Government leaders often claim that the economy has suffered badly because of the 'sahinsa' (violent) movement carried out by the opposition 18-party combine in the months immediately before the largely voter-less election of 5th January, 2014. Media experts also echo their view with gay abandon. Public memory being short, the more recent events of the pre-5th January days are still fresh in mind, but what went on months or years before have already faded. Add to it the fact that the public are uninformed about complex economic matters, it is easy to see why they should be influenced by the facile assertions of the government and its supporting cohorts.

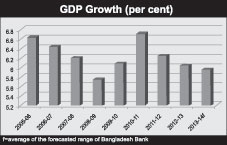

A close look at information provided by the government itself gives a somewhat different picture of how the economy has fared during the reign of the Awami League (AL)-led government since 2009. The national accounts data of Bangladesh Bureau of Statistics (BBS) show that the economy grew markedly between fiscal years (FYs) -- 2008-09 and 2010-11, but since then it has been on a declining trend (Chart below). There was virtually no political movement during FY 2011-12, but the largest fall in gross domestic product (GDP) was recorded during that year. Although some political disturbances began by the second half of the next year, the growth rate dipped by a smaller per centage.

There were widespread political agitations during the first half of 2013-14, but we shall not have official GDP data for this year for another three months. However, Bangladesh Bank (BB) has forecasted an even smaller reduction this year (the Finance Minister has actually predicted a substantial increase while the World Bank has forecasted a large decline). The export sector, especially apparels, was frequently claimed to be the hardest hit by the political events. It so happens that this sector will most likely post the highest growth rate of the last three years in FY 2013-14. There is little scope of attributing the declining trend solely or even mainly to political agitations, there were more serious challenges confronting the economy and business.

The world economy grew at 3.0 per cent in 2013 and is expected to grow at 3.7 per cent in 2014 (International Monetary Fund or IMF). Hence it is unlikely to impart any negative shock to our economy in the current fiscal year. One cannot fail to notice that the declining trend followed the revelations of a series of financial scandals. The first one to break news was the share market crash of December 2010. This was not a crash due to expectational errors or market corrections. It was deliberately engineered by a small group of people to defraud the share market investors of hundreds of billions of taka. Within only two and half months, the share market capitalisation lost Taka 1267 billion. Although a probe committee was set up, no action was taken against the perpetrators. The investors lost confidence in the market, the DGEN index kept on declining in fits and spurts for 30 months, and then remained stagnant for about another six months.

The share market crash was only a precursor of a series of financial scams on a gargantuan scale. The Hallmark-Sonali Bank loan scam, Destiny and other multi-level-marketing frauds, Padma Bridge corruption, Basic Bank scam etc., are all too well known to bear repetition. All these scandals, and importantly the failure of the government to take prompt action against the real perpetrators took their toll on business confidence. Business investment plummeted as evidenced by falling import of capital goods and sharply declining private credit. The fall in investment inexorably pulled down the growth rate of the economy.

The role of expectations is a widely discussed topic in economics and business studies. The centrality of expectations in business decisions is well established. Most business spending yield benefits in the future, and the size of the benefits depends very much on the state of things in the future. The future being inherently uncertain, business people have to form expectations of the future on the basis of information available currently.

These massive financial scams and bank frauds, the questions over the sustainability of the claim about the legitimacy of the government and its style of running the administration that has already resulted in unaccounted and uncontrolled corrupt practices are all part of the current information that go into forming business expectations. The prospect of these eventually leading to mass discontent and political agitations only add to the anxieties of business people and worsen their pessimism about the future. They hedge against possible adverse future outcomes by reducing current investment.

Acceleration of the rate of investment requires better business or investment friendly climate. Such climate can be provided only by rule of law and strong institutions, market friendly economic policies and good infrastructure. It is not hard to understand why Bangladesh ranks very low in attractiveness for business investment relative to countries of South-East Asia. The prospect of political instability unnerves the business community, both domestic and foreign, and erodes their confidence in the future of the economy.

A consequence of this is the abysmal rate of foreign direct investment (FDI) in Bangladesh. It cannot expect to raise the growth trajectory without substantial foreign investment. Empty words do not influence the business people seeking investment opportunities. The government needs to take concrete steps to improve business confidence. It needs to engage in sincere dialogues with all stakeholders in order to minimise the prospect of political instability.

The government seems to have opted for greater public investment in order to offset the lack of adequate private investment. The move for a two-and half trillion taka budget for the next fiscal year reflects such an intention. This cannot possibly improve the economic situation in the long term. The largest public investment project undertaken by the government is the construction of the Padma Bridge. A recent investigative report in a Bangla daily has revealed that the per kilometer cost of this bridge is three to five times greater than the cost of similar projects in some Asian and European countries. This gives some indication of the magnitude of wastages in public projects in Bangladesh due to inefficiency and outright corruption. Greater public investment will eventually pull down the productivity and the growth rate of the economy.

Another worry is that government expenditure once raised cannot be brought down easily. It is not uncommon in the developed countries to raise government spending during economic downturns to boost aggregate demand. However, the spending budgets in these countries are usually trimmed once the economy recovers. The government in a country such as Bangladesh will, on the other hand, attempt to maintain its newly acquired greater share of the economic pie. It will inevitably engage in competition with the private sector for more resources, which could eventually lead to greater inflationary pressures. This would weaken the foundation of accelerated economic growth. Past experience shows that it takes a long time to rebottle the inflation genie once it is out. The government should be very cautious about treading this path to economic development.

(The writer is Professor and chairman, Department

of Economics, University

of Dhaka. E-mail: m_a_taslim@yahoo.com)

© 2026 - All Rights with The Financial Express