The policy about management of capital market-related trust funds, in the nature of Mutual Funds (MFs) and unit funds, is spelt out under securities rules.

But this, according to some market-analysts, is not being properly adhered to, in the case of unit certificates of the government-owned Investment Corporation of Bangladesh (ICB) while fixing the surrender value.

Such analysts largely share the concern of many certificates-holders over the prevailing state of affairs about ICB Unit Fund (IUF).

Meanwhile, an open-ended fund, under the provisions of Section 51 (2) of Mutual Fund (MF) Rules, 2001, is to be wound up if more than 75 per cent of related holders surrender their units.

Besides, the securities market regulator or the trustees can take the decision about winding up of any such trust fund, if it becomes necessary, for the sake of upholding unit holders' interest.

According to some forward-looking market observers, the Bangladesh Securities & Exchange Commission (BSEC), the regulatory body for the country's capital market, can set a time-limit for winding up the long-running IUF of a hybrid type for ensuring consistency, uniformity and transparency of such a kind of MF.

The existing holders of ICB unit certificates should not also be deprived of their legitimate claims, they noted.

By setting a time-frame for winding up the IUF, the BSEC can consider giving the ICB a choice between letting their existing unit certificate-holders either to opt for any other new product or investment or encashing their existing units, both at actual NAV, they suggested.

Such a move, according to such observers, will help further deepen and widen they base of the country's capital market on some innovative lines. No investors' trust fund, whatever may be its kind, should be allowed to continue in perpetuity, they added.

The securities market watchdog, as competent sources and concerned quarters including the investors do strongly feel, can not keep its eyes shut to the operations of an unlisted security like that of IUF unit certificates that have some strong traits of being considered as a MF.

The existing holders of the certificates of the IUF should, on no logical ground, be deprived of the benefits of market-gains that belong to them, according to them.

However, the watchdog cannot also ignore the possible impact, positive or negative, of this security on the market, in the event of its unbundling or fixing a tenure for folding up of its operations, they added.

"The IUF is beyond our overall supervision. However, we will send a letter to the ICB for submitting the copy of the agreement under which the IUF was floated," one competent source within BSEC told this correspondent.

The BSEC source preferred not saying anything about the operation of the IUF or commenting on the ICB's policy about fixation of the 'surrender value' of the IUF's units.

The officials of the BSEC's concerned department said the ICB do not give annual fees for the IUF.

For the ICB, the hard matters of consequence, according to relevant sources, remain to be: ensuring dividend -- either in cash or in the form of new 'unlisted' units or certificates -- at a higher rate, however modest it may be -- in every successive year to their existing holders, avoiding thereby a 'too heavy' one-time load on its financial operations.

A strong fear, meanwhile, persists among the concerned ICB personnel about market destability, in the event of any large scale 'surrender' of its only 'flagship security' by its holders for reaping 'market' or 'capital' gains.

On its part, the ICB has otherwise an impressive track-record, largely through its subsidiaries, of being quite proactive, some close observers of the market noted.

It has been playing a 'all-weather' supportive role for ensuring both stability and liquidity, particularly in times of adversities of the market, they added.

A member of the relevant committee of the ICB, meant to set the NAV and fix surrender value of the units of the IUF, claimed that the surrender value or repurchase rate of its unit certificates is fixed by evaluating the NAV, period of holding units and some other circumstances as well.

Asked, whether the unit holders who are willing to surrender units are being deprived of 'due' benefits, the member said this issue is a matter of perception.

"However, the surrender value is periodically fixed to encourage long-term investment and to ensure higher rate of dividend on a steady and sustained basis," he told the FE, asking not to be named.

ICB managing director Md. Fayekuzzaman said they manage the IUF in a balanced way.

"Tendency of surrendering units may be triggered if the re-purchase rate is fixed in an imbalanced way. This will also have adverse knock-on effects on the capital market," Mr. Fayekuzzaman observed.

The IUF, he said, plays an important role in promoting industrialisation and also developing the capital market, while providing a reasonable rate of return to the unit-holders on a sustainable basis.

Meanwhile, the job of the auditors -- K. M. Alam & Co and Rahman Mostafa Alam & Co -- that have been appointed to audit the financial statements of the IUF, is mainly to examine statements of its assets, liabilities and profits while authenticating the financial statements, according to sources.

"I think the ICB fixes the surrender value or repurchase rate, as per the conditions set under an earlier agreement," said an auditor requesting for anonymity.

The ICB charges Tk 1.25 per unit (net outstanding) as management fees. It is also the custodian of all assets of the fund.

The ICB realised about Tk 91.42 million and Tk 149.98 million as management fees for the year that ended on June 30, 2013 and on June 30, 2014, respectively. It also received custodial fees worth above Tk 16.73 million for the year that ended on June 30, 2014.

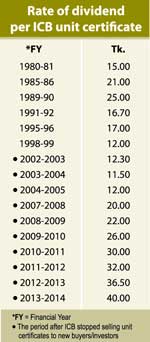

The dividend rate on every unit of the IUF was Tk 22.00 in the financial year (FY), 2008-09, Tk 26.00 in FY 2009-10, Tk 30 in FY 2010-11, Tk 32.00 in FY 2011-12, Tk 36.50 in FY 2012-13 and Tk 40 in FY 2013-14.

In FY 2012-13 and FY 2013-14, fresh units under the CIP that were issued stood, in value terms, at Tk 799.9 million and above Tk 1.01 billion respectively.

Two years back, the ICB introduced 'nominee system' among family members, only to avoid difficulties, consequent upon the death of any or of the unit-certificate holders.

Asked, whether the IUF is an open-ended trust fund or not, ICB managing director Mr. Fayekuzzaman said in the sense of a MF, the IUF cannot be called an open-ended one as only the existing unit-holders are allowed to receive new units or sell their existing ones.

mufazzal.fe@gmail.com

© 2026 - All Rights with The Financial Express