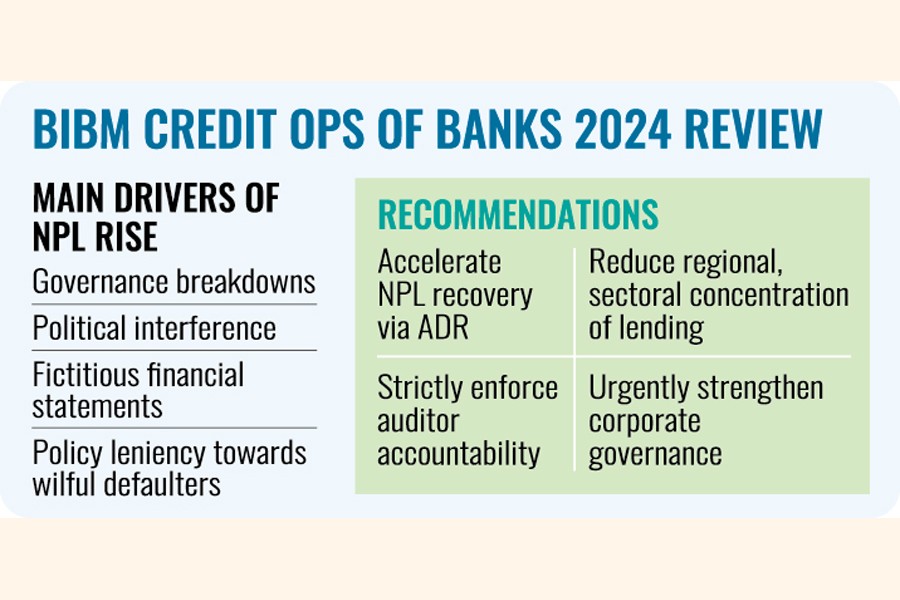

Governance breakdowns, political interference, fictitious financial statements, and policy leniency towards wilful defaulters are the primary drivers behind Bangladesh's record non-performing loans (NPLs), the Bangladesh Institute of Bank Management (BIBM) revealed on Monday at a high-profile review workshop on the country's banking sector.

The findings - presented at the BIBM's auditorium in Dhaka before senior bankers, regulators, and academics - came from its Credit Operations of Banks 2024 review.

The study revealed that NPLs surged to Tk 420.34 billion last year, with Tk 300.03 billion concentrated in just 10 banks.

The gross NPL ratio rose to 12.56 per cent in June 2024 from 10.11 per cent a year earlier, while state-owned commercial banks posted the highest level at 32.77 per cent.

Net NPLs at state-owned commercial banks nearly doubled to 18.32 per cent, underscoring the depth of the problem.

BIBM's review stressed that the roots of the crisis are "psycho-political" rather than merely economic.

Borrowers, particularly in state-run banks, often fail to repay because they anticipate repeated rescheduling, interest waivers, and extended repayment periods granted through policy favour, it said.

The report described an unhealthy corporate culture in certain banks, driven by greed, self-dealing, and inflated profit targets, which led to major scandals.

The problem has been worsened by fictitious balance sheets and poor audit oversight, which have masked the true extent of bad loans.

In some instances, the NPL ratio reported at year-end was 4 per cent, only to leap to 36 per cent in the following quarter after misreporting came to light.

The review found that financial statements provided to regulators have long been unreliable, misleading policymakers and investors alike.

The slow pace of loan recovery - especially in cases tied up in the Artha Rin Adalat and higher courts - remains a significant challenge.

The Bangladesh Bank (BB) has responded with a series of reforms, including the introduction of rules for identifying and penalising wilful defaulters, tighter loan classification norms, an asset quality review, and a plan to align loan provisioning with International Financial Reporting Standard (IFRS) 9 by 2027.

It also aims to set up an asset management company to manage and recover bad loans, and is pursuing the recovery of stolen assets domestically and abroad through dedicated task forces.

Beyond defaults, the report shows a weak private credit market, with growth at just 7.2 per cent in May 2025 - well short of the central bank's 9.8 per cent target - due to low business confidence, political instability, liquidity shortages, and heavy government borrowing crowding out private lending.

Credit distribution is highly concentrated, with Dhaka and Chattogram divisions receiving 86.49 per cent of loans in 2024 and rural areas only 8.16 per cent.

Large borrowers dominate the lending landscape, holding 43.81 per cent of total credit in accounts above Tk 200 million.

While some positive trends were noted - such as a 23 per cent growth in industrial term loans, particularly in service industries and cottage enterprises - agriculture, transport and consumer finance sectors experienced declines.

Sustainable finance nearly doubled to Tk 4.59 trillion, but the review warned that this progress would not counteract systemic weaknesses without a broader improvement in lending quality.

In its recommendations, the BIBM called for urgent strengthening of corporate governance to insulate banks from political influence and nepotism, and for strict enforcement of auditor accountability to prevent fictitious reporting.

It urged a reduction in the regional and sectoral concentration of lending, expansion of credit to rural areas, and more disciplined use of credit risk assessment tools, such as the Internal Credit Risk Rating System.

The review also stressed accelerating the recovery of default loans through alternative dispute resolution (ADR) and ensuring that sustainable finance growth is matched by strong credit discipline.

Opening the workshop, BIBM Executive Committee Chair and Bangladesh Bank Deputy Governor Ms Nurun Nahar emphasised that a sound credit system is essential for economic stability and growth.

Concluding the session, BIBM Director General SM Abdul Hakim said the findings should serve as a wake-up call.

"We have the tools, but without political will, transparency, and discipline in credit operations, the structural weaknesses in our banking sector will persist."

Speaking as the chief guest, Ms Nahar stressed the need for good governance in banks.

She also identified the lack of banking literacy among people as the key reason for the state of banks. Among others, Faruq M Ahmed, AK Gangopadhyay Chair Professor of BIBM; Md Ali Hossain Prodhania, Supernumerary Professor of BIBM; Kazi Md Wahidul Islam, Managing Director of Rupali Bank, spoke at the event.

bdsmile@gmail.com

© 2026 - All Rights with The Financial Express