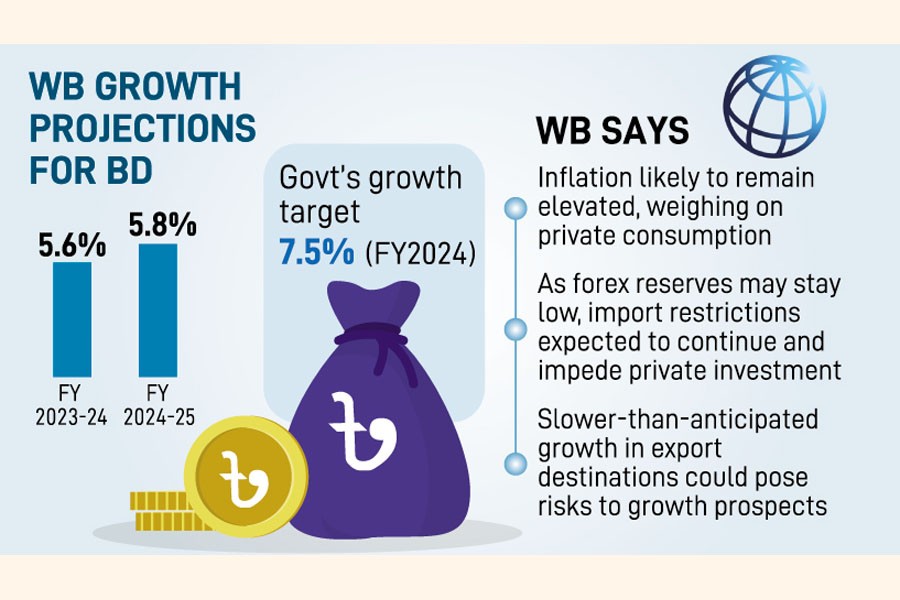

Bangladesh's economic growth may slow to 5.6 per cent in the current fiscal as the election ruckus has dampened private-sector activity, the World Bank (WB) says on the cusp of a new government taking over.

In its revised forecast, lowering the GDP growth by 0.6-percentage points from its June projection for the financial year (FY) 2023-24, the global lender also projects a lower growth at 5.8 per cent for the next fiscal.

The WB has presented such revised reckonings on state of Bangladesh economy in its six-month flagship report styled 'Global Economic Prospect (GEP)'. The report was released Wednesday from its headquarters.

For Bangladesh, it says, slower-than-anticipated growth in its export destinations, particularly in the European Union, "could pose a risk to growth prospects", in addition to domestic decelerators.

"The heightened uncertainty around these elections could dampen activity in the private sector, including foreign investment," the report adds in its opinion in an implicit reference to the poll-time problems stemming from boycotting opposition agitations.

The projected 5.6-percent gross domestic product (GDP) growth is 0.43-percentage-point lower than the 6.03 per cent achieved in the last FY2023, and 1.9-percentage-point down the government target at 7.5 per cent in the current FY2024.

Meanwhile, the Asian Development Bank (ADB) in December also had revised down Bangladesh's economic growth by 0.3-percentage points to 6.2 per cent for the current fiscal by citing much the same reasons-economic slowdown and uncertainties over the January election.

Yet another multilateral financier-the International Monetary Fund-followed suit as the IMF in October last year pared down growth forecast for the country to 6.0 per cent for the current FY2024--lower from its previous projection of 6.5 per cent.

"The growth in Bangladesh is forecast to slow to 5.6 percent in FY2024 (July 2023 to June 2024)," says the World Bank in its GEP update.

In such a low-growth milieu, inflation is likely to stay elevated, forex reserves low, and import restrictions to continue and impede private investment, it predicts about the challenges the incoming government inherits.

"Inflation is likely to remain elevated, weighing on private consumption. As foreign-exchange reserves are likely to stay low, import restrictions are expected to continue and impede private investment," the report reads.

"In contrast, public investment is envisaged to remain resilient. Growth is expected to rise in FY2025 as inflationary pressure recedes."

The World Bank focuses on spillover effects on the economic front from waves of elections in a number of countries across the world, including South Asia, in the current year 2024.

"In a number of South Asian Region (SAR) economies including Bangladesh, Bhutan, India, the Maldives, and Pakistan, parliamentary or national assembly elections are scheduled or planned in 2024. The heightened uncertainty around these elections could dampen activity in the private sector, including foreign investment," it notes.

"If combined with political or social unrest and elevated violence, this could further disrupt and weaken economic growth. In addition, particularly in countries with the weak fiscal positions, an increase in spending prior to these elections could exacerbate macro-fiscal vulnerabilities."

However, hopes for growth acceleration are pinned on post-poll peace and proper policy pursuit. The implementation of policies to reduce uncertainty and strengthen growth potential after elections could lead to an improvement in prospects.

The WB in its global forecasts makes a special mention of influence of economic giant China.

In countries where China is a major trading partner or key source of foreign investment, a sharper-than-expected slowdown in China could undermine growth, it says.

Meanwhile, the GDP growth in SAR is expected to edge marginally down from an estimated 5.7 per cent last year to 5.6 per cent in 2024-still the fastest pace among all emerging-market and developing-economy (EMDE) regions-and then firm to 5.9 per cent in 2025, the WB report says.

Growth in India is projected to remain strong, largely driven by robust investment and services. In other economies, the adverse effects of persistently high inflation and monetary-and fiscal- policy tightening, as well as policy uncertainty, will weigh on growth, it adds.

"Risks to the outlook are tilted to the downside, with the most pressing concerns being higher energy and food prices caused by the ongoing conflict in the Middle East and adverse spillovers from elevated policy rates in advanced economies."

Risks of financial and fiscal stress, extreme weather events, slowing activity in China, and election-related uncertainty in some countries pose further downside risks for the SA region, the WB notes in its report.

kabirhumayan10@gmail.com

© 2026 - All Rights with The Financial Express