According to October 2020 report of IMF, Bangladesh is an emerging economic power of South Asia. Bangladesh is overtaking India in terms of per capita GDP scoring US$ 1888. Notably, in 2015, just five years ago, India's per capita GDP was around 40 per cent higher than Bangladesh's. While many countries in the world are experiencing negative growth due to the Covid-19 pandemic, Bangladesh is experiencing positive economic growth and it is now a matter of discussion in the media of neighbouring countries and beyond.

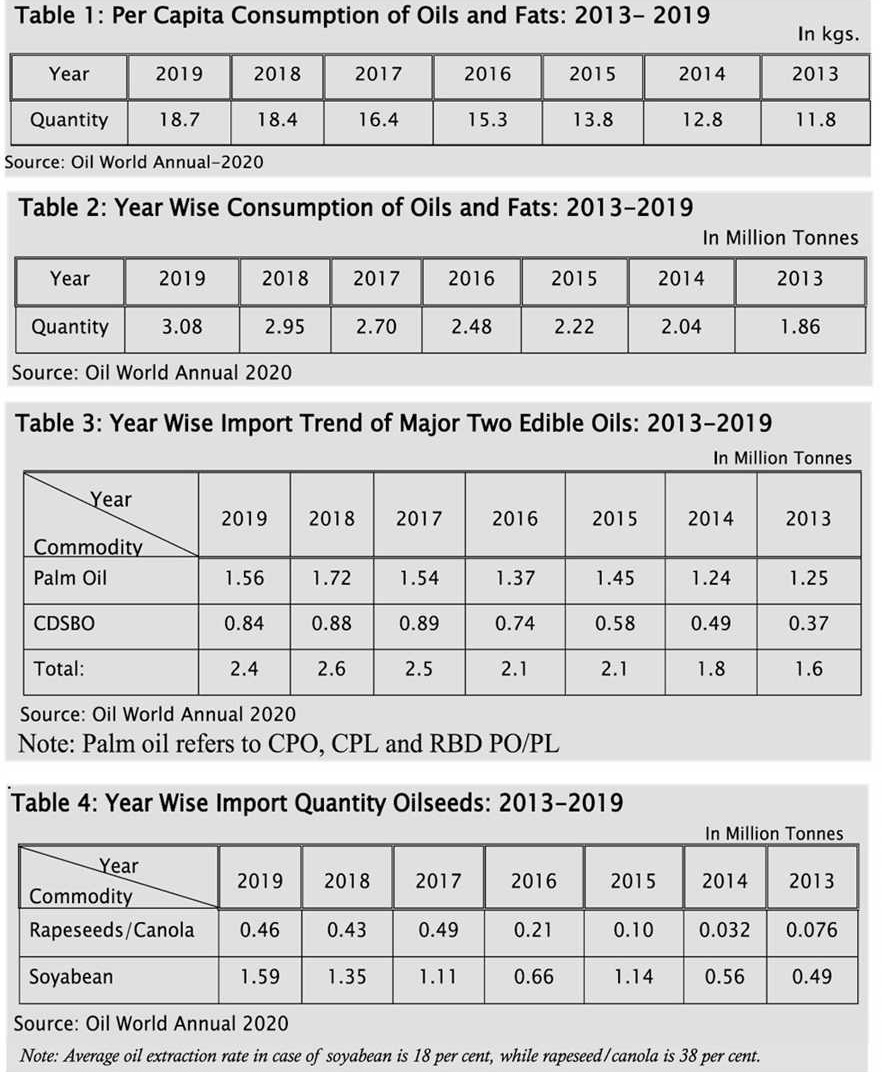

In pace with the economic progress, living standard and food habit of Bangladeshis are also changing. Urban people are now more inclined towards processed foods and eating in restaurants, eateries and in fast food shops. Standard of foods consumed by rural people, who constitute about 70 per cent of the 170 million population, are also changing. They now consume more oily foods compared to the past. All these changes contributed greatly to increased consumption of oils and fats during the last one decade. Country's per capita consumption increased to 18.9 kg in 2019 from 13.8 kg in 2015.

