Consumer lending in the country's banking sector continued its upward trajectory in the January-March quarter of FY26, with outstanding loans surpassing Tk 1.58 trillion despite elevated lending rates and persistent inflation.

The steady increase indicates that households are increasingly relying on bank financing to meet housing, education, healthcare and other personal expenses as rising living costs continue to strain purchasing power.

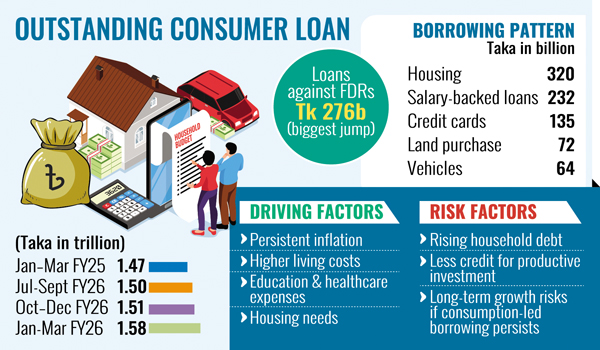

According to the latest Bangladesh Bank (BB) data, outstanding consumer loans climbed to more than Tk 1.58 trillion during the January-March quarter, up from Tk 1.51 trillion in the October-December quarter and Tk 1.50 trillion in the July-September quarter of FY26.

The figure was also higher than Tk 1.47 trillion recorded in the same quarter of FY25. The quarter-on-quarter growth was driven mainly by higher borrowing for housing, salary-backed loans, credit cards, land purchases and other personal financing.

Loans for purchasing flats and apartments increased to Tk 320 billion in the January-March quarter from Tk 310.85 billion in the previous quarter, while outstanding salary-backed loans rose to Tk 232.35 billion from Tk 225.95 billion.

Credit card loans climbed to Tk 135.19 billion from Tk 131.03 billion, while loans for land purchases increased to Tk 71.81 billion from Tk 69.36 billion. Financing for motor vehicles and motorcycles also rose to Tk 63.74 billion from Tk 60.85 billion.

One of the sharpest increases was recorded in personal loans secured against fixed deposits and other savings instruments, which jumped to Tk 276.25 billion from Tk 225.91 billion.

Doctors' and professional loans edged up to Tk 10.63 billion from Tk 10.38 billion, while loans against provident funds rose to Tk 18.87 billion from Tk 17.50 billion. Other personal loans also increased to Tk 30.66 billion from Tk 29.90 billion.

However, financing for household appliances, including televisions, refrigerators and computers, declined slightly to Tk 345.35 billion from Tk 346.62 billion.

Bankers said consumer loans are increasingly being used to finance essential spending rather than discretionary purchases, as many households seek credit to cover education, healthcare, marriage, travel and other day-to-day expenses amid persistent inflation and erosion of purchasing power.

They also noted that banks have expanded their consumer lending portfolios as demand remains resilient despite relatively high lending rates.

Arif Hossain Khan, spokesperson for Bangladesh Bank, said rising consumer demand for small-ticket financing, coupled with aggressive promotional campaigns by banks, has contributed to the continued growth in consumer lending.

"Banks have faced challenges in expanding corporate lending amid weak private-sector investment and rising credit risks. As a result, many lenders are increasingly focusing on consumer finance, which offers relatively quicker loan disbursement and diversification of their credit portfolio," he said.

Syed Mahbubur Rahman, managing director and CEO of Mutual Trust Bank PLC, said rising living costs and persistent inflation were prompting more people to rely on consumer loans to meet everyday expenses.

Banks are also diversifying their loan portfolios by expanding consumer lending as private-sector credit growth had remained below 5.0 per cent amid weak demand for business loans, Rahman said, adding that at the same time, lenders have stepped up promotional activities to attract retail borrowers.

Mutual Trust Bank alone disbursed around Tk 1.0 billion in consumer loans over the past three months, reflecting growing demand for such financing, he added.

Economists, however, warned that while consumer credit can provide short-term financial relief to households, excessive reliance on borrowing could increase debt burdens and financial vulnerability over time.

They also cautioned that if a growing share of bank lending continues to flow into consumption rather than productive sectors, it could undermine private investment, employment generation and long-term economic growth.

Dr Masrur Reaz, chairman of Policy Exchange Bangladesh, said the continued growth in consumer lending suggests many households are increasingly relying on bank borrowing to cope with rising living costs rather than finance discretionary spending.

"Inflation has eroded purchasing power, prompting consumers to borrow for essential expenses such as education, healthcare and housing," he said.

While consumer credit can support domestic demand in the short term, excessive dependence on such borrowing could increase household debt and financial vulnerability if income growth fails to keep pace, he added.

Dr Reaz said banks should ensure credit expansion remains balanced by directing a larger share of lending to productive sectors to stimulate private investment, create jobs and sustain long-term economic growth.

Otherwise, an economy driven mainly by consumption-led credit may not be sustainable, he added.

He suggested that lenders should strengthen their credit assessment and risk management, warning that high interest rates and weak economic conditions could affect borrowers' repayment capacity in the coming months.

sajibur@gmail.com

© 2026 - All Rights with The Financial Express