Foreign direct investment in Bangladesh has been on a prolonged slowdown with worrisome macroeconomic implications notwithstanding consistent high economic growth in past decades, an economic study shows.

Foreign direct investment in Bangladesh has been on a prolonged slowdown with worrisome macroeconomic implications notwithstanding consistent high economic growth in past decades, an economic study shows.

The economic growth-FDI paradox is presented in a report on the study, titled 'Expanding private investment in Bangladesh in the context of LDC graduation', which has been submitted to finance ministry.

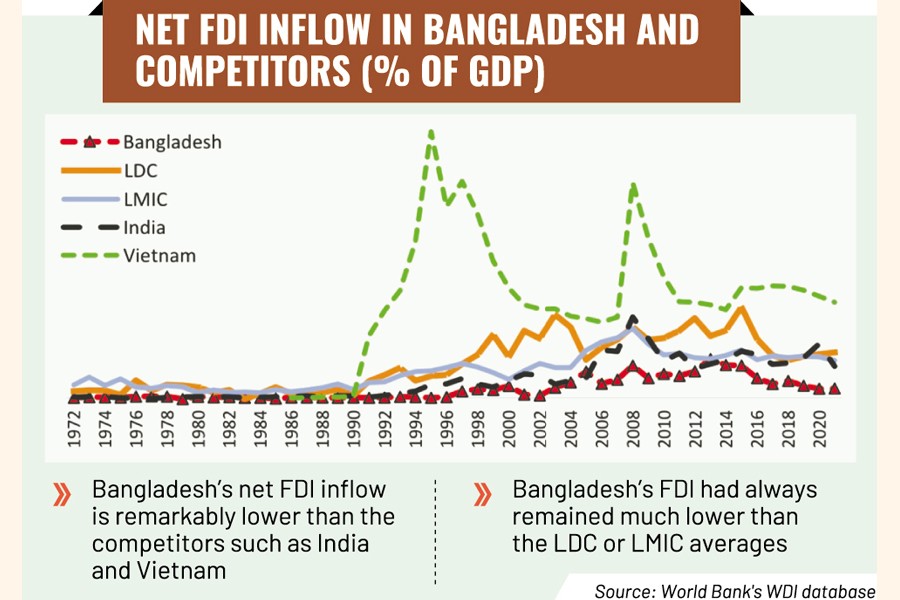

A copy of the report on the study, conducted by an economic think-tank, is obtained by the FE, which points out that since 1972 and until 2005, net FDI flow into Bangladesh always remained less than 1.0 per cent of gross domestic product (GDP).

And between 2005 and 2015, there had been a gradual, but slight, rise in the net inflows with a peak at 1.74 per cent in 2013.

Commenting on the macroeconomic parameter, Dr Selim Raihan of SANEM told the FE that raising FDI is a major challenge as Bangladesh is going to be a middle-income country.

"We are far below compared to our competitors in attracting FDI," says the economist running the South Asian Network on Economic Modeling (SANEM).

He notes that increase in FDI is crucial in offsetting the challenges stemming from critical BoP situation. "The establishment of so many EPZs will also be futile if we fail to attract FDI."

But, ever since 2013, net FDI inflow in Bangladesh has been on the decline, and in 2021, accounted for only 0.41 of the GDP of Bangladesh, the report says.

Comparing the country's FDI inflow with competitor countries, the study report says Bangladesh's net FDI inflow is remarkably lower than that of competitors on the trading front, like India and Vietnam.

The FDI in India or Vietnam had started accelerating since the early 1990s. "Nevertheless, Vietnam stands out as an exception in this context. In the mid-1990s, net FDI inflow in Vietnam stood as high as 12 per cent."

In contrast to Vietnam, FDI in India followed global trend and remained close to the Lower-Middle-Income Country (LMIC) average, the country group India belonged to. Since 2018, India had always been on a par with the LMIC average FDI inflow.

According to the study findings, in contrast to India and Vietnam, Bangladesh's FDI had always remained much lower than LDC or LMIC averages.

In 2021, the LDC average net FDI inflow stood at 2.0 per cent whereas the LMIC average 1.41 per cent of GDP.

"It clearly shows, on average, Bangladesh has not been as successful in attracting FDI as most other LDC or LMIC countries," the study says.

Referring to the views of business-insiders and industry experts, it says the low rates resulted from several factors in Bangladesh, including bureaucratic red tapes and inefficiencies, poor infrastructure, unreliable energy supply, corruption, lack of good governance, low labour productivity, underdeveloped money and capital markets, high cost of doing business, complex tax system, and frequent changes in policies.

"Additionally, Bangladesh currently does not have an investment-grade rating. Emerging-market countries seek investment-grade status to reduce sovereign financing costs, expand potential investors to include institutional investors, and provide corporations with the opportunity to reduce borrowing costs."

The current sovereign-credit ratings for Bangladesh are equivalent to speculative or junk bond ratings.

The most recent one from S&P lowered Bangladesh's long-term credit- rating outlook to be negative from stable.

This fall in credit rating is an outcome of the deteriorating external liquidity position of Bangladesh since 2022. Such falling credit rating adversely affects foreign direct-investment prospects in manufacturing or services sector.

About sectoral analysis of the FDI the study says in FY2021-22, the key sectors for inward FDI included power, gas and petroleum (22.3 per cent), RMG (20per cent), and the financial sector (17 per cent ).

While the volume of FDI in the country has increased for all these sectors, however, it is worth mentioning that FDI in new "thrust sectors" - such as electronics, light engineering, agro-processing, plastic and furniture, leather and leather goods etc-did not pick up.

Foreign investment in new and emerging manufacturing sectors exhibits 'transfer of technology', and 'spillover effects', and also produces 'supply-chain effects' creating self-sustaining sectoral growth momentum.

Bangladesh, therefore, would need a more reinvigorated approach to attracting FDI in the thrust sectors in the coming years, the study suggests.

According to the study, in terms of sources of FDI, the USA, China, the UK, Singapore and Korea tops the list.

Nevertheless, the sectoral FDI significantly varies from the source countries.

Almost 70 per cent of USA's total FDI stock is in the gas and petroleum industry.

In the case of the UK, the investments are higher in banking (51.3 per cent, apparel industry (20per cent), food processing (10.5per cent), and pharmaceuticals (6per cent).

Singapore's major investments are in power (24 per cent), telecommunications (17.3per cent), and apparel industries (8.5per cent).

South Korea is mostly engaged in the apparel industry (68per cent), leather (13.6per cent) and banking (9.3per cent).

Out of China's total FDI stock in Bangladesh, 51.3 per cent of the investments are in the power sector, followed by apparel (21per cent), and trading (9per cent). Amongst others, Netherlands and Malaysia are mostly engaged in the telecommunications industry, while the rest are mostly integrated into the apparel industry.

mirmostafiz@yahoo.com

© 2026 - All Rights with The Financial Express