The operational and management aspects of the longest-running - now over 33-year old since its launch in April 1981 -- unit certificate scheme of the state-owned Investment Corporation of Bangladesh (ICB) have raised a lot of questions.

The questions revolve around its character, tenure, mismatch between repurchase rate -- the rate which the ICB offers when its holders surrender the same for encashment -- and real net asset value (NAV) -- that are not made public -- amid a striking difference between the two and the investors' deprivation of the actual market gains of the securities that are held in the portfolio of assets against such unit certificates.

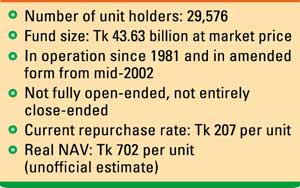

The number of unit holders of the ICB Unit Fund (IUF), according to data available in the annual report of the ICB, stood at 29,576 as on June 30, 2014. Among such holders, the majority belong to the mid-segment of the middle income groups -- retired and serving public and private sector employees.

The IUF, as the data in the ICB's latest annual report shows, is sized at plus Tk 43.61 billion at market prices of its portfolio, as on October 30, 2014.

But a good number of such unit certificate-holders as well as many market analysts and observers have doubts, on real or perceived grounds, over this figure. They are sceptical over the transparency and accuracy of accounting methods about the IUF.

Unlike other mutual funds (MFs) - the type of securities that the IUF can otherwise be likened to, the ICB does not make the real NAV public.

The repurchase value of one unit certificate that was fixed last week by the ICB's relevant committee for management and operations of the IUF was set at Tk 207.

But the 'real' net asset value (NAV), according to some insiders, of one such certificate is estimated at Tk 702 at current market prices of the listed securities in the portfolio of the IUF.

A unit holder, however, receives the value of his/her unit certificates, if he/she surrenders the same for encashment, at the 'repurchase' rate, fixed by the ICB from time to time, notwithstanding what the real NAV per unit of the IUF is.

This, according to some knowledgeable circles, tentamounts to denial of benefits that an individual unit certificate-holder is otherwise entitled to receive, rightfully or legally. This denial is morally and ethically unacceptable because it concerns the activities of a government-owned entity in the country's capital market, they observed.

The IUF was sponsored by the parastatal, initially with the objectives of mobilising savings through sales of its units to small investors, channelising the fund for supporting investment activities through marketable securities and also ensuring attractive rates of dividend as well as the benefits of market gains at the time of surrender or sale of such certificates.

The Asian Development Bank (ADB) as part of conditions of its assistance for development of the country's capital market in the second half of the 1990s, following the first stock market crash in 1996, debarred the ICB from carrying out new operations (sales) of unit certificates.

At such, the ICB now manages the operations of its unit certificate scheme only for those who were holding them at the time of discontinuation of selling units to any new investor or buyer -- on July 1, 2002.

The actual or real asset valuation of the portfolio of the ICB's IUF, according to market analysts and observers, should follow the standard accounting rules and practices as are applied in the case of MFs.

'Mark to market' can be a better approach to doing that but it is not possible to do that under the present circumstances as the IUF, unlike the practice in many comparator countries, is not a listed security, they noted.

The ICB-managed unit certificates lost one basic and essential character of their counterparts elsewhere, as being an open-ended one as far back as in mid-2002, according to most market analysts and observers.

Only those who are holding such certificates under Cumulative Investment Plan (CIP) are now issued new certificates, following annual declaration of dividend at year-end.

From this angle, this, as the competent sources added, is a partly "open-ended" scheme. Existing holders other than those under CIP receive cash dividends annually, upon their declaration.

The 'hybrid' nature of existing ICB unit certificates, the sources further pointed out, make them somewhat different from the Mutual Funds (MFs) that are close-ended types and listed with the stock exchanges where their market price is set by the interplay of demand-and-supply factors.

However, both unit certificates under IUFs and MFs are essentially trust funds and asset portfolios of both, whether listed or not, belong only to their holders, the sources said.

Their managers or issuers can only charge management fees for handling the matters of their portfolios with due diligence and proper judgment, they added.

mufazzal.fe@gmail.com

© 2026 - All Rights with The Financial Express