i.e. percentage of the value of the transaction). Stamp duties are payable on instruments such as tenancy agreements, bills of exchange, promissory notes, receipts, transfer agreements, mortgage, insurance policies, share capital, guarantees amongst others. The government is the only competent authority empowered to impose, charge and collect duties on eligible instruments if such instruments relate to matters executed between a company and an individual, group or body of individuals. In case of charge documents two types of stamps are used: (i) one is judicial and another is (ii) non-judicial whereas the judicial stamp is classified in two types such as (i) revenue stamp and (ii) adhesive stamp. A revenue stamp is attached to an item to indicate that government tax has been paid. An "adhesive stamp" is one which either has an adhesive on it when purchased, or which is intended to be affixed by adhesive to something. The following table shows the charge documents and stamp duty as per latest circular of government:

Some of the charge documents require stamp duty; stamp duty is a tax that is levied on documents. The duty rates vary depending on the types of instruments or nature of transactions and these may be flat charges or ad valorem charges (i.e. percentage of the value of the transaction). Stamp duties are payable on instruments such as tenancy agreements, bills of exchange, promissory notes, receipts, transfer agreements, mortgage, insurance policies, share capital, guarantees amongst others. The government is the only competent authority empowered to impose, charge and collect duties on eligible instruments if such instruments relate to matters executed between a company and an individual, group or body of individuals. In case of charge documents two types of stamps are used: (i) one is judicial and another is (ii) non-judicial whereas the judicial stamp is classified in two types such as (i) revenue stamp and (ii) adhesive stamp. A revenue stamp is attached to an item to indicate that government tax has been paid. An "adhesive stamp" is one which either has an adhesive on it when purchased, or which is intended to be affixed by adhesive to something. The following table shows the charge documents and stamp duty as per latest circular of government:

Note: Stamp duty is applicable as per stamp act as and when change. It is also be noted where adhesive stamp is not available, charge document can be executed using Non-Judicial Stamp of same value writing all context which is written in the respective charge document(s).

Awareness for creation of charge documents properly is surely conducive to protection of a bank's interest. Normally there is a sense of hurriedness observed in disbursing a loan after approval from the competent authority which might lead to improper creation of charge documents. All concerned officials' active vigilance will ensure further improvement and ultimately contribute to upholding a bank's interest and the country's wellbeing as well.

Muhammed Zahirul Alam is Deputy Managing Director, Small Medium and Retail Banking,

Bank Asia Limited, Corporate Office, Dhaka.

© 2026 - All Rights with The Financial Express