Emergent entrepreneurs get into a quandary as countryside banking squeezes amid fallouts from uncapped high interest rates and obdurate inflation, thus affecting the overall national economy, sources say.

Of late, commercial banks' focus on rural Bangladesh keeps shifting with the disbursement of formal credits and the number of branches in the least-developed regions constantly shrinking, officials and bankers said.

Especially facing a dire predicament is cottage, micro, small and-medium enterprise (CMSME) sector in the rural areas as they are gradually losing their market.

Bankers cite several factors like rising cost of funds and production in this higher-interest and-inflation regime that dent the demand for credits in lockstep with the covid-induced shocks.

As a result, the flow of fresh disbursement in the rural communities continues receding in recent months. As a matter of fact, the banks, as part of their cost-cutting mechanism, keep reducing the number of rural outlets but serve their rural clients through agent banking.

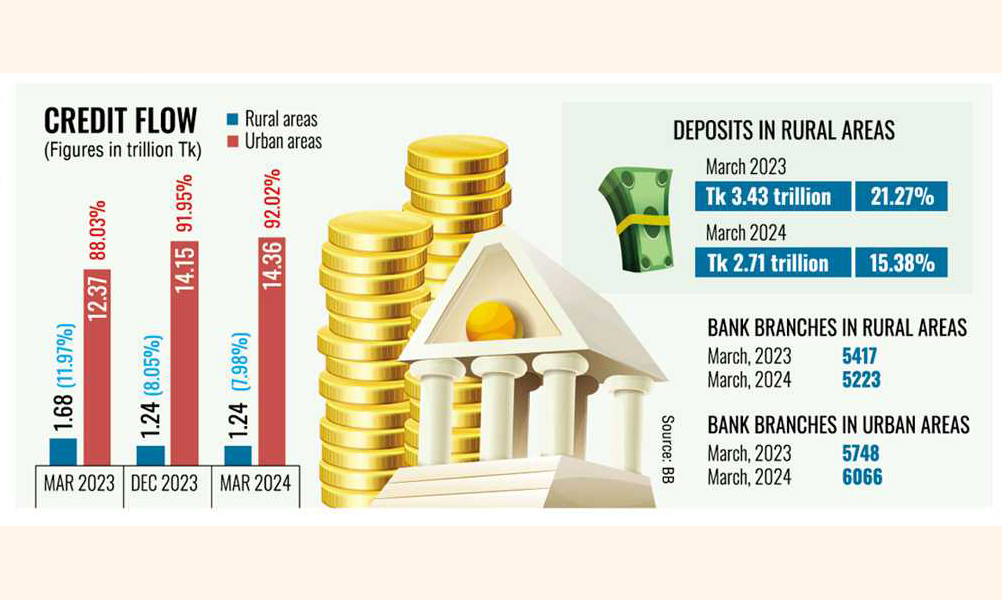

According to data available with Bangladesh Bank (BB), commercial banks altogether had invested Tk 14.05 trillion in various sectors across Bangladesh up to March 2023 when the share of rural areas was 11.97 per cent or Tk 1.68 trillion. The remaining part (Tk 12.37 trillion or 88.03 per cent) was invested in the urban regions.

The share of bank loans in rural territories continued to decline, reaching 8.05 per cent or Tk 1.24 trillion at the end of December 2023, while the share of urban areas in the same rose to 91.95 per cent or Tk 14.15 trillion.

The downtrend in disbursement of loan in rural areas continued further to stand at 7.98 per cent or Tk 1.25 trillion while the share of loans and advances in the urban areas rose to 92.02 per cent or Tk 14.36 trillion, the central bank data as of March 31, 2024 showed.

Seeking anonymity, a BB official said alongside disbursement of loans, the rural deposit portfolio in banks also dropped significantly in recent months probably because of higher inflationary pressure.

Citing data, the central banker said the share of rural deposits was 21.27 per cent or Tk 3.43 trillion until March 2023 but it dropped to 15.38 per cent or Tk 2.71 trillion by the end of March this year.

Not only the deposit and investment portfolios but also the number of rural bank branches declined significantly in recent times, having dropped to 5,223 till March 2024 from 5,417 recorded a year ago.

On the other hand, the number of urban branches rose to 6,066 in March this year from 5748 recorded a year earlier, according to BB data.

Contacted for his view, managing director of Shahjalal Islami Bank PLC Mosleh Uddin Ahmed said the central bank introduced refinancing schemes for the CMSMEs for assisting them in recovery from Covid-induced shocks. But the one-year-long funds have already been repaid and no fresh such refinance scheme has been introduced yet.

The experienced banker says the higher inflationary pressure and rising interest- rate regime badly affected the operations of CMSMEs and the result is obvious: cost of fund and production continues mounting.

"So, their (CMSMEs) products keep losing their competitiveness with the imported goods, which is probably another reason behind the falling demand for credits in rural regions," he says about the shifting dynamics of the economy.

Regarding the falling number of rural branches, Mr. Ahmed says maintaining full-scale rural branches under the current liquidity tightness has become costly and unviable for any commercial bank.

"I think financial inclusion like agent banking is the right instrument for rural development now," he adds.

Top executive of Dhaka Bank PLC Emranul Huq thinks the growth of CMSMEs remains stymied in recent months as the rate of fresh disbursement keeps falling.

He says the rate of interest for bank credits has increased significantly since June last year amid the central bank's contractionary monetary stance to contain inflation, which naturally enhances the cost of fund and production for the rural enterprises.

"This could be a reason behind falling demand for credit in rural areas."

President of Barisal Metropolitan Chamber of Commerce and Industry (BMCCI) Mohammad Nizam Uddin says the entrepreneurs in the region, particularly in the rural areas, have been severely suffering due to poor access to formal credits over the years.

"We keep requesting the higher bank officials about the pains, but nobody listens to us even though entrepreneurs have all the documents required for getting funds. I don't know why the bankers are so shy in giving credit," he adds.

"Because of the reluctance of top bank management to give loans to rural areas, the entrepreneurs are getting demoralised for not receiving the bank finance, which is the key to industrial and employment growth," the business leader observes.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express