The central bank unveils its monetary policy that, according to its outgoing governor, is cautious in stance and has a tightening bias.

The central bank unveils its monetary policy that, according to its outgoing governor, is cautious in stance and has a tightening bias.

It, however, is hopeful about maintaining support to economic recovery process and ensuring necessary flow of funds to economy's productive and employment generating activities.

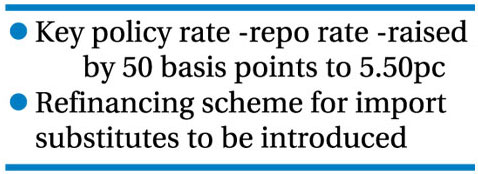

Under the policy announced Thursday, Bangladesh Bank (BB) increased its key policy rate - repurchase agreement (repo) rate -further by 50 basis points to 5.50 per cent aiming to curb inflationary pressure on the economy.

Earlier on May 29, the central bank had raised such interest rate for the first time in a decade to contain inflation The country's central bank will also introduce a new refinancing line of credit for import-substituting products to minimize import dependence and save foreign-exchange reserves.

The central bank will tighten its letter of credit (LC) margin rules for luxury goods, fruits, non-cereal foods, canned and processed foods with the margin hiked from the existing level of maximum 75 per cent to 100 per cent to discourage their imports.

"We've followed a cautious policy stance with a tightening bias to contain inflation and exchange-rate pressures while facilitating achieving optimum economic growth for the fiscal year (FY) 2022-23," outgoing BB Governor Fazle Kabir said while announcing the monetary policy statement (MPS) at the central bank headhunters in Dhaka.

Mr Kabir advised the new governor to review the MPS in the month of September or October, if necessary.

The central bank, however, says in its MPS that the ongoing 9.0-percent lending-rate cap might pose a challenge in the near future, saying that it would narrow down the interest spread to some extent.

"Under the current tight money-market condition with the increased cost of funds amid higher inflationary and exchange-rate pressures, keeping the lending-rate cap fixed at 9.0 per cent might pose a challenge in the near future as it will narrow down the interest-rate spread to some extent," the central bank explains in the MPS.

It also says the weighted average lending rates for all banks stood at 7.08 per cent as of May 2022, meaning that the 9.0-percent lending cap still has enough space for usual lending activities.

"Nonetheless, BB will remain watchful of this lending-cap issue and take policy actions if necessary," the central bank notes.

Earlier, the BB had instructed all the scheduled banks to fix a maximum 9.0-percent interest rate on all loans, except credit cards, as part of government initiative to bring down the rate to single digit from April 01, 2020.

Meanwhile, senior economists as well as the International Monetary Fund (IMF) already suggested the policymakers for phasing out cap on the lending and borrowing rates to help strengthen monetary transmission.

The latest BB moves came against the backdrop of rising trend in the inflationary pressure on the economy in recent months, following higher prices of both food and non-food items in lockstep with their global price rises.

The inflation - as measured by consumer price index (CPI) - rose to 5.99 per cent in May 2022 on a 12-month-average basis from 5.81 per cent a month before, according to the Bangladesh Bureau of Statistics (BBS) latest data.

The BB Modeling and Forecasting Unit's forecast and inflation expectation survey also show that a higher inflation trajectory will continue in FY'23.

"We'll not compromise in inflation with anything," the central bank chief said while replying to a query.

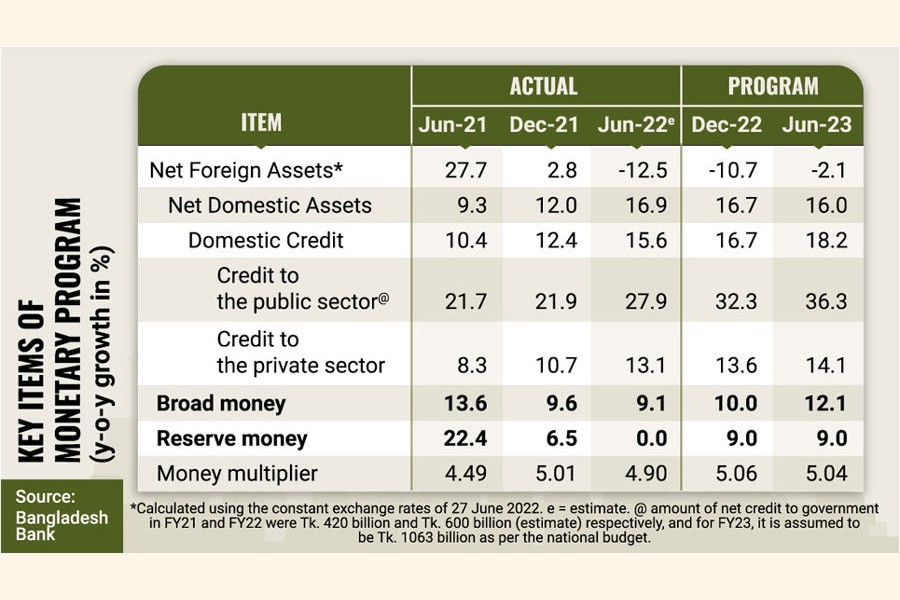

The central bank, however, fixed domestic credit-growth target at 18.2 per cent for FY '23 while goals of broad money (M2) supply and reserve money have been projected at 12.1 per cent and 9.0 per cent respectively.

The private-sector credit-growth target has been set at 13.6 per cent and 14.1 per cent respectively for the first half (H1) and the second half (H2) of the FY '23 while the public-sector credit growth at 32.3 per cent and 36.3 per cent respectively.

The central bank estimated the private-sector credit growth at 13.1 per cent in June. It was 1.70-percentage-point lower than the BB's target of 14.80 per cent for the second half (H2) of the outgoing fiscal.

"The private-sector credit-growth target is set at 14.1 per cent for FY'23, a bit higher than the actual growth in FY'22 and lower than last year's ceiling of 14.8 per cent, commensurate with some tightening bias while supporting investment, employment and growth as well," the BB explains.

It also says the implementation of the government's ongoing megaprojects, including the recent opening of the Padma Bridge, is expected to boost private investment and employment, beefing up the country's GDP.

The BB's monetary and credit programmes for FY'23 are designed to ensure adequate money and credit flows to support 7.5-percent real GDP (gross domestic product) growth while keeping inflation within the desired level at 5.6 per cent.

Regarding the foreign-exchange (forex) market, the MPS says the central bank intervened in the forex market throughout the year to ensure a market-aligned competitive rate.

As part of the moves, the BB sold around US$ 7.3 billion (net) during FY'22 (up to 28 June), while it bought US$7.7 billion (net) during the last year.

As of 28 June 2022, the country's foreign-exchange reserves stood at $41.9 billion compared with $46.4 billion at the end of June 2021.

Apart from containing inflation at tolerable levels, keeping import payments manageable and maintaining stability on the foreign-exchange market would be a critical challenge for the economy, according to the MPS.

Besides, the climate-and environment-related vulnerabilities, like the recent sudden floods in the North and Northeastern part of the country, could have some headwinds on the country's overall price stability and growth prospect, it notes.

Talking to the FE, Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development (InM), said essential products should be imported plan-wise to minimize impact of 'imported inflationary pressure' on the economy.

"The MPS tools are not becoming effective so much to contain the inflationary pressure on the economy," the senior economist said while replying to a query.

Mr Mujeri, also a former chief economist of the BB, said domestic production should be incentivized, like export-oriented industries, to discourage import-payment obligations in future.

siddique.islam@gmail.com

© 2026 - All Rights with The Financial Express