Despite its immense potential, the once-economically vibrant Barishal division has become least-focused region in the country in terms of banking services availability.

Even during the British regime, the region was considered one of the economically important areas of Bengal due to its fertile land resources and water connectivity.

However, things started to deteriorate with the emergence of road connectivity-driven economic dominance and the coastal region continued losing its shine over the years.

Now, the coastal region, spanning 13,295 square kilometres and comprising six districts since its establishment as a division in 1993, has become the worst victim of regional disparity in terms of banking network, deposit collections and loans and advances distributed by commercial banks.

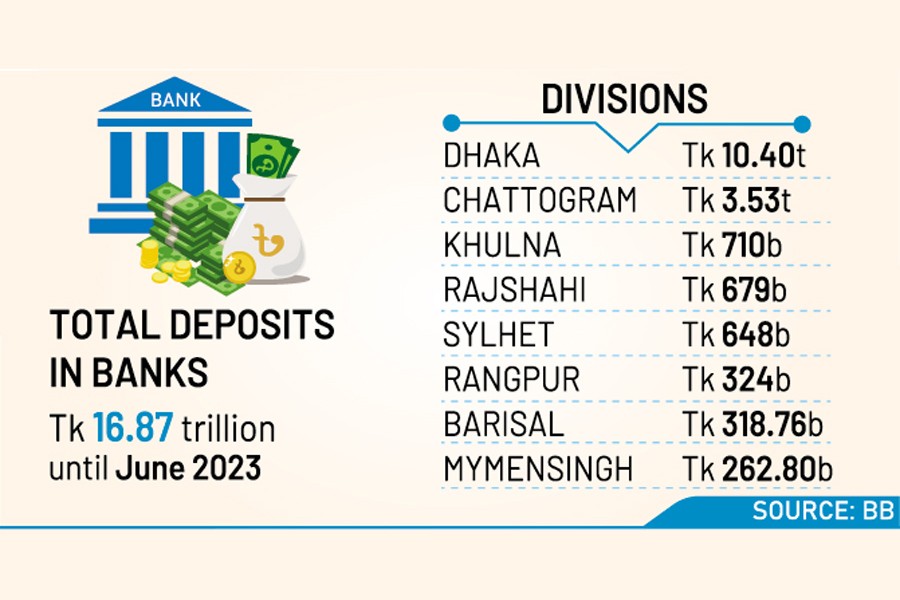

According to Bangladesh Bank (BB) statistics, the total deposits in the banking industry reached Tk 16.87 trillion until June 2023, with Dhaka division contributing the highest share of 61.66 per cent, or Tk 10.40 trillion, of the entire deposit portfolio in the banking sector.

This was followed by Chattogram (Tk 3.53 trillion), Khulna (Tk 710 billion), Rajshahi (Tk 679 billion), Sylhet (Tk 648 billion) and Rangpur (Tk 324 billion).

Barishal has become a region with the second-lowest deposit volume at Tk 318.76 billion, following the recently formed Mymensingh division with Tk 262.80 billion.

The scheduled banks across the country provided loans and advances amounting to Tk 14.46 trillion as of June 2023.

The Barisal region received the lowest volume of formal credits, with only Tk 174 billion, while bank investments in other regions were as follows: Dhaka (Tk 9.81 trillion), Chattogram (Tk 2.54 trillion), Rajshahi (Tk 610 billion), Khulna (Tk 573 billion), Rangpur (Tk 376 billion), Mymensingh (Tk 199 billion), and Sylhet (Tk 176 billion).

In terms of the banking network, there are a total of 563 out of 11,177 branches located in Barisal, which is the second-lowest number after the administrative bloc of four districts in the Mymensingh region, which has 467 bank outlets.

Speaking on condition of anonymity, a Bangladesh Bank official said that although Barisal contributes the second-lowest regional deposits after Mymensingh, the ratio of loans and advances to deposits is much lower in Barisal compared to that of Mymensingh.

"The investment-to-deposit ratio in Barisal is 0.55 per cent, while it is 0.76 per cent in Mymensingh," the official said.

Explaining further, the central banker said the banks collected deposits amounting to Tk 318.76 billion from Barisal, but they invested only Tk 174 billion. On the other hand, banks gave Tk 199 billion in loans to Mymensingh, but the region contributed Tk 263 billion in deposits to the banks.

"Barisal people are not getting even 60 per cent of their deposits. Is it logical?" the BB official questioned.

While talking to the FE, President of Barisal Metropolitan Chamber of Commerce and Industry (BMCCI) Mohammad Nizam Uddin said the entrepreneurs in the region have been severely suffering due to poor access to formal credits over the years.

"We keep requesting the higher bank officials about the pains, but nobody listens to us even though entrepreneurs have all the documents required for getting funds. I don't know why the bankers are so shy in giving credit," he said with frustration.

"There is a saying that transferring bank officials to Barisal is a kind of punishment, like the hill districts. And entrepreneurs are getting demoralised for not receiving the bank finance, which is the key to industrial and employment growth," the business leader said.

The country's longest Padma Multipurpose Bridge -- which connects the southern districts with other parts of the country by road -- opened last year, providing a ray of hope for the business communities in the coastal region. However, two major bottlenecks -- red tape and the silence of banks -- have started shattering their hopes, according to him.

The immediate-past Barisal divisional commissioner, Md Amin Ul Ahsan, who is now attached to the cabinet division, said the number of marginalised people in Barisal is quite high and agriculture is the main economic activity for this group.

The majority of the land in the region is single-crop land and problems like submergence and salinity affect the farmers there. As a result, crop diversity is not taking place in the region. "These are probably a few factors discouraging the bankers from focusing more in the area," he said.

When contacted, Managing Director and Chief Executive Officer of Mutual Trust Bank (MTB) Limited Syed Mahbubur Rahman said Barisal was not a priority area for banks due to poor infrastructure, lack of industrialisation and lower per-capita income of the people there.

"So, banks cannot show the courage to invest in such areas with insufficient development activities," he said.

However, things are believed to be improving in the coming days due to the opening of the Padma Bridge, which will help facilitate industrial growth, employment opportunities and other basic facilities. "If it happens, banks will pay more attention to the least-developed areas. I think people will have access to a lot of things in the coming days," he added.

He said Barisal is one of the areas where the volume of non-performing loans (NPLs) is quite high, which might also discourage banks from paying more attention to the area.

Talking about the issue, former lead economist at the World Bank's Dhaka Office Dr Zahid Hussain said Barisal is one of the poorest regions in the country where people earn much less than in other parts of the country.

"That's why financial institutions are not going there. As the lenders are not going, people are finding it hard to escape poverty," he said.

If road connectivity, along with other facilities like gas, power, health and education, are ensured with the support of the Padma Bridge, banking penetration is surely improve by a large margin, the economist said.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express