Market Overview:

Total consumption of oils and fats in the country increased little over 3.o million tonnes in 2019, of which about 97 per cent was for the edible purpose and the remaining 3.0 per cent for inedible purpose. In 2015 annual consumption vis-à-vis import was respectively 2.2 million tonnes and 2.3 million tonnes and that increased to 3.08 million tonnes and 2.8 tonnes in 2019. This could be translated that in 5 years' span of time consumption vis-à-vis import of oils and fats increased 40 per cent and 22 per cent respectively.

Bangladesh has a deficit in oils and fats since early '60s. It is an over-populated country with limited land for cultivation of oilseed crops. The land for oilseed cultivation is shrinking due to competition with food crops, which left no other choice but to import almost 90 per cent of country's annual requirement of oils and fats. Local production of oils and fats is about 350,000 tonnes against the present annual demand for little over 3.0 million tonnes. Among the locally produced edible oils, mustard oil is the major edible oil, which constitutes about 36 per cent of the indigenous production of edible oils. Other oils are rice bran oil, ground nut oil, coconut oil, sesame oil, etc. Soyabean is the 2nd largest oilseed crop produced in the country to the tune of 130,000 to 140,000 tonnes annually, but the entire quantity is used as poultry feed. Among other oilseeds crops are linseed, black cumin, etc. which are also produced in the country, but in a very insignificant quantity and having almost no contribution to the country's oils and fats production.

Accordingly, the country is almost 90 per cent dependent on imported oils and fats, which sees an upward trend in pace with increase of consumption. Consumption of oils and fats, in general, witnessed a growing trend, specially during last one decade, in pace with population growth, economic development vis-à-vis increase of purchasing power of the general consumers. Details on import trend of edible oils and oil seeds during 2013 to 2019 may be seen in Table 3 and Table 4.

