Local think-tank Centre for Policy Dialogue (CPD) finds Bangladesh's latest monetary policy deficient on many counts, including job and income generation in this crisis time, and says it is unlikely to help steer the economy through the headwind.

"The monetary policy statement (MPS) is not supportive of the moves necessary to address the existing challenges," said Dr Fahmida Khatun, executive director at the CPD.

In their view all monetary aggregates now remained downwards except for remittance inflow.

The private-sector credit target for the current fiscal year is not realistic. "This [unrealistic target] will not help generate employment and incomes for the people," she told the press in explaining salient features of the MPS rolled out by the central bank last week.

Dr Khatun, however, stressed quick repayment of loans disbursed by banks under the stimulus packages by the big corporate houses in order to lower the ballooning NPLs (non-performing loans) the banking sector is heaving under.

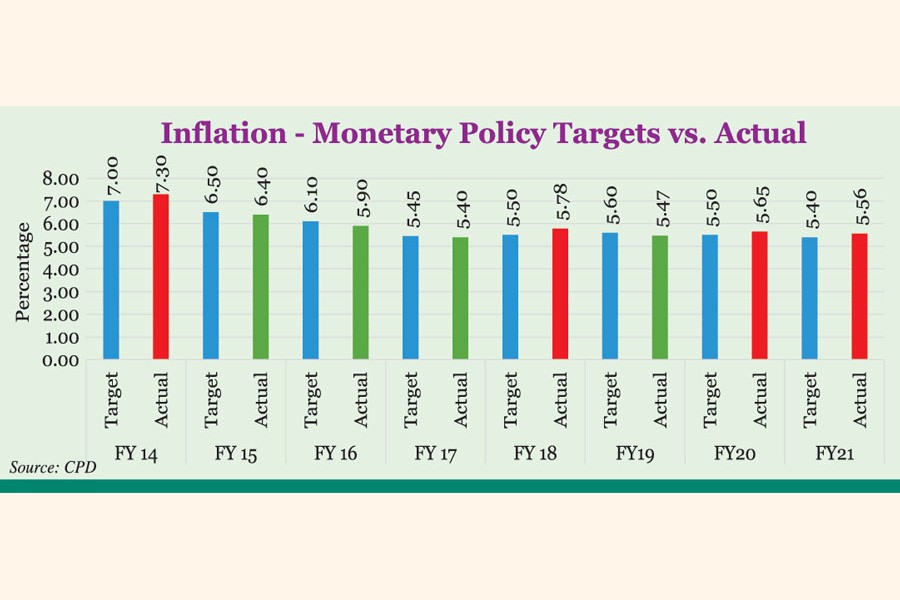

Inflation targets should be practical, based on a 16-year-old consumption basket, she said, as living is getting costlier.

"The rate of inflation now remains above the target," the economist said, adding that the cost of living has increased manifold.

The policy advocacy came up with the observations on the economic front at a programme styled 'CPD's Reaction on MPS Fiscal Year 2021-22: To What Extent Monetary Policy Meets the Needs of the Economy' held Tuesday on virtual platform.

Dr Fahmida Khatun made a presentation on the topic, touching on major sectors of life and economy during the pandemic.

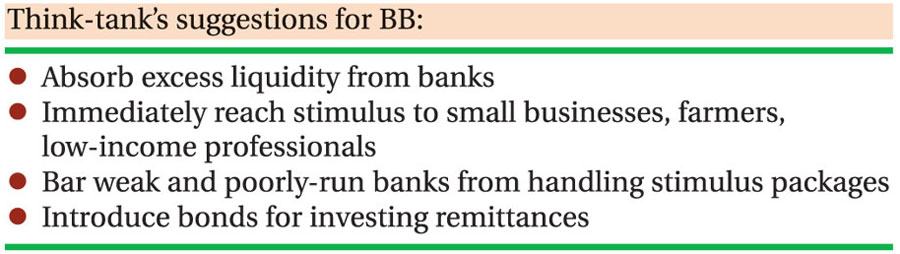

While presenting the keynote she said the central bank has refrained from taking any active step in reducing the liquidity glut in the banking system, but has assured that it will not hesitate to act if the need arises.

The CPD suggests the central bank may increase the cash-reserve ratio in order to dilute the excess liquidity in the economy.

Replying to a volley of questions relating to high inflow of remittance, Dr Khatun said the government may consider withdrawing the cash incentive [2.0 per cent] now being given on the remittances.

Professor Dr Mustafizur Rahman, one of CPD's distinguished fellows, said that the government may create bonds to ensure optimal use of the remittance inflow.

"Actually we need to diversify instruments and bond creation may be an ideal one for using higher inflow of the remittances," Dr Rahman said.

He said there are many mega-projects in the country and that the government may utilise the funds.

Replying to another question relating to poor investment in the country, Dr Rahman said investment does not depend merely on the physical infrastructures.

"Service delivery, one-stop service and a good business environment usually help attract investment".

He said: "Economic zones are necessary conditions to this end [investment attractions], but it does not ensure sufficient conditions to attract investment."

Dr Rahman mentioned that many digital platforms, including bKash, were showing interest in disbursing funds. Under such new cases the existing interest rate should be hiked, he suggests.

Replying to a question on fund diversion towards the capital market, CPD director (research) Dr Khondaker Golam Moazzem said the capital-market regulator should ensure transparency of the BO [beneficiary owner] accounts.

In the think-tank's view, governance of the banking sector will be an important determinant for better recovery of the economy, which suffers shocks from the pandemic that has disrupted trade and business across the globe.

"Unfortunately, reforms in the banking sector remain outside the radar of the central bank at present," it noted.

The other recommendations are: (1) loan defaulters should not be allowed to access any of the covid-related liquidity-support packages; (2) weak and poorly governed banks should be barred from participating in the covid-time liquidity-support packages; (3) banks which are not fully compliant with BASEL III or the Banking Company Act should not be allowed in the liquidity-bailout packages; and (4) clear, objective, and quantitative criteria should be declared to properly identify 'affected' businesses and individuals.

It would also like to see transparency and accountability mechanisms built into all COVID-related liquidity-support packages, and more disaggregated data on the implementation status of all such stimulus dollops published on a monthly basis.

"Disbursement of government's COVID-19-liquidity support for small businesses, farmers, and low-income professionals should be expedited immediately," the policy advocacy feels.

jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express