Agent banking in Bangladesh witnessed significant year-on-year growth in November 2024 in terms of both loan disbursement and deposit collection, despite a decline in the number of agents and outlets.

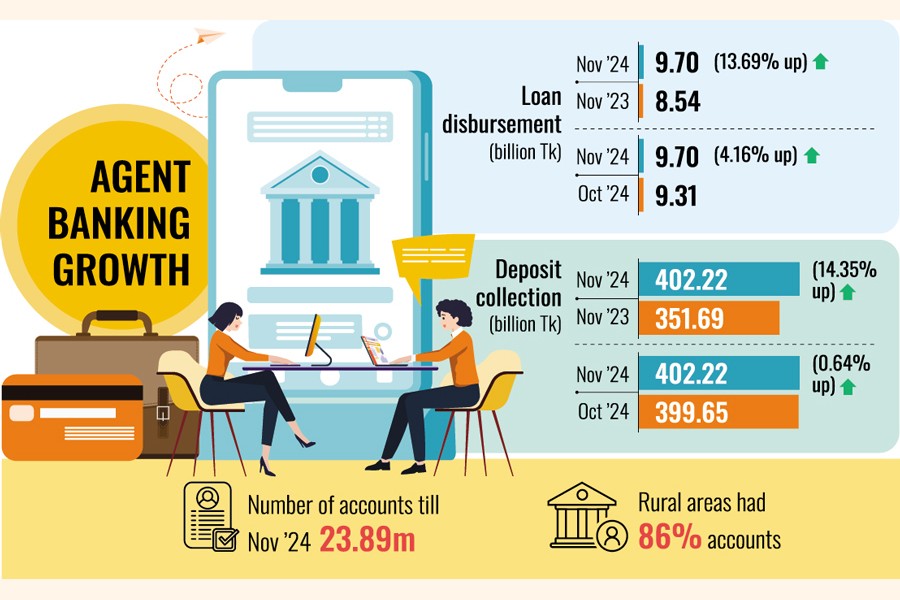

According to the Bangladesh Bank (BB) data, loan disbursement reached Tk 9.70 billion in November 2024, up 13.69 per cent from Tk 8.54 billion in the same month a year before.

On the other hand, deposit collection rose to Tk 402.22 billion, marking a 14.35 per cent increase from Tk 351.69 billion in November 2023.

This steady rise in financial activities highlights the growing acceptance and utilisation of agent banking

services, particularly in rural areas where 86 per cent of the accounts are concentrated.

The data reveals that agent banking is playing an increasingly vital role in bringing banking services to the underserved communities. Till November 2024, the total number of accounts under agent banking stood at 23.89 million.

Despite the decrease in agents (six fewer) and outlets (seven fewer) compared to October 2024, deposit growth remained steady, with a 0.64 per cent month-on-month increase from Tk 399.65 billion in October to Tk 402.22 billion in November.

Loan disbursement also showed consistent growth over the months, reflecting a rising demand for credit in rural areas. From January to November 2024, loan disbursement exhibited a steady upward trend, starting at Tk 7.73 billion in January and peaking at Tk 9.70 billion in November.

This growth contrasted sharply with the November 2023 disbursement figure of Tk 8.54 billion, underlining a year-on-year increase of Tk 1.16 billion.

While the year-on-year growth paints a positive picture, the month-on-month variations highlight interesting patterns. For instance, loan disbursement in November 2024 rose by 4.16 per cent from October's Tk 9.31 billion.

This increase follows a similar trend observed in the preceding months, with September registering Tk 8.55 billion and July recording Tk 6.26 billion, the lowest figure of the year.

Deposit collection, while stable, also showed monthly variations. The November figure of Tk 402.22 billion marked a slight increase from Tk 399.65 billion in October. However, seasonal dips were evident in months like April (Tk 369.46 billion) and February (Tk 362.38 billion).

Experts attribute these fluctuations to cyclical economic activities, including agricultural harvests and festivals, which affect both savings and borrowing patterns.

They see the year-on-year growth in agent banking as a testament to its potential for financial inclusion.

Dr M Masrur Reaz, chairman of Policy Exchange of Bangladesh, said the growth in loan disbursement and deposit collection under agent banking reflects a deepening penetration of financial services in the rural economy.

"This is significant for an economy like Bangladesh, where rural and peri-urban households and firms often lack access to formal banking channels," he told The Financial Express.

However, he cautioned about the declining number of agents and outlets. "While the financial performance is impressive, the reduction in agents and outlets raises concerns about sustainability. Policymakers and banks need to focus on incentivising agents to ensure the network's expansion rather than contraction."

Reaz emphasised the role of agent banking in driving rural entrepreneurship and expanding the economy's formalisation.

"The rising demand for credit in rural areas indicates a surge in small business activities. Agent banking is bridging the gap by offering access to credit where traditional banks are absent," he noted.

Despite its achievements, agent banking faces several challenges, including the declining number of agents and outlets. Experts warn that without adequate incentives and support, banks may struggle to maintain their agent networks.

Additionally, regulatory oversight is crucial to prevent misuse of the system, especially in loan disbursement and deposit mobilisation.

To ensure sustained growth, experts recommend targeted policies to encourage banks to expand their agent networks, especially in underserved regions. Digitalisation and training programmes for agents can also enhance efficiency and customer trust.

The agent banking model ensures real-time banking for customers at agent points, providing services equivalent to those at the main branch. Only for the sake of additional security, work is done at the agent point using biometric devices, meaning everyone has to operate by providing their fingerprints. Fingerprint verification is mandatory when opening a primary bank account.

Individuals can open an account at an agent point or access various services if they already have an account at another branch. This includes activities such as withdrawing and depositing money, remittance, and transferring funds between different bank accounts, both within the same bank and across others.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express