Expected Oils and Fats Import vis-à-vis Consumption Scenario: 2020 to 2025

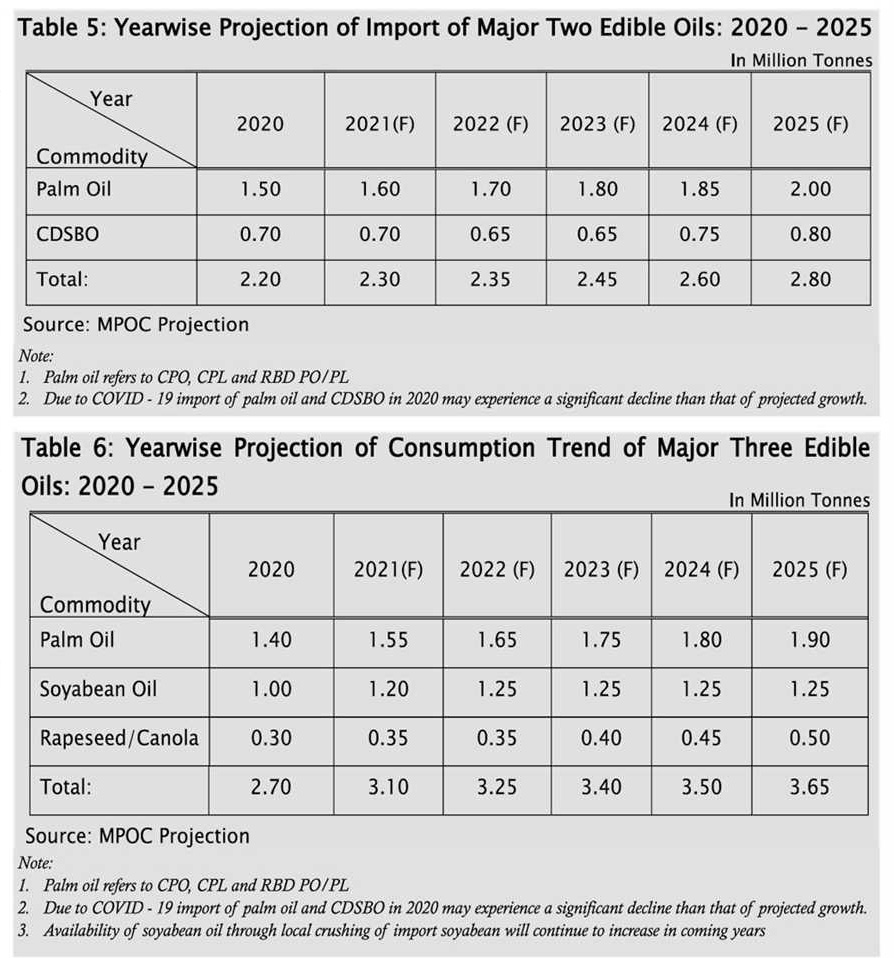

Bangladesh was experiencing a steady economic growth during the last couple of years, which contributed greatly to an increase in purchasing power of the general consumers' resulting significant increase in consumption of oils and fats. To meet the increasing demand, it is expected that the total import of oils and fats and oil seeds as well would increase in coming years.

It may be mentioned here that there are three major edible oils, namely palm oil, soyabean oil and rapeseed/mustard oil consumed in the country. Of these three major edible oils, palm oil has been the leading edible oil since 2003. During last couple of years, consumption vis-à-vis import of these three oils were found to be hovering at 53 per cent, 40 per cent and 7.0 per cent, on an average. Contrary to this trend, import of soyabean oil is likely to decline in coming years, while import of palm oil is likely to increase to meet the shortfall as well as the increasing local demand. Accordingly, annual consumption vis-à-vis ratio of these oils is expected to change in coming years.

Although import of edible oils in the country would increase in coming years, import of crude degummed soyabean oil (CDSBO) in the country in coming years may experience gradual decline due to the increasing trend in import of soyabean, which is used to produce feed meal for poultry and simultaneously contributing ro availability of crude soyabean oil locally at a cheaper price. While producing soya meal from soyabean, crude soyabean oil is obtained as a by-product at the rate of 20 per cent, on an average. Import of soyabean is exempted from payment of 15 per cent Value Added Tax (VAT), while imported crude soyabean oil is subject to 15 per cent VAT and accordingly, locally obtained crude soyabean oil is cheaper compared to imported crude degummed soyabean oil. Considering the aforesaid facts, projection on the growth of import of two major edible oils from 2020 to 2025 in Bangladesh is shown in Table - 5.

Consumption Trend: 2020 - 2025

Of the three major edible oils, which are consumed in the country, market potentials for palm oil in Bangladesh are wide compared to other two edible oils mainly because of price competitiveness. A major segment of the consumers of the country comprises mainly lower and lower- middle income people and hence the price of edible oils is an important factor for them. Accordingly, palm oil would continue to be a leading edible oil in the country. Considering the economic growth, increasing purchasing power, change of food habit, etc. projected consumption quantity of major three edible oil during 2020 to 2025 is shown in Table - 6.

Strength of Palm Oil:

i. Use of palm olein/super olein as cooking oil is the major consumption area of palm oil in this country. In pace with increase of population, change in food habit due to rapid urbanisation the consumption in this area would grow further.

ii. Vanaspati manufactures are the single largest industrial consumer of palm oil occupying about 30 per cent of total annual consumption of palm oil in the country. Consumption of shortening/ vanaspati would continue to see an upward trend in pace with increase of consumption of industrially processed foods.

iii. Industrial users, which include giant fast-food companies such as KFC, Pizza Hut, Nandos as well as local fast-food chain and numerous numbers of local bakery item producers, industrial food processors, fried snack food item producers, instant noodles producers, condensed milk producers, etc. are the loyal consumers of palm oil. In pace with the country's economic growth, change of food habit due to urbanisation, the consumption of palm oil in the aforesaid areas would also grow.

Considering the facts narrated above, it is most likely that import of palm oil in the country would continue to grow in coming years in pace with the increase in consumption vis-a-vis import of oils and fats and expected to cross the 2.0 million-tonne benchmark by 2025.

...........................................

AKM Fakhrul Alam is Regional Manager of Malaysian Palm Oil Council. fakhrul@mpoc.org.bd

© 2026 - All Rights with The Financial Express