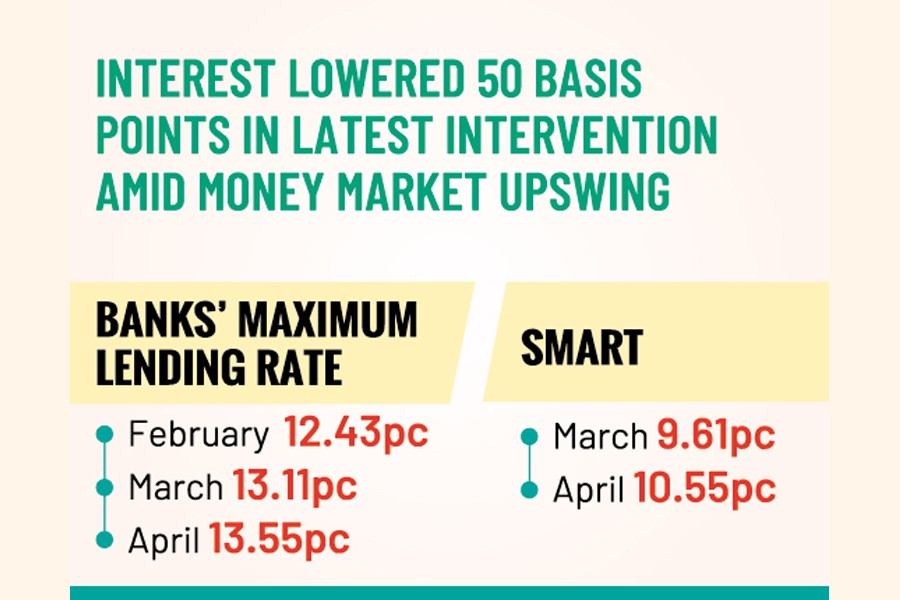

Formal credits become costlier yet as the maximum lending rate in the banking sector rises to 13.55 per cent for April amid significant push from the reference-rate SMART.

As the SMART (six-months moving average rate of treasury bill) rate climbed to 10.55 per cent applicable for April from the bygone March count of 9.61 per cent despite various cautious approach of the Bangladesh Bank, the central bank decided to reduce the interest-rate margin by 50 basis points to 3.0 per cent from the existing 3.50 per cent to ease the doing-business ambiance.

With the latest cut in interest margin, the maximum lending rate in the banking sector rose to 13.55 per cent for this month of April, 44-basis-point higher from March's 13.11 per cent. In February, the maximum lending rate was 12.43 per cent.

The central bank since early this fiscal (FY'24) has opted for interest rate-targeting regime from monetary targeting with the introduction of reference rate called SMART in the process of uncapping lending and deposit rates.

And banks have fixed the lending rate by adding maximum margin of 3.00 per cent to the SMART rate. So, if the SMART rate rises, the cost of formal credits will automatically go up.

Issuing a circular on Sunday, the central bank made the revision in the interest-rate margin asking the commercial banks to follow the instructions "immediately".

Apart from other regular loans, the maximum interest margin for pre-shipment export loan, and agriculture and rural loans also goes down 50 basis points to 2.0 per cent from the existing 2.50 per cent, according to the circular.

Seeking anonymity, a BB official said the SMART rate had continued rising since its introduction, which becomes a matter of concern for the businesses.

To ease the burden on private-sector enterprises in the current macroeconomic context, the official said, the central bank reduced the interest-rate margin twice (25 basis points on 29th February 2024 and 50 basis points on March 31, 2024) by 75 basis points so that the businesses can absorb the pressure.

Bankers apprehend that this will impact their profit margin as the existing cost of doing business remains high amidst the higher inflationary pressure on the economy and tight liquidity.

"Our profit margin will be affected badly," says Syed Mahbubur Rahman, managing director & CEO of a leading private commercial bank, Mutual Trust Bank PLC.

Mr. Rahman mentions that they have been procuring funds at higher cost as the money market has had liquidity shortages for long.

Economists say this is not right decision at a time when the inflation rate remained high. They feel that the central bank should take more time observing the market manners.

Dr Zahid Hussain, an independent economist, thinks the central bank has lost its patience under pressure from business circles.

"We should have learned from the best practices of the world. What do they do during such high inflationary pressures?"

He goes on asking rhetorical questions: "Could you give me an example where the central bank intervenes on lending rate under such higher inflationary pressure on the economy?"

He mentions that the lending rate just crossed 13-percent mark from the 9.0-percent cap.

"The objective of the SMART will not be attained once such twice reductions in the lending margin take place within five months."

In the meantime, businesspeople say that doing business under such a higher lending rate is difficult for many entrepreneurs. This type of SMART has been increasing by leaps and bounds since July last and nobody knows where it should end.

Anwar Ul Alam Chowdhury (Pervez), president of Bangladesh Chamber of Industries or BCI, was critical of the SMART system. "This is rising fast and the lending rate has increased sharply since July last," he lamented.

"How will we survive amid higher inflation? We are not making a profit now rather we want to survive," says the chamber chief.

He mentions that entrepreneurs have been facing problems following higher inflation in the economy. During inflationary pressures, during inflationary periods, prices are higher, and it is more expensive to borrow. For these reasons, companies cannot sell products as expected and the expansionary activity remained slow.

jasimharoon@yahoo.com and jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express