Bank deposits had a slower growth than that of credits in 2016 as depositors these days feel discouraged from putting money in banks for lower interest rates, sources said.

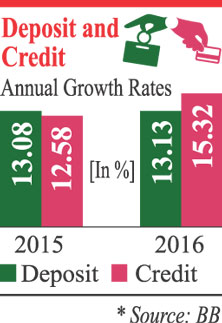

According to central bank statistics, the growth in deposits, on a year-on-year basis, rose to 13.13 per cent in the last calendar year from 13.08 per cent a year before while the credit growth increased to 15.32 per cent from 12.58per cent.

Deposit growth has been on a gradual decrease mainly due to lower interest rates, offered by the banks, according to the central bankers.

The growth rate of deposits came down to 13.5 per cent in September 2016 from 14.46 per cent at the end of June in the past year. It further came down to 13.13 per cent in December.

On the other hand, the credit growth climbed to 15.32 per cent in December from 14.5 per cent in September 2016. The rate was 15.42 in June.

Bankers and experts said depositors now feel encouraged to invest their money in government savings schemes and stock market for getting higher returns on their investments.

Some depositors also prefer non-banking financial institutions (NBFIs) to banks in depositing their money because the NBFIs rather offer higher interests on term deposits, they added.

The NBFIs are now offering interest rates on term deposits ranging between around 6.0 per cent and 16 per cent while the banks offer a near-negative 0.10 per cent to maximum 9.50 per cent.

The NBFIs are now allowed to collect fixed deposit from individuals and organisations for three months instead of previous term of six months.

The banks, however, offer interest rates on savings deposits ranging between 0.40 per cent and 6.0 per cent, according to the BB's latest monitoring report.

"Such falling trend in interest rates has pushed far down the overall deposit growth than credit growth in the banking sector," a senior official of the Bangladesh Bank (BB) explained.

He also said the deposit-growth rate fell slightly in the recent months following adjustment of loans with loans and 'push loans' particularly in small and medium enterprise (SME) sector.

Such comparative trends between deposits and credits had continued until February last, according to the central banker.

All banks' deposits, excluding inter-bank balance, rose to Tk 9088.64 billion as of last December from Tk 8583.31 billion as of June 30, 2016. The aggregate deposit amounted to Tk 8033billion as of December 2015.

On the other hand, their outstanding loans, excluding inter-bank balance, rose to Tk 6864.80 billion as of December 2016 from Tk 6421.74 billion. The amount was Tk 5953 billion in December 2015.

"Depositors, particularly small ones, are now losing interest in making further deposit with the banks mainly due to lower interest rates on deposits," former BB governor Salehuddin Ahmed told the FE.

Besides, such lower interest rates on deposits cast an adverse impact on people's savings habit, particularly in the banking system, Dr. Ahmed explained.

"Such discouraging savings tendency has also pushed up currency outside banks," the former governor said while explaining the impact on the financial front.

The overall currency outside banks (money kept in traditional caches instead of depositing into bank account) jumped by 22.27 per cent or Tk 206.08 billion to Tk 1131.53 billion in December 2016 from Tk 925.45 billion a year ago, the BB data showed.

Contacted for his remark on such a situation with savings, SK Sur Chowdhury, deputy governor of the BB, said the central bank had already issued a directive to the managing directors and chief executive officers (CEOs) of all the scheduled banks to remain proactive and help check the falling interest rates on deposits.

The latest BB move came against the backdrop of a faster decline in deposit rates than that of the lending rates.

The weighted average interest rates on deposits came down to 5.22 per cent in December 2016 from 5.39 per cent three months ago. It was paid at 5.54 per cent by the banks last June.

The weighted average deposit rate at more than 20 banks slipped below 5.0 per cent in December 2016, according to findings in the BB report.

On the other hand, the weighted average interest rates on lending came down to 9.93 per cent in December 2016 from 10.15 per cent three months before. It was 10.39 per cent in June last.

In January 2017, the weighted average interest rates on deposits came down to 5.13 per cent from 5.22 per cent a month before while the weighted average interest rates on lending fell to 9.85 per cent from 9.93 per cent.

"We've taken the latest measures to protect the interests of depositors," Mr. Sur Chowdhury told the FE while explaining the main objective of the moves.

It will also help discourage expenses in the less-productive sectors, the deputy noted.

He also said the falling trend in the interest rates on deposits affected the saving habit of the people, prompting them to spend on wasteful consumption and unproductive sectors.

However, the credit-deposit ratio (CDR) -- officially known as advance-deposit ratio (ADR) -- of all banks reached 71.85 as of December last from 71.59 per cent as of June 30. It was 70.98 per cent as of December 31, 2015.

The central bank of Bangladesh had earlier set the safe limit of CDR at 85 per cent for conventional banks and at 90 per cent for Sharia-based Islamic banks.

Talking to the FE, Syed Mahbubur Rahman, managing director (MD) and chief executive officer (CEO) of Dhaka Bank Limited, said: "Higher interest rates on savings instruments, offered by the government, have encouraged depositors to purchase the high-yielding instruments by withdrawing their bank deposits."

Currently, average interest rate on deposit, offered by the commercial banks, is more than 5.00 per cent, while the rate for savings instruments is paid on average 11 per cent, according to the senior banker.

"The banks may face problem to manage their funds in future if the existing trend in deposit growth continues," Mr. Rahman said, without elaborating on their possible cash position.

siddique.islam@gmail.com

© 2026 - All Rights with The Financial